Masters in

Finance - Financial Markets

Final Masters Project

Dissertation

Risk Profiling and the DOSPERT Scale: An Approach Using

Prospect Theory

Rui Jorge Carmo Pereira da Silva

Finance - Financial Markets

Final Masters Project

Dissertation

Risk Profiling and the DOSPERT Scale: An Approach Using

Prospect Theory

Rui Jorge Carmo Pereira da Silva

Orientation: Raquel M. Gaspar

Pedro Rino Vieira

Abstract

Compreender a forma como as pessoas se comportam e reagem quando enfrentam situa¸c˜oes envolvendo risco ´e uma componente chave para os consultores financeiros. Neste estudo ´e proposta uma tradu¸c˜ao Portuguesa da escala DOSPERT de Weber et al. (2002) e s˜ao encontrados ind´ıcios de que esta poder´a levar a uma forma simplificada, em termos de c´alculos, de obter um resultado equivalente ao coeficiente de avers˜ao `a perda proveniente da Prospect Theory. Come¸camos por validar a nossa tradu¸c˜ao da escala com uma popula¸c˜ao

Acknowledgements

List of Tables IV

List of Figures V

1 Introduction 1

2 Literature Revision 3

2.1 Expected Utility Theory . . . 3

2.2 Behavioral Finance . . . 4

2.3 Prospect Theory . . . 4

2.4 Loss Aversion . . . 5

2.5 Cumulative Prospect Theory . . . 6

2.6 The DOSPERT Scale . . . 8

3 Methodology and Results 9 3.1 Validation Stage . . . 9

3.1.1 Translation . . . 9

3.1.2 Results . . . 10

3.2 DOSPERT scale and Prospect Theory . . . 13

3.2.1 Methodology . . . 13

3.2.2 Results . . . 14

3.3 Demographic Characteristics Analysis . . . 21

3.3.1 Risk Coefficient as Dependent Variable. . . 22

3.3.2 Financial Coefficient as Dependent Variable . . . 24

3.3.3 Multinomial Logit Analysis . . . 25

4 Conclusions 28

5 References 30

Appendix A 34

Appendix C 37

Appendix D 38

I Descriptive statistics for participants’ age, overall and by gender, from the DOSPERT-PT validation stage; . . . 10 II Sub-scale domain specific Cronbach’s alpha for Risk Taking, Expected

Ben-efits and Risk Perception; . . . 11 III Total-Item Correlations by sub-scale and domain for the Portuguese,

Ger-man and English DOSPERT scales; . . . 12 IV Descriptive statistics from the comparison stage . . . 15 V Reliability and internal consistency results from the comparison stage . . . 16 VI Risk-Taking sub-scale results from the comparison stage . . . 17 VII Pearson correlations between Loss Aversion, Risk Coefficient, the Financial

domain and its two sub-domains; . . . 18 VIII Models fit with Loss Aversion as dependent variable and the Financial

do-main as predictor; . . . 19 IX Models fit with Loss Aversion as dependent variable and the Gamble

sub-domain as predictor; . . . 20 X Individual significance tests with Risk Coefficient as the dependent variable

and the personal characteristics as predictors . . . 23 XI Individual significance tests with Financial coefficient as the dependent

vari-able and the personal characteristics as predictors . . . 25 XII Participant’s distribution according to their risk profile based on the overall

DOSPERT-PT coefficient; . . . 26 XIII Participant’s distribution according to their risk profile based on the

List of Figures

2.1 Value Function from Kahneman and Tversky (1992); . . . 7 2.2 Probability Weighting Function from Kahneman and Tversky (1992); . . . 7

3.1 Scatter plot with the relationship between the Risk Coefficient and the Expected-Benefits sub-scales; . . . 13 3.2 Scatter plot with the relationship between the Risk Coefficient and the

Risk-Perception sub-scales; . . . 13 3.3 Fit plot of tested models with Loss Aversion as dependent variable and the

Financial domain as independent variable; . . . 19 3.4 Fit plot of tested models with Loss Aversion as dependent variable and the

Finding the adequate investment for each investor has always been a key factor to a suc-cessful financial adviser. One of the most important tools available for financial advisers to do just that, is their clients risk profile, which is obtained through profile questionnaires designed to understand how investors react when faced with financial decisions involving risk, and to assess their willingness to deal with potential losses ergo, their risk aversion.

Despite the fact that Expected Utility Theory by von Neumann and Morgenstern (1947) is still considered the mainstream way to measure and understand investors decision making process, many authors disagree with the effectiveness of the axioms that guide that theory and propose different approaches. One of those alternatives is Prospect Theory, proposed and developed by Kahneman and Tversky (1979, 1992) as a descriptive model to predict people’s decision making process. This theory departs from the normative foundations and utility maximization by rational agents that characterize Expected Utility, in favor of the following key components:

• The value and utility come from the changes in wealth and not the final assets position;

• The value function is concave for gains and convex and steeper for losses (leading to the risk averse and risk seeking behaviors respectively plus the phenomena of loss aversion);

• Decision weights inferred from choices between gambles do not coincide with stated probabilities;

• The weighting function relates decision weights and probabilities and allows mod-eling of the probability distortion that results from the fact that individuals treat probabilities as non linear;

• The weighting function exhibits overweighting of small probabilities and under-weighting of large probabilities;

high probability and risk aversion for small probability losses and risk seeking for small probability gains;

There are however other approaches to the study of decision making process. As stated in Kahneman and Tversky (1984) that process is complex and can be comprehended in several fields of study. Psychology, for instance, plays a big role in the way we structure and make our decisions and there is one particular psychometric scale that tries to cap-ture people’s risk profile in several domains of activity (namely financial, ethical, social, recreational and health and safety). That scale, named DOSPERT (Domain Specific Risk Taking scale) was presented by Weber et al. (2002) with the aforementioned objective and also to measure the impact of how we perceive risks and benefits in our disposition to engage in risky behaviors. We believe that it would be interesting to take advantage of DOSPERT’s psychometric capabilities to accurately capture people’s risk profile, and apply that in a financial context.

The question one can pose is if there is a way to measure someone’s risk aversion coef-ficient that is compatible with the result given by Prospect Theory, without using complex situations to assess it. That is the question this study tries to answer, if the DOSPERT scale can be used in a financial application, specifically to offer a simpler way to obtain a risk coefficient equivalent to Prospect Theory’s loss aversion coefficient.

measured by the DOSPERT scale in section 3.3 and conclude in chapter 4.

Chapter 2: Literature Revision

2.1

Expected Utility Theory

The mainstream way to measure individual’s choice and their decision making process is, according to Levy and Levy (2002), Expected Utility Theory (EUT), proposed by von Neumann and Morgenstern (1947). These authors brought forth EUT by proposing a set of axioms, both necessary and sufficient, to represent people’s decision making process based on the maximization of expected utility. This theory is based in the fact that investors are rational, want to maximize their utility and operate in efficient markets. Their decision making process is supported on the four axioms by Von Neumann-Morgenstern:

• Completeness - People show preference between lotteries: L1L2, L2L1, or both;

• Transitivity - If L1 L2 and L2 L3, then L1 L3;

• Continuity - There is a combination of pL1 + (1-p)L3 L2, but there is also other

that makes L2 pL1 + (1-p)L3;

• Substitution - If L1 L2, then pL1 + (1-p)L3 pL2 + (1-p)L3;

Rui Silva Risk Profiling and the DOSPERT Scale

small probability gambles. Still, arguably, the two most popular and studied critiques to this theory come from Allais (1953) and Prospect Theory. The Allais Paradox showed that the substitution axiom from EUT was violated when looking at empirical data and set the field for Kahneman and Tversky (1979) that conducted an experiment with a series of choice problems to comprehend the decision making process. Using the results, the au-thors identify several violations of EUT assumptions resulting from effects that generally occur in the decision making process but that are not explained by that theory.

2.2

Behavioral Finance

So, when dealing with investors risk profiles and behavior, we need to enter the realm of Behavioral Finance, since the traditional financial theory is not enough to fully understand investors’ actions. The importance of Behavioral Finance when studying relationships be-tween who the investor is, and how he reacts to certain market events, lies in the ability to offer new solutions and interpretations that traditional finance and its assumptions usually do not cover. Ritter (2003) provides a brief introduction to behavioral finance which tries to understand the investors without the usual assumptions of expected utility maximization with rational investors in efficient markets.

