Revista

de

Administração

http://rausp.usp.br/ RevistadeAdministração52(2017)341–352

Entrepreneurship

Are

similar

ones

different?

Determinant

characteristics

of

management

tool

usage

within

companies

sharing

the

same

institutional

environment

Os

semelhantes

se

diferem?

Características

determinantes

do

uso

de

controles

gerenciais

em

empresas

que

compartilham

o

mesmo

ambiente

institucional

¿Los

semejantes

se

distinguen?

Características

que

determinan

el

uso

de

controles

de

gestión

en

empresas

que

comparten

el

mismo

entorno

institucional

Franciele

do

Prado

Daciê

a,∗,

Márcia

Maria

dos

Santos

Bortolocci

Espejo

a,

Fernando

Antonio

Prado

Gimenez

a,

Reinaldo

Rodrigues

Camacho

baUniversidadeFederaldoParaná,Curitiba,PR,Brazil bUniversidadeEstadualdeMaringá,Maringá,PR,Brazil

Received5April2016;accepted19December2016 Availableonline15May2017

ScientificEditor:MariaSylviaMacchioneSaes

Abstract

Technicalliteraturedescribeslocalproductivearrangements (LPAs)asaninstitution.It alsostatesthatexistinginteractionlinkswithintheir membersfosterthemtoactquitesimilarly.However,entrepreneursandtheircharacteristicattributestendtodistinguishtheirdecisions.Therefore, accordingto such,thisresearchexaminedifentrepreneurpsychologicalcharacteristicswould beabletoinfluencemanagementpracticesand theperformanceofcompaniessharingthesameinstitutionalenvironment.Thisstudyfollowssuchobjectivesviaanepistemologicallypositivist approach–quantitativeview–anddatagatheringthroughformsusedin121firmsfromclothingindustryLPAinParanaNorthwest.Theresearch modelhasbeentestedthroughstructuralequationmodellingtechniques.Amongstfindings,itmaybeobservedmanagementcontrolpracticeshave a46.42%positiveeffectoncompanyperformance.Characteristicsofentrepreneurialorientationhavebeenabletopositivelyinfluencetheusageof managementcontrolsin38.38%,andcompanyperformancein14.90%.However,nostatisticalinferencesregardingtheindividual’smetacognitive abilityofpredictingthevariablesofentrepreneurialorientation,managementcontrolsandcompanyperformancehavebeencarriedout. ©2017DepartamentodeAdministrac¸˜ao,FaculdadedeEconomia,Administrac¸˜aoeContabilidadedaUniversidadedeS˜aoPaulo–FEA/USP. PublishedbyElsevierEditoraLtda.ThisisanopenaccessarticleundertheCCBYlicense(http://creativecommons.org/licenses/by/4.0/).

Keywords:Institutionalenvironment;Entrepreneurialorientation;Metacognition;Managementcontrol

Resumo

Aliteraturadescrevequeosarranjosprodutivoslocaissãoumainstituic¸ãoequeosvínculosdeinterac¸ãoexistentesentreosmembrososlevamaagir deformabastantesemelhante.Noentanto,entende-sequeoempreendedoreaexistênciadealgunsatributoscaracterísticosaeletendeadistinguir suasdecisões.Diantedessecontexto,essapesquisaverificouseascaracterísticaspsicológicasdoempreendedorseriamcapazesdeinfluenciar aspráticasgerenciaiseodesempenhodeempresasquecompartilhamummesmoambienteinstitucional.Oestudoadotaumposicionamento epistemologicamentepositivista,comabordagemquantitativaecoletadedadosoperacionalizadapormeiodeumquestionárioaplicadoem121 empresasindustriaisdoAPLdeconfecc¸ãodo noroestedo Paraná.OmodelodapesquisafoitestadopormeiodatécnicadeModelagemde

∗Correspondingauthorat:Av.PrefeitoLothárioMeissner,632,CEP80210-170Curitiba,PR,Brazil.

E-mail:[email protected](F.P.Daciê).

PeerReviewundertheresponsibilityofDepartamentodeAdministrac¸ão,FaculdadedeEconomia,Administrac¸ãoeContabilidadedaUniversidadedeSãoPaulo –FEA/USP.

http://dx.doi.org/10.1016/j.rausp.2017.05.006

Equac¸õesEstruturais.Dentreosachados,observou-sequeaspráticasdecontrolegerencialexercemefeitopositivode46,42%sobreodesempenho empresarial.Ascaracterísticasdeorientac¸ãoempreendedoraforamcapazesdeinfluenciarpositivamenteousodecontrolesgerenciaisem38,38%, eem14,90%odesempenhodasempresas.Noentanto,nãoforamrealizadasinferênciasestatísticasacercadopoderdacapacidademetacognitiva doindivíduopredizerasvariáveisdeorientac¸ãoempreendedora,controlesgerenciaisedesempenhoempresarial.

©2017DepartamentodeAdministrac¸˜ao,FaculdadedeEconomia,Administrac¸˜aoeContabilidadedaUniversidadedeS˜aoPaulo–FEA/USP. PublicadoporElsevierEditoraLtda.Este ´eumartigoOpenAccesssobumalicenc¸aCCBY(http://creativecommons.org/licenses/by/4.0/).

Palavras-chave: Ambienteinstitucional;Orientac¸ãoempreendedora;Metacognic¸ão;Controlesgerenciais

Resumen

Enlaliteraturasedefiendequelossistemasyarreglosproductivoslocalessonunainstitución,yquelosvínculosdeinteracciónexistentesentresus miembroslosconducenaactuardeunamaneramuysimilar.Sinembargo,seentiendequealgunosdelosatributoscaracterísticosdelemprendedor tiendenallevarlo adecisionesdistintas. Enestecontexto, elpresenteestudioexamina silascaracterísticaspsicológicas delosempresarios podríaninfluirenlasprácticasdegestiónyeldesempe˜nodelasempresasquecompartenelmismoentornoinstitucional.Sehaadoptadoun posicionamientoepistemológicopositivista,conunenfoquecuantitativoysehanrecogidolosdatospormediodeuncuestionarioaplicadoa121 empresasindustrialesdelAPLdeconfeccióndelnoroestedelestadodeParaná.Elmodelodelestudiosehapuestoapruebapormediodela técnicademodelosdeecuacionesestructurales.Entreloshallazgos,seobservaquelasprácticasdecontroldegestióntienenunefectopositivodel 46,42%enelrendimientoempresarial.Lascaracterísticasdeorientaciónemprendedorahansidocapacesdeinfluirpositivamenteenelusodelos controlesdegestiónenel38,38%,yenel14,90%elrendimientodelasempresas.Sinembargo,nosehanrealizadoinferenciasestadísticassobre elpoderdelacapacidadmetacognitivadelindividuoparapredecirlasvariablesdeorientaciónemprendedora,controlesdegestiónyelrendimiento empresarial.

©2017DepartamentodeAdministrac¸˜ao,FaculdadedeEconomia,Administrac¸˜aoeContabilidadedaUniversidadedeS˜aoPaulo–FEA/USP. PublicadoporElsevierEditoraLtda.Esteesunart´ıculoOpenAccessbajolalicenciaCCBY(http://creativecommons.org/licenses/by/4.0/).

Palabrasclave: Entornoinstitucional;Orientaciónemprendedora;Metacognición;Controldegestión

Introduction

The establishment of business conglomerates,also known aslocalproductivearrangements(LPA),isaproposal consid-eredaswidelyviabletoorganisationssearchingforrendertheir operations within dynamic, unstable and highly competitive environments (Cassiolato &Szapiro, 2003). Such configura-tionpromotesstrengtheningoflocaleconomies,thearticulation, interaction,cooperationandlearningamongmembers,besides fosteringthesharingofcommonelements–suchasemployees, suppliersandsponsors(Cassiolato,Lastres,&Szapiro,2000). TherearemanyfactorswhichinstigatestudiesregardingLPAs –speciallytheanalysisofitshighlyinnovativelocalprofileand thetendencyoftheirmemberstoestablishconnectionstowards financialandoperationalgrowth(Cassiolato&Szapiro,2003). Moreover,asconsequenceoftheinteractionprocesswithin this environment,LPAs present characteristics whichqualify themasinstitutions;and,members–withinsuchenvironments– presentbehaviourbasedonmodelscreatedordevelopedin inter-action(Cassiolatoetal.,2000).TheNewInstitutionalSociology (NIS) supports such concept discussing formal and informal demands within institutions, leading local members towards parameterisedactions(Dimaggio&Powell,1983).

