Carlos Firetti, CFA

-

55 11 2178 5363 [email protected]Strong Ship, Rough Waters

Although the European crisis remains a potential risk for the market, as various European countries still have a fragile fiscal situation and weak economic growth, we believe there is little chance of the crisis escalating (a “full-blown” crisis being unlikely) in the short

term due to the European Union’s commitment to helping weaker economies and

consequently the Euro. On the other hand, we see some drivers for the market: (1) continued recovery of the US economy, which still seems on track despite some weaker economic indicators; and (2) expectations that the Chinese economy will continue to reduce its imbalances without clear discontinuity. In this scenario, we see some room for a recovery despite volatility.

In Brazil, we believe the economic scenario remains positive despite expectations that monetary tightening will continue, which should drive the Selic rate to 11.50% at YE10 and 12.50% at YE11. Our expectation is that growth should decelerate, with full-year GDP growth coming in at 6.8% for 2010 and 3.5% for 2011. We see a new administration delivering fiscal adjustment regardless of who wins the elections.

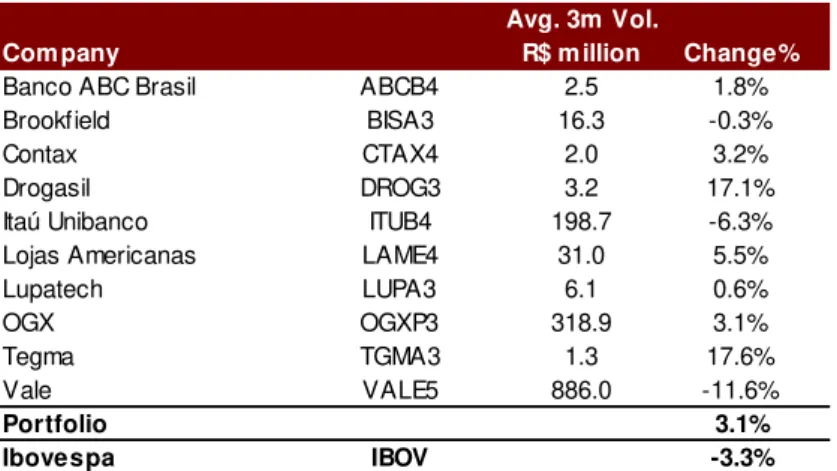

Main changes in our portfolio. In our portfolio for July, we have included BR Properties (BRPR3), Gafisa (GFSA3), Gerdau (GGBR4), Gol (GOLL4) and Marfrig (MRFG3), and excluded Brookfield (BISA3), Contax (CTAX4), Lupatech (LUPA3), Tegma (TGMA3) and Banco ABC (ABCB4).

Performance. Our recommended portfolio for June went up 3.1%, compared to -3.3% for the Ibovespa. YTD in 2010, our focus list has accumulated performance of -4.9%, compared to -11.1% for the Ibovespa.

Source: Bloomberg and Bradesco Corretora estimates

ADTV 3m

R$m n Target Upside 2010 2011 2010 2011

Top Picks - July

BR Properties BRPR3 Outperform 3.3 R$ 19.50 51.8% 24.0 21.1 8.5 6.2

Drogasil DROG3 Outperform 3.7 R$ 43.00 24.6% 21.7 16.7 12.5 9.6

Gafisa GFSA3 Outperform 48.1 R$ 14.60 35.2% 10.7 7.9 9.4 7.4

Gerdau GGBR4 Outperform 134.1 R$ 38.20 61.9% 12.2 7.5 7.3 5.3

Gol GOLL4 Outperform 30.2 R$ 31.00 45.0% 20.7 20.3 8.9 7.4

Itaú ITUB4 Outperform 199.9 R$ 44.00 35.4% 11.0 9.6

Lojas Americanas LAME4 Outperform 29.9 R$ 17.60 34.6% 45.6 38.5 11.1 9.1

Marfrig MRFG3 Outperform 32.7 R$ 26.30 55.8% 23.0 8.3 7.8 5.1

OGX OGXP3 Outperform 287.9 R$ 29.00 73.4% 150.2 214.6 n.m n.m

Vale VALE5 Outperform 886.7 R$ 79.20 108.9% 7.1 4.7 4.3 3.1

Com pany Ticker Rating Price P/E EV/EBITDA

Focus List

Bradesco Corretora – Av. Paulista, 1.450 – 7th

floor – Sao Paulo – Brazil – 55 11 3556-3001 Chief Economist

Top Picks

Banco Itaú (ITUB4)

Rating: Outperform Target Price: R$44.00

Upside: 35.4%

Market Cap.: R$147,139mn 3-month ADTV: R$199.9mn

Maintained from the previous month

What we like about the stock: We expect Banco Itaú to benefit in 2010 from strong expansion in net earnings, with a decline in non-performing loans (and consequently provision expenses), while keeping costs under control due to synergy gains from the merger with Unibanco. For 2011, the bank should be operating with almost 100% of the synergies already captured. We project ROE recovering significantly in 2010 to the 24% range. After a recent correction, we see ITUB4 trading at attractive levels.

