© FECAP

DOI: 10.7819/rbgn.v16i52.1865

Subject Area: Finance and Economics

RBGN

Behavioral Finance in Brazil: applying the prospect theory to potential

investors

Finanças Comportamentais no Brasil: uma aplicação da teoria da perspectiva em

potenciais investidores

Finanzas comportamentales en Brasil: aplicación de la teoría de la perspectiva a

los inversores potenciales

Claudia Emiko Yoshinaga1 hiago Borges Ramalho2

Received on January 14, 2014 / Approved on November 11, 2014 Responsible editor: João Maurício Gama Boaventura, Dr.

Evaluation process: Double Blind Review

1. Doctor in Management with focus on Finances from University of São Paulo (USP) [[email protected]] 2. Master in Management with focus on Finances from FECAP [[email protected]]

Authors’ address: FECAP University Center

Avenida da Liberdade, 532 – CEP: 01502-001 – São Paulo – SP – Brazil

ABSTRACT

he premise of unbounded rationality defended by the Eicient Market Hypothesis is challenged by the theoretical framework that involves Behavioral Finance, whose basis, Kahneman and Tversky’s Prospect heory (1979), questions the Expected Utility heory, an important element of Neoclassical Economics, as basis for decision-making. This research aims to replicate the empirical research of Kahneman and Tversky’s seminal article (1979) to evaluate the decision-making process of employees (potential investors) from a major national inancial institution. he results of this study were compared to those obtained in the original article and to other similar studies. The questionnaire employed

that both age and level of income were negatively related to total violations.

Keywords: Prospect theory. Heuristics. Cognitive

biases. Decision-making process. Investor characteristics.

RESUMO

A premissa de racionalidade ilimitada preconizada pela Hipótese dos Mercados Eficientes é contestada como ferramenta para tomada de decisões pelo arcabouço teórico que envolve as Finanças Comportamentais, cuja base, a Teoria da Perspectiva de Kahneman e Tversky (1979), questiona o que prediz a Teoria da Utilidade Esperada, importante elemento da Economia Neoclássica. A presente pesquisa objetiva replicar a investigação empírica do artigo seminal de Kahneman e Tversky (1979) para avaliar o processo decisório de funcionários (potenciais investidores) de uma importante instituição inanceira nacional. Os resultados deste estudo foram comparados aos obtidos no trabalho original e em pesquisas similares. O questionário adotado foi uma adaptação do originalmente utilizado, para que se pudesse testar, na amostra estudada, a aplicabilidade da Teoria da Perspectiva, mais especiicamente no que diz respeito aos Efeitos Certeza, Relexão e Isolamento. Foram analisadas, ainda, as diferenças no comportamento frente à tomada de decisões considerando os peris demográicos dos respondentes (gênero, idade e renda). Os resultados obtidos conirmaram a presença dos efeitos e comprovaram que uma grande parcela do público amostral apresentou efetiva inconsistência em suas escolhas segundo os fundamentos da Teoria da Utilidade Esperada, o que indica que suas decisões não foram tomadas de forma estritamente racional. Como contribuição, foi analisado se as violações estão relacionadas a características dos investidores, por meio de um modelo de regressão linear. Os resultados indicam que, em relação aos peris, idade e renda apresentaram relação negativa com o total de violações.

Palavras-chave: Teoria do prospecto.Heurís-ticas. Vieses cognitivos. Processo decisório. Características dos investidores.

RESUMEN

La premisa de la racionalidad ilimitada defendida por la hipótesis del mercado eiciente se contempla como una herramienta para la toma de decisiones en el marco teórico que implica el comportamiento inanciero, cuya base, la teoría de la perspectiva de Kahneman y Tversky (1979), cuestiona la teoría que predice la utilidad esperada, un elemento importante de la economía neoclásica. Esta investigación tiene como objetivo replicar la investigación empírica del artículo seminal para evaluar el proceso de toma de decisiones de los trabajadores (potenciales inversionistas) de una institución inanciera nacional importante. Los resultados de este estudio se compararon con los obtenidos en la obra original y los estudios similares. El cuestionario utilizado fue una adaptación del utilizado originalmente, para que se pudiera probar, en nuestra muestra, la aplicabilidad de la teoría de la perspectiva, más especíicamente en lo que respecta a los efectos certeza, relexión y aislamiento. Se analizaron también las diferencias de comportamiento en la toma de decisiones teniendo en cuenta los periles demográicos de los entrevistados. Los resultados confirmaron la presencia de los efectos y demostraron que una gran parte de la muestra pública mostró inconsistencia efectiva en sus decisiones, de acuerdo a los principios de la teoría de utilidad esperada, lo que indica que sus decisiones no fueron tomadas de manera estrictamente racional. Como contribución, analizamos si los incumplimientos están relacionados con las características de los inversores a través de un modelo de regresión lineal. Los resultados indican que, en relación con el peril, la edad y los ingresos mostraron una relación negativa con los incumplimientos totales.

Palabras clave: Teoría de la perspectiva. Heurística. Sesgos cognitivos. Proceso de toma de decisiones. Características de los inversores.

1 INTRODUCTION

of Neoclassical Economic Theory, assumes that economic subjects make decisions with unlimited rationality, present risk aversion and aim to maximize expected utility at every decision made. However, Simon (1955) was already critical of the current paradigm, claiming that people’s decision-making processes are based on limits to rationality, paving the way for the emergence of a new and promising ield of study in inance, later known as Behavioral Finance.

Behavioral Finance challenged the Eicient Market Hypothesis (EMH), based on the belief that economic subjects do not make strictly rational decisions and that there are limits to the role of so-called rational arbitrageurs. Two of its main theorists, Daniel Kahneman and Amos Tversky, concluded – in research carried

out in the 1970s – that decisions are made with the use of heuristics (simpliied decision-making processes) that are subject to systematic errors (cognitive biases).

Considering, then, that the EMH has not been suicient to explain people’s decision-making behavior, the theoretical scope involving Behavioral Finance, based on the development of Kahneman and Tversky’s Prospect heory (1979), signals that it is able to ill the gap left by Modern Finance heory with regard to understanding phenomena that clash with the rational model.

Regarding the applicability of the Prospect heory, several studies have been carried out, but with few sample variations, mostly made up of students, as summarized in Chart 1:

CHART 1 – Studies that replicated the original questionnaire by Kahneman and Tversky (1979) Authors Year Sample (public) Sample Conclusion (summary)

Kahneman and Tversky (original) 1979

Israeli, North-American and Swedish students and professors

66 to 141 Development of the Prospect heory, facing the presence of Certainty, Relection and Isolation Efects.

Kimura, Basso

and Krauter 2006

University students

and professors 97 to 189

Results are similar to those obtained by original research (despite certain diferences in terms of statistical signiicance), suggesting that behavioral aspects in decision-making remain over time and are little inluenced by possible cultural biases.

Rogers et al. 2007 Graduate students 114

Corroborates the inluence of behavioral aspects and the low inluence of cultural biases on decision-making. Also ratiies the presence of Certainty, Relection and Isolation Efects.

Lemenhe 2007 Graduate students 601

Concludes that there are preferences explained by the Expected Utility heory and that there are preferences explained by the Prospect heory and that there are preferences that are not explained by the Expected Utility heory nor by the Prospect heory.