Furthermore,thisscenarioisadjoinedbythesuggestionthat dailypracticesare adoptedinmanagementprocesses towards objectives,strategies,and, consequently,betterperformances; withinsuchconditions,literatureupholdsmanagementcontrol usagemaysignificantlyimprovedailyoperationsand informa-tionalmanagement requirements(Frezatti,Carter, &Barroso, 2014; Otley & Berry, 1980). According to NIS, Oyadomari,

Cardoso,Mendonc¸aNeto,andLima(2008)affirmthat, simi-larlytoinstitutionalisedbehaviourpatterns,theenvironmentin whichorganisationsworkmayalsoinfluenceselection,adoption andusageofmanagementtools;whichinitiallysuggests organi-sationswouldhaveasimilarbehaviourregardingmanagement processtoolswithinbusinessconglomerates.

However,researchesstressimplementationofmanagement tools insmallercompanies isoftenflawedduetothe incom-prehension regarding usage and interpretation of available information, fostering alternative management practices, or even decision-makingthrough business acumen (Dyte,2005; Mehralizadeh&Sajady,2006;Stroeher&Freitas,2008). There-fore,the institutionalapproach–centredonstressingrational structureswhichsculptorganisationalbehaviour–may,perhaps, ignorethefactthatcompanymanagementoccursthroughpeople (speciallytheentrepreneur.)Therefore,itmakessensetoreason people have distinct profilesand their actions are provenient fromcognitiveprocessessuchasrelationswithsocialgroupsor previousexperiences(Estes,1975).

Moreover,theentrepreneurisseen–inliterature–asa dif-ferentbeing,havingtheindependentcapabilityofdefiningand establishing mechanisms towards decision-making processes (Kets de Vries, 1977). Researches about behaviour state the humanbeingisrationallyabletounderstandhis/herknowledge andoptforthebestalternativetowardsproblemsolving, sug-gesting entrepreneurs may be less vulnerable toenvironment influencesandmoreselfsteeredtowardstheirownwill(Flavell, 1979;Lumpkin&Dess,1996;Miller,1983).

influence towards breaking the paradigms regarding action reproduction of companies within an institutional environ-ment; hence producing effects on management practices in his/herenterprise.Literaturesupportstwoattributes are note-worthyinsuchperson:(1)metacognitionand(2)entrepreneurial orientation (Flavell, 1979; Lumpkin & Dess, 1996; Miller, 1983). The former states a human being is able to under-stand; become aware; and, control processes of evaluation and decision-making (Estes, 1975): whilst the latter regards noteworthy abilities within entrepreneurs (Lumpkin & Dess, 1996; Miller, 1983). Ipso facto, the question this research aims to answer is: do entrepreneur psychological character-isticsregardingentrepreneurial orientationandmetacognition affecttheusageofmanagementcontrolandtheperformanceof companiessharingthesameinstitutionalenvironment?

Moreover, this investigation is supported by many moti-vations. Considering the concepts made known by the New InstitutionalSociology,onemayempiricallyassumecompanies locatedwithin clothingindustryLPAinParana State– target populationrange–adoptsimilarmanagementpractices, prove-nientfrominteraction,cooperationandinternalisationoflocal knowledge(Dimaggio&Powell,1983).However,thestudyof conditions which are likely to break/dismiss this isomorphic paradigm is still within its infancy; however able to distin-guishsignificanttheoreticalcontributions.Timelythethorough discussionregardingthecomplexityofinterpretationand obso-lescenceofmanagementreportswasusedtoponderaboutthe existenceofalternativeandsimplifiedinternalcontrolswith sim-ilarfunctiontotheonessupportedbytheory–designatedwithin thisstudyasmanagementcontrolproxies(Dyte,2005;Frezatti etal.,2014).Atlast,theselectedresearchenvironmentisknown as the largestnational complex of clothing industry (MDIC, 2006),aconditionwhichfostersnewinvestigationsduetothe significant environmentcondition anddueto the opportunity toconnectpractical reality adoptedindecision-making situa-tionstotheoreticalknowledge,thusfosteringtheadvancement ofknowledge.

Inthiscontext,thispaperisstructuredwithinfoursections inadditiontothisintroduction.Thenextsection presentsthe theoreticalreferenceinwhichtheresearchisbased,aswellasits hypothesis;thethirdonepresentsresearchprocedures;thefourth onepresentsthedescriptionandanalysisofresults;and,atlast, therearefinalconsiderations pointingout papercontributions towardsknowledge,furtherstudysuggestionsandlimitation.

Theoreticalbackground

Inthissection thereare previousstudiesregarding institu-tionalenvironmentmanagementcontrolusageandorganisation entrepreneurprofileaspects.Basedonsuchliterature, hypothe-seshavebeensuggestedand,afterwards,verified.

Managementcontrolusagewithininstitutional environments

Theusageofmanagementcontrolswithinorganisation man-agementcompriseswidesupportmechanismstoactionplans,

informationsystematisation,sponsoringplanningactivity, mon-itoringandoperationcontrol,aswellasmanagementfunctions (Frezattietal., 2014;Mehralizadeh&Sajady, 2006;Otley& Berry, 1980). However, empirically, evidences are presented showinglowusageofformalmanagementcontrolwithin organi-sations–speciallysmallerones(Dyte,2005;Stroeher&Freitas, 2008). Researches such as the ones from Kassai (1997) and StroeherandFreitas(2008)stressaccountingreportsareseenas difficulttoolstointerpret,causingaversiontotheirusage. Alter-natively,itmaybeinferredsimplertechniquesappearinorderto supportorganisationmanagement(Frezattietal.,2014).Within such conception, thisstudy understands management control are practicestheoreticallyspreador adapted toorganisational environment– as longas theycontribute, somehow,tofoster operationmanagement.

Relationsbetweenmanagementinstrumentusageand com-pany performance have been acknowledged for a long time (Ashton,1974;Chenhall&Langfield-Smith,1998;Chenhall& Morris, 1986;Mehralizadeh&Sajady, 2006).With itsusage, useful information towards task improvement is made avail-abletomanagers,whomaydecidethemostadequateactions forbetterperformance(Ashton,1974).Moreover,management toolspotentiallyandsimplycontributetoorganisational perfor-mancefollow-up(Chenhall&Langfield-Smith,1998).Within smallcompaniestheybecomeprompttoolsforsurvival,mainly towardssuperiorincomes(Mehralizadeh&Sajady,2006).Thus, thisstudysuggeststhefollowinghypothesis:

H1. Theusageofmanagementcontrolproxiesdoesinfluence theperformanceofcompanieslocatedintheclothingindustry LPA.

Furthermore,thefactthatwithinorganisationalenvironment therearenoregulationstostandardisetheusageand manipula-tionofmanagementcontrols–noteworthyvariationsuggesting theinfluenceofmanagerprofileoveritsusageonorganisations – is considered. Power attributed to such person and auton-omyoncoordinationanddeliberationofoperationsarefactors alreadyestablishedascounterpointtothetraditionalapproach ofinstitutionaltheory.Therefore,discussionasKassai(1997), Stroeher and Freitas (2008), and, Frezatti et al. (2014) sug-gestitiscommonentrepreneursoptfortheproductionoftheir owninformation,or,additionally,supporttheirdecision-making processonintuition.Then,informationalbackingwithindaily actionsmaybecognitivelyconditionedbyknowledgeand expe-rience, eventhoughwhenever submittedtothe strengthof an institutionaldimension.

