Rev. bras. gest. neg. vol.17 número55

Texto

Imagem

Documentos relacionados

Neste trabalho o objetivo central foi a ampliação e adequação do procedimento e programa computacional baseado no programa comercial MSC.PATRAN, para a geração automática de modelos

A Lesão Vértebro Medular (LVM) determina uma alteração neura motora irreversível com défices motores e necessidade de autocuidado permanentes. Quando num contexto de

The methodology applied in the validation is a thorough methodology and, from the obtained results, it is possible to conclude that the Portuguese version of the Clinical Nursing

Para tal, nos próximos capítulos ir-se-á estudar a perspetiva dos empresários das unidades de Alojamento Local da cidade de Aveiro no sentido de perceber a

In this study, it was possible to identify alterations in the biodynamics of swallowing of cardiac infants after surgical procedure, as well as the presence of dysphagia in a high

A extração de minerais e metais de minas gera um elevado volume de lamas que apresentam uma quantidade muito signigicativa de material siltoso, conhecidas por rejeitados. Devido ao

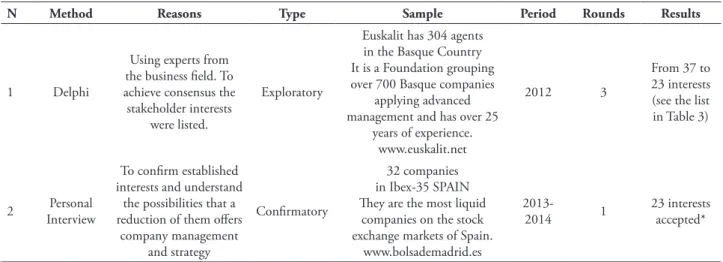

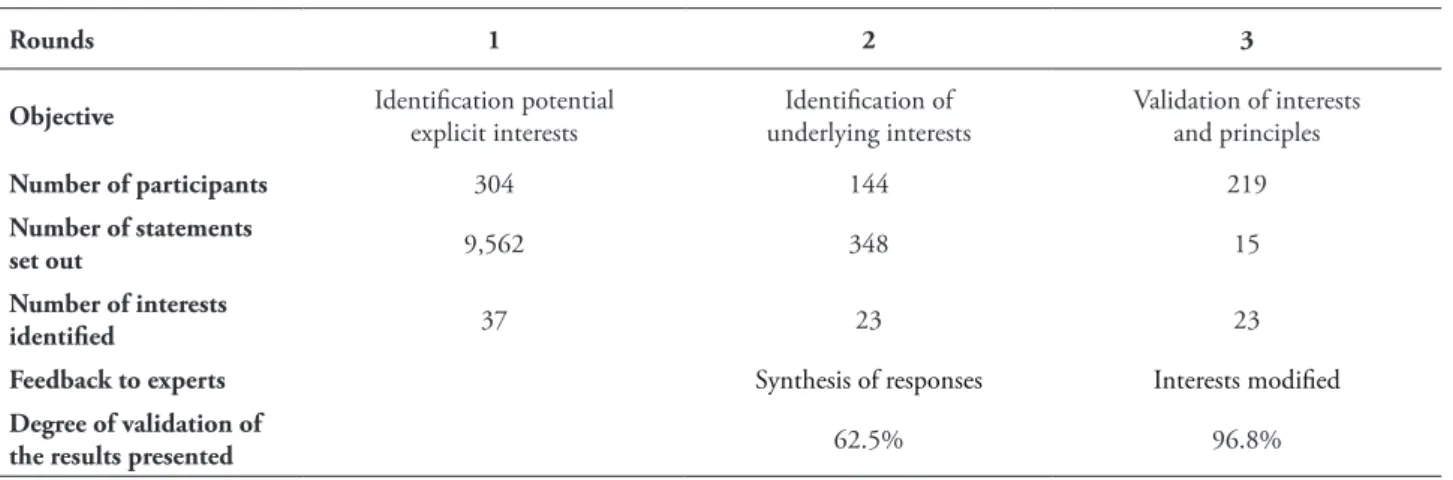

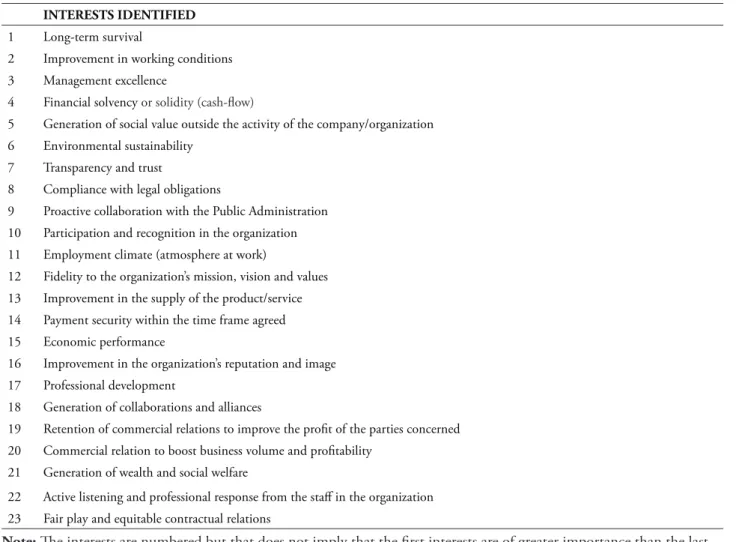

It is assumed that it is possible to identify factors (that is, the set of variables clustered in categories) that influence the implementation process of integrated

From farmland to musseque, from musseque to a modernist neighbourhood and from then to now: houses, streets and infrastructures that survived forty years of war (colonial