Rogers, Favato

and Securato 2008 Graduate students 186

Results obtained conirmed the presence of Certainty, Relection and Isolation Efects, but found no diferences between the decision-making behavior of respondents who had more or less inancial education.

Melo 2008 Graduate students and accountants 91 and 425 Results obtained indicated that, in general, there is no signiicant inluence of the characteristics listed on the level of loss aversion.

Côrtes 2008

Professionals who work or worked with the inancial market

40 Concludes that decision-makers tend to present risk aversion in the ield of gains and are prone to risk in the ield of losses.

Marinho et al. 2009 Graduate students 216

Concludes that there is no inluence of rational evolution on the phases of the decision-making process, diferently from gender, considering that, based on the answers collected, females present greater risk aversion.

Torralvo 2010 Postgraduate students 206

Investors do not act in a purely rational way, and there are diferences between the studied demographic proiles, such as, for example, the fact that men’s behaviors are more biased than women’s.

Marconi and Lakatos (2010, p. 63) indicate that the function of science is “improvement, through the growing body of knowledge, of man’s relationship with his world”. They also considered “invention of new ideas (hypotheses, theories or techniques) or production of new empirical data that promise to solve the problem” (MARCONI; LAKATOS, 2010, p. 66) as one of the steps of the scientific method. This research, in an unprecedented way, in order to produce new empirical data, has used employees from a major national financial institution as sample. We must mention that these employees are also customers of the said bank and, hence, are potential investors.

Also differently, and to quantify the groups’ majority preferences for alternatives that reveal or do not reveal violations of the rational decision-making model, this research measured the percentage of respondents who actually made inconsistent choices, considering the precepts of the Theory of Expected Utility; as an additional contribution, we used econometric models to analyze differences between the studied demographic profiles.

We must also mention that this work’s sample in made up of 2,590 respondents, a much larger number than earlier research carried out on the subject and summarized in Chart 1.

The results confirmed the presence of the effects and proved that a large portion of the sample presented effective inconsistency in their choices, according to the principles of the Theory of Expected Utility, which indicates that decisions were not made in a strictly rational way. As to the analysis of behavioral differences between demographic profiles analyzed, the proposed econometric models indicated a negative relationship between age and income and total violations, according to the rational model.

2 THEORETICAL FRAMEWORK

2.1 Origins of behavioral inance

According to classical economic theory, prices of goods are deined based on their respective production costs. Neoclassical economic theory included, in analysis of the formation of price, the importance of demand, deined – based on subjective assessment – by the satisfaction or utility provided to consumers, whose choices are made respecting the postulate of rationality.

he heory of Expected Utility, according to Cusinato (2003), assumes that the value of things cannot be based on their prices, but on the utility they provide, so that each level of income is associated with a degree of ultimate beneit, deined as a utility, which can take positive weights (in the ield of gains) and negative weights (in the ield of losses), with symmetric weights. hus, based on the premise that people are fully rational, that all information is efectively processed by decision-making subjects and that markets are eicient, each decision is made to maximize its expected utility.

Under the precepts of neoclassical economics, especially with regard to the rationality of economic subjects and the pursuit of maximizing expected utility at every decision made, the Modern Theory of Finance was founded.

to be eicient, such as the lack of transaction costs, equal access to available information, and homogeneity of investors’ expectations as to asset return probabilities.

According to Shleifer (2000, p. 5), the Eicient Market Hypothesis assumes that “when people are rational, markets are eicient by deinition”. Based on the studies of Fama (1970), he also lists three arguments that support this hypothesis: rational evaluation of assets by investors, randomness of transactions by irrational investors (which cancel out without afecting prices) and correction – by rational arbitrageurs – of any possible price deviations caused by irrational investors.

Based on the assumption that people present risk aversion and are fully rational, that all information is efectively processed by decision-making subjects and that markets are eicient, decisions are made in order to maximize expected utility. However, criticism of the current paradigm by several studies led to the emergence of a new inancial theory: Behavioral Finance, based on the premise, therefore, that decision-makers do not behave in a strictly rational way, but make judgments and choices under the inluence of emotional aspects, using mental shortcuts or simplifying rules that are called heuristics and can lead to systematic errors and deviations, considered cognitive biases.

According to Tversky and Kahneman (1974), beliefs concerning uncertainty are eventually expressed as probabilities, and often subjectively evaluated based on heuristics and not on statistical calculations. In the same study, they are segmented into heuristics of representativeness, availability and adjustment and anchorage, explaining their cognitive biases.

The heuristics of representativeness bases evaluation of the probability that certain events will be created by certain processes on the similarity between them and stereotypes. he heuristics of availability explains cases in which

probabilities or frequencies are based on how easily occurrences are remembered. he heuristics of adjustment and anchorage bases judgments on a reference (anchor) that may or may not refer to the events involved in the decision.

Irrational decisions in inancial markets may cause so-called anomalies. To Macedo Jr, Kolinsky and Morais (2011, p. 265), “an anomaly is statistical evidence of the incorrect establishment of asset prices by the market”. According to the Modern Finance Theory, anomalies occur randomly and can be solved by arbitration. According to what Behavioral Finance advocates, this isn’t always possible, due to certain limits. hus, we can state, as observed by Shleifer (2000), that Behavioral Finance is based on two pillars: on the limits of arbitration and on the limits of economic subjects’ rationality, as well as on the respective cognitive process leading to decision-making, also known as investor sentiment.

Regarding limited rationality, according to Halfeld and Torres (2001, p. 65), “the man of Behavioral Finance is not totally rational; he is simply a normal man”. In the same line of reasoning, psychology, particularly research on decision-making, such as the study carried out by Richard haler, Daniel Kahneman and Amos Tversky, became enormously important to new research in the ields of economics and inance. haler (1999) relates understanding the market to understanding people, and states that, in a not too distant future, the term “Behavioral Finance” will be redundant – after all, he asks, does any type of inance not include behavioral aspects?

how decisions should ideally be made. The model that considers the limits of rationality, the descriptive one, deals with how decisions are actually made, given the constraints to resources such as information and time.

The EMH advocates that, while they randomly occur, eventual “irrational” movements by so-called noise traders are corrected by rational subjects in a timely way, correcting any possible deviations in asset prices caused by arbitration. According to Rabelo Jr. and Ikeda (2004, p. 5), arbitration is the “simultaneous buying and selling of the same title, or of an essentially similar one, in two diferent markets, at diferent prices, in order to obtain an advantage in the operation”.

However, according to theoretical supporters of Behavioral Finance, the actions of arbitrageurs are limited; this can be corroborated by observing, over the years, the presence of inancial bubbles and other anomalies in the market (phenomena considered random by EMH advocates). Arbitration can be expensive and risky and, in some cases, unfeasible, because of its limitations. Baker and Wurgler (2011) conclude that, based on literature concerning limited arbitration, price deviations (mispricing) in the market often do not present real opportunities for arbitration. hese limits refer to the fundamental risks of assets (absence of substitute titles), to risks inherent to actions of so-called noise traders and to the risks of implementation costs involved. According to Shleifer (2000), arbitration can be risky and limited because asset prices do not instantly converge to their core values. Moreover, there are also the inherent implementation costs that refer to arbitration strategies that can make them less attractive or viable.

2.2 he prospect theory

Kahneman and Tversky (1979) created the Prospect heory, a critique of the heory of

Expected Utility as a tool for decision-making in situations involving uncertainty and risk, adopting as premises the presence of irrationality and the corresponding use of heuristics in people’s decision-making processes, leading to systematic errors due to biased cognitive processes.