Risks: (i) a banking crisis in Europe; (ii) delivering lower-than-expected cost reduction after completing its merger; (iii) lower-than-expected credit growth; and (iv) an acquisition outside Brazil.

Valuation: According to our numbers, ITUB4 is currently trading at P/E multiples of 11.0x for 2010 and 9.6x for 2011, and a P/BV 2010 of 2.5x. At our target, ITUB4 would trade at P/E multiples of 14.9 for 2010 and 12.9x for 2011, and a P/BV 2010 of 3.3x.

BR Properties (BRPR3)

Rating: Outperform Target Price: R$19.50

Upside: 51.8%

Market Cap.: R$1,857mn 3-month ADTV: R$3.4mn

Included this month

What we like about the stock: BR Properties is trading at a discount to its main peers in Brazil, with a cap rate of 12.5% in FY10, against shopping center

comparables’ 9.7%. Moreover, the company has already reached over 900k sqm of GLA, as promised in the IPO (currently having 970k sqm of GLA), and intends to deliver much more than that by YE10.

Drivers/catalysts: (i) acquisitions; (ii) interest rates (the company’s main benchmark); and (iii) the domestic economy.

Risks: (i) higher interest rates; (ii) contract renewals; and (iii) unexpected contingencies in acquisitions.

Drogasil (DROG3)

Rating: Outperform Target Price: R$43.00

Upside: 24.6%

Market Cap.: R$2,166mn 3-month ADTV: R$3.7mn

Maintained from the previous month

What we like about the stock: Consolidation in the retail drugstore sector intensified by a change in the tax regime to payment of VAT in advance (which

should eliminate small players’ unfair competitive advantage in being able to evade

taxes) should continue contributing to solid growth for Drogasil, with expanding market share. We expect the company to post an EBITDA CAGR 11-14 of 23%. Drivers/catalysts: (i) high fragmentation of the retail drugstore sector in Brazil; (ii) decline in informality; and (iii) sector consolidation.

Risks: low liquidity of the stock.

Valuation: DROG3 is trading at 9.6x EV/EBITDA 2011, with an estimated EBITDA CAGR 11-14 of 26.1%. We have a TP of R$43.00 for DROG3, implying an EV/EBITDA 2011 of 12.9x and upside potential of 24%.

Gafisa (GFSA4)

Rating: Outperform Target Price: R$14.60

Upside: 35.2%

Market Cap.: R$4,628mn 3-month ADTV: R$48.1mn

Included this month

What we like about the stock: We have recently upgraded Gafisa to Outperform from Market Perform (see our June 10 sector update report: “Does the Sector’s High Volatility Make Sense?"). Gafisa has strong liquidity of R$48.1mn, third in the sector among local stocks (excluding ADR volumes), and is trading at a discount to Cyrela and MRV. Furthermore, we expect Gafisa’s margins to improve over the course of the year, as the Tenda operation is more efficient. The company’s EBITDA guidance for full-year 2010 is 18.5%-20.5%, compared to 17.5% in 2009. It is worth mentioning that there should no longer be non-recurring expenses, which undermined the company’s results in previous quarters.

Drivers/catalysts: (i) operational improvements; (ii) low multiples; and (iii) attractive DCF-based upside potential.

Risks: (i) rising inflation could have a negative impact on low-income operations since units have a price cap under the Minha Casa, Minha Vida program, limiting the pass-through of costs to prices.

Gerdau (GGBR4)

Rating: Outperform Target Price: R$38.20

Upside: 62.7%

Market Cap.: R$33,609mn 3-month ADTV: R$134.1mn

Included this month

What we like about the stock: The latest statistics on the steel sector are proving our main investment thesis for Gerdau to be correct. We expect growth in the

company’s Brazilian division to more than offset a slow recovery in its US

operations. Growth in the Brazilian division should come from this division’s two business lines: (i) rolled products for the domestic construction sector; and (ii)

pre-processed steel for exports, produced in the Açominas factory. In Gerdau’s 1Q10

results, domestic sales were up 5.4% QoQ and exports rose 17.4% QoQ. Statistics on Brazilian long steel sale in May shows that this growth continued in 2Q10. Furthermore, 50% YoY growth in credit outstanding to the housing sector in May is a leading indicator that this growth should remain quite strong for several quarters. Drivers/catalysts: (i) recent data from the Brazilian Steel Institute, indicating long steel sales in Brazil up 57.1% YoY, vs. a 53.3% YoY rise in flat steel sales; (ii) 50% growth in credit outstanding to the housing sector in the last 12 months; and (iii) 2Q10 results, in which we should see the impact of sales growth.