Theentrepreneurprofilewithinorganisations

practices anddecision styles (Miller, 1983).These andother characteristicswithinentrepreneurshipactionsareincorporated totheentrepreneurialorientation(Lumpkin&Dess,1996).

Seminally, Miller (1983) empirically measures entrepreneurial orientation (EO) within three dimensions, (1) risk-taking, (2) proactiveness, (3) innovativeness. After-wards,LumpkinandDess(1996)exploredthethemeandadded twofurtherrangestosuchvariables:competitiveaggressiveness andautonomy.Insuchsense,EOhasbeenintenselyexplored withinorganisationalanalysisandithasmappedasasignificant tool towards better company operation performance in com-paniesaroundtheworld(Cho&Jung,2014;Rauch,Wiklund, Lumpkin,&Frese,2009;Wiklund&Shepherd,2003).

Researches such as performed by Wiklund and Shepherd (2003) with Swedish companies, demonstrated the positive effectintherelationbetweenEOandperformance.Rauchetal. (2009),concluded – through ameta-analysisof 51 investiga-tions– thatthereisamoderatelylargecorrelationamongthe resultsofstudieswhichcoverbothdiscussionvariables. More-over,asurveycarriedoutbyChoandJung(2014)within190 Americanbusinessmenhasalsoshownthepositiveeffectfrom theseconstructanalysis.Basedonsucharguments,thesecond hypothesisisformulated:

H2. The entrepreneurial orientation of the entrepreneur–businessman does influence the performanceof companieslocatedintheclothingindustryLPA.

Literature states rationality as a representative motiva-tionalfactortowardssearchingforideasconsideredinteresting or worthy by entrepreneurs. Accordingly, Haynie, Shepherd, Mosakowski, and Earley (2010) state such people apply their cognitive strategy towards promoting new bonds with potential opportunities. Works regarding relations between entrepreneurialorientationandmanagementcontrolusagestress therelevanceininvestigatingsuch subjects(Li,Liu,&Zhao, 2006;Spillecke&Brettel,2013).Lietal.(2006),when conduct-ingaresearchwithinproductdevelopmentandhumanresource sectors,haveobservedapositiveeffecttowardscompany oper-ations when entrepreneurial orientation characteristics were observedinactivities.Accordingly,SpilleckeandBrettel(2013) haveconductedananalysisinthesalesdepartmentof268 orga-nisations,alsoascertainconfirmingEOusageovermanagement controlinsuchdepartmentswas representativetowardsbetter organisational performance. The described scenario suggests managementcontrolusagemaybeinfluencedbyentrepreneurial orientation when business performance improvement is the objective.Duetotheoreticalandempiricalevidence,thethird hypothesisissuggested:

H3. Entrepreneurial orientation influences manager– entrepreneurswithincompanieslocatedintheclothingindustry LPAtousemanagementcontrolproxies.

Inaccordancewiththediscussionregardingthemain func-tionofmanagers–decision-making–studiessuchasShane’s andVenkataraman’s(2000)describetwo mainfactors, intrin-sictohumanbeings,whichareabletointerfereinopportunity discerning:(1)possessionofnecessaryinformationtoidentify

anopportunity,and,(2)cognitivepropertieswhichallow infor-mationexploration.Inviewofthisinvestigationscenario,itis understoodthefirstconditionmaybemetthroughmanagement controlusage,asalreadyexplained.Moreover,thestudyof psy-chologicalelements–herebydefinedasmetacognitivefactors– seemstoefficientlyfulfiltheanalysisofcognitivefactors.The conceptionofsuchtermregardsthecomprehensionprocessof cognitivecapacity,awareness,andcontroloverdecision-making (Estes,1975).

Inviewofthissuggestion,itisbelievedthatanindividual’s cognitiveinterpretationtowardsaspecificscenario,thatis,the presence of moreor less refined metacognitive abilities,may generatedistinctwaysofactingwithinaspecificsituation–as inthiscase,occurringregardingmanagementcontrolproxies. Studiessuggestmetacognitiveabilitiesmayguidehumanbeings towardsbeingabletorecallsolutions,and,tochoosethemost adequateone(Haynie,2005;Haynieetal.,2010).Inviewofsuch understanding,fiverangesaresupportedbyFlavell(1979)for evaluation:(1)goalorientation,(2)metacognitiveknowledge, (3) metacognitivestrategy,(4)metacognitiveexperience, and, (5)monitoring.

Accordingly,Nelson(1996)stresseshumanbeingmonitoring abilitiestakealsoexpressivefunctionsassignallingfor motiva-tionalre-evaluationforthetargetand/orfortheotherranges,for, according toachievedperformancetowards agoal, strategies conceivedforfurtheractionsmaybealtered.Itisunderstood, hereinbefore, manager metacognitive abilities may influence management control practices, once its usageusefulness and relevancearecognitivelydiagnosedtowardsthe improvement ofmanagementprocessesandbetterdecision-making.Support withinliteraturehasnotbeenfound;however,thisnoteworthy optionshallbeexploredthroughthefollowinghypothesis:

H4. Manager–entrepreneurmetacognitioninfluences manage-mentcontrolproxiesusageincompanieslocatedintheclothing industryLPA.

In accordance towhat has been discussed, metacognition may be perceived as potential element for individual adap-tation towards company environment (Haynie et al., 2010). ThenationwidestudyofLimaFilhoandBruni(2014), empir-ically supports this idea: findings demonstrate 42.79% of entrepreneurial characteristics maybe explained by manager metacognitive perspectives; furthermore, there are interna-tional findings confirming metacognitive ability effects on entrepreneurial orientation(Cho&Jung,2014;Haynie etal., 2010). Moreover, there are researches not suggesting direct relationsamongthevariables;albeit/notwithstanding metacog-nition supportingrolewithinentrepreneurial action(Shane& Venkataraman,2000;Wiklund&Shepherd,2003).Timely,the fifthhypothesisisconstructed:

H5. Manager–entrepreneurmetacognitioninfluenceshis/her entrepreneurialorientation.

incorporate them within their next actions (Batha &Carroll, 2007; Melot, 1998; Schraw& Dennison, 1994).Schraw and Dennison (1994) perceive metacognitive awareness, that is, the way an action is performed and the interpretation of its consequences, as positively related to flexibility in decision-making.Melot (1998) adds this variable is able to influence thesensitivityandreceptivityofenvironmentfeedback, improv-ingfurtherdecisions.BathaandCarroll(2007)observepeople withlow metacognitiveabilities oftenestablishflawed strate-gies or present difficulties within unreliable environments. It maybehereuponexploredif improvedperformancesmaybe observedfrommindfulactions.Therefore,thelasthypothesisis suggested:

H6. Manager–entrepreneurmetacognitiondoesinfluencethe performanceofcompanieslocatedintheclothingindustryLPA.

In the end of the section, the discussion is based on the assumptionelementsintegratingthe institutionalenvironment of the LPA follow a parameterised behaviour model, essen-tiallyinasmuchasmanagementpracticeusage,inaccordanceto theNISisomorphicconcept.Alternatively,itisunderstoodthe entrepreneurpossessesdistinctivecharacteristics,beingableto upholdattitudesconsideredideal,byhimself.Thus,theadopted positioningdeterminesmetacognitionandentrepreneurial ori-entationas attributeswithinwaysofactingandreasoning;for theseelementsmayoppose theformalstructure of behaviour imitationifitexertsanyeffectsontheusageofauxiliary manage-mentinstruments:suggesting,then,some‘rethinking’regarding institutionalenvironmentgeneralisation.

Methodology

Researchstructuralmodelanddatagatheringprocedures

This study adopts Institutional Theory as subjacent to the analysed environment. The NIS isomorphic concept upholds organisationsare configuredunder alargeand inter-organisationalrelationshipnetwork,and,practicesandroutines would be legitimised by social actors (Dimaggio & Powell, 1983).However, differently, the objectof thisresearch – the entrepreneur– seemstopossesssomedistinctcharacteristics: theentrepreneurialorientationandmetacognitiveabilities.This conceptfostersmoreprecisescenarioexploration,verifyingif hisattributesare,somehow,abletoaffectlocalcompany man-agementcontrols.