Two steps can be observed in the decision-making process, according to Kahneman and Tversky (1979): editing (preliminary analysis and simpliication of perspectives) and evaluation (evaluation and choice of the highest value perspective).

The Prospect Theory, even assuming that people tend to attach greater weight to possibilities as their respective probabilities increase, challenges this principle by stating that the change from 0% to 5% creates a nonexistent possibility and, therefore, although highly unlikely, causes decision-makers to overweight the value attributed to this condition, characterized as the Possibility Efect (amounts paid in lotteries conirm this bias). On the other hand, the change from 95% to 100% results in another bias, the so-called Certainty Efect, in which highly probable possibilities are underweighted and greater weight is attributed to events that are certain than to events that are possible.

GRAPH 1 – he prospect theory’s hypothetical value function the prospect theory

Source: Kahneman and Tversky (1979, p. 279)

his bias was named the Relection Efect, a trend towards risk aversion in the ield of gains and towards risk seeking in the ield of losses, with greater recovery of losses when compared to gains.

Loss aversion and the use of a reference point when making choices refer us to another phenomenon known as the Endowment Efect, developed by haler, in which, in a way that is inconsistent with rational analysis, we tend to overweight certain property that we possess if it is intended to be used, resulting in discrepancies between values attributed at the time of buying and of selling (KAHNEMAN, 2012). “When it is more painful to give up a good than it is pleasurable to obtain it, buying prices will be significantly lower than selling prices.” (KAHNEMAN; TVERSKY; 1984, p. 348)

When we are in situations that involve more than one problem and, therefore, more than one decision, we tend to make case by case evaluation, whilst each problem presents itself, characterizing a narrow framework and highlighting the bias Isolation Efect. Concerning this bias in the context of the Prospect heory, Macedo Jr, Kolinsky and Morais (2011, p. 276) point out that “people generally discard components that are shared by all considered probabilities” and Rogers et al. (2007, p. 52)

point out that “to simplify the decision-making process, subjects generally disregard many of the characteristics of the available choices and focus analysis on the components that diferentiate these options”.

Based on the Isolation Efect, considering the non-linearity of the Prospect Theory’s hypothetical value function and the fact that decisions are based on a reference point, the Framing Efect arises, in which the choices for the same problem may be diferent according to the way in which the latter is framed (KAHNEMAN; TVERSKY, 1984).

3 METHODOLOGICAL PROCEDURES

We deined employees who work in the sales and high net worth (except Private Banking) segments of a major national inancial institution in the state of São Paulo as the sample of this paper.

For this research, we adapted the questionnaire first used by Kahneman and Tversky (1979) in their seminal article, explained in the discussion of results, changing the currency to the Brazilian real and including qualitative questions to analyze respondents’ demographics. he numbers of the questions presented in this article refer to those used in the questionnaire that was applied.

Between October 26, 2012 and November 25, 2012, at random, to avoid selection bias, 21,267 questionnaires were sent electronically to respondents, and data was collected by the SurveyMonkey tool. Questionnaire could only be completed if all answers were illed in; of the 3,143 respondents who started to answer the questionnaire, 2,590 concluded it, representing a 12.2% success rate as to the total sent, and an 82.4% success rate as to the total of those who began to answer.

using the chi-square test, with signiicance levels of 1% and 5% of the ratio of choices for each alternative – and if there was a majority preference for any of them. To this end, the following assumptions were considered:

H0: there is no majority preference for an alternative. In this case, the ratio of choices for alternative A is equal to the ratio of choices for alternative B, that is, the observed ratio is equal to the expected ratio (50% for both).

H1: there is a majority preference for an alternative. In this case, the ratio of choices for alternative A is diferent from the ratio of choices for alternative B, that is, the observed ratio is diferent from the expected ratio (50% for both).

Next, the answers were analyzed in pairs and, if inconsistent, were considered violations. According to Kimura, Basso and Krauter (2006, p. 44), “inconsistency depends on identifying incoherence between attitudes”. Importantly, the presence of inconsistency does not mean error on the part of the respondents, but implies only that their preferences are inconsistent with what the Expected Utility heory predicts. If there were inconsistent majority preferences among the questions that make up each pair, this proves that there are deviations from behavior predicted by expected utility in respondents’ decision-making as to Certainty, Relection and Isolation Efects. hus, the following hypotheses were considered:

H0: there is no evidence of deviation from

behavior predicted by expected utility in respondents’ decision-making. In this case, there are no majority inconsistent preferences among the questions that involve each pair.

H1: there is evidence of deviation from behavior predicted by expected utility in respondents’ decision-making. In this case,

there are majority inconsistent preferences among the questions that involve each pair.

As well as analyzing the majority preferences for alternatives that demonstrate deviations to rationality, we also analyzed, pair by pair, if there was a majority preference for effectively inconsistent alternatives, that is, respondents who chose alternative A and B (or B and A) in each pair, respectively. In this case, the following hypotheses were considered:

H0: there is no majority preference for

efectively inconsistent alternatives. In this case, the ratio of choices for alternatives A and A or B and B is equal to the ratio of choices for alternatives A and B or B and A, that is, the observed ratio is equal to the expected ratio (50% for both).

H1: there is a majority preference for efectively inconsistent alternatives. In this case, the ratio of choices for alternatives A and A or B and B is diferent from the ratio of choices for alternatives A and B or B and A, that is, the observed ratio is diferent from the expected ratio (50% for both).

So as to test and measure diferences in respondents’ decision-making behavior, taking analyzed demographic proiles into account, we developed econometric models that are detailed in section 4.2.

4 RESULTS OBTAINED

4.1 Questions – discussion of results

CHART 2 – Question 8

Which of the two alternatives do you prefer? Utility

Alternative A: a 33% chance of winning R$ 2,500.00, a 66% chance of winning R$ 2.400,00 and a 1% chance of winning R$ 0.00

0.33 × U(2,500) + 0.66 × U(2,400)

Alternative B: a 100% chance of winning R$ 2,400.00 U(2,400)

Source: Adapted from Kahneman and Tversky (1979)

According to the Certainty Effect, we expect most respondents to have chosen alternative B, preferring the certainty of gains.

Thus: 0.33 × U(2,500) + 0.66 × U(2,400) < U(2,400). Simplifying the inequation, thus:

0.33 × U(2,500) < 0.34 × U(2,400).

CHART 3 – Question 9

Which of the two alternatives do you prefer? Utility

Alternative A: a 33% chance of winning R$ 2,500.00 and a 67% chances of winning R$ 0.00 0.33 × U(2,500) Alternative B: a 34% chance of winning R$ 2,400.00 and a 66% chance of winning R$ 0.00 0.34 × U(2,400)

Source: Adapted from Kahneman and Tversky (1979)

here will be evidence of deviation as to the behavior predicted by the Expected Utility heory in decision-making by respondents as to the Certainty Efect if the majority chose alternative A, indicating a preference for the largest gain (since there is no alternative with a gain that is certain) even facing a one percentage point smaller chance of it occurring. he result of this preference is described by 0.33 × U(2,500) > 0.34 × U(2,400). hese deviations can be proven by comparing inequations 0.33 × U(2,500) < 0.34 × U(2,400)

and 0.33 × U(2,500) > 0.34 × U(2,400).