2.3

Prospect Theory

Pioneering the Behavioral Finance paradigm, Prospect Theory was presented by Kahne-man and Tversky (1979), introducing the fundamentals of a new descriptive theory that incorporates and models the behavioral tendencies found to violate traditional expected utility axioms. Since then, other models for decision making under risk and uncertainty have been proposed but we will focus on prospect theory. A good review of those models and their performance according to fit and parsimony can be found in Harless and Camerer (1994).

The value function replaces the utility function over states of wealth and focuses on gains or losses in relation to the status quo1

. This function is concave above the reference point (gains) and convex below it (losses), leading to a risk seeking behavior for losses and risk aversion when considering gains. Using firms and sectors instead of individuals, Fiegenbaum and Thomas (1988) studied the risk-returned paradox in light of behavioral decision theories available at the time (like PT) and found support for risk aversion in the gains domain and risk seeking when facing losses, results robust within and across indus-tries for the time frame studied (1960-1979). Another characteristic of the value function is the fact that this s-shaped function is steeper for losses than for gains (something that would lead to the concept of loss aversion as seen in Kahneman and Tversky (1984)) since the pleasure obtained from gaining a sum of money is lower than the “pain” from losing an equal amount.

Gonzalez and Wu (1999) describe the weighting function as a way to measure people’s tendency to distort probabilities when faced with risky decisions, by underweighting large probabilities and overweighting small ones. In prospect theory, the value of an outcome does not depend on subjective probabilities but on non linear decision weights that do not need to obey probability axioms and should not be interpret as such, as stated by Kahneman and Tversky (1979). The weighting function acts as the bridge between deci-sion weights and stated probabilities and is compatible with the four properties that their empirical analysis found on the weighting function (overweighting of small probabilities, subadditivity, subcertainty and subproportionality).

2.4

Loss Aversion

A concept brought forth by prospect theory was loss aversion, a phenomena found in decisions under risk and uncertainty, that comes from the idea that losses have a bigger impact than an equal amount of gains, seen in the steeper value function for losses (Tver-sky and Kahneman (1991)). Other way to put it was tested in Kahneman et al. (1990) where people asked for a larger compensation to let go of an object they had possession, than what they were willing to pay for it in the first place, something that was presented by Thaler (1980) as the endowment effect. Benartzi and Thaler (1995) study the equity premium puzzle identifying the concept of myopic loss aversion and finding that prospect theory, and loss aversion especially, can explain the premium differences between equities and bonds. Camerer (1998) provides a good review of other common patterns of decision

1

Rui Silva Risk Profiling and the DOSPERT Scale

making that can be explained by loss aversion. There are several ways to calculate the loss aversion coefficient and a good review of such methods can be found in Abdellaoui et al. (2007). This study also provides a non parametric method that, according to the authors, has the advantage of not depending on functional forms. Bond and Satchell (2006) also incorporate loss aversion in their work, studying volatility forecasts for financial applica-tions that account for asymmetries and distorapplica-tions, in preferences and returns.

2.5

Cumulative Prospect Theory

In light of the critiques made by some authors regarding traditional prospect theory, Tver-sky and Kahneman (1992) presented an improved version called Cumulative Prospect The-ory (CPT). This would deal with the main points of disagreement with the assumptions and conclusions of the aforementioned theory regarding stochastic dominance violations2

.

According to Tversky and Kahneman (1992), to improve on the previous version and some of its inconsistencies, CPT departs from the monotonic transformation of the out-come probabilities, allowing it to avoid violating stochastic dominance assumptions (with-out resorting to editing procedures), and also accommodate prospects with a larger number of outcomes than before. While the first version of prospect theory was designed for deci-sions under risk with two non-zero outcomes at most, CPT introduces the ability to deal with decisions under uncertainty and the capacity to adjust to any number of possible (finite) outcomes. This is done using the cumulative functional for both risk and uncer-tainty, separately for gains and losses to allow different decision weights for each, leading to outcomes being weighted by the cumulated probabilities of obtaining them. In CPT decisions weights now sum up to the unity in the case of gains or losses but, when mixed prospects are considered, the sum can be higher or lower than one.

This new theory explains risk aversion and risk seeking using the value function and the cumulative weighting functions, that can be seen in Figures 2.1 and 2.2 and one of its central contributions is the so called “fourfold pattern of risk attitudes”. According to Tversky and Kahneman (1992) and considering only the non mixed prospects, i.e. gains and losses, the value and weighting functions suggest risk aversion for gains and risk seeking behaviors for losses when dealing with moderate or high probability outcomes. The opposite happens when dealing with small probabilities, with risk aversion for small

2

probability of a loss and risk seeking for gains in that same condition.

Figure 2.1: Value Function from Kahneman and Tversky (1992);

Figure 2.2: Probability Weighting Function from Kahneman and Tversky (1992);

Prospect Theory (CPT) is considered for many practical uses. De Giorgi and Hens (2009) for instance, believe that it describes well how investors perceive risk and that means a closer look to this theory should be given with wealth management in perspective, backing up their opinion with empirical analysis where CPT reveals itself superior to Mean-Variance Theory. This study also argues against Markowitz (1952) conclusion that volatility aversion is the only measure of risk, in favor of PT’s loss aversion3

. According to

3

De Giorgi and Hens (2009), their results reveal that the added value to wealth management firms generated by the use of PT to create efficient portfolios is bigger than the cost to implement it and that if PT was used in the risk profiling stage, gains could even be bigger. Levy et al. (2003) argue that adopting CPT as the descriptive model for decisions under risk does not invalidate the CAPM model as the standard asset pricing model, since the SML theorem remains intact. They also point that if both mean-variance theory and CPT are compatible with first order stochastic dominance (FSD), the portfolio choice by FSD is optimal in both cases. Levy and Levy (2004) also studied possible relations between mean variance analyses and prospect theory, leading them to conclude that efficient portfolios from these theories almost coincide4

, meaning that would be possible to use MV algorithms to construct efficient PT portfolios, with the PT set being a sub-set of the MV efficient set.

2.6

The DOSPERT Scale

The DOSPERT scale plays a crucial part in this study and represents a useful tool when it comes to understanding people and measuring their attitudes towards risk. Like pre-viously mentioned, the scale was presented in Weber et al. (2002) to understand if there were differences between people’s risk profile when considering different domains, and was later translated and applied in different areas (see Center for Decision Sciences (2010)). The scale is divided in 3 sub-scales designed to measure people’s proneness to engage in risk behaviors, the benefits expected from those behaviors and how risky they are per-ceived. In Weber et al. (2002) the authors concluded that the degree of risk taking was different depending on the domain and that women tended to be more risk averse. They also noted that the domain and gender differences stem from differences in perception and expectations regarding the risky behaviors, with results showing that the higher the expected benefits from one activity, the higher the propensity to engage in said activity, and the exact opposite when it comes to the perceived risk associated with that activity. Using a German translated version of this scale in Johnson et al. (2004) the potential for cross cultural studies was tested. The scale’s latest version from Blais and Weber (2006) has reduced and revised the number of items from 40 to 30, 6 questions in each domain, to generalize them to wider ranges of age and cultures, improving its value as a cross cultural instrument.

allows for different portfolios based on PT;

4

Chapter 3: Methodology and Results

This study will be divided in two parts. The first part of this study will cover both the translation and application to a Portuguese population of the DOSPERT scale, in order to validate and use the full scale in Portuguese, something that, to the best of our knowledge, has not been done before. The second part will be the application of the translated Risk Taking sub-scale in conjunction with Prospect Theory (CPT), to a sample of Portuguese students from ISEG, to assess whether or not that sub-scale, can stand as a suitable method to evaluate people’s risk profiles, and thus whether the DOSPERT can be used in financial applications. The second part of this study will also contain tests to check whether some personal characteristics of the participants have impact on their risk profile, as measured by the DOSPERT scale.