The work takes an epistemological positivist approach, withquantitative problem approach, strategies for data gath-eringanddataanalysis throughstructural equation modelling (SEM). Thesecriteria have been adopted towardssuggesting a new perspective regarding action imitating within institu-tional environment under the assumption psychological and behaviouralentrepreneurcharacteristics(entrepreneur orienta-tionandmetacognitivecharacteristics) haveanimpactonthe aforementionedperson.

Testing of hypothesis H1–H6 has been carried out by a research instrument structured in four groups, being formed by 55 statements regarding the following constructs:

metacognition,entrepreneurialorientation,and,proxiesof man-agement control and performance. A range from 0 (zero) to 10 (ten) pointsmeasures the agreement level towards the entrepreneurwaysofacting,thinkinganddeciding,with prac-ticesrelatedtobusinessmanagementandbusinessperformance perception.Picture1showstheresearchdefinedstructuralmodel whichgeneratedtheform.

Apre-testcarriedoutwithfiveprofessionals(fromthe fol-lowing areas: accounting, finance, market anddesign), being twoofthemmanager–entrepreneurs,grantedvaluable contrib-utionsandconfirmedthevalidityofexpressionoftheinstrument. The suggestions obtained fromthis researchstagewere duly discussed amongthe participantsand some terms have been modified(proxyconstructsofmanagementcontroland metacog-nition)fortheywereconsideredincomprehensibleorwithtoo complexalanguageforthetargetpopulation.Besides,through thisproceduretheaveragenecessarytimeforfillinguptheforms wasestimatedin25min.Theinstrumentwasalsosubmittedto thescrutinyofareaprofessorsandresearcherstowards validat-ingofquestioncontent(Hair,Black,Babin,&Anderson,2010). Itisconvenienttoclarifyallquestionnairesansweredwithinthis procedure havebeen consideredinvalid onSEM application. Furthermore,theconstructsfollowedthecriteriaof identifica-tion validity according to Hairet al. (2010), whichsuggests variablesmeasurementtobeconstitutedbythreeorfour indica-tors(statements/enquiries).Thestructureoftheinstrumentused indatagatheringisshowninTable1.

Datagatheringwascarriedoutfrom20thofOctober2015and 20thDecember2015fromentrepreneur–managerswithin com-paniesbasedintheclothingindustryLPAinParanaNorthwest (CianorteandMaringá).Thedefinedpopulationwas organisa-tionsrangedas industrialandregisteredwithintheir category representativeunions:SINVESTE(SindicatodasIndústriasdo VestuáriodeCianorte),SINDVEST(SindicatodaIndústriado Vestuário de Maringá); andassociated toACIM (Associa¸cão ComercialeIndustrial de Maringá).In total, 136 companies registeredinSINVESTEand116companiesrelatedto SIND-VESTandACIMwerechosen.Sampleselectionwasdoneby accessibility, either telephone contacts or in loco visits have been carriedoutinorderto,primarily, invite organisationsto takepartintheresearch.Incasetheyaccepted,appointments were scheduled to form filling. It is convenient tostress the foundermanagerandcompanycapitalinvestorwasdefinedas the potentialresearchrespondent– and,therefore,considered asentrepreneur–managerwithinthisresearch.Wheneversuch contact was notpossible, duetosuccession reasons,the cur-rentmanager(children,grandchildren,andfamily)wasinvited fortheresearch.Finalsamplingcovered121companies,67in Cianorteand54inMaringá.

Table1

Constructsappliedinresearchdesignoperationalization.

Constructs–1storder Constructs–2ndorder Numberofindicatorsa Questions Theoretical/empiricalsupport

Managementcontrolproxies Planning 3 1–3

Dyte(2005)

MehralizadehandSajady(2006) StroeherandFreitas(2008)

Financialandaccounting 4 4–7 Marketandclients 3 8–10

People 3 11–13

Process 3 14–16

Entrepreneurialorientation Proactiveness 4 17–20

Miller(1983)

LumpkinandDess(1996)

Risk-taking 3 21–23

Autonomy 3 24–26

Competitiveaggressiveness 3 27–29 Innovativeness 4 30–33

Metacognition Goalorientation 4 34–37 Flavell (1979) Haynie and Shepherd (2009)

Metacognitiveknowledge 4 38–41 Metacognitivestrategy 3 42–44 Metacognitiveexperience 4 45–48

Monitoring 4 49–52

Organisationalperformanceb Environmentorganisation performanceb

3 53–55 LumpkinandDess(1996) SpilleckeandBrettel(2013)

aNumberofindicators.

b Performanceconstructmeasurementapproaches:

(i)Theobjectivefinancialreturnreachedentrepreneurexpectations; (ii)Therewasanincreaseinmarketshare;

(iii)Clientsatisfactionimprovementtowardscompanyproducts.

sizeanalysis towardsvalidating statisticalpowerwithin SEM estimationhasoccurredviaG*Power3.1.9software.The fol-lowingparameterswereconsidered:(1) testpower=0.95;(2) effectsize(f2)=0.15;and,(3) thelargestnumberof predictor variable=3(performancevariable)(Hairetal.,2014).After cal-culations,thesoftwareindicated119observationswouldmeet analysisobjectives,confirmingthenumberofapproacheswould beenoughtoanswerthesuggestedmodel.

Proceduresadoptedinstructuresofstructuralequation modelling(SEM)

The structural equation modelling (SEM) is a relevant testtechniquefor theoreticallyestimated models.Thecurrent researchusespartialleastsquare(PLS)asadjustmentmethod, as it is the most adequate within studies with non-standard normaldistribution(itdoesnotpre-considerdistribution),and less demanding regarding sample sizing when compared to maximum-likelihoodestimation(Hairetal.,2010).

InaccordancetoindicationspriortoSEMinSmartPLS (esti-mationstowardsmeasuringthe“strength”ofeachindicator),a confirmatoryfactoranalysis(CFA)wasestimatedviaSPSS (Sta-tisticalPackagefortheSocialSciences)forquestionsregarding the constructsof 2ndorder. It isimportant tonoteeach con-structof2ndorder(withexceptionofperformance–seeFig.1) was measured from three or four questions, totalising a 52-assertivemodel.CFAwas,then,appliedtoeachassertivegroup whichmeasuredtheirrespective2ndorderconstructwithinthe questionnaire,groupingeach questionresultswithinonlyone measurementunity– onefactorfor each2ndorderconstruct. Theprincipalcomponentextractionmethodwasusedandthe

H3

H5

H4

H6

H1 H2

Entrepreneurial orientation

Metacognition

Management control proxies

Organisational performance

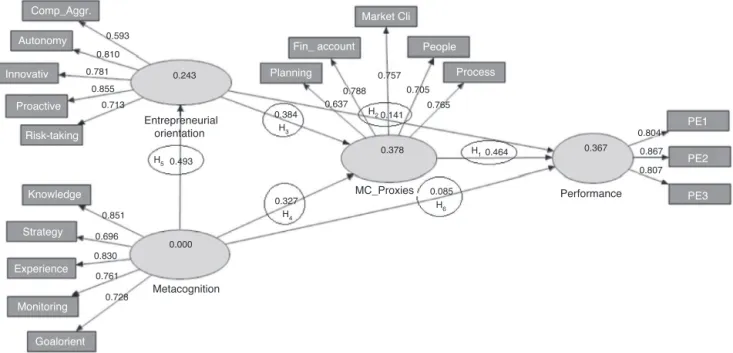

Fig.1.Structuralmodel/researchoutline.

variableshavenotbeenrotated(Hairetal.,2010).ThefactCFA wasnotusedintheperformancevariablewasratified,onceitwas measuredbyexactlythreeindicators(statements/questions).