With regard to question 8, the choice for alternative B (75.4%) prevailed, conirming preference for the alternative that ofers a gain that is certain. However, with regard to question 9, we cannot state that there was a majority choice among alternatives, thus not revealing inconsistency in respondents’ decision-making process.

When we analyzed the percentage of efectively inconsistent responses, we observed that most respondents were consistent in their choices (54.1%).

CHART 4 – Question 10

Which of the two alternatives do you prefer? Utility

Alternative A: an 80% chance of winning R$ 4,000.00 and a 20% chance of winning R$ 0.00 0.80 × U(4,000) Alternative B: an 100% chance of winning R$ 3,000.00 1.00 × U(3,000)

Source: Adapted from Kahneman and Tversky (1979)

According to the Certainty Efect, we expect the majority of respondents to have chosen alternative B, preferring the certainty of

gain. hus: 0.80 × U(4.000) < 1.00 × U(3,000).

Dividing both sides of the inequation by 4, we ind: 0.20 × U(4,000) < 0.25 × U(3,000).

CHART 5 – Question 11

Which of the two alternatives do you prefer? Utility

Alternative A: a 20% chance of winning R$ 4,000.00 and an 80% chance of winning R$ 0.00 0.20 x U(4,000) Alternative B: a 25% chance of winning R$ 3,000.00 and a 75% chance of winning R$ 0.00 0.25 x U(3,000)

here will be evidence of deviation as to the behavior predicted by the Expected Utility heory in decision-making by respondents as to the Certainty Efect if the majority chose alternative A, indicating a preference for the largest gain (since there is no alternative with a gain that is certain) even facing a ive percentage point smaller chance of it occurring. he result of this preference is described by: 0.20 × U(4,000) > 0.25 × U(3,000). hese deviations can be proven by comparing inequations 0.20 × U(4,000) < 0.25 × U(3,000) and 0.20 × U(4,000) > 0.25

× U(3,000).

With regard to question 10, the same as in question 8, the choice for alternative B (87.3%) prevailed, conirming preference for the alternative that ofers a gain that is certain. However, with regard to question 11, considering the preference for alternative B in the total of answers, we can observe consistency in respondents’ decision-making process.

When we analyzed the percentage of efectively inconsistent responses, we observed an expressive ratio of biased choices (41.2%), although the majority presented effective consistency in their choices (58.8%).

CHART 6 – Question 12

Which of the two alternatives do you prefer? Utility

Alternative A: a 50% chance of winning a 3-week trip to England, France and Italy and a 50% chance

of not winning anything 0.50 × U (3-week trip)

Alternative B: an 100% chance of winning a 1-week trip to England 1.00 × U (1-week trip)

Source: Adapted from Kahneman and Tversky (1979)

According to the Certainty Efect, we expect the majority of respondents to have chosen alternative B, preferring the certainty of

gain. hus: 0.50 × U(3-week trip) < 1.00 × U (1-week trip).

CHART 7 – Question 13

Which of the two alternatives do you prefer? Utility

Alternative A: a 5% chance of winning a 3-week trip to England, France and Italy and a 95% chance of not winning anything

0.05 × U (3-week trip)

Alternative B: a 10% chance of winning a 1-week trip to England, and a 90% chance of not winning anything

0,10 × U (1-week trip)

Source: Adapted from Kahneman and Tversky (1979)

here will be evidence of deviation as to the behavior predicted by the Expected Utility heory in decision-making by respondents as to the Certainty Efect if the majority chose alternative A, indicating a preference for the largest gain (since there is no alternative with a gain that is certain) even facing a ive percentage point smaller chance of it occurring. he result of this preference is described by: 0.05 × U (3-week trip) > 0.10 × U (1-week trip). hese deviations can be proven by comparing inequations 0.50 ×

U(3-week trip) < 1.00 × U(1-week trip) and 0.50 × U(3-week trip) > 1.00 × U(1-week trip).

CHART 8 – Question 14

Which of the two alternatives do you prefer? Utility

Alternative A: a 45% chance of winning R$ 6,000.00 and a 55% chance of winning R$ 0,00 0.45 × U(6,000) Alternative B: a 90% chance of winning R$ 3,000.00 and a 10% chance of winning R$ 0.00 0.90 × U(3,000)

Source: Adapted from Kahneman and Tversky (1979)

According to the Certainty Efect, we expect the majority of respondents to have chosen alternative B, preferring the certainty of gain,

even if it smaller. hus: 0.45 × U(6,000) < 0.90

× U(3,000).

CHART 9 – Question 15

Which of the two alternatives do you prefer? Utility

Alternative A: a 0.1% chance of winning R$ 6,000.00 and a 99.9% chance of winning R$ 0.00 0.001 × U(6,000) Alternative B: a 0.2% chance of winning R$ 3,000.00 and a 99.8% chance of winning R$ 0.00 0.002 × U(3,000)

Source: Adapted from Kahneman and Tversky (1979)

here will be evidence of deviation as to the behavior predicted by the Expected Utility heory in decision-making by respondents as to the Certainty Efect if the majority chose alternative A, indicating a preference for the largest gain (since there is no alternative with a gain that is certain) even facing a one-tenth of a percentage point smaller chance of it occurring, in perspectives that involve extremely small probabilities. he result of this preference is described by: 0.001 × U(6,000) > 0.002 × U(3,000). Multiplying both sides of the inequation by 450, we ind: 0.45 × U(6,000) > 0.90 × U(3,000). hese deviations can be proven

by comparing inequations 0.45 × U(6,000) < 0.90 × U(3,000) and 0.45 × U(6,000) > 0.90

× U(3,000).

With regard to question 14, the choice for alternative B (85.7%) prevailed, conirming preference for the alternative that ofers greater probability of gain, even though it is smaller. With regard to question 15, considering the preference for alternative A in the total of answers (59.9%), we can observe inconsistency in respondents’ decision-making process. his is conirmed by analyzing the ratio of efectively inconsistent choices, majority preference of the total of respondents (52.8%).

Analysis of questions 10, 11, 14, 15, 16, 17, 18 and 19 aims at testing for the Relection Efect, people’s tendency to be risk averse in the ield of gains and prone to risk in the ield of losses.

CHART 10 – Question 16

Which of the two alternatives do you prefer? Utility

Alternative A: an 80% chance of losing R$ 4,000.00 and a 20% chance of losing R$ 0.00 0.80 × U(-4,000) Alternative B: an 100% chance of losing R$ 3,000.00 1.00 × U(-3,000)

Source: Adapted from Kahneman and Tversky (1979)

here will be evidence of deviation as to the behavior predicted by the Expected Utility heory in decision-making by respondents as to the Relection Efect if the majority chose alternative A, indicating aversion to the alternative

that ofers certain loss (B), even when the latter presents a smaller value that the probable loss than the former. he result of this preference is described by: 0.80 × U(-4,000) > 1.00 ×

comparing inequations 0.80 × U(4,000) < 1.00

× U(3,000) and 0.80 × U(-4,000) > 1.00 × U(-3,000).

Just as what was analyzed previously, with regard to question 10, the choice for alternative B prevailed, confirming preference for the alternative that ofers a gain that is certain. With

regard to question 16, considering the preference for alternative A in the total of answers (84.6%), we can observe inconsistency in respondents’ decision-making process, conirmed by analyzing the ratio of effectively inconsistent choices (74.9%).