3.1

Validation Stage

3.1.1 Translation

The first part of the validation process was the translation. Using Brislin’s back-translation method (Brislin and Freimanis (1995)), we translated the DOSPERT’s 30 items and 3 sub-scales1

from English to Portuguese and then back to English to check for descrepancies. The next step was a pre-test with colleagues to revise and perfect the Portuguese ver-sion (from now on DOSPERT-PT, see Appendix A). Participants were asked to fill the 30 items in all three subscales, rating each item from “1 Extremely Unlikely” to “7 -Extremely Likely” in the Risk-Taking sub-scale allowing us to measure their propensity to engage in the described risky behaviors; from “1 - No Benefits at all” to “7 - Extreme Benefits” in the Expected-Benefits sub-scale, where we wanted to evaluate the benefits each participant saw in the described activity or behavior; and from “1 - Not at all Risky” To “7 - Extremely Risky” in the Risk-Perception sub-scale, where we asked participants to evaluate how risky they perceived each situation based on their gut feeling. The feedback was positive and no unexpected questions were asked about the items or the sub-scales which made us comfortable with our translated DOSPERT-PT version, leaving our 30

1

Rui Silva Risk Profiling and the DOSPERT Scale

item scale with 29 of its original items plus a slightly altered one2

.

3.1.2 Results

After the conclusion of the translation and pre-testing phase, we moved on to the validation of the full DOSPERT-PT. This stage was conducted in two separate days, in six random classes from Instituto Superior de Economia e Gest˜ao (ISEG), with College and Master students. A total of 123 students participated in the study and, as seen in Table I, we got 103 valid responses, 45 from male individuals (43,69%) and 58 from female individuals (56,31%), with an average age of 22,83 years ranging from 19 to 44 years old.

Table I: Descriptive statistics for participants’ age, overall and by gender, from the DOSPERT-PT validation stage;

N N (%) Avrg AGE Max AGE Min AGE Males 45 43,69% 23,18 38 19 Females 58 56,31% 22,57 44 19 Overall 103 100% 22,83 44 19

The male, female and overall sample mean coefficient (in our 7 point scale) and stan-dard deviations for each sub-scale, by domain, are presented in Appendix B thru D, as well as the alpha for each sub-scale by gender and overall.

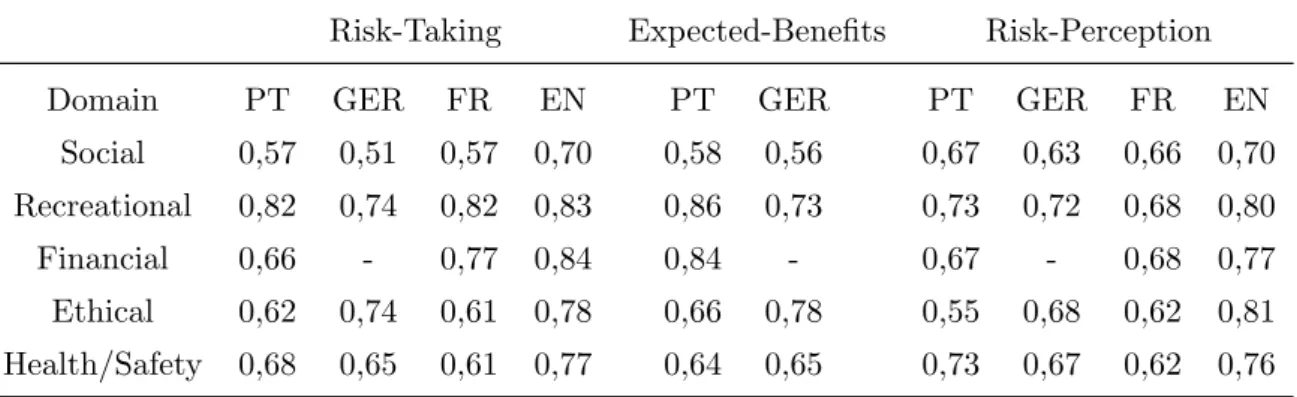

In Table II we have reliability tests computed using SPSS for the DOSPERT-PT scale and other DOSPERT versions with domain specific Cronbach’s Alpha for Risk-Taking, Expected-Benefits and Risk-Perception. The Cronbach alpha is a measure of reliability from internal consistency. The values for the DOSPERT scales in German, French and English were obtained from previous DOSPERT applications (Weber et al. (2002); Johnson et al. (2004); Blais and Weber (2006)). Also note that the English and German versions had 40 items while both our version and the French one had only 30 items. Starting by the Risk-Taking sub-scale we see that our values are overall in line with previous applications, with the Social domain presenting the lowest value for the alpha (our scale matches the French one with an alpha of 0,57 and both are higher than the German version that stands at 0,51) and the Recreational domain providing the highest one. The original version (English) provides the higher values overall, and the Recreational domain is where the

2

other scales come closer to the original version (0,83) and again our scale and the French one are tied with 0,82 while the German scale provides an alpha of 0,74. In the Financial domain there is no value for the German version to compare with since the authors separate gambling and investment in their paper. Our scale provides an alpha of 0,66, lower than the 0,77 value for the French scale. Our scale had the highest Health/Safety alpha with 0,68 followed by the German one at 0,65 while the French presented an alpha of 0,61.

In the next sub-scale, Expected-benefits, there is no comparison available for the En-glish and French versions due to lack of data. In this sub-scale our version had higher alpha values in the Social and Recreational domains (0,58 and 0,86 versus 0,56 and 0,73) and lower alpha values in the Ethical and Health/Safety domains (0,62 and 0,68 versus 0,74 and 0,65). It is relevant to note that our Financial domain had a solid alpha value of 0,84, higher than both the gambling and investment ones provided in the German version. In the Risk-Perception sub-scale we again have all the four versions to compare results. The English version still reigns supreme in the alpha department showing its highest value in the Ethical domain (0,81) and the lowest one again in the Social domain (0,7). None of the other scales follow this exact trend. Our scale (that this time provides results above the other two scales in all domains except Ethical and Financial) has its highest value of the Cronbach’s alpha in both Health/Safety and Recreational domains with 0,73 and the lowest in the Ethical domain (0,55).

Table II: Sub-scale domain specific Cronbach’s alpha for Risk Taking, Expected Benefits and Risk Perception; note that German, French and English results were obtained from previous DOSPERT applications;

Risk-Taking Expected-Benefits Risk-Perception Domain PT GER FR EN PT GER PT GER FR EN

Social 0,57 0,51 0,57 0,70 0,58 0,56 0,67 0,63 0,66 0,70 Recreational 0,82 0,74 0,82 0,83 0,86 0,73 0,73 0,72 0,68 0,80 Financial 0,66 - 0,77 0,84 0,84 - 0,67 - 0,68 0,77 Ethical 0,62 0,74 0,61 0,78 0,66 0,78 0,55 0,68 0,62 0,81 Health/Safety 0,68 0,65 0,61 0,77 0,64 0,65 0,73 0,67 0,62 0,76

Rui Silva Risk Profiling and the DOSPERT Scale

obtained in all sub-scales.

Table III: Total-Item Correlations by sub-scale and domain for the Portuguese, German and English DOSPERT scales;

DOSPERT-PT DOSPERT-G DOSPERT-EN

Domain RT EB RP RT EB RP RT RP

Social 0,33 0,35 0,40 0,51 0,56 0,63 0,40 0,40 Recreational 0,59 0,65 0,46 0,74 0,73 0,72 0,55 0,50 Financial 0,39 0,61 0,41 - - - 0,57 0,47 Ethical 0,35 0,39 0,29 0,74 0,78 0,68 0,50 0,53 Health/Safety 0,41 0,36 0,47 0,54 0,54 0,55 0,47 0,46

A Rotated Factor Matrix for each sub-scale, used for Factor Analysis, was computed once again using SPSS to check for factor loadings (i.e. to check whether our a priori classification of the items in their domains was in line with what the results show). The extraction method used was alpha factoring and the rotation method was Varimax with Kaiser normalization, a method that as noted in Pahor (2011) is based on orthogonal rotation designed to simplify the interpretation. Our results are solid with mostly good loadings for every sub-scale.

