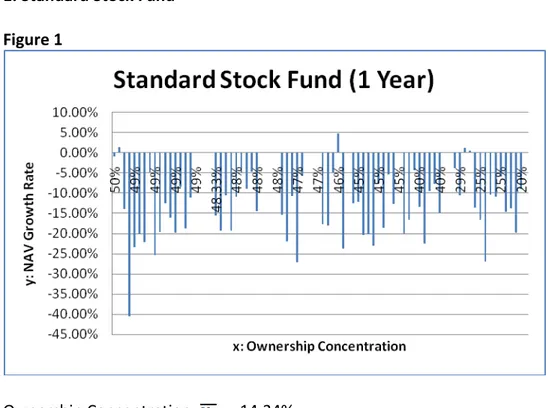

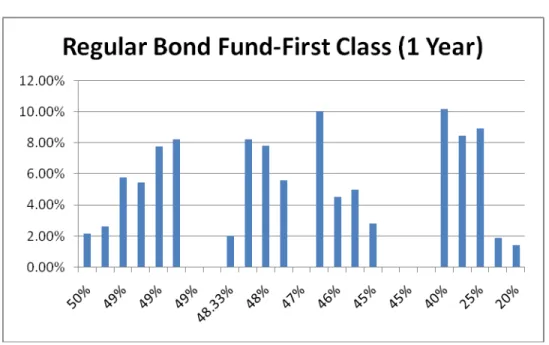

The Core Issues of Open-Ended Funds in China: Conflicts of Interest and Ownership Structure

Texto

Imagem

Documentos relacionados

The fourth generation of sinkholes is connected with the older Đulin ponor-Medvedica cave system and collects the water which appears deeper in the cave as permanent

Extinction with social support is blocked by the protein synthesis inhibitors anisomycin and rapamycin and by the inhibitor of gene expression 5,6-dichloro-1- β-

DECIDES to establish, in accordance with Rule 42 of the Rules of Procedure of the Health Assembly, an open-ended intergovernmental working group that shall be open to all States and

Neste trabalho o objetivo central foi a ampliação e adequação do procedimento e programa computacional baseado no programa comercial MSC.PATRAN, para a geração automática de modelos

Ousasse apontar algumas hipóteses para a solução desse problema público a partir do exposto dos autores usados como base para fundamentação teórica, da análise dos dados

A norma ISO 14001 estabelece as diretrizes básicas para o desenvolvimento de um sistema que gerencie a questão ambiental dentro da empresa, ou seja, um sistema de gestão ambiental

The probability of attending school four our group of interest in this region increased by 6.5 percentage points after the expansion of the Bolsa Família program in 2007 and

Tidal analysis of 29-days time series of elevations and currents for each grid point generated corange and cophase lines as well as the correspondent axes of the current ellipses