CHART 11 – Question 17

Which of the two alternatives do you prefer? Utility

Alternative A: a 20% chance of losing R$ 4,000.00 and a 80% chance of losing R$ 0.00 0.20 x U(-4,000) Alternative B: a 25% chance of losing $ 3,000.00 and a 75% chance of losing R$ 0.00 0.25 x U(-3,000)

Source: Adapted from Kahneman and Tversky (1979)

here will be evidence of deviation as to the behavior predicted by the Expected Utility heory in decision-making by respondents as to the Relection Efect if the majority chose alternative B, indicating aversion to the alternative that ofers larger loss (A), even with a 5 percentage point smaller probability of occurring. The result of this preference is described by: 0.20 × U(-4,000) < 0.25 × U(-3,000). hese deviations

can be proven by comparing inequations 0.20

× U(4,000) > 0.25 × U(3,000) and 0.20 × U(-4,000) < 0.25 × U(3,000).

Differently from what is expected according to the Relection Efect, we observe that, with regard to question 11, there was

majority preference for alternative B for the total respondents. With regard to question 17, also diferently from what is expected according to the Relection Efect, there was a majority preference for alternative A for the total respondents (53.1%). Even so, even facing majority preference for alternatives that were not expected according to the Relection Efect, most of the respondents were inconsistent in their choices.

his is conirmed by analyzing the ratio of efectively inconsistent answers (49.3%). We cannot state that there was majority preference for alternatives that revealed efective inconsistency in their choices. It is important to note the expressive ratio of biased choices (49.3%).

CHART 12 – Question 18

Which of the two alternatives do you prefer? Utility

Alternative A: a 45% chance of losing R$ 6,000.00 and a 55% chance of losing R$ 0,00 0.45 × U(-6,000) Alternative B: a 90% chance of losing R$ 3,000.00 and a 10% chance of losing R$ 0.00 0.90 x U(-3,000)

Source: Adapted from Kahneman and Tversky (1979)

here will be evidence of deviation as to the behavior predicted by the Expected Utility heory in decision-making by respondents as to the Relection Efect if the majority chose alternative A, indicating aversion to the alternative that ofers greater probability of loss (B), even if the latter presents a smaller value. he result of this preference is described by: 0.45 × U(-6,000)

> 0.90 × U(-3,000). These deviations can

be proven by comparing inequations 0.45 ×

U(6,000) < 0.90 × U(3,000) and 0.45 × U(-6,000) > 0.90 × U(-3,000).

probability of gain, even though it is smaller. With regard to question 18, considering the preference for alternative A (72.4%), we can observe inconsistency in respondents’

decision-making process, conirmed by analyzing the ratio of effectively inconsistent choices (64.8%). We can state that most respondents chose efectively inconsistent alternatives (52.8%).

CHART 13 – Question 19

Which of the two alternatives do you prefer? Utility

Alternative A: a 0.1% chance of losing R$ 6,000.00 and a 99.9% chance of losing R$ 0.00 0.001 × U(-6,000) Alternative B: a 0.2% chance of losing R$ 3,000.00 and a 99.8% chance of losing R$ 0.00 0.002 × U(-3,000)

Source: Adapted from Kahneman and Tversky (1979)

here will be evidence of deviation as to the behavior predicted by the Expected Utility heory in decision-making by respondents as to the Relection Efect if the majority chose alternative B, indicating aversion to the alternative that ofers greater loss (B), even with a one-tenth of a percentage point smaller probability of occurring, in perspectives that involve extremely low probabilities. he result of this preference is described by: 0.001 × U(-6,000) < 0.002 ×

U(-3,000). hese deviations can be proven by

comparing inequations 0.001 × U(6,000) > 0.002 × U(3,000) and 0.001 × U(-6,000) < 0.002 × U(-3,000).

With regard to question 15, we observe preference for alternative A. With regard to question 19, as is expected according to the

Relection Efect, we can observe inconsistency in respondents’ decision-making process, since there was a preference for alternative B (56.5%). his is conirmed by analyzing the ratio of efectively inconsistent choices (64.8%). We can state that most respondents chose efectively inconsistent alternatives. Although we cannot state that the majority of respondents chose efectively inconsistent alternatives, we highlight, however, the expressive ratio of biased choices (51.5%).

Analysis of questions 11 and 21 aims at testing for the Isolation Efect, a bias observed when, facing situations that include more than one problem and, thus, involve more than one decision, people tend to make case-by-case evaluations, while issues are presented, instead of being analyzing them together.

CHART 14 – QUESTION 21

Consider a game with two phases. In the irst phase, there is a 75% probability that the game ends without you winning anything and a 25% probability that you move to the second phase. If you reach the second phase, you can choose between the following alternatives. Please note that the choice must be made before the game starts.

Utility

Alternative A: an 80% chance of winning R$ 4,000.00 and a 20% chance of winning R$ 0.00 0.20 × U(4,000) Alternative B: an 100% chance of winning R$ 3,000.00 0.25 × U(3,000)

Source: Adapted from Kahneman and Tversky (1979)

here will be evidence of deviation as to the behavior predicted by the Expected Utility heory in decision-making by respondents as to the Isolation Effect if the majority chose alternative B, indicating that the irst phase of the question was discarded and that, at the second

stage, there was preference for alternative that ofers certain gain. he result of this preference is described by: 0.20 × U(4,000) < 0.25 × U(3,000).

hese deviations can be proven by comparing inequations 0,20 × U(4,000) > 0.25 × U(3,000)

Differently from what is expected according to the Certainty Efect, we observe that, with regard to question 11, there was majority preference for alternative B. With regard to question 21, there was a majority preference for alternative B (83.6%), conirming what is expected according to the Isolation Efect. Most of the respondents, however, were consistent in their choices.

his is conirmed by analyzing the ratio of efectively inconsistent answers (41.9%). We can state that there was majority preference for alternatives that revealed efective inconsistency in their choices.

he results of this research, for the total respondents, are compared with those obtained by Kahneman and Tversky (1979) and other similar work carried out, such as the study by Kimura, Basso and Krauter (2006), which has been reference for the preparation of other studies. he numbering of questions adopted was the one used in this work.

Table 1 presents the results for pairs involving the analysis of the Certainty Efect. Preferences observed in questions 8, 10 and 12, involving alternatives that ofer certain gains, and issues 14 and 15, that signal diferent decision weights assigned to diferent levels of probability, are common to all papers, which strongly indicates presence of the Efect, regardless of the diferent

sample, geographic and time characteristics of each study.

In question 9, whose alternatives do not ofer certain gain and that present minor diferences between probabilities and gains, in this study, as observed in Kimura, Basso and Krauter (2006), but unlike other studies, there is no statistically signiicant preference.