Figures 3.1 and 3.2 provide scatter plots to check the relationship between the Risk-Taking sub-scale and the other two sub-scales at an individual level. This is not part of our proposed investigation but it is something we believe that provides insight into people’s decision process when faced with risky situations. It is also something that was tested in previous DOSPERT applications. In Figure 3.1 we see a positive relation between risky behaviors and the benefits participants expect to get from those behaviors. The larger the expected benefit, the more prone to engage in risky behaviors these subjects seem to be. Figure 3.2 shows the relationship between Risk-Taking (namely its result Risk Coefficient) and Risk-Perception and, as expected, there seems to be a negative tendency, i.e., the riskier we perceive a situation, the less we are compelled to engage in that risky behavior.

Figure 3.1: Scatter plot with the relation-ship between the Risk Coefficient and the Expected-Benefits sub-scales;

Figure 3.2: Scatter plot with the relation-ship between the Risk Coefficient and the Risk-Perception sub-scales;

3.2

DOSPERT scale and Prospect Theory

This section covers the second part of this study, the use of the DOSPERT-PT in conjunc-tion with Prospect Theory to find evidence that it can be used in financial applicaconjunc-tions, namely to predict a risk coefficient that is compatible with the Loss Aversion coefficient given by Prospect Theory.

3.2.1 Methodology

After validating the DOSPERT-PT as a whole, we used one of its sub-scales, Risk-Taking, to predict people’s risk profile, that we named Risk Coefficient (obtained by the average of a person’s score in each domain), and compare it to CPT’s Loss Aversion coefficient. This sub-scale gives us a result from 1 to 7, with 1 being the more risk averse possible and 7 being the more risk seeking possible.

In order to compare those results we built a questionnaire with three stages . The first one was designed to obtain loss aversion and the second stage contained the questions to obtain the Risk Coefficient. This way, we would have a Loss Aversion coefficient and a Risk Coefficient for each person that participated. The third section covered the personal data gathering that will be approached in the designated section further ahead.

Rui Silva Risk Profiling and the DOSPERT Scale

were answering. In the gain’s prospects, the participants faced the dilemma that con-sisted in the choice between which of the presented sure gains would lead them to keep that amount, and in which would they prefer a gamble for larger gains. That gamble had designated probabilities for a bigger gain and for no gain at all. The participants faced a similar choice in the losses’ prospects but this time they had sure losses and a gamble that could lead to bigger or no losses. In the mixed prospects, respondents were faced with prospects in a pair, and asked to fill in what value would they need to get in one of the prospects to see both as equally risky or rewarding. This way several certain equivalents were calculated in order to obtain the loss aversion coefficient by the method described in Tversky and Kahneman (1992) and Gonzalez and Wu (1999). The loss aversion cal-culations were done in parthership with Ana Cunha and are reported in Cunha (2012). It is important to note that we did not use monetary incentives due to the fact that in the literature, several previous studies showed that there was no significant impact on the results when subjects were paid and when they were not. Examples of those findings are given in Kachelmeier and Shehata (1992) where the authors presented a study done with Chinese students that offered real and high payments (up to triple their average monthly income) and again found no evidence of different results.

The second stage contained the already tested and validated Risk-Taking sub-scale of our DOSPERT-PT scale, that we used to obtain participant’s Risk Coefficient (defined before as one’s propensity to engage in risky behaviors).

3.2.2 Results

After building and testing the questionnaire we used the QUALTRICS online platform to conduct our survey, and thru ISEG services we sent the links to a random selection of present and former ISEG students gathering 159 responses.

who stated that they have only finished high-school, meaning they are still doing their college degree in ISEG.

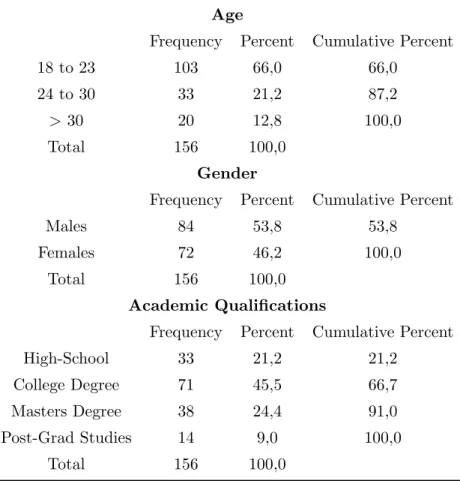

Table IV: Descriptive statistics from the comparison stage for participants age, gender and academic qualifications;

Age

Frequency Percent Cumulative Percent

18 to 23 103 66,0 66,0

24 to 30 33 21,2 87,2

>30 20 12,8 100,0

Total 156 100,0

Gender

Frequency Percent Cumulative Percent

Males 84 53,8 53,8

Females 72 46,2 100,0

Total 156 100,0

Academic Qualifications

Frequency Percent Cumulative Percent

High-School 33 21,2 21,2

College Degree 71 45,5 66,7 Masters Degree 38 24,4 91,0 Post-Grad Studies 14 9,0 100,0

Total 156 100,0

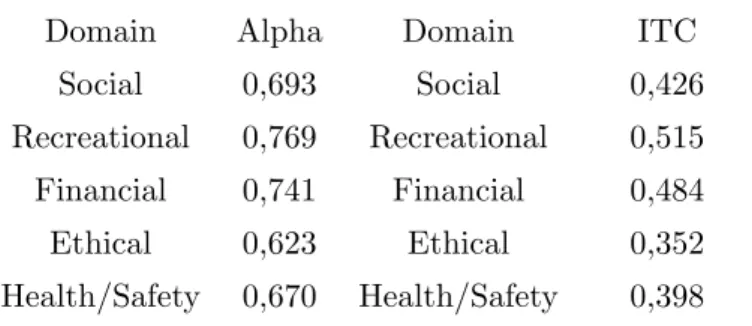

To confirm validity and consistency we repeated the validation tests with this new sample. Results are in Table V with the most relevant new data being the improvement of the alphas (especially for the Financial domain to 0,741) further supporting our confidence in our scale and the results it provides.

Rui Silva Risk Profiling and the DOSPERT Scale

Table V: Reliability and internal consistency results from the comparison stage (Cronbachs Alpha and Item-Total Correlations by domain);

Reliability and Internal Consistency Results:

Domain Alpha Domain ITC Social 0,693 Social 0,426 Recreational 0,769 Recreational 0,515 Financial 0,741 Financial 0,484 Ethical 0,623 Ethical 0,352 Health/Safety 0,670 Health/Safety 0,398

need be. The item-total correlation seems to back this up with values of 0,668 and 0,562 for Gamble and Investment respectively.

Table VI shows the average Risk Coefficient value per gender and domain, plus its standard deviations and the Cronbach’s Alpha by gender and overall. In the overall sam-ple, the Social and Recreational domains present the highest mean value (5,05 and 3,57 respectively), followed by the Financial domain (3,45). The Ethical domain has the lowest mean value at 2,51 meaning our sample is less likely to engage in risky behaviors connected to it. The highest standard deviation presents itself in the Recreational domain with 1,27. On the opposite side is the Social domain, having the smaller standard deviation at 0,85. The mean of all domains (Risk Coefficient) for our sample is 3,521 in our 7 point scale. Looking at our male participants only (n = 84), the pattern from the overall sample is still present in both means and standard deviations. The average Risk Coefficient for male respondents is 3,6687 points, higher than the female (3,348) and overall samples. Looking at the Cronbach’s Alpha for our male participants we see a standardized value of 0,711, higher than both the 0,708 overall and female participant’s alpha 0,674. The female respondents (n = 72) followed similar patterns but with values smaller than males.

Table VI: Risk-Taking sub-scale mean and standard deviation results by gender in each domain from the comparison stage;

Risk Taking Sub-Scale

Domain Males Females Overall Mean (StDev) Mean (StDev) Mean (StDev) Social 5,101 (0,797) 4,998 (0,906) 5,053 (0,848) Recreational 3,704 (1,21) 3,403 (1,331) 3,565 (1,271) Financial 3,639 (1,005) 3,225* (0,995) 3,448 (1,018) Ethical 2,708 (0,928) 2,271* (0,744) 2,506 (0,873) Health/Safety 3,191 (1,088) 2,843* (1,012) 3,030 (1,065)

Sub-Scale Alpha 0,711 0,674 0,708

(*) difference between male and female participants is statistically significant.

in the situations described in this scale). The Social and Recreational domains showed p-values above 0,05, so we cannot conclude that there is any difference in risk taking in those domains between men and women.

