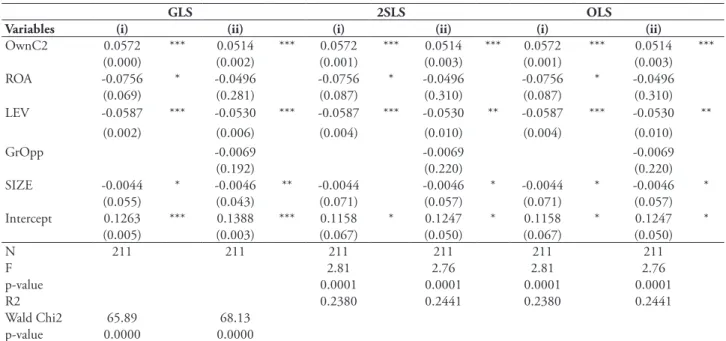

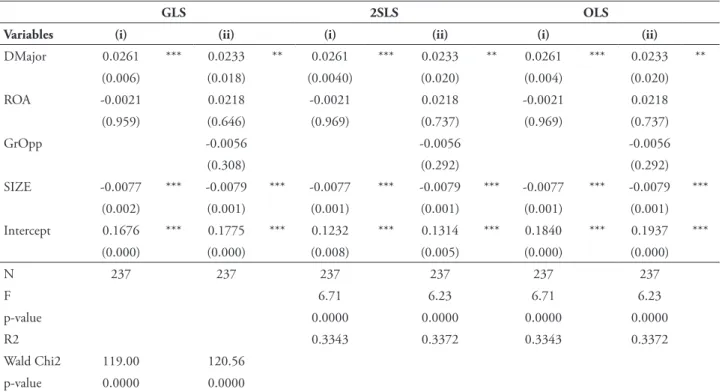

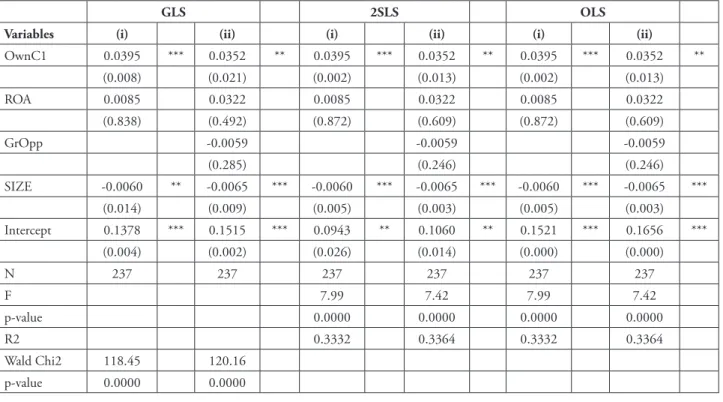

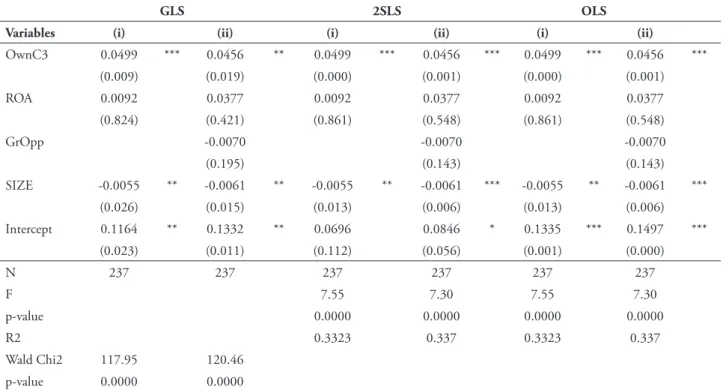

Rev. bras. gest. neg. vol.17 número55

Texto

Imagem

Documentos relacionados

MACROINVERTEBRADOS ASSOCIADOS ÀS FOLHAS EM DECOMPOSIÇÃO DE RIACHOS NEOTROPICAIS: INFLUÊNCIA DA QUALIDADE QUÍMICA, VARIEDADE DE ESPÉCIES VEGETAIS, BIOMASSA DE FUNGOS E TEMPO

Taking into account that the thermal-gradient block described by Labouriau and Agudo (1987) has been proven to be an efficient device in the studies of

Com este último ponto, sugerido em forma de questionamento, apresento descritivamente o novo “lugar” do ensino de filosofia no currículo da educação básica, tal como

Não há uma legislação específica como o decreto brasileiro 3551 de 2000: enquanto a lei brasileira cria instrumentos como o inventário e o registro de bens culturais

Os trabalhos realizados pela Inspetoria tiveram por base os dados relativos à execução orçamentária e financeira enviados por meio magnético, através do

Os municípios buscam a descentralização das ações de controle da TB para a ABS, e é de grande importância o estudo da implantação desse plano estratégico também no município

Prophylaxis has been shown to be beneficial when prenatal sonographic findings are sugges- tive of uropathies, until the imaging investigation has been completed, in the presence

VR – has the fact that electricity has been produced from nuclear energy at a moderate cost, not taking into account the costs of decommissioning and long-term management