Claudia Emiko Yoshinaga / Thiago Borges Ramalho

TABLE 1 – Comparison of results – certainty efect

Pair 1 Alternative Present Study KT (79) KBK (06) R et al (07) RFS (08) C (08) T (10)

A 24.6% 18.0% 30.0% 31.0% 24.7% 42.0% 35.9%

B 75.4%** 82.0%** 70.0%** 69.0%** 75.3%** 58.0%** 64.1%**

A 50.8% 83.0%** 52.0% 94.0%** 81.2%** 65.0%** 70.8%**

B 49.2% 17.0% 48.0% 6.0% 18.8% 35.0% 29.2%

Pair 2 Alternative

A 12.7% 20.0% 29.0% 30.0% 24.7% 37.0% 25.7%

B 87.3%** 80.0%** 71.0%** 70.0%** 75.3%** 63.0%** 74.3%**

A 44.8% 65.0%** 57.0% 61.0%** 57.0% 73.0% 64%**

B 55.2%** 35.0% 43.0% 39.0% 43.0% 27.0% 36.0%

Pair 3 Alternative

A 11.3% 22.0% 20.0% 25.0% 25.3% 10.0% 17.6%

B 88.7%** 78.0%** 80.0%** 75.0%** 74.7%** 90.0% 82.4%**

A 39.2% 67.0%** 49.0% 54.0% 45.7% 63.0%** 53.9%

B 60.8%** 33.0% 51.0% 46.0% 54.3% 37.0% 46.1%

Pair 4 Alternative

A 14.3% 14.0% 23.0% 19.0% 19.4% 12.0% 27.7%

B 85.7%** 86.0%** 77.0%** 81.0%** 80.6%** 88.0% 72.3%**

A 59.9%** 73.0%** 72.0%** 66.0%** 54.3% 80.0% 77.2%**

B 40.1% 27.0% 28.0% 34.0% 45.7% 20.0% 22.8%

Certainty Effect

Question 8

Question 9

Question 10

Question 11

Question 12

Question 13

Question 14

Question 15

Percentages in bold are statistically signiicant at levels 1% (**) and 5% (*).

KT (79): Kahneman and Tversky (1979); KBK (06): Kimura, Basso and Krauter (2006); R et al (07): Rogers et al (2007); RFS (08): Rogers, Favato and Securato (2008); C (08): Côrtes (2008); T (10): Torralvo (2010)

Source: he authors

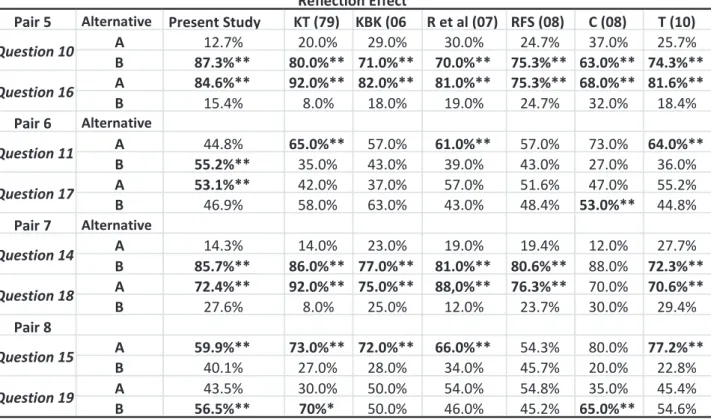

Table 2 presents the results for pairs that involve an analysis of the Relection Efect. Questions 10, 11, 14 and 15 have already been discussed in analysis of the Certainty Effect. Preferences observed in questions 16 and 18, involving alternatives that ofer certain loss and a high probability of loss, respectively, are common to all papers, strongly indicating the presence of the Relection Efect, especially with regard to loss aversion.

In question 19, similarly to the question 15, but formulated in terms of losses, whose alternatives involve very low probabilities, this study and the one carried out by Côrtes (2008) followed the results of Kahneman and Tversky (1979).

In question 17, which is analogous to question 11, also formulated in terms of losses, without any perspective that ofers certainty of loss, this study was the only one with a reverse

preference to that observed in the original work of Kahneman and Tversky (1979), with statistical signiicance, repeating what occurred in questions 11 and 13.

Behavioral Finance in Brazil: applying the prospect theory to potential investors

TABLE 2 – Comparison of results – relection efect

Pair 5 Alternative Present Study KT (79) KBK (06 R et al (07) RFS (08) C (08) T (10)

A 12.7% 20.0% 29.0% 30.0% 24.7% 37.0% 25.7%

B 87.3%** 80.0%** 71.0%** 70.0%** 75.3%** 63.0%** 74.3%**

A 84.6%** 92.0%** 82.0%** 81.0%** 75.3%** 68.0%** 81.6%**

B 15.4% 8.0% 18.0% 19.0% 24.7% 32.0% 18.4%

Pair 6 Alternative

A 44.8% 65.0%** 57.0% 61.0%** 57.0% 73.0% 64.0%**

B 55.2%** 35.0% 43.0% 39.0% 43.0% 27.0% 36.0%

A 53.1%** 42.0% 37.0% 57.0% 51.6% 47.0% 55.2%

B 46.9% 58.0% 63.0% 43.0% 48.4% 53.0%** 44.8%

Pair 7 Alternative

A 14.3% 14.0% 23.0% 19.0% 19.4% 12.0% 27.7%

B 85.7%** 86.0%** 77.0%** 81.0%** 80.6%** 88.0% 72.3%**

A 72.4%** 92.0%** 75.0%** 88,0%** 76.3%** 70.0% 70.6%**

B 27.6% 8.0% 25.0% 12.0% 23.7% 30.0% 29.4%

Pair 8

A 59.9%** 73.0%** 72.0%** 66.0%** 54.3% 80.0% 77.2%**

B 40.1% 27.0% 28.0% 34.0% 45.7% 20.0% 22.8%

A 43.5% 30.0% 50.0% 54.0% 54.8% 35.0% 45.4%

B 56.5%** 70%* 50.0% 46.0% 45.2% 65.0%** 54.6%

Reflection Effect

Question 14

Question 18

Question 15

Question 19 Question 10

Question 16

Question 11

Question 17

Percentages in bold are statistically signiicant at levels 1% (**) and 5% (*).

KT (79): Kahneman and Tversky (1979); KBK (06): Kimura, Basso and Krauter (2006); R et al (07): Rogers et al (2007); RFS (08): Rogers, Favato and Securato (2008); C (08): Côrtes (2008); T (10): Torralvo (2010)

Source: he authors

Table 3 presents the results for the pair that involves analyzing the Isolation Efect. Preferences observed in question 21, formulated in two phases and that, at the second phase, ofer certain gain, are common to all papers, strongly indicating the presence of the Efect, as to contempt for the irst phase of the problem and total focus on the second, analyzing perspectives separately, rather than together.

Regarding inconsistency in respondents’ decision-making from the point of view of

Claudia Emiko Yoshinaga / Thiago Borges Ramalho

TABLE 3 – Comparison of results – isolation efect

Pair 9 Alternative Present Study KT (79) KBK (06) R et al (07) RFS (08) C (08) T (10)

A 44.8% 65%** 57.0% 61.0%** 57.0% 73.0% 64%**

B 55.2%** 35.0% 43.0% 39.0% 43.0% 27.0% 36.0%

A 16.4% 22.0% 22.0% 29.0% 28.0% 30.0% 18.4%

B 83.6%** 78.0%** 78.0%** 71.0%** 72.0%** 70.0% 81.6%** Isolation Effect

Question 11

Question 21

Percentages in bold are statistically signiicant at levels 1% (**) and 5% (*).