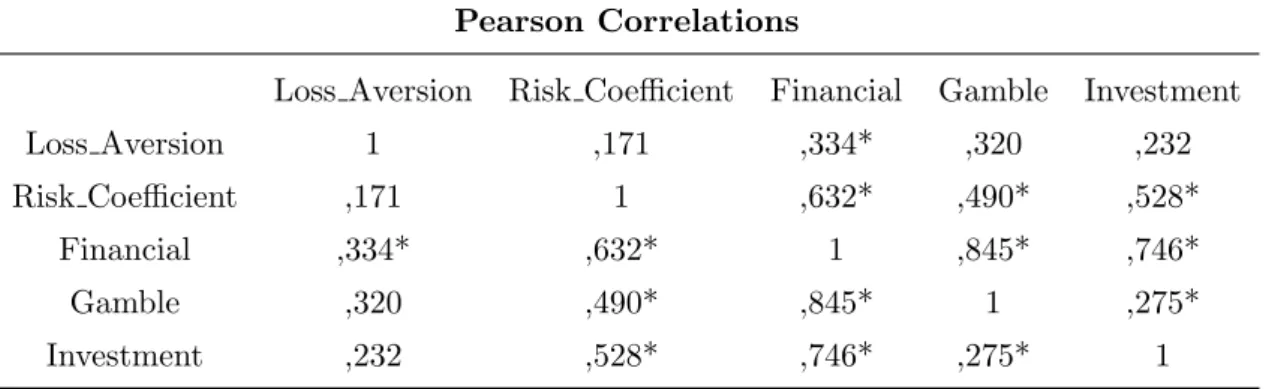

After analyzing our sample, we moved on to the main point. Having calculated the Loss Aversion coefficient, we found out that there were only 36 answers to the first part of our questionnaire that were consistent. As shown in Fox and Poldrack (2008) regarding previous Prospect Theory work, consistency from respondents is usually a problem. With this in mind, we were satisfied with our sub-sample of 36 participants that was used to test the DOSPERT-PT’s Risk Coefficient and Prospect Theory’s Loss Aversion coeficient. We started by searching for correlations between our key variables (Loss Aversion, Risk Coefficient and the Financial risk coefficient) and, since all were normally distributed, we computed Pearson Correlations between them, plus “Gamble” and “Investment” sub-domains. Table VII shows the correlations between the referred variables and the results are somewhat expected.

Rui Silva Risk Profiling and the DOSPERT Scale

Table VII: Pearson correlations between Loss Aversion, Risk Coefficient, the Financial domain and its two sub-domains;

Pearson Correlations

Loss Aversion Risk Coefficient Financial Gamble Investment

Loss Aversion 1 ,171 ,334* ,320 ,232

Risk Coefficient ,171 1 ,632* ,490* ,528*

Financial ,334* ,632* 1 ,845* ,746*

Gamble ,320 ,490* ,845* 1 ,275*

Investment ,232 ,528* ,746* ,275* 1

*. Correlation is significant at the 0.05 level (2-tailed).

loss aversion, since the point of the full scale is to measure people’s distinct risk profile in different domains; and that on the other hand, the Financial domain would be a signifi-cant variable when compared to loss aversion. After separating the Financial domain, we expected that both sub-domains were correlated with loss aversion and the fact that only Gamble is, inspires us to further analyze this issue.

0,047.

Table VIII: Models fit with Loss Aversion as depen-dent variable and the Financial domain as predictor;

Model Summary and Parameter Estimates

Dependent Variable:Loss Aversion

Equation Model Summary

R Square F df1 df2 Sig. Linear 0,111 4,263 1 34 0,047 Power 0,061 2,208 1 34 0,147 Logarithmic 0,091 3,409 1 34 0,074 Logistic 0,078 2,879 1 34 0,099

The independent variable is Financial.

This test suggests that the best way to try to capture the relationship between the Financial Coefficient and the Loss Aversion coefficient is using the linear regression. Figure 3.3 shows the model’s fit.

Figure 3.3: Fit plot of tested models with Loss Aversion as dependent variable and the Financial domain as independent variable;

Rui Silva Risk Profiling and the DOSPERT Scale

Table IX: Models fit with Loss Aversion as dependent variable and the Gamble sub-domain as predictor;

Model Summary and Parameter Estimates

Dependent Variable:Loss Aversion

Equation Model Summary

R Square F df1 df2 Sig. Linear 0,102 3,87 1 34 0,057 Power 0,05 1,804 1 34 0,188 Logarithmic 0,073 2,672 1 34 0,111 Logistic 0,079 2,913 1 34 0,097

The independent variable is Gamble.

The last independent variable tested was the Investment Coefficient. The fit tests sug-gest this variable has no relationship with loss aversion. This comes as a surprise since we expected both Financial sub-domains to be somewhat related to loss aversion.

This models fit test allowed us to restrict our comparison tests to the Financial domain and the Gamble sub-domain and we did Linear Regressions with Loss Aversion as the dependent variable and those coefficients as independent ones. The first regression was Loss Aversion by the Financial Coefficient (the result from the financial domain for each participant) and we obtained a R2

of 0,111, an F-Statistic of 4,263 with a p-value of 0,047 for our model and Equation (3.1):

Loss Aversion= 0,775 + 0,334.F inancial+ǫ (3.1)

This confirms that there is a statistically significant linear relation between the Loss Aversion coefficient measured by Prospect Theory and the Financial Coefficient measured by the DOSPERT-PT scale. We then proceeded into the second linear regression, Loss Aversion by the Gamble sub-domain which produced Equation (3.2):

Loss Aversion= 0,877 + 0,320.Gamble+ǫ (3.2)

This model presented a R2

Figure 3.4: Fit plot of tested models with Loss Aversion as dependent variable and the result from the Gamble sub-domain as independent variable;

this particular way of calculating a person’s loss aversion captures its position to gam-ble prospects and situations better than its position in other financial issues. Similar division of the Financial domain was tested in previous DOSPERT applications and a possible explanation for this fact can be found in March and Shapira (1987). The authors found that managers tend to consider investment and gambling decisions as different sets, the former involving a more controllable decision making process, and the later a more chance/luck based process, thus providing a possible explanation as to why one of the sub-domains has predictor value and the other does not. Nonetheless, the whole Financial domain from the DOSPERT-PT’s Risk-Taking sub-scale seems capable of explaining or predict the loss aversion coefficient which leads us to a possible conclusion to the ques-tion we were asking. The DOSPERT-PT scale showed potential to be used in financial applications, particularly its Financial domain shows promise of being a step to obtain a proxy to people’s loss aversion as measured by financial theory, namely Prospect Theory.

3.3

Demographic Characteristics Analysis

Rui Silva Risk Profiling and the DOSPERT Scale

and area, area of residence and their current employment status.

3.3.1 Risk Coefficient as Dependent Variable

Table X: Individual significance tests with Risk Coefficient as the dependent variable and the personal characteristics as predictors;

I.V. F-Statistic p-value Type Method R2

GENDER 8,691 0,004 Nominal glm 0,053 A Studies 1,155 0,329 Nominal glm 0,022 WORK 1,779 0,154 Nominal glm 0,034 RES 1,036 0,429 Nominal glm 0,252 AREAF 2,717 0,032 Nominal glm 0,073 AREAM 0,054 0,994 Nominal glm 0,002 AGE 2,854 0,093 Ordinal CatReg 0,020 EDUC 1,319 0,271 Ordinal CatReg 0,013 INCOME 8,089 0,000 Ordinal CatReg 0,048 LivCond 6,390 0,002 Ordinal CatReg 0,038 EDUCF 3,176 0,045 Ordinal CatReg 0,049 EDUCM 7,509 0,000 Ordinal CatReg 0,044

Dependent Variable: Risk Coefficient.

the father’s area of studies. Five dummies were created using the GLM command in SPSS one for each category (Economics/Management, Arts, Humanities, Sciences and Other) just like before. Despite the fact that it has a p-value below 0,05, the dummy variables apart from AREAF4 (Sciences) have no statistical significance. There is no evidence of differences in the impact caused between them and the reference group (AREAF5=other area of studies), but if the father’s area of studies is AREAF4, it seems to translate into a bigger propensity to engage in risky situations than if the father of the participant has education in an area different from those we mentioned in the questionnaire. The next tested variable was AREAM, which represents the mother’s area of studies. Once again five dummies were created for the same areas tested for the fathers and both the F-statistic and the coefficients p-values show that their mother’s field of studies has no impact on people’s Risk Coefficient.