Risks: (i) slower-than-estimated recovery in Gerdau’s US operations.

Valuation: Gerdau is trading at 7.3x EV/EBITDA10 and 5.3x EV/EBITDA11, vs.

local peers’ average of 6.4x for 2010 and 4.8x for 2011, and international peers’ 4.8x for 2010 and 4.3x for 2011. Our TP is R$38.2/share, with upside potential of 62.7%, implying an EV/EBITDA10 multiple of 10.7x

Gol (GOLL4)

Rating: Outperform Target Price: R$31.00

Upside: 45.0%

Market Cap.: R$5,662mn 3-month ADTV: R$30.1mn

Included this month

What we like about the stock: Gol has the lowest marginal cost in the sector and

continues to benefit from the sector’s best phase in its history. Demand in the airline sector is rising at a fast pace, not only in the domestic market (average of 30% in 2010) but also in the international market (average of 11.7% in 2010). Companies are also benefiting from stable FX and oil prices, the main drivers for costs.

Drivers/catalysts: (i) Stronger demand (ANAC data); (ii) oil costs (~40% of companies’ costs); and (iii) FX volatility.

Risks: (i) higher oil prices; (ii) BRL depreciation; (iii) competition reducing yields (fares); and (iv) government intervention in the company’s operations and the

sector’s structure.

Lojas Americanas (LAME4)

Rating: Outperform Target Price: R$17.60

Upside: 34.6%

Market Cap.: R$9,868mn 3-month ADTV: R$29.9mn

Maintained from the previous month

What we like about the stock: Lojas Americanas is enjoying a strong pace of growth in the brick and mortar business with expansion plans to open 400 stores in the next 4 years, from the current 476 stores. The business model is highly flexible, both in terms of store format and product portfolio. Furthermore, we expect the e-commerce operation (B2W) to start improving its operating results, especially in 2H10.

Drivers/catalysts: (i) growth, driven by SSS but mainly due to sales area expansion; (ii) improving results in the e-commerce division (B2W); and (iii) increasing formalization of retail.

Risks: (i) high leverage pressuring the bottom line with higher interest rates; and (ii) competition in e-commerce, which could affect online subsidiary B2W.

Valuation: LAME4 is trading at 9.1x EV/EBITDA 2011, with an estimated EBITDA CAGR 11-14 of 23%. We have a TP of R$17.60 for LAME4, implying an EV/EBITDA 2011 of 12.0x and upside potential of 35%.

Marfrig (MRFG3)

Rating: Outperform Target Price: R$26.30

Upside: 55.8%

Market Cap.: R$7,580mn 3-month ADTV: R$32.7mn

Included this month

What we like about the stock: We expect improving margins for meatpackers on the back of favorable costs (due to a higher global availability of grains and an increasing cattle herd in Brazil) and a positive outlook for animal protein prices worldwide, with a decrease in inventories and a continuing increase in consumption. Marfrig is a cheap option in the sector and also offers the upside of gaining market share in processed foods in Brazil after the acquisition of Seara. Drivers/catalysts: (i) improving margins due to bullish outlook for meat prices and bearish outlook for input costs; (ii) synergies with Seara; (iii) leverage of recent expansion in installed capacity; and (iv) gaining market share in the Brazilian processed foods market.

Risks: (i) high exposure to a single customer (McDonald’s) after the acquisition of Keystone Foods; (ii) volatility in input costs or protein prices; and (iii) high leverage (net debt/EBITDA ~4.0).

OGX (OGXP3)

Rating: Outperform Target Price: R$29.00

Upside: 73.4%

Market Cap.: R$54,039mn 3-month ADTV: R$287.9mn

Maintained from the previous month

What we like about the stock: OGX is still sustaining the same 100% success ratio from 2009’s exploration campaign. Thus far, the company has already drilled 15 wells, 13 of which resulted in oil discoveries – of which 7 have been dimensioned, indicating a total recoverable oil volume ranging from 2.6bn to 5.5bn

boe. The midrange (4.1bn boe) already represents 61% of the company’s initial

estimate of 6.7bn boe. In addition, considering the surpluses in the already-dimensioned discoveries, the total potential resources reaches 8.5bn boe (potentially reaching 7.1bn at the low end of the range, but 9.9bn boe at the high end of the range).

Drivers/catalysts: We reinforce our view that 2010 should be the year in which

OGX’s investment case should materialize, not only regarding its exploration

campaign (27 drilling wells, of which 9 already started, with 7 discoveries), but also the commercial availability of a considerable amount of resources (we expect ~2bn boe), and a potential farm-out transaction, which we believe could be a relevant trigger for the stock in the short term.

Risks: (i) oil prices; (ii) low level of discoveries; and (iii) FX rate.

Valuation: On May 14 we raised our target price to R$29/share (from R$27.7/share) due to a decrease in exploration risk, on the back of the announcement that the OGX-6 (Etna) and OGX-2A (Pipeline) wells are connected, being part of a single, giant reservoir.