KT (79): Kahneman and Tversky (1979); KBK (06): Kimura, Basso and Krauter (2006); R et al (07): Rogers et al (2007); RFS (08): Rogers, Favato and Securato (2008); C (08): Côrtes (2008); T (10): Torralvo (2010)

Source: he authors

4.2 Econometric model – demographic proiles

Several studies have been carried out in order to research, for various demographic profiles, differences with regard to people’s decision-making behavior in situations involving uncertainty and risk, identifying the presence of bias in their choices.

Barsky et al. (1997) concluded, among other characteristics, that, separately, people with higher levels of education and those who are very rich are more prone to risk. On the other hand, people with an average income level and education and aged between 55 and 70 are more risk averse.

Torralvo (2010), too, among other characteristics, identiied more biased behavior, separately, in men, in respondents who were graduated in courses associated with Management, with a greater volume of inancial instruments, with no inancial experience and in managing third party funds. On the other hand, he did not identify any diferences between individuals with or without inancial dependents. Bhandari and Deaves (2006) found that men with a high educational level are more prone to overconidence.

According to Bajtelsmit and Bernasek (1996), many studies have found that women invest more conservatively and with greater risk aversion, which is corroborated by Marinho et al. (2009). Santos and Barros (2011) also attributed to men a greater propensity to risk. On this track,

according to Barber and Odean (2005), men are more overconident than women; they cite other studies that conirm this conclusion.

Décourt (2004) noted the presence of behavioral biases in inancial executives, doctors, MBA and university students. Similarly, Ribeiro (2010) concluded that inancial experts are more likely to take risks than non-specialists, and Rogers, Favato and Securato (2008, p. 1) state that “bias in the cognitive process and limits to learning remain even in individuals with a higher level of education and more structured inancial education”.

Hallahan, Faff and McKenzie (2004) concluded that gender, age, number of dependents, marital status, education, income and wealth are related to risk tolerance. hey also studied variations in the results when analysis is segmented: number of dependents, for example, has an inverse relationship with risk tolerance when the entire base is analyzed, but becomes not signiicant when only respondents aged over 60 were analyzed, just as occurred with married and unmarried respondents, when analyzed separately. According to the authors, the results for gender, education and income are consistent with the previous literature. However, the relationship between wealth and risk tolerance contrasts with previous research, emphasizing the presence of conlicting results observed in diferent studies.

respondents, taking into account the demographic profile analysis, econometric models were developed (multiple regressions with parameters estimated by OLS and TOBIT, the latter considering 0 and 9 as lower and higher). To this end, initially, we veriied, considering the nine pairs referring to Certainty, Reflection and Isolation Effects, how many violations (inconsistent choices with the rational model)

each respondent committed in making his decision. The total violations, expressed as a percentage scale, was deined as the dependent variable model, as summarized in Chart 15:

Regarding consumers’ boycott, Cruz, Pires Jr and Ross (2013, p. 504) concluded, from the study sample, that “women feel more guilty than men with regard to the motivations for boycott”.

CHART 15 – Dependent variable model

Dependent Variable Efect Interval

Ytotal Total Violations All 0 to 100% (OLS)

0 to 9 (TOBIT)

Source: he authors

Next, we deined the independent variables presented in Chart 16:

CHART 16 – Independent variable models

Independent Variable Nature Interval Dummy = 1

X1 age Quantitative 18 to 72 DNA

X2 Income 4 Dummy 0 to 1 Income below R$ 4 thousand

X3 Income4to6 Dummy 0 to 1 thousand and R$ 6 thousandIncome between R$ 4

X4 Man Dummy 0 to 1 Man

Source: he authors

he resulting models are expressed by the following equation:

Total Violations (% for OLS and quantity for TOBIT) = β0 +β1age +β2income4+β3income4to6 +β4man + u

Table 4 presents the results of the econometric models estimated by OLS and TOBIT:

TABLE 4 – Results of regressions

Variable OLS TOBIT

Method Coeicient Robust standard

deviation p-value Coeicient

Robust standard

deviation p-value

age -.1225918 ** .0480865 0.011 -.0118213 *** .0045255 0.009 income4 -2.466916 ** 1.132108 0.029 -.2395307 ** .10425 0.022 Income4to6 -1.425233 1.223503 0.244 -.1440494 .1124809 0.200

man 1.385536 .8627834 0.108 .1207144 .0800183 0.132

Constant 56.3603 *** 2.346062 0.000 5.115782 *** .2188416 0.000

F 3.42 *** 0.0085

R2 0.0049 0.012

LR 13.08 ** 0.0109

#Obs 2590 2590

* , ** and *** denote signiicance at 10%, 5% and 1% levels, respectively.

We observed, in both estimations, that the age and income below R$ 4,000 coeicients are signiicant at 5% and have a negative relationship with the total violations. Considering, then, as a basis, respondents who are women, aged 0 and with an income over R$ 6,000, we can conclude that, as age increases, violations decrease, and, as income decreases, violations increase. As to gender, the male dummy variable was a positive coeicient, although not signiicant, indicating that total violations tend to increase if the investor is man. hese results are potentially signiicant, although the degree of explanation of the parameters and correlation coeicients of the models are low.

5 CONCLUSIONS

For the efects studied, this study allowed us to:

a) quantify majority preferences for alterna-tives that do or do not reveal violations of the rational model for decision-making, compared to the results obtained in the original article and similar research; b) quantify proportions of respondents

who were efectively inconsistent in their choices according to what the heory of Expected Utility predicts;

c) propose and test an econometric model to investigate the diferences between the proiles of the respondents.

Regarding the Certainty Efect, the results conirmed the preference for options that ofered certain gain and presented efective inconsistency in decision-making by most respondents only when the choice involved perspectives with extremely low probabilities, and, in this situation, decision weights were higher than their respective probabilities. We should mention, however, the signiicant proportion of efectively inconsistent choices for all respondents: 45.9%, 41.2%, 35.5% and 52.8%, referring to pairs 1, 2, 3 and 4, respectively.

With regard to the Relection efect, the results indicated the presence of asymmetry of weights assigned to gains and losses, with risk aversion trend in perspectives formulated in terms of gain and risk propensity formulated in terms of loss, indicating loss aversion. Only in the case of the second pair of questions (Pair 6) did the results not conirm what is expected by the Relection Efect. Still, there was inconsistency in the choice of respondents, which occurred in all pairs, and effective inconsistency in pairs 5, presenting perspectives that involve certain gains and losses, and 7, which involves high probabilities of gains and losses. We should mention, also, to this efect, the signiicant proportion of efectively inconsistent choices for all respondents: 74.9%, 49.3%, 64.8% and 51.5%, referring to pairs 5, 6, 7 and 8, respectively.

Regarding the Isolation Effect, results conirm the expected considering the majority preference for the alternative that indicated realization, by the respondents, of disjunctive analysis and isolation of phases at the time of their decision-making. However, there was a majority preference for efective alternatives that revealed efective consistency in their choices, when the pair concerning the efect was examined. Nevertheless, it is important to note, as has been done for Certainty and Relection efects, a signiicant proportion of biased choices for all respondents: 41.9%.

of Finance seems to have been overcome. On the other hand, an also signiicant proportion of consistent choices show that there is also an absolute and incontestable truth about the matter, which refers to the need to carry out further research. We suggest, therefore, that this research continues, preferably with the goal of trying to understand the reasons why part of the decisions are made rationally, and part are not.