Rui Silva Risk Profiling and the DOSPERT Scale

each of the independent variables. The first ordinal variable tested using the CATREG command was AGE. This variable is statistically significant at the 10% level (p-value 0,093) as seen in Table X meaning the participants age may have some impact on their Risk Coefficient, namely a positive impact (the higher the age, the higher the risks taken) since theβ is positive. This is in line with Wang and Hanna (1997); Halek and Eisenhauer (2001) where the higher the age, the lower is risk aversion. The next tested variable was EDUC, a variable that reflects the participant’s academic qualifications. According to Ta-ble X this variaTa-ble is not statistically significant which means that based on our sample, there is no relation between the academic education one completes, and one’s propensity to engage in risky situations. The next variable analyzed was INCOME that represents the monthly income from our participants, including salary and allowences. Since the coefficient is statistically significant (p-value = 0,00), we conclude that people’s monthly income has in fact importance when predicting their Risk Coefficient, and that someone who tends to have higher monthly income, also tends to engage more in risky activities, the opposite of what Cunha (2012) found. The variable LivCond, which includes the par-ticipant’s perception of their living conditions (below average, average and above average), was the next analyzed variable. We can see in Table X that it has a p-value below the 5% level (0,002) which leads us to believe that this variable has statistical significance and, due to the positive value of itsβ, there seems to be a positive relation between the variables, meaning that, on average, the higher someone sees their own living conditions, the more that person tends to engage in risky activities. The last two variables are EDUCF and EDUCM that represent the father’s and the mother’s level of education, respectively, and both are statistically significant with (β > 0) and the higher their education, the higher that person’s tendency to engage in risky activities is, on average.

3.3.2 Financial Coefficient as Dependent Variable

After testing the impact of several personal characteristics from our participants in their global attitude towards risk, we questioned ourselves if there would be similar results when considering the Financial domain coefficient, i.e. the propensity to engage in risky behaviors when faced with financial risky decisions. We tested the same twelve inde-pendent variables as before, again using the GLM command for the nominal variables we found out that there were less predictors with clear impact on our new dependent variable. GENDER is still statistically significant when we consider attitudes towards financial risky decisions, with males again being more prone to risky behaviors.

Table XI: Individual significance tests with Financial coefficient as the dependent variable and the personal characteristics as predictors;

I.V. F-Statistic p-value Type Method R2

GENDER 6,651 0,011 Nominal glm 0,041 A Studies 2,501 0,062 Nominal glm 0,047 WORK 0,395 0,757 Nominal glm 0,008 RES 0,763 0,830 Nominal glm 0,199 AREAF 0,829 0,509 Nominal glm 0,023 AREAM 0,287 0,886 Nominal glm 0,008 AGE 1,023 0,313 Ordinal CatReg 0,017 EDUC 1,446 0,239 Ordinal CatReg 0,015 INCOME 1,177 0,311 Ordinal CatReg 0,027 LivCond 7,344 0,001 Ordinal CatReg 0,034 EDUCF 2,719 0,069 Ordinal CatReg 0,029 EDUCM 1,752 0,159 Ordinal CatReg 0,032

Dependent Variable: Financial.

EDUCF and although this variable is not significant at the 0,05 level, it is significant at the 0,1 level and also has aβ >0.

3.3.3 Multinomial Logit Analysis

After testing every variable individually against both our intended dependent variables, we tried to test them all in one model. Instead of using the Risk Coefficient and the Fi-nancial Coefficient as dependent variables we transformed them into categories in order to use the Multinomial Logit Model. The group of the Risk Coefficient categories was called Risk Profile and the group of the Financial Coefficient categories Risk Profile F. We cal-culated the mean and standard deviation for both variables and classified our respondents in each of those variables into three groups: Risk Averse (below the average minus the standard deviation), Risk Neutral (between the average minus the standard deviation and the average plus the standard deviation) and Risk Seeking (above the average plus the standard deviation) just like described in Weber et al. (2002). A summary of our par-ticipant’s distribution according to these categories can be found in Tables XII and XIII. Due to its construction, this method has the downside of presenting a distribution with the bulk of our participants being located in the Risk Neutral category, different than one would expect in the “real world” (with the majority of people being risk averse).

Rui Silva Risk Profiling and the DOSPERT Scale

Table XII: Participant’s distribution according to their risk profile based on the overall DOSPERT-PT coefficient;

Risk Profile

Category Frequency Percent Risk Averse 21 15,0 Risk Neutral 97 69,3 Risk Seeking 22 15,7

Total 140 100

this multinomial implementation. Regarding Risk Profile we can see that 21 participants (15%) were evaluated as Risk Averse, 97 as Risk Neutral (69,3%) and 22 as Risk Seeking (15,7%). In terms of their financial propensity to engage in risky situations we see that Risk Profile F has 18 participants labeled as Risk Averse (12,86%), 98 as Risk Neutral (70%) and 24 as Risk Seeking (17,14%). Because our dependent variables had more

Table XIII: Participant’s distribution according to their risk profile based on the financial DOSPERT-PT coefficient;

Risk Profile F

Category Frequency Percent Risk Averse 18 12,9 Risk Neutral 98 70,0 Risk Seeking 24 17,1 Total 140 100,0

than two categories each, we had to use the multinomial model. We first started with Risk Profile as dependent variable (with Risk Averse as the reference group) and the demographic characteristics as independent variables. Despite wanting to test all variables simultaneosly, we used the forward entry method that starts with none of the variables in the model and then adds the significant ones by steps.

Table XIV has the Step Summary, where we can see that three variables entered the model using the chi-square test for entry selection based on the likelihood ratio.

Step Summary

Model Action Effect(s) Model Fitting Criteria Effect Selection Tests -2 Log Likelihood Chi-Squarea

df Sig. 0 Entered Intercept 232,290 .

1 Entered AREAF 204,741 27,549 8 ,001 2 Entered LivCond 192,039 12,702 4 ,013 3 Entered GENDER 184,595 7,444 2 ,024

Stepwise Method: Forward Entry.

a. The chi-square for entry is based on the likelihood ratio test.

LivCond and its categories are significant (p-value below the 0,05 level). According to UCLA (2012a) this allows to reach the conclusion that the multinomial logit odds that people have a higher risk profile when comparing Risk Neutral to Risk Averse, increase if your perceived living conditions are higher, on average, ceteris paribus. In the last vari-able entered, GENDER, there seems to be evidence that males, on average, tend to have a higher tendency to engage in risky activities, measured by their risk category according to our classification, in relation to the reference group. This means that, on average when holding the rest of the variables constant, the multinomial logit odds to have a higher risk profile classification (in this case Risk Neutral relative to the reference group Risk Averse) increase when you are male. The second model contained the estimations for Risk Seeking in relation to Risk Averse. The first variable, AREAF, only has one significant category: AREAF4 (Sciences), meaning that the multinomial logit probability of having a higher risk profile than the reference group, on average, increases if the father area of studies is related to sciences. None of LivCond categories are statistically significant in this model. This time Gender categories are statistically significant and the results suggest that, on average, the difference between male and female risk profiles is bigger when we consider the more risk seeking individuals.

Rui Silva Risk Profiling and the DOSPERT Scale

Chapter 4: Conclusions

This study was focused on the DOSPERT scale and Prospect Theory (especially Loss Aversion) and in the search to find evidence of a relation between them.

We started off by translating and validating a Portuguese version of the DOSPERT scale that we named DOSPERT-PT and, after testing it with a sample of students from ISEG, we found out that this version still maintains its validity and internal consistency, visible in similar results to previous applications in alphas and item-total correlations, making it one of the contributions of this study. We also encountered the same patterns found in previous implementations of the scale, like a positive relation between Risk-Taking and Expected-Benefits since the higher the benefits expected from an action, the higher the propensity to engage in said action, or a negative relation between Risk-Taking and Risk-Perception since the riskier someone considers a behavior, the less prone to engage in it they are. To our best knowledge, this is also the first time this scale is used with a Portuguese population and the reported information could be valuable to understand how Portuguese individuals behaved when faced with risky situations.

Finally we turned our attention to the demographic characteristics obtained from our questionnaire and analyzed their impact, both individually and simultaneously. We con-cluded that individually, with Risk Coefficient as the dependent variable, the variables GENDER, AREAF, INCOME, LivCond, EDUCF and EDUCM are statistically signif-icant at the 5% level and the variable AGE is statistically signifsignif-icant at the 10% level meaning that these characteristics have an impact on our risk profile. When the Fi-nancial Coefficient is the dependent variable, the variables GENDER and LivCond are statistically significant at the 5% level, and A Studies and EDUCF are statistically sig-nificant at the 10% level. To test the personal characteristics and their combined impact on our dependent variables, a Multinomial Logit Model was used and, when considering our overall Risk Profile, we found out that three demographic variables had a statistically significant impact (AREAF, LivCond and GENDER). When Risk Profile F is the depen-dent variable, none of our independepen-dent variables showed a significant impact on that result.

Although we are happy with our findings, there are some limitations that need to be addressed. First there is not a definitive way to measure loss aversion, with different authors proposing different definitions and methods to obtain it; second, the sample is limited to individuals with high education in finance/economics might insert some bias in our results. Another limitation was the number of valid responses and the fact that we could only use 36 of our participants when considering loss aversion due to inconsistency rules violated in most cases. That could lead to new lines of investigation such as expand-ing our process to a bigger sample to better counter act the number of dropped responses due to inconsistency, while the same could be achieved including more mixed prospects questions. After comparing the DOSPERT-PT results with loss aversion, it would be interesting to test them against the current risk profile questionnaires and also to try and replicate De Giorgi and Hens (2009) results with the signficant domains from this scale.

Chapter 5: References

Abdellaoui, M., H. Bleichrodt, and C. Paraschiv (2007). Loss aversion under prospect theory: A parameter-free measurement. Management Science 53(10), 1659–1674.

Allais, M. (1953). Le comportement de l’homme rationnel devant le risque: Critique des postulats et axiomes de l’ecole americaine. Econometrica 21(4), 503–546.

Benartzi, S. and R. H. Thaler (1995, February). Myopic loss aversion and the equity premium puzzle. The Quarterly Journal of Economics 110(1), 73–92.

Blais, A.-R. and E. U. Weber (2006). A domain-specific risk-taking (dospert) scale for adult populations. Judgment and Decision Making 1, 33–47.

Bond, S. and S. Satchell (2006). Asymmetry, loss aversion, and forecasting. The Journal of Business 79(4), 1809–1830.

Brislin, R. W. and C. Freimanis (1995). Back-translation: A tool for cross-cultural research. In C. Sin-Wai and D. E. Pollard (Eds.), An Encyclopedia of Translation: Chinese-English, English-Chinese. The Chinese University Press.

Camerer, C. F. (1998). Prospect theory in the wild: Evidence from the field. Working Papers 1037, California Institute of Technology, Division of the Humanities and Social Sciences.

Center for Decision Sciences, C. B. S. (2010). DOSPERT Scale. Available in: http://www.dospert.org/ [Accessed in: 2012.04.20].

Cunha, A. A. (2012). Cumulative prospect theory: A parametric analysis of the functional forms and applications. Master’s thesis, Instituto Superior de Economia e Gest˜ao.

De Coster, J. (2004). Data Analysis in SPSS. Available in: http://www.stat-help.com/spss.pdf [Accessed in: 2012.02.27].

Fiegenbaum, A. and H. Thomas (1988). Attitudes toward risk and the risk-return paradox: Prospect theory explanations. The Academy of Management Journal 31(1), 85–106.

Fox, C. and R. Poldrack (2008). Prospect theory and the brain. In P. Glimcher, E. Fehr, C. Camerer, and R. Poldrack (Eds.), Handbook of Neuroeconomics. San Diego: Aca-demic Press.

Gonzalez, R. and G. Wu (1999). On the shape of the probability weighting function. Cognitive Psychology 38(1), 129 – 166.

Halek, M. and J. Eisenhauer (2001). Demography of risk aversion. The Journal of Risk and Insurance 68, 1–24.

Harless, D. W. and C. F. Camerer (1994). The predictive utility of generalized expected utility theories. Econometrica 62(6), 1251–89.

Johnson, J., A. Wilke, and E. U. Weber (2004). Beyond a trait view of risk taking: A domain-specific scale measuring risk perceptions, expected benefits, and perceived-risk attitudes in german-speaking populations. Polish Psychological Bulletin 35, 153–172.

Kachelmeier, S. and M. Shehata (1992). Examining risk preferences under high monetary incentives: Experimental evidence from the people’s republic of china. The American Economic Review 82, N5, 1120–1141.

Kahneman, D., J. L. Knetsch, and R. H. Thaler (1990). Experimental tests of the endow-ment effect and the coase theorem. Journal of Political Economy 98(6), 1325–48.

Kahneman, D. and A. Tversky (1979). Prospect theory: Analysis of decision under risk. Econometrica 47, n2, 263–292.

Kahneman, D. and A. Tversky (1984). Choices, values and frames. American Psycholo-gist 39, 341–350.

Kontek, K. (2011). What is the actual shape of perception utility?

Levy, H., E. D. Giorgi, and T. Hens (2003). Prospect theory and the capm: A contradiction or coexistence? IEW - Working Papers iewwp157, Institute for Empirical Research in Economics - University of Zurich.

Levy, H. and M. Levy (2004). Prospect theory and mean-variance analysis. Review of Financial Studies 17(4), 1015–1041.

Rui Silva Risk Profiling and the DOSPERT Scale

March, J. and Z. Shapira (1987). Managerial perspectives on risk and risk taking. Man-agement Science 33, N11, 1404–1418.

Markowitz, H. (1952). The utility of wealth. Journal of Political Economy 60, 151.

Moss, S. (2008). Categorical Regression Analysis. Available in: http://www.psych-it.com.au/Psychlopedia/article.asp?id=160 [Accessed in: 2012.04.12].

Nunnally, J. C. and I. H. Bernstein (1994). Psychometric theory (3 ed.). McGraw-Hill.

Pahor, M. (2011). PCA and Factor Analysis. Available in: http://miha.ef.uni-lj.si/ dokumenti3plus2/193004/IMB 2011 Seminar6 PCA FA.pdf [Access date: 2012.02.26].

Rabin, M. (2000). Risk aversion and expected-utility theory: A calibration theorem. Econometrica 68(5), 1281–1292.

Ritter, J. (2003). Behavioral finance. Pacific-Basin Finance Journal 11, n4, 429–437.

Schubert, R., M. Gysler, M. Brown, and H.-W. Brachinger (2000). Gender specific at-titudes towards risk and ambiguity: An experimental investigation. Technical report, Center for Economic Research (SFIT).

Thaler, R. (1980). Toward a positive theory of consumer choice. Journal of Economic Behavior & Organization 1(1), 39–60.

Tversky, A. and D. Kahneman (1986). Rational choice and the framing of decisions. The Journal of Business 59(4), S251–78.

Tversky, A. and D. Kahneman (1991). Loss aversion in riskless choice: A reference-dependent model. The Quarterly Journal of Economics 106(4), 1039–61.

Tversky, A. and D. Kahneman (1992). Advances in prospect theory: Cumulative repre-sentation of uncertainty. Journal of Risk and Uncertainty 5, 297–323.