Vale (VALE5)

Rating: Outperform Target Price: R$79.20

Upside: 108.8%

Market Cap.: R$202,464mn 3-month ADTV: R$886.7 mn

Maintained from the previous month

What we like about the stock: With a new iron ore pricing system (the IODEX), linked to the spot price, we expect a massive upgrade in iron ore prices and thus

Vale’s EBITDA, making the company’s valuations reach levels that do not suit such a blue chip. We are assuming a 90% iron ore price rise this year, and another 10% next year (which is conservative, considering that Vale has already raised prices by more than 150% this year). With that alone, Vale should generate R$75.5bn in EBITDA next year, resulting in a low EBITDA11 multiple of only 3.1x, far below its historical level of 8.7x. We expect iron ore prices to remain high in the short/middle term due to a combination of two factors. On one hand, little additional capacity should come on-stream in the next two years. On the other hand, even with deceleration in Chinese demand (69% of the market), supply should be unable to keep up with growth in absolute terms. We also point out that investors have

recently been taking profits on Vale because of Petrobras’ capitalization. However,

since the capitalization has been postponed, it should not be a driver for the stock in the short term.

Drivers/catalysts: (i) iron ore spot prices resuming their upward momentum; and (ii) 2Q10 results, for which we estimate EBITDA up 134% QoQ (in USD).

Risks:(i) disruption in China’s economic growth and not just a slowdown.

The Month Ahead

–

Mapping Fundamentals and Beyond

ACTIVITY: Credit figures do not indicate an immediate slowdown.

Brazil stands out for posting an impressive 2.7% QoQ growth (11.2% SAAR) in 1Q10. Once again, the strong number reflects stimulated domestic demand. 7.4% QoQ expansion in gross fixed capital formation (investments) has given investors some confidence regarding the quality of the recovery. Clearly, official lending (BNDES and mortgage financing) has pushed up these figures. The main bottleneck is not a lack of investments but the lethargic savings rate (15%). This process resulted in imports jumping 13.1% QoQ (an annualized rate of 64%!). The dynamics are likely to continue through 2010, although the need for consolidation in 2011 keeps growing (especially on the fiscal front and official lending through the BNDES).

We have revised our GDP growth forecast for 2010 to 6.8%. We are fully aware that this figure lies at the bottom of the range. However, it is due to our more conservative (and cautious) assessment of the global economy in 2H10 (see below).

Total credit outstanding rose 19% YoY (2.1% MoM) in May. Despite the usual seasonal strength of this month, the growth was nonetheless remarkable (comparable to pre-crisis levels). The robust expansion resulted from a combination of continuing recovery of “market credit” and renewed thrust from earmarked lending. The strength of auto financing was somewhat incompatible with the slowdown in actual car sales (in May), although general credit to individuals maintained a good recovery trend. Credit to companies also fared well (better than expected).

There is no sign of an evident and/or consistent slowdown in the Brazilian economy over the next quarter, although the pace of growth should accommodate slightly going forward. Lower growth should only be expected in 2011.

INFLATION: Finally, relief on the inflation front.

The IPCA-15 rose 0.19% in June, significantly less than previous inflation releases, pulled by long-awaited deflation in food prices (-0.42% MoM). The result also shows a better inflationary picture for nonfood items. Annual inflation fell to 5.1% YoY. The importance of these results lies not so much in the moderation of inflation (still not consistent) but the likely positive impact on

inflation expectations, the main “villain” of the recent deterioration in the

inflationary outlook and a key variable behind COPOM’s decision-making. For the last IGP-M release, important deceleration in the impressive iron ore price uptrend helped bring the index below 1% in June (0.85%).

The latest inflation report reveals a somewhat dovish view of the inflation reading, given the relatively benign estimates for inflation over the coming quarters – both in the reference scenario and market scenario. We expect

another 0.75bps hike at July’s meeting followed by a 0.50bps increase in

FISCAL: Not bad, but far from enthusiastic.

The accumulated primary surplus for the last 12 months equaled 2.13% of GDP in May. The numbers continue to disappoint to some extent, given the continuing acceleration in expenditures (despite record federal tax collections of late). Consequently, the nominal result climbed to 3.28% of GDP during the month (from 3.21% in April).

Fortunately, the larger deficits have not materially impacted net debt as a percentage of GDP, which fell to 41.4% (from 41.8% in April). The decrease was due to the revaluation of foreign reserves. On the other hand, the gross debt ratio rose to 60.1% of GDP (60% in April).

Fiscal accounts are not a market issue given the relative stability of debt levels. Challenges remain in terms of the quality of the budget execution and the long-term sustainability of fiscal accounts (not the immediate month-to-month fiscal performance).

BOP: Several changes in balance of payments data.