The proposed econometric models indicated a negative relationship between age and income and the total violations according to the rational model, with low levels of explanation and determination coefficients, which refers to the need to carry out further research to investigate the diferences in behavior between diferent decision-making demographic proiles. We suggest, also, that new studies be carried out by means of laboratory situations or actual investment transactions by individuals, to capture more safely the “real” behavior of decision-makers.

REFERENCES

BAJTELSMIT, V. L.; BERNASEK, A. Why do woman invest diferently than men? Financial

Counseling and Planning, 1996. Available at: <http://ssrn.com/abstract=2238>. Accessed on: 26 May 2013.

BAKER, M.; WURGLER, J. Behavioral corporate inance: an updated survey. NBER Working Paper, 17333, Aug. 2011. Available at: < http://www.nber.org/papers/w17333>. Accessed on: 20 May 2012.

BARBER, B. M.; ODEAN, T. Individual investors. In: THALER, R. (Org.). Advances in behavioral inance. New York: Russell Sage Foundation, 2005. v. 2, p. 543-569.

BARSKY, R. B. et al. Preference parameters and behavioral heterogeneity: an experimental approach in the health and retirement study. he

Quarterly Journal of Economics, Cambridge, v. 112, n. 2, p. 537-579, 1997.

BAZERMAN, M. H.; MOORE, D. Processo decisório.7. ed. Rio de Janeiro: Elsevier, 2010. BHANDARI, G.; DEAVES, R. he demographics of overconidence. he Journal of Behavioral Finance, Philadelphia, v. 7, n. 1, p. 5-11, 2006.

CÔRTES, F. M. Finanças comportamentais:

uma aplicação da teoria do prospecto na tomada de decisão de investidores no Brasil.2008. 71 f. Dissertação (Mestrado em Administração de Empresas) – Pontifícia Universidade Católica do Rio de Janeiro, Rio de Janeiro, 2008.

CRUZ, B. P. A.; PIRES JR, R. J. M; ROSS, S. D. Diferença de gênero na percepção de culpa no boicote de consumidores. Revista Brasileira

de Gestão de Negócios, São Paulo, v. 15, n. 49,

p. 504-523, Oct/Dec. 2013.

CUSINATO, R. T. Teoria da decisão sob incerteza e a hipótese da utilidade esperada: conceitos analíticos e paradoxos. 2003. 181 f. Dissertação (Mestrado em Economia) – Universidade Federal do Rio Grande do Sul, Porto Alegre, 2003.

DÉCOURT, R. F. As inanças comportamentais e o processo de decisão no mercado inanceiro brasileiro. 2004. 122 f. Dissertação (Mestrado

em Administração de Empresas) – Centro Universitário Álvares Penteado – Unifecap, São Paulo, 2004.

FAMA, E. Eicient capital markets: a review of theory and empirical work. Journal of Finance, Malden, v. 25, n. 2, p. 383-417, 1970.

HALLAHAN, T. A.; FAFF, R. W.; MCKENZIE, M. D. An empirical investigation of personal financial risk tolerance. Financial Services Review-Greenwich, [S.l.], v. 13, n. 1, p. 57-78, 2004.

JENSEN, M.C. Some anomalous evidence regarding market eiciency. Journal of Financial Economics, Amsterdan, v. 47, n. 2, p. 263-291, 1979.

KAHNEMAN, D. Rápido e devagar: duas formas de pensar. Rio de Janeiro: Objetiva, 2012.

______; TVERSKY, A. Prospect theory: ananalysis of decision under risk. Econometrica, Chicago, v. 47, n. 2, p. 263-291, Mar. 1979.

______; ______. Choices, values, and frames.

American Psychologist, Washington, D.C, v. 34, n. 4, p. 341-350, 1984.

KIMURA, H.; BASSO, L. F. C; KRAUTER, E. Paradoxos em finanças: teoria moderna versus inanças comportamentais. Revista de Administração de Empresas – RAE, São Paulo, v. 46, n. 1, p. 41-58, 2006.

MACEDO JUNIOR, J. S.; KOLINSKY, R.; MORAIS, J. C. J. Finanças comportamentais: como o desejo, o poder, o dinheiro e as pessoas inluenciam nossas decisões. São Paulo: Atlas, 2011.

MARCONI, M. A.; L AKATOS, E. M.

Fundamentos de metodologia científica.

7. ed. São Paulo: Atlas, 2010.

MARKOWITZ, H. Portfolio selection. The Journal of Finance, Malden, v. 7, n. 1, p. 77-91, Mar. 1952. Available at: <http://www.math.ust. hk/~maykwok/courses/ma362/07F/markowitz_ JF.pdf>. Accessed on: 09 Jun. 2012.

MODIGLIANI, F.; MILLER, M. H. he cost of capital, corporation inance, and the theory

of investiment. American Economic Review, Nashville, v. 48, n. 3, p. 261-297, June 1958. ______; ______. Dividend policy, growth and the valuation of shares. Journal of Business, Chicago, v. 34, n. 4, p. 411-433, 1961.

______; ______. Corporate income taxes and the cost of capital: a correction. he American Economic Review, Nashville, v. 53, n. 3, p. 433-443, 1963.

RABELO JUNIOR, T. S.; IKEDA, R. H. Mercados eicientes e arbitragem: um estudo sob o enfoque das inanças comportamentais. Revista Contabilidade & Finanças, São Paulo, v. 15,

n. 34, p. 97-107, Jan./Apr. 2004.

R I B E I RO , D . P. C . Pr o s p e c t t h e o r y, diversiicação ingênua e propensão a risco de especialistas em mercado: evidência empírica

no Brasil. 2010. 55 f. Dissertação (Mestrado em Finanças e Economia Empresarial) - Escola de Pós-Graduação em Economia, Fundação Getúlio Vargas, Rio de Janeiro, 2010.

ROGERS, P. et al. Finanças comportamentais no Brasil: um estudo comparativo. Revista de Economia e Administração, São Paulo, v. 6, n.1, p. 49-68, 2007.

______; FAVATO, V.; SECURATO, J. R. Efeito educação financeira no processo de tomada de decisões em investimentos: um estudo a luz das inanças comportamentais. In: CONGRESSO ASSOCIAÇÃO NACIONAL DE PROGRAMAS DE PÓS-GRADUAÇÃO EM CIÊNCIAS CONTÁBEIS, 2, 2008, Salvador.

Anais eletrônicos... Salvador: ANPCONT, 2008.

p. 1-17. Available at: <http://www.pablo.prof. ufu.br/artigos/anpcont2.pdf>. Accessed on: 23 Jun. 2012.

SHARPE, W. F. Capital and prices: a theory of market equilibrium under conditions of risk.

Journal of Finance, Malden, v. 19, n. 3, p.

SHLEIFER, A. Inefficient markets: an introduction to behavioral inance. New York: Oxford University Press, 2000.

SIMON, H. A. A behavioral model of rationality choice. Quarterly Journal of Economics, Cambridge, v. 69, n.1, p. 99-118, 1955.

THALER, R. he end of behavioral inance.

Financial Analysts Journal, Charlottesville, v. 55, n. 6, p. 12-17, 1999.

TORRALVO, C. F. Finanças comportamentais:

uma aplicação da teoria do prospecto em alunos brasileiros de pós-graduação. 2010. 124 f. Dissertação (Mestrado em Administração) – Universidade de São Paulo, São Paulo, 2010. TVERSKY, A.; KAHNEMAN, D. A judgment under uncertainty: heuristics and biases. Science,