Theaforementionedprocedureresultsgenerated15factors: fiveofthemregardingmanagementcontrolproxies(planning, financeandaccounting,marketandclients,people,processes), fivefor entrepreneurialorientation(proactiveness, risk-taking, autonomy, competitive aggressiveness, innovativeness), and, five for metacognition (objective orientation, metacognitive knowledge, metacognitivestrategy,metacognitive experience, monitoring).Obtainedresultshavebeensavedwithinthe soft-ware and, from then on, became defined as indicators for measurement for each respectivelatent variable(construct of 1storder)withinthepathdiagraminSmartPLS.

Dataanalysis

Table2

Companydemographicdata.

Basecity Number Percentage Constitutiontime

Cianorte 67 55.37% Average 14years Maringá 54 44.63% Min 3months

Max 50years Total 121 100% Mode 15years Income Number Percentage

≤R$2.4million 84 69.42% >R$2.4millionand≤R$16million 28 23.14% >R$16millionand≤R$90million 9 7.44%

Total 121 100%

Sampledescriptiveanalysis

Informationwithinthissection describesrespondentsocial and demographic characteristics and the configuration of researchedcompanies.Thesamplecovered121organisations, whereas64of them(52.89%)weremanagedbywomen,and, 57(47.11%)bymen.Theinterviewedhaveanaverageageof 41yearsold,rangingfrom21to67yearsofageand49wasthe mostfrequentage.Regardingacademicbackground,27 partici-pants(22.32%)arespecialist/post-graduated,44(36.36%)have finishedhighschool,andthe totalof 50(41.32%) are gradu-atedoraregraduating.Additionally,Table2presentsrespondent characteristics.

The survey hasverified, as inaccordance toTable 2, that research samples range from 55.37% of organisations based in Cianorte and 44.63% in Maringá, with and average con-stitution time of 14 years (data range from 3 months to 50 years).Categoriesregardingannualgrossincomeshow respon-dentcompaniesaremainlycategorisedasmicroandsmallsized enterprises,withexceptionof 7.44%ofcases–consideredof mediumsize.Itisimportanttostressthe samplecovers orga-nisationswithheadquartersinCianorteandshopsinMaringá, andviceversa.Theapproachofthesecaseshasconsidered,for descriptionparameters,thelocalofadministrativeoffice.

Structuralequationmodelling(SEM)analysis

Aftersavingtheresultsobtained fromfactors,asdescribed in“Proceduresadoptedinstructuresofstructuralequation mod-elling(SEM)”section,validityofmodeladjustmentconditions weretestedwithinevaluationsofmeasurementmodelandpath modelling(Henseler, Ringle,& Sinkovics, 2009).Regarding the first criterion, the model meets the order condition, pre-sentingmoredegreesoffreedom(df)thanpathstobeconsidered, and,establishingtheGof (Goodnessof Fit– Gof)ratehigher than 0.36 (χ2 average=0.3842) (Hair et al., 2010; Wetzels,

Odekerken-Schröder, & Van Open, 2009:187). Besides, the valuefoundfor theabsolute fitindicator SRMR(Standardise RootMean Residual)was of 0.075, inaccordancewith stan-dardsof ameasurementmodel withgood adjustment(values until|0.08|)(Hairetal.,2010).

Table3

Convergentvalidityofthemodel.

Latentvariables AVEa CRb R2c Cronbach’s

alpha Performance 0.6831 0.8660 0.3665 0.7690 Metacognition 0.6005 0.8820 0.000 0.8332 Entrepreneurial

orientation

0.5715 0.8679 0.2434 0.8187 Management

controlproxies

0.5364 0.8519 0.3783 0.7873

aAveragevarianceextracted. b Compositereliability. cCoefficientofdetermination.

Hairetal.(2010)suggestmeasurementmodelvalidationto becarriedoutbyanalysisofaabsolutefitindexandoftwo incre-mentalindicatorsorqualityones(ComparativeFitIndex–CFI, GoodnessofFitIndex–GFI,NormedFitIndex–NFI,among others).Duetodatapreviouslypresentedinthelastparagraph, theabsenceoffurtherindicesisjustified–fortheadopted soft-wareusedforSEManalysisdoesnotsupplyenoughdatatowards identifyingfurtherindices.Suchlackofinformationstressesthe writers, Hairetal.(2010)alsostate the exclusiveanalysisof theseindicatorsisnotenoughtovalidateagoodmodel adjust-ment;however,parameterestimatesshouldbeanalysed–astep tobeconfirmedintheevaluationofthepathmodellingtofollow. The second condition to be investigated is the construct adequacyvalidity–measuredthroughconvergentvalidityand discriminantvalidity.Inordertotestthefirstitem,theindicators ofeachlatentvariable(LV)ofthemodelwereverifiedtoconfirm theysharestandardvariancethroughfactorloadinganalysisof eachindicator,throughaveragevarianceextracted(AVE)from thelatentvariablesandthroughcompositereliabilityindex(CR) (Hairetal.,2010).Table3presentstheresults.

Regardingfactorloadings, all indicatorsappearas statisti-callymeaningfulinthemodel,thatis,withvaluesequalorhigher than0.50.Furthermore,mostofindicatorsfulfilledideal con-ditions tofactor measurement(loadings above 0.70),and, as exceptionthereare: proactiveness(entrepreneurial orientation LV), planning(management control proxyLV) and metacog-nitivestrategy(metacognitionLV)(Henseleretal.,2009).The modelalsofulfilsAVEacceptablelevels,withvaluesequalor higherthan0.5(Fornell&Larcker,1981).CRalsofulfils sat-isfactory standards(0.70–0.90), proving the“strength” which relatesLV totheir indicatorsissufficientlyabletomeasureit (Henseleretal.,2009).

Table4

Discriminantvaliditytestresults–FornellandLarcker(1981).

Entrepren_orientation Metacognition

Performance

Latent variables a MC_proxiesb

Performance 0.8265 0.3944

Metacognition 0.7749 0.4934

0.4360

Entrepren_orientation 0.7560 0.5452

0.5166 0.5850

MC_proxies 0.7324

Correlationstolevelα=0.05. aEntrepreneurialorientation. bManagementcontrolproxies.

Table5

Matrixcrossloadingsofdiscriminantvalidity–Chin(1998).

Performance

Indicators Metacognition Entrepren_orientation MC_proxies

PE_1 0.8044 0.2514 0.3333 0.4465

PE_2 0.8670 0.3292 0.3288 0.4563

PE_3 0.8066 0.3826 0.4076 0.5346

0.2744

Goal orientation 0.7247 0.4142 0.3371

0.3610

Metacognitive knowledge 0.8512 0.4830 0.4335 0.1810

Metacognitive strategy 0.6960 0.2388 0.3341 0.3075

Metacognitive experience 0.8301 0.3916 0.4300 0.3642

Monitoring 0.7612 0.3421 0.4493

0.5231 0.4627

Proactiveness 0.8549 0.5761

0.2737 0.2386

Risk-taking 0.7134 0.2760

0.3742 0.2340

Autonomy 0.8103 0.3301

Competitive aggressiveness 0.1561 0.5926 0.1788 0.1754 0.3737

0.4037

Innovativeness 0.7810 0.5019

0.3100 0.3767

0.2659

Planning 0.6366

0.4998 0.4334

0.5655

Financial and accounting 0.7877

0.4811 0.3455

0.4141

Market and clients 0.7575

0.2706 0.2477

0.3046

People 0.7052

0.3697 0.4479

0.4952

Processes 0.7648

isfreefrombias,andthedatagathering instrumentisreliable (Hair,Hult,Ringle,&Sarstedt,2014).

Besidesconvergentvalidity,thereisaprocedurewhichalso guarantees the construct suitability validity: this second pro-cedureisthediscriminantvalidity.Thus,thefulfilmenttothis condition guaranteesthe model presentsaconstruct whichis distinct from others, that is, each LV does measuredifferent “things”(Hairetal.,2014).Withinsuchprocedure,thecriteria suggestedbyFornellandLarcker(1981)andbyChin(1998)are checked.ThefirstofthemispresentedinTable4.