May’s external accounts showed an accommodation of the current account

deficit (US$2.0bn), with the accumulated 12-month CA shortfall shrinking to 1.94% of GDP (1.99% in April) after 7 consecutive monthly expansions. A rebound in FDI (US$3.5bn) was also noticeable after 11 consecutive declines, substituting portfolio investments, which fell to US$3.7bn during the month after 12 consecutive monthly increases.

The decline in the current account deficit in May is attributable to a larger trade balance for the month (US$3.4bn; vs. US$1.3bn in April), in turn explained by recovering exports.

The drop in portfolio investments by foreigners in May (US$3.7bn; vs. US$7.3bn in April) was due to retrenchment of equity investments (US$0.5bn net outflow, the first negative result since June 2009). Fixed income investments remained strong (flat at US$4bn), although more as a result of operations closed in April whose settlement was carried forward into May.

So far, so good. We have been arguing that the size of the current account deficit is not a concern and until now the speed of the deterioration has been quite

acceptable, with no “explosion” in the magnitude the deficits over the short term.

This seems increasingly an issue for 2012 and beyond, not now.

GLOBAL: What to worry about – the US, China or Europe?

The G-20 meeting in Canada included an unusual proposal for fiscal adjustment (slashing deficits in half by 2013). This was the most important change in perception since the crisis in 2008. Correct or not, justified or not, expanding stimuli has been defended since late 2008, and the recovery has always been linked to these pushes. The recent change in course is due to the severe deterioration of fiscal accounts in Europe.

For the United States, perhaps its greatest fear is still the possibility of another

unemployment benefits) to 1.3mn Americans, a sharp cutback in the finances of state and local governments, inducing severe cost cutting – all these elements together indicate a far more fragile economic recovery. The last quarter of this year and the beginning of 2011 promise to be radically different: a double-dip scenario should not be ignored. Whereas, before, the odds were 10%, now the probability of the US entering a new recession is 40%.

Greece continues to diverge from the rest of the PIIGS countries, with spreads already at 1,100bps. Debt restructuring is becoming increasingly obvious as time goes by.

While the finances of local governments in the US have long been a problem, concerns have grown exponentially over the last few weeks. Information is very opaque, although their situation is clearly awful. We do not intend to go into the substance of the data, but it seems likely that several municipalities will have trouble rolling over their debt in 2010. The problem here is the contractionary effect of adjustment measures.

Looking at China, a quite interesting official report became public recently (not leaked, but purposefully released) showing a more difficult situation for local government financing vehicles (LGFVs). What is most intriguing is the official recognition of the problem, which brings us back to something else unusual about China. The Chinese Communist Party succession in 2012 could be in the works, with different political groups within the party advocating different strategies. Controlling a potentially critical situation in the future is of major interest to any group willing to take power. Monetary tightening/administrative controls on the banking system are likely to continue.

CONCLUSIONS/ECONOMY AND MARKETS

EQUITY ENVIRONMENT. Upward growth revisions have always been an extraordinary driver for the equity markets. While consensus estimates have been gradually rising since the beginning of the year, concerns about Europe and potentially China have eclipsed the higher growth figures. At this juncture, it is likely that at 7%+, revisions in consensus for 2010 will be marginal – especially considering that these revisions are not being carried over into 2011. The current activity numbers will probably show some sort of fatigue next month as a natural accommodation from very intense growth levels for retail sales and industrial production over the last three months. Relief from inflation could boost

confidence and visibility regarding the “final stop” for interest rates. With most of

the interest-tightening already priced in, we do not expect a scenario of equities being negatively impacted by local factors (an accommodation of activity could even be positive, since it would help avoid further problems in dealing with inflation). Target prices remain above current levels for most companies, although catalysts for price improvements are not necessarily present.

INTEREST/BONDS/COPOM. Inflation expectations for 2011 holding steady at

4.8% for many weeks is an important signal reflecting the market’s view that the

meeting. As such, we expect the Selic rate to reach 11.5% in December 2010 and 12.5% by mid-2011.

USD/BRL. The BRL has not been strengthened by a more heated domestic economy. The European financial crisis is largely to blame, with China coming into center stage recently. We have maintained our R$1.85/US$1 forecast since 3Q09, not changing this call for now. If there is a way to go in terms of betting on

the FX space, it is “buy vol.”

Performance of Top Picks

Our Performance in June

Figure 1: Performance of Top Picks in June

Source: Economática and Bradesco Corretora

Avg. 3m Vol.