UCLA, A. T. S. (2012a).Annotated SPSS Output Multinomial Logit Regression. Available in: http://www.ats.ucla.edu/stat/spss/output/mlogit.htm [Accessed in: 2012.04.16].

UCLA, A. T. S. (2012b). Regression with SPSS: Chap-ter 3 - Regression with Categorical Predictors. Available in: http://www.ats.ucla.edu/stat/spss/webbooks/reg/chapter3/spssreg3.htm [Accessed in: 2012.04.02].

http://www.ats.ucla.edu/stat/mult pkg/whatstat/nominal ordinal interval.htm [Ac-cessed in: 2012.04.12].

von Neumann, J. and O. Morgenstern (1947). Theory of Games and Economic Behavior (2 ed.). Princeton University Press.

Wang, H. and S. Hanna (1997). Does risk tolerance decrease with age? Financial Coun-seling and Planning 8.

Appendix A:

Portuguese translated Risk-Taking sub-scale:

• Para cada uma das seguintes afirma¸c˜oes, indique a probabilidade de realizar a atividade ou comportamento descritos, caso se encontrasse na situa¸c˜ao relatada. Classifique cada afirma¸c˜ao desde “Extremamente Improv´avel” at´e “Extremamente Prov´avel”.

Portuguese translated Expected-Benefits sub-scale:

• Para cada uma das seguintes afirma¸c˜oes, indique por favor, os benef´ıcios que espera obter em cada situa¸c˜ao, desde “Nenhum Benef´ıcio” at´e “Benef´ıcio Extremo”.

Portuguese translated Risk-Perception sub-scale:

• Frequentemente vemos risco em situa¸c˜oes em que existe incerteza sobre qual o seu desfecho e em que existe a possibilidade de ocorrerem consequˆencias negativas. No entanto, esse risco ´e uma medida muito pessoal e intuitiva e por isso estamos in-teressados em determinar a forma instintiva como avalia cada situa¸c˜ao. Para cada uma das seguintes frases indique por favor, qu˜ao arriscada considera a situa¸c˜ao ou comportamento descritos. Avalie desde “Nada Arriscado” at´e “Extremamente Ar-riscado”.

DOSPERT-PT scale items (with the respective domain in brackets):

1. Admitir que os seus gostos s˜ao diferentes dos de um amigo. (S)

2. Acampar num meio selvagem. (R)

3. Apostar o rendimento de um dia de trabalho em corridas de cavalos. (F)

4. Investir 10% do seu rendimento anual num fundo de crescimento moderado. (F)

5. Ingerir uma quantidade exagerada de ´alcool durante um evento social. (H/S)

6. Efetuar dedu¸c˜oes discut´ıveis no preenchimento da declara¸c˜ao de IRS. (E)

8. Apostar o rendimento de um dia de trabalho num jogo de poker de apostas elevadas. (F)

9. Ter um caso com um(a) homem/mulher casado(a). (E)

10. Apresentar trabalho de outrem como sendo seu. (E)

11. Descer uma pista de esqui, cujo grau de dificuldade est´a acima das suas capacidades. (R)

12. Investir 5% do seu rendimento anual numa a¸c˜ao muito especulativa. (F)

13. Fazer rafting em ´aguas bravas durante a primavera. (R)

14. Apostar o rendimento de um dia de trabalho no resultado de um evento desportivo. (F)

15. Fazer sexo sem prote¸c˜ao. (H/S)

16. Revelar o segredo de um amigo(a) a outra pessoa. (E)

17. Conduzir um carro sem pˆor o cinto de seguran¸ca. (H/S)

18. Investir 10% do seu rendimento anual numa nova oportunidade de neg´ocio. (F)

19. Ter uma aula de paraquedismo. (R)

20. Andar de mota sem capacete. (H/S)

21. Escolher uma carreira que realmente goste em vez de uma carreira mais segura. (S)

22. Emitir a sua opini˜ao sobre um tema controverso numa reuni˜ao no trabalho. (S)

23. Tomar banhos de sol sem protetor solar. (H/S)

24. Fazer “bungee jumping” a partir de uma ponte alta. (R)

25. Pilotar um avi˜ao de pequenas dimens˜oes. (R)

26. Regressar a casa sozinho(a) a p´e durante a noite por uma zona insegura da cidade. (H/S)

27. Mudar-se para uma cidade longe do seu n´ucleo familiar. (S)

28. Come¸car uma carreira nova ap´os os trinta anos. (S)

29. Deixar as suas crian¸cas sozinhas em casa enquanto vai tratar de um assunto/recado. (E)

Appendix B:

Table I: Risk-Taking sub-scale mean and standard deviation results by gender in each domain; sub-scale alpha by gender;

Risk Taking Sub-Scale

Domain Males Females Overall Mean (StDev) Mean (StDev) Mean (StDev) Social 5,274 (0,758) 5,005 (0,612) 5,123 (0,689) Recreational 4,215 (1,499) 3,419 (1,103) 3,767 (1,344) Financial 3,577 (0,884) 2,963 (0,725) 3,231 (0,851) Ethical 2,941 (0,893) 2,331 (0,717) 2,597 (0,851) Health/Safety 3,896 (1,206) 2,859 (0,832) 3,312 (1,131)

Table I: Expected-Benefits sub-scale mean and standard deviation results by gender in each domain; sub-scale alpha by gender;

Expected Benefits Sub-Scale

Domain Males Females Overall Mean (StDev) Mean (StDev) Mean (StDev) Social 4,404 (0,936) 4,408* (0,840) 4,406 (0,879) Recreational 3,726 (1,552) 3,023 (1,260) 3,330 (1,431) Financial 3,663 (1,335) 2,876 (0,946) 3,220 (1,193) Ethical 2,541 (1,106) 1,989 (0,601) 2,229 (0,897) Health/Safety 2,085 (0,835) 1,506 (0,547) 1,759 (0,742)

Appendix D:

Table I: Risk-Perception sub-scale mean and standard deviation results by gender in each domain; sub-scale alpha by gender;

Risk Perception Sub-Scale

Domain Males Females Overall Mean (StDev) Mean (StDev) Mean (StDev) Social 3,567 (0,909) 3,655* (0,794) 3,617 (0,843) Recreational 4,651 (0,968) 5,014* (0,866) 4,856 (0,925) Financial 5,167 (0,916) 5,379* (0,582) 5,286 (0,749) Ethical 4,863 (0,732) 5,287 (0,753) 5,102 (0,769) Health/Safety 5,374 (0,909) 6,063 (0,691) 5,762 (0,861)

Table I: Estimated parameters for the Multinomial Logit Models with Risk Profile as the dependent variable and the significant characteristics as independent variables;

Parameter Estimates

Risk Profilea

β Std. Error Wald df Sig.

Risk Neutral

Intercept 19,586 ,792 612,198 1 ,000 [Gender=0] -,625 ,528 1,403 1 ,236 [Gender=1] 0b

. . 0 .

[LivCond=1] -19,076 1,216 246,287 1 ,000 [LivCond=2] -17,903 ,660 735,864 1 ,000 [LivCond=3] 0b

. . 0 .

[AREAF=1] -,552 ,592 ,871 1 ,351 [AREAF=2] 18,418 10919,444 ,000 1 ,999 [AREAF=3] 18,455 5965,385 ,000 1 ,998 [AREAF=4] 1,514 1,159 1,707 1 ,191 [AREAF=5] 0b

. . 0 .

Risk Seeking

Intercept 18,678 ,633 871,335 1 ,000 [Gender=0] -1,912 ,753 6,448 1 ,011 [Gender=1] 0b

. . 0 .

[LivCond=1] -38,493 6324,058 ,000 1 ,995 [LivCond=2] -19,029 ,000 . 1 . [LivCond=3] 0b

. . 0 .

[AREAF=1] ,904 ,861 1,104 1 ,293 [AREAF=2] 19,893 10919,444 ,000 1 ,999 [AREAF=3] ,504 8221,459 ,000 1 1,000 [AREAF=4] 3,497 1,292 7,331 1 ,007 [AREAF=5] 0b

. . 0 .

a. The reference category is: Risk Averse.