According to Fornell and Larcker (1981), Table 4 shows squarerootsofAVEsvalues(shadedfigures)arehigherthanthe correlationbetweentheLVofthemodel(lowerportionoftable). Suchinferences demonstratesuch model is effective towards fulfilling the parameters, and, so far,there is no evidenceof problemsregardingdiscriminantvalidity.Additionally,Table5 shows variable matrix cross loadingsresult, as suggested by Chin(1998).

InaccordancetoChin(1998),Table5showsfactorloadings ofrespectiveindicatorsof eachconstruct(shaded figures)are higherthantheirfactorloadingsdistributedamongfurtherones, indicatingtheinexistenceofanycrossloadingsamongmeasured variablesoramongtermsoferrors.Therefore,thisascertainment verifiedthroughTables3and4ensurethediscriminantvalidity withintheconstructsuitabilitymodel.

Bootstrappinganalysis,nextusedvalidationtechnique, per-mits the testing of relation significance among constructs – identifying the existence of further variables (not measured within the model), which maysignificantly interferetowards deeperrelationsofthetheoreticalproposition(Henseleretal., 2009).Therefore,fromZvalues,tworelationswereverifiedas maybe partially compromised (Z testwith values lowerthan 1.96): (1) metacognition– performance (Z=1.1969) and (2) entrepreneurial orientation– performance(1.6028).However, evenifvalueslowerthan1.96presentevidencessothatthenull hypothesisisnotrejected,and,thatothervariableswithfurther relations within the model mayexist, it is believed this sce-narioisalsoderivedfromthelowercorrelationamongLVs – respectively0.3944and0.4360(asinTable4).Oncenoother evidenceinvalidating themodel hasbeenobtained,suggested relationshavebeenkept.

Comp_Aggr.

Autonomy 0.593 0.810

0.781

0.855

0.713

0.243

0.493

0.327

0.085 0.384

0.637 0.788

0.757 0.705

0.765

0.378 0.464 0.367

0.804

0.867

0.807 0.141

0.851

0.696

0.830

0.761

0.728

0.000 H5

H4

H1

H6 H3

H2 Innovativ

Proactive

Risk-taking

Entrepreneurial orientation

Metacognition

MC_Proxies Performance

PE2

PE3 Knowledge

Strategy

Experience

Monitoring

Goalorient

Planning Fin_ account

Market Cli

People

Process

PE1

Fig.2.Relationspresentedonresearchstructuralmodel.

Table6

Predictivevalidity(Q2)andeffectsize(f2).

Latentvariables Predictivevalidity(Q2) Effectsize(f2)

Metacognition 0.4040 0.4040 Entrepreneurialorientation 0.1190 0.3520 Managementcontrolproxies 0.1720 0.3040 Performance 0.2280 0.3510

proxyfulfilaverageparameters(0.15<f2<0.35)(Ringleetal., 2014).Table6presentssuchindices.

Aftervalidationconfirmationofthemodelandtheconstructs, thenextstepwasthepathcoefficientanalysis,identifyingthe levelwhereLVisforecastbyother.Thehypothesesformulated withinthisstudyhavebeentestedthroughStudent’st-test, defin-ingα=0.05fortype1erroroccurrence.Thereforehypothesis

withZvalueof1.96orhigherhasbeenconsiderednotrejected, indicating the alternative hypothesiswithin thisresearch has been confirmed. Meaningfuleffects within relations are pre-sentedandevidenced(shadedfigures)inTable7.

Findingsposteriortoaforementionedanalysishave permit-ted some inferences: among them, it was verified personal entrepreneurial characteristics are able to forecast 8.38% of interviewedmanagementcontrol.Besides,thevariableisable

to influence in 14.09% towards organisational performance. Regardingmanagementcontrolusageanditseffectover busi-nessperformance,therelationswerenoteworthyandpositively forecastin46.42%.Fig.2representsstructuralrelationsamong modelvariablesandtheexplanatorypowerofeachLV.

Duetoobtained results, theverification ofhypothesis for-mulated tothisstudy will be discussed.The first hypothesis, stronglyupheldbyliterature,defendstheinfluenceof manage-ment control usageover organisational performance(Frezatti etal.,2014).Itisunderstoodtheseassistthroughinformation made availabletodecision-makingpersonnel,fosteringwider knowledge regarding operation and leading them to choose moresuitable,objective-drivenalternatives(Ashton,1974).In accordance to such scenario, H1 test results allow inferring managersusingoperationmanagementpracticespresentbetter businessperformance(withinfinancial,operationaland proce-duralconcepts).Besides,itisimportanttostressthat,although the research adopted strategy covers informal management tool usage, this adopted form seems to collaborate effec-tivelywithdecision-makingprocesses.Suchscenarioprovesto be favourabletowards reflectionsregarding actualconceptual parametersusefulnesstheoreticallydisseminated,and,agreat opportunityfornewpracticallysimplifiablepropositions.From presentedconsiderations,resultsinferH1hasbeenvalidated.

Table7

Pathcoefficients:direct,indirectandtotaleffectsamongconstructs.

Suggested relation among latent variables Hypothesis Direct effect Indirect effect Total effect MC_proxies → performance H1 0.4642* 0.0000 0.4642*

Entrepreneurial orientation → performance H2 0.1410* 0.1781* 0.3191*

Entrepreneurial orientation → MC_proxies H3 0.3838* 0.0000 0.3838*

Metacognition → MC_proxies H4 0.3273 0.1893 0.5166

Metacognition → entrepreneurial orientation H5 0.4934 0.0000 0.4934

Metacognition → performance H6 0.0851 0.3093 0.3944

Consideringtheexistenceofaninstitutionalisedenvironment andthecharacteristicprofileofanentrepreneurialbeing,itis pro-posedisomorphicpressuresmaybefaultyoversuchbeingand, that,his/herbehaviouralelementsenumeratehis/herdecisions withinmanagementprocesses–hereto,H2wastested.Results statemanagerswhohaveEOintrinsiccharacteristicsareproneto forecast,around14.10%,betterperformancewithinoperations theymanage.Suchscenariosuggestsentrepreneurs,whenever searchingforbetterresults,choosemethodsandpracticeswhich distinguishthemfromtheircompetitors,adoptinnovative strate-giesandboldpostureswithintheiractions.Suchfindingsratify previousresearches,asRauchetal.(2009)andChoandJung (2014).Hence,itispossibletoinfertheentrepreneurial orienta-tionpositiveeffectoverorganisationperformance,and,within asignificancelevelof5%,H2wasalsoconfirmedinthemodel. Undertheconceptentrepreneurshavecognitiveabilities con-nectingthemtobetterresult compromises,it isbelievedthey adoptmanagementpracticesasinformational supportin deci-sions.ThetestperformedfromH3,assumessuchassumptions, and,verifiesifthemanager–entrepreneurorientationinfluences management control proxies usage in companies located in clothingindustryLPA.Findingsshowapositiveeffectof38.38% fromEO overbusiness management control.It isunderstood studyresultsagreewithinvestigationsapplyingEOin organisa-tionsectors,asLietal.(2006),Rauchetal.(2009)andSpillecke andBrettel(2013).Thus,althoughwithinisomorphicpressure environment,theentrepreneurialprofileisabletoassociate risk-takingpronebehaviour(EO)totheusageoftoolsabletofollow actionplansandoperationmonitoring;consequently,its mean-ingfuleffectoverorganisationalperformanceisnoticed.Hence, findingsallowtheinferringH3wasconfirmedatasignificance levelof5%.

Thelastconstructincorporatedtomodeldiscussionrefersto themanager–entrepreneur metacognitiveabilities. Metacogni-tion,asexposedbyFlavell(1979),isunderstoodastheperson’s capacitytobeawareof decisionstaken (Haynie,2005). Inso-far, scholars uphold the notion human beings are rationally able to understand their own thinking whenever interacting with the environment and people around them (Estes, 1975; Shane&Venkataraman,2000).Thus,itisconceivablethat peo-ple are aware of their actions, and, that they recognise their ownstrengths,weaknesses,suppositionsandmotivations.The theoretical background of this investigation presented some researches which support the effect – or proposition – that, thisvariableinfluencestowardsusageofmanagementpractices, towardsentrepreneurial orientationandtowardsbusiness per-formance(Cho&Jung,2014;Haynieetal.,2010;Melot,1998; Shane&Venkataraman,2000).