Com pany R$ m illion Change%

Banco ABC Brasil ABCB4 2.5 1.8%

Brookfield BISA3 16.3 -0.3%

Contax CTAX4 2.0 3.2%

Drogasil DROG3 3.2 17.1%

Itaú Unibanco ITUB4 198.7 -6.3%

Lojas Americanas LAME4 31.0 5.5%

Lupatech LUPA3 6.1 0.6%

OGX OGXP3 318.9 3.1%

Tegma TGMA3 1.3 17.6%

Vale VALE5 886.0 -11.6%

Portfolio 3.1%

Analyst Certification (i) (ii) (i) (ii) (iii) (iv) (v) Important Disclosures 1 x 2 x 3 5

Rating Definition BR²

Outperform Expected to outperform the Ibovespa by more than 10%. 84%

Market Perform Expected to perform in the range of 10% above or below the Ibovespa. 93%

Underperform Expected to underperform the Ibovespa more than 10%. 75%

Under Review This indicates that both the target price and the rating are currently being revised. 100%

Restricted The analyst cannot express his/her view s on the company. 100%

(1) 7/1/10 92 companies

(2)

under coverage globally.

Bradesco Corretora had

Price target and rating history

4

Any other actual material conflict of interest of Bradesco Corretora and/or its affiliates know n at the date of this report.

4%

Percentage of companies under coverage globally w ithin this rating category. As of

Each analyst responsible for the preparation and content of this report hereby certifies, pursuant to SEC Regulation AC and applicable law s and regulations of other jurisdictions, that:

The ratings reflect only the analyst’sexpectation on the future performance of the relevant stock. A“Outperform” rating does not necessarily represent that the analyst approves of the company and its management w hilst a“Underperform”rating does not necessarily means that the analyst has a negative view on the company. Within Bradeco Corretora coverage universe there are sound companies, w ith good fundamentals as per the market consensus, and fair priced stock, and w ould not be Bradeco Corretora investment pick.

Coverage¹ 62% 30%

the view s expressed herein accurately and exclusively reflect his or her personal view s and opinions about the subject company(ies) and its or their securities;

that no part of their compensation w as, is, or w ill be paid directly or indirectly, related to the specific recommendation or view s expressed by that analyst in this report; and

the recommendations indicated in this report solely and exclusively reflect his or her personal opinions and w ere prepared independently and autonomously, including in relation to Bradesco Corretora;

Bradesco Corretora, for w hich he or she w orks, may be involved in the acquisition, sale or dealing of securities of the company(ies) analyzed in this report;

pursuant to Brazilian securities exchange commission (Comissão de Valores Mobiliários – CVM) Instruction 388/03:

he or she does not receive compensation for services provided and does not have commercial relations w ith the company(ies) analyzed in this report, or w ith individuals, legal entities, funds, trusts or estates that act representing the same interest as the company(ies). How ever,

Bradesco Corretoramay receive compensation for services provided or have commercial relations w ith the company(ies) analyzed in this report, or w ith individuals, legal entities, funds, trusts or estates that act representing the same interest as the company(ies); and

his or her compensation is not linked to the pricing of any securities issued by the company(ies) analyzed in this report, or the proceeds of trades or financial operations conducted by Bradesco Corretora.

he or she has no relation w ith the persons acting w ithin the company(ies) analyzed in this report;

Company-specific regulatory disclosures

1% 2%

Bradesco Corretoraand/or its affiliates beneficially ow n one percent or more of any class of common equity securities of the subject company(ies). This position reflects information available as of the business day prior to the date of this report;

Bradesco Corretora research ratings distribution

Bradesco Corretora and/or its affiliates have received compensation for investment banking services from the subject company(ies) in the tw elve months preceding the date of publication of the research report and/or expects to receive or intends to seek compensation for investment banking services from the subject company(ies) in the three months follow ing the date of this report;

Bradesco Corretora and/or its affiliates have managed or co-managed a public or Rule 144A offering of the subject

company’s(ies’) securities in the tw elve months preceding the date of this report;

Bradesco Corretoraand/or its affiliates w ere making a market in the subjectcompany’s(ies’)equity securities at the date of this report;

Percentage of companies w ithin this rating category for w hich [investment banking] services w ere provided w ithin the past 12 months.

Bradesco Corretora ratings

Bradesco Corretora ratings are constantly revised and any temporary inconsistencies betw een the upside potential that gave rise to any such rating and the upside potential in connection w ith the target price are at all times deliberate. The official rating shall prevail.

Additional Disclosures (i) (ii) (iii) (iv) (v) General Disclosures 1) 2) 3) 4) 5) 6) 7)

This report, including the estimates and calculations of Bradesco Corretora, is based on publicly available information that it consider reliable, but it do not represent it is accurate or complete, and should not be relied upon as such.

Non-US research analysts w ho have prepared this report are not registered or qualified as research analysts w ith FINRA but instead have satisfied the registration and qualification requirements or other research-related standards of a non-US jurisdiction.

are persons to w hom an invitation or inducement to engage in investment activity (w ithin the meaning of section 21 of the Financial Services and Markets Act 2000) in connection w ith the issue or sale of any securities to w hich this report relates may otherw ise law fully be communicated or caused to be communicated (all such persons together being referred to as "relevant persons").

