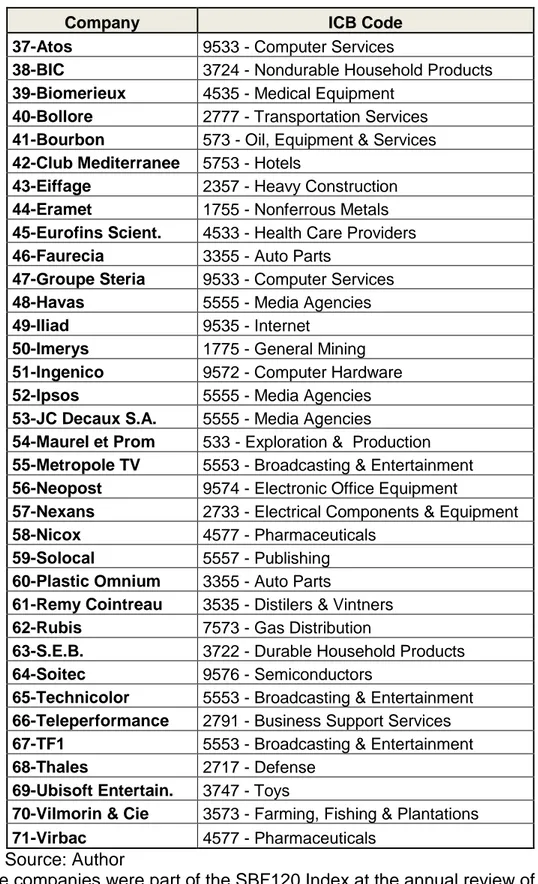