Aforementioned conditions suggest,albeit not empirically supported,thepossibility entrepreneurmetacognitiveabilities mayinfluencemanagementtoolusagewithinmanagement pro-cesseswouldbeabletobetestedinH4.Thus,apersonwould be ableto usereports andinternalcontrols for operations as decision-makingsupportmaterial.Furthermore,metacognition effectasEOpredictorisarelationempiricallyevidencedthrough researchesasHaynieetal.(2010),ChoandJung(2014),and, Lima Filho and Bruni (2014). Such theoretical background

fosteredH5tobeverifiedundertheassumptionthathumanbeing judgments (evaluationsanddecisions)wouldbeabletoguide adoptedentrepreneurialattitude.Atlast,bysuggestingpeople who have higher metacognitiveabilities are also moreprone to considermultipleavailable alternatives andtomoreeasily recognisethebestones,H6wasformulated.

However, dueto thesample scenario, it wasobserved the metacognition variabledid not affectthe model;although its validationfulfilledtheliteraturecriteria,coefficientsofH4,H5 andH6didnotappearmeaningfulwithinthemodel,indicating that the suggestedeffect relationwasnot confirmedbythese hypotheses.Statistically,itisconsideredthat,possibly– corre-lationsofρ=0.3944,ρ=0.4934andρ=0.5166(p-value<0.05)

for,respectively,performance,entrepreneurialorientation,and, management controlproxies(seeTable3)–maycompromise relation analysisdue tomulticollinearityeffects albeit within low degree (Cohen, Cohen, West, &Aiken, 2002). Besides, it is taken into consideration that the LPA alternative may condition,withinsomelevel,people’swaysofthinking–that is –therationalprocessissomehowadapted toreality where the entrepreneur is, inhibiting people’s metacognitive ability overenvironmentpressure.

Finalconsiderations

Literature describes business associations as an accessi-ble alternative to organisations within unsure environments. TheestablishmentofLPAs,for example,isabletostrengthen regional economies; increase competitive abilities; constitute relationswithintheirmembers;and,toenableinformation shar-ing(Cassiolato&Szapiro,2003).Furthermore,thecreationof such bonds isbelieved toinducethe applicability of implicit social andeconomicalmechanismswhichareessentially iso-morphic–which,hence,stimulatescompaniestoadoptsimilar posturesandpractices(Dimaggio&Powell,1983).Undersuch perspective, this study is based onsupport from Institutional Theorywhichstatestheexistinginteractionamongcompanies withinthesameenvironmentwouldfostersimilaractionsand behaviours.

However, discussions regarding human behaviour support entrepreneurshaveabilitiesdistinctfromothers;alsobeingmore prone topresentcompetitiveaggressiveness, autonomy, inno-vativeness, and,risk-takingabilities(Lumpkin&Dess,1996; Miller,1983):itisimportanttostresswithinsmallbusinesses, theyoftenaretheoneswhoadministratethecompanies.

Additionally, it is known human actions are guided by metacognitiveprocess,alsoknownas,knowledgeofcognition and control of cognition. Literature describes entrepreneurial orientation as intrinsically supported by metacognitive pro-cesses, a condition whichsuggests the ability of a personto cognitivelyunderstandhis/herownobjectives,actionsand moti-vations,possibly,forecastshisbehaviourasanagentofchange (Haynieetal.,2010).

1996;Miller, 1983)and metacognition(Flavell,1979). Prac-tices relatedtoactionanalysis refertousage of management control–toolsmeaningfullyactingasdecision-makingsupport (Chenhall& Morris, 1986). Hence,the distinct and commit-tedentrepreneurialbehaviourwouldberesistanttoenvironment pressures,abletounbalanceinstitutionprototypes.

Amongst findings, it has been verified manager entrepreneurial orientation was able to affect over two model variables, management practices (management control proxies)andcompanyperformance.Thefirstrelationshowed entrepreneurial orientation predicts approximately 38.38% of theinternalmanagementcontrols.Accordingtosuch,literature is quite persuasive regarding management tool usefulness, and, it is believed their usage is an efficient informational alternative for decision-making within challenging environ-ments.Furthermore,althoughintuitiveelementsmayoccurin actions,itis suggestedsuchtool usagemaybehaveas away tomanagerssupport their intuitionwhenfacing problems, as whenprojectingsituationalscenarios.

It was observed entrepreneurial orientation was able to directlyforecastorganisationalperformanceinapproximately 14.10%.However, findings presented within such interaction showthat–althoughacompetitive,innovativeand opportunity-driven behaviour may be necessary, it becomes less influent regarding business results when compared to effects from management practices. It is understood that to undertake an enterprise,and–specially–tomanagetheinvestment,includes analysisand viabilityprocedures, forecasting andmonitoring activities–thesepossiblycarriedoutthroughmanagement prox-ies.Thus,testingwithEOvariableshaveshownevenpersons with characteristics such as autonomy, competitiveness, and pronetorisk-taking,havebeenabletodiscernauxiliary man-agementtoolsactasfosteringcompanysuccess.

Asobserved,when entrepreneurs embraceuncertainty,the risk related to his decision, and, the management informa-tion made available, they consequently notice improvements inorganisational performance.The46.42%effectfromproxy variablesof management control over company performance confirmsthisconcept.

Thus,it isconceivableresearchfindingsfosterfurther dis-cussionsregardingthelevelinstitutionalforcesareactuallyable tosteerthebehaviourof insertedelements,inasmuchas –for suchscenario – entrepreneurialorientationwas abletodirect actionswhilemetacognitionhadnoresponsepower.Therefore, itisbelievedthestructuralmodelheresuggestedmaybetested byisolatingtheconstructentrepreneurialorientation,and veri-fyingitsindividualeffectoverproxyvariablesofmanagement proxyandperformance,whichmayresultinamoreadjusted model.

Besides, found evidences are understood as behaving as questioningisomorphicbehaviour;foronlyentrepreneurial ori-entation characteristics are able tointerfere somehow within institutional structures, sculpting a behaviour prone to imi-tateLPApractices.However,itisbelievedtherearevariables endogenous to the ones adopted in this research that may havesomeinfluenceonmanagementpracticesTherefore,itis suggestedfutureresearchesinvestigateforfurtherbehavioural

characteristics which may be representative in the mimetic behaviouraldigressionwithinanenvironment.

It is convenient to stress the sample was configured by accessibility,whichmayjeopardisesomekindofgeneralisation for other sectors. This study was also concerned in presum-ing, as supported by literature, that APL members take an isomorphic behaviour within such situations, which may be further confirmed more precisely in future researches. The approach is presented as a introductory suggestion,breaking paradigmsregardingcharacterisationofcompanygroupsasan institution.Empiricalvalidationofinterventionfromindividual entrepreneurcharacteristicsovertheusageofinternalpractices ofmanagementinenvironments“theoretically”definedas insti-tutionalisedmaybeasignofthisconjecture.

Conflictsofinterest

Theauthorsdeclarenoconflictsofinterest.

References

Ashton,R.H.(1974).Cueutilizationandexpertjudgements:Acomparisonof independentauditorswithotherjudges.JournalofAppliedPsychology,59, 437–444.

Batha,K.,&Carroll,M.(2007).Metacognitivetrainingaidsdecisionmaking.

AustralianJournalofPsychology,59,64–69.

Cassiolato,J.E.,Lastres,H.M.M.,&Szapiro,M.(2000).Arranjosesistemas produtivoslocaiseproposi¸cõesdepolíticasdedesenvolvimentoindustrial etecnológico.RiodeJaneiro:UFRJ/IE.