This report is directed only at relevant persons and must not be acted on or relied on by persons w ho are not relevant persons. Any investment or investment activity to w hich this report relates is available only to relevant persons and w ill be engaged in only w ith relevant persons. No public offer of any securities to w hich this report relates is being made by Bradesco UK or Bradesco Corretora in the United Kingdom or elsew here in the European Economic Area.

United States:This report is distributed in the United States by Bradesco Securities Inc. Bradesco Securities Inc., a U.S. registered broker-dealer and a w holly-ow ned subsidiary of Banco Bradesco S.A., is a member of FINRA/SIPC. All U.S. recipients of this report w ishing to effect transactions in securities discussed should contact and place orders through Bradesco Securities Inc. at (212) 888-9141.

Other Countries:This report, and the securities discussed herein, may not be eligible for distribution or sale in all countries or to certain categories of investors. In general, this report may be distributed only to professional and institutional investors.

Any additional information may be obtained by contacting your representative or by sending an email to [email protected]

BradescoCorretora’sand itsaffiliates’salespeople, traders and other professionals may provide oral or w ritten market commentary or trading strategies to their clients and their proprietary trading desks that reflect opinions that are contrary to the opinion expressed in this report. Such market commentary or trading strategies reflect the different time frames, assumptions, view s and analytical methods of the persons w ho prepared them, andBradesco Corretoraand its affiliates are under no obligation to ensure that such market commentary or trading strategies are brought to the attention of any recipient of this report.

This report is not an offer or a solicitation for the purchase or sale of any financial instrument. It is not intended to provide personal investment advice and it does not take into account the specific investment objectives, financial situation and the particular needs of any specific person w ho may receive this report. Investors should seek financial advice regarding the appropriateness of investing in any securities, other investment or investment strategies discussed or recommended in this report and should understand that statements regarding future prospects may not be realized.

Investors should note that income from securities or other investments, if any, referred to in this report may fluctuate and that price or value of such securities and investments may rise or fall. Accordingly, investors may receive back less than originally invested. Past performance is not necessarily a guide to future performance.Bradesco Corretoraand its affiliates do not accept responsibility for any direct or indirect loss arising due to use of this report. Investors should consider w hether any advice or recommendation in this research is suitable for their particular circumstances and, if appropriate, seek professional advice, including tax advice. Exchange rate movements could have adverse effects on the value or price of, or income derived from, certain investments.

This report has been prepared solely by Bradesco Corretora and is being provided exclusively for informational purposes. The information, opinions, estimates and projections constitute the judgment of the author as of the current date and are subject to modifications w ithout prior notice. Bradesco Corretorahas no obligation to update, modify or amend this report and inform the reader accordingly, except w hen terminating coverage of the issuer of the securities discussed in this report.

No portion of this docum ent m ay be (i) copied, photocopied or duplicated in any form , or by any m eans, or (ii) redistributed w ithout

are outside the United Kingdom, or

United Kingdom and European Econom ic Area:In the United Kingdom and elsew here in the European Economic Area, this report may be made or communicated by Bradesco Securities UK Limited ("Bradesco UK"). Bradesco UK is authorized and regulated by the Financial Services Authority and its registered office is at: 20-22 Bedford Row , London, WC1R 4JS. This report is for distribution only to persons w ho:

have professional experience in matters relating to investments falling w ithin Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (as amended, the "Financial Promotion Order");

are persons that are eligible counterparties and professional clients of Bradesco UK;

are persons falling w ithin Article 49 (2) (a) to (d) ("high net w orth companies, unincorporated associations etc") of the Financial Promotion Order;

From time to time,Bradesco Corretoraor its affiliates and officers, directors and employees, not including its analysts may, to the extent permitted by law , hold long or short positions, or otherw ise be interested in transactions in assets directly or indirectly related to this report. The follow ing disclosures are required under or based on the law s of the jurisdiction indicated, except to the extent already made above w ith respect to United States law s and regulations. Brazil:This report is distributed in Brazil byBradesco Corretora. Any investor in Brazil w ho receives this report and w ishes to conduct transactions w ith stocks analyzed herein should contact and request execution of orders throughBradesco Corretora

at (55 11) 3556-3001.

Although CVM Instruction 388/03 permits that each analyst responsible for the preparation and content of this report may hold securities of the company(ies) analyzed in this report, provided that such securities not exceed 5% of the personal assets of each and such analyst,Bradesco

Corretora’sinternal policy prohibits its analysts, professionals reporting to analysts and members of their households from ow ning securities in any company in theanalysts’area of coverage Analysts are paid in part based on the profitability of Bradesco Corretora and its affiliates, w hich includes investment banking revenues. Bradesco Corretora policy prohibits its analysts, persons reporting to its analysts or members of their

(Eco no mist)

Head of Research

Carlos Firetti, CFA 55 11 2178 5363 carlo sfiretti@bradesco bbi.co m.br

Banking

Carlos Firetti, CFA 55 11 2178 5363 carlo sfiretti@bradesco bbi.co m.br Luis Azevedo 55 11 2178 5321 luis.azevedo @bradesco bbi.co m.br

Rafael Frade, CFA 55 11 2178 4056 rafaelf@bradesco bbi.co m.br Rodrigo Geraldes 55 11 2178 4276 ro drigo @bradesco bbi.co m.br

Financial Services (non-banking) Education

Carlos Firetti, CFA 55 11 2178 5363 carlo sfiretti@bradesco bbi.co m.br Vítor Pini 55 11 2178 4274 vpini@bradesco bbi.co m.br

Rafael Frade, CFA 55 11 2178 4056 rafaelf@bradesco bbi.co m.br Ricardo Boiati 55 11 2178 5326 rbo iati@bradesco bbi.co m.br

Health Care

Rafael Frade, CFA 55 11 2178 4056 rafaelf@bradesco bbi.co m.br Ricardo Boiati 55 11 2178 5326 rbo iati@bradesco bbi.co m.br

Carlos Firetti, CFA 55 11 2178 5363 carlo sfiretti@bradesco bbi.co m.br Vítor Pini 55 11 2178 4274 vpini@bradesco bbi.co m.br

Rodrigo Geraldes 55 11 2178 4276 ro drigo @bradesco bbi.co m.br

Auro Rozenbaum 55 11 2178 5315 auro @bradesco bbi.co m.br

Bruno Varella 55 11 2178 5310 bvarella@bradesco bbi.co m.br Raphael Biderman 55 11 2178 5313 rbiderman@bradesco bbi.co m.br

Gina Montone 55 11 2178 4272 gina@bradesco bbi.co m.br

Edigimar Maximiliano 55 11 2178 5327 maximiliano @bradesco bbi.co m.br Alessandro Mady 55 11 2178 5329 alessandro tm@bradesco bbi.co m.br

Luiz Peçanha 55 11 2178 5324 pecanha@bradesco bbi.co m.br

Real Estate Vladimir Pinto 55 11 2178 5323 vladimir.pinto @bradesco bbi.co m.br

André Rocha 55 11 2178 4223 andre.ro cha@bradesco bbi.co m.br Marcelo Sá 55 11 2178 4273 marcelo .sa@bradesco bbi.co m.br

Alain Nicolau 55 11 2178 5316 alain@bradesco bbi.co m.br Fixed Incom e

Altair Pereira 55 11 2178 4279 altair@bradesco bbi.co m.br

Caio Lombardi 55 11 2178 4225 lo mbardi@bradesco bbi.co m.br

Institutional Sales Team

João Saldanha, CFA saldanha@bradesco bbi.co m.br Marcelo Cabral mcabral@bradesco securities.co m

José Arvelos arvelo s@bradesco bbi.co m.br Alison Kulach akulach@bradesco securities.co m

Juvenal Neves juvenal@bradesco bbi.co m.br Vikram Kapur vic@bradesco securities.co m

Jason Myers jaso n@bradesco securities.co m

Daniel Vaz daniel.vaz@bradesco securities.co m

Adilson dos Santos 5900.adilso n@bradesco .co m.br shin@bradesco securities.co m

bo bcallahan@bradesco securities.co m

Ana Carolina Quadros caro lina.quadro s@bradesco bbi.co m.brAlec Cunningham alec@bradesco securities.co m

Fernanda Weber Bratz fernanda@bradesco bbi.co m.br Christopher Barresi cbarresi@bradesco securities.co m

Robert Vespa ro bert@bradesco securities.co m

Dauro Zaltman dauro @bradesco bbi.co m.br

Denise Chicuta denise.chicuta@bradesco bbi.co m.br Victor Cortes victo r@bradesco securities.co m

Keite Bianconi keite@bradesco bbi.co m.br Robert Hulme rhulme@bradesco securities.co m

Roland Campbell ro land@bradesco securities.co m

Guilherme Zraick gzraick@bradesco securities.co m

Sales - Fixed Incom e – 44 203 178 4103 Sales – 44 203 178 4168

Sales - Fixed Incom e - 55 11 2178 6959 Sales Trading – 01 212 888 9141

Sales - Local Fixed Incom e - 55 11 2178 4419 Bradesco Securities UK, Ltd

Telecom , Media and Technology

Consum er Goods and Retail

Steel, Mining, Pulp & Paper

Electric Utilities, Water & Sew age Oil & Gas, Petrochem icals and Sugar & Ethanol

Transportation, Logistics, Malls and Sm all Caps

Robert Callahan

Bradesco Corretora CTVM S.A. – São Paulo

Shinichiro Fukui

Sales – 55 11 3556 3001 Sales – 01 212 888 9141

Bradesco Securities, Inc. – New York (FINRA/SIPC Mem ber)