Cassiolato,J.E.,&Szapiro,M.(2003).Umacaracterizac¸ãodearranjos pro-dutivoslocaisdemicroepequenasempresas.InH.M.M.Lastres,J.E. Cassiolato,&M.L.Maciel(Eds.),Pequenaempresa:Coopera¸cãoe Desen-volvimentoLocal.RiodeJaneiro:Dumará.

Chenhall,R.H.,&Langfield-Smith,K.(1998).Therelationshipbetween strate-gicpriorities,management techniquesand managementaccounting:An empiricalinvestigationusingasystemsapproach.Accounting, Organiza-tionsandSociety,23,243–264.

Chenhall,R.H.,&Morris,D.(1986).Theimpactofstructure,environment, andinterdependenceontheperceivedusefulnessofmanagementaccounting systems.TheAccountingReview,61,16–35.

Chin,W.W.(1998).Thepartialleastsquaresapproachforstructuralequation modeling.InG.A.Marcoulides(Ed.),Modernmethodsforbusinessresearch

(pp.236–295).London:LawrenceErlbaumAssociates.

Cho,Y. S.,& Jung,J.Y.(2014).Therelationshipbetweenmetacognition, entrepreneurialorientation,andfirmperformance:Anempirical investiga-tion.AcademyofEntrepreneurshipJournal,20,71–86.

Cohen,J.,Cohen,P.,West,S.G.,&Aiken,L.S.(2002).Appliedmultiple regression/correlationanalysisforthebehavioralsciences(3rdedition). NewJersey:Routledge.,736pp.

Dimaggio,P.J.,&Powell,W.W.(1983).Theironcagerevisited:Institutional isomorphismandcollectiverationalityinorganizationalfields.American SociologicalReview,48,147–160.

Dyte,R.(2005).Whatistheuseoffinancialcompliance?Thecaseofsmall businessinAustralia.InInternationalCouncilforSmallBusiness(ICSB) WorldConference,Vol.50,15–18June2005,Washington.Proceedings. Washington:ICSB.

Estes,W.K.(1975).Handbookoflearningandcognitiveprocesses.Hillsdale: LawrenceErlbaum.

Flavell,J.H.(1979).Metacognitionandcognitivemonitoring:Anewareaof cognitivedevelopmentalinquiry.AmericanPsychologist,34,906–911.

Frezatti,F.,Carter,D.B.,&Barroso,M.F.G.(2014).Accountingwithout accounting:Informationalproxiesandconstructionoforganisational dis-courses.Accounting,Auditing&AccountabilityJournal,27,426–464.

Hair,J.F.,Jr.,Black,W.C.,Babin,B.J.,&Anderson,R.E.(2010).Multivariate dataanalysis(7thed.).UpperSideRiver:PrenticeHall.

Hair,J.F.,Jr.,Hult,T.M.,Ringle,C.M.,&Sarstedt,M.A.(2014).Primeron partialleastsquaresstructuralequationmodeling(PLS-SEM).LosAngeles: Sage.

Haynie,J.M.(2005).Cognitiveadaptability:Theroleofmetacognitionand feed-backinentrepreneurialdecisionpolices(Doctoraldissertation).pp.238f. UniversityofColoradoBoulder.

Haynie,J.M.,&Shepherd,D.A.(2009).Ameasureofadaptivecognition forentrepreneurshipresearch.EntrepreneurshipTheoryandPractice,33, 695–714.

Haynie,J.M.,Shepherd,D.A.,Mosakowski,E.,&Earley,P.C.(2010).A situ-atedmetacognitivemodeloftheentrepreneurialmindset.JournalofBusiness Venturing,25,217–229.

Henseler,J.,Ringle,C.M.,&Sinkovics,R.R.(2009).Theuseofpartialleast squarespathmodelingininternationalmarketing.AdvancesinInternational Marketing,20,277–319.

Ireland,R.D.,Hitt,M.A.,&Sirmon, D.G.(2003).Amodelofstrategic entrepreneurship:Theconstructanditsdimensions.JournalofManagement,

29,963–990.

Kassai,S.(1997).AsempresasdepequenoporteeaContabilidade.Caderno deEstudos,9,60–74.

KetsdeVries,M.F.R.(1977).Theentrepreneurialpersonality:Apersonatthe crossroads.JournalofManagementStudies,14,34–57.

Levine,D.M.,Berenson,M.L.,&Stephan,D.(2000).Estatística:Teoriae Aplica¸cõesusandoMicrosoftExcelemPortuguês.RiodeJaneiro:LTC.

Li,Y.,Liu,Y.,&Zhao,Y.(2006).Theroleofmarketandentrepreneurship orientationandinternalcontrolinthenewproductdevelopmentactivitiesof Chinesefirms.IndustrialMarketingManagement,35,336–347.

LimaFilho,R.N.,&Bruni,A.L.(2014).Metacognic¸ãoeempreendedorismo: serempreendedorinfluenciaatitudesmetacognitivas?Gestão& Regionali-dade,30,63–74.

Lumpkin,G.T.,&Dess,G.G.(1996).Clarifyingtheentrepreneurialorientation constructandlinkingittoperformance.AcademyofManagementReview,

21,135–172.

Mehralizadeh,Y.,&Sajady,H.(2006).Astudyoffactorsrelatedto success-fulandfailureofentrepreneursofsmallindustrialbusinesswithemphasis

ontheirlevelofeducationandtraining.SocialScienceResearchNetwork, 1–39.

Melot, A.(1998). The relationship between metacognitive knowledge and metacognitiveexperiences:Acquisitionandre-elaboration.European Jour-nalofPsychologyofEducation,13,75–89.

Miller,D.(1983).Thecorrelatesofentrepreneurshipinthreetypesoffirms.

ManagementScience,29,770–792.

Ministério do Desenvolvimento, Indústria e Comércio Exterior. (2006).

Plano de desenvolvimento do arranjo produtivo local do vestuário de Cianorte/Maringá –Paraná.. Retrievedfrom:.http://www.mdic.gov. br/arquivos/dwnl1248271195.pdf

Nelson,T.(1996).Consciousnessandmetacognition.AmericanPsychologist,

51,102–129.

Otley,D.,&Berry,A.J.(1980).Control,organizationandaccounting. Account-ing,OrganizationsandSociety,5,231–244.

Oyadomari,J.C.,Cardoso,R.L.,Mendonc¸aNeto,O.R.,&Lima,M.P.(2008).

Fatoresqueinfluenciam aadoc¸ãode artefatosdecontrolegerencialnas empresasbrasileiras.RevistadeContabilidadeeOrganiza¸cões,2,55–70.

Rauch,A.,Wiklund,J.,Lumpkin,G.T.,&Frese,M.(2009).Entrepreneurial orientationandbusinessperformance:Anassessmentofpastresearchand suggestionsforthefuture.EntrepreneurshipTheoryPractice,33,761–787.

Ringle,C.M.,Silva,D.,&Bidu,D.(2014).Modelagemdeequac¸õesestruturais comutilizac¸ãodoSmartpls.RevistaBrasileiradeMarketing,13,54–71.

Schraw,G.,&Dennison,R.S.(1994).Assessingmetacognitiveawareness.

ContemporaryEducationalPsychology,19,460–475.

Shane,S.,&Venkataraman,S.(2000).Thepromiseofentrepreneurshipasa fieldofresearch.AcademyofManagementReview,25,217–226.

Spillecke,S.B.,&Brettel,M.(2013).Theimpactofsalesmanagement con-trolsontheentrepreneurialorientationofthesalesdepartment.European ManagementJournal,31,410–422.

Stroeher,A.M.,&Freitas,H.(2008).Ousodasinformac¸õescontábeisnatomada dedecisãoempequenasempresas.RevistadeAdministra¸cãoEletrônica,1.

Triola,M.F.(1999).Introdu¸cãoàEstatística(7thed.).RiodeJaneiro:LTC.

Wetzels,M.,Odekerken-Schröder,G.,&VanOpen,C.(2009).UsingPLS pathmodelingforassessinghierarchicalconstructmodels:Guidelinesand empiricalillustration.MISQuarterly,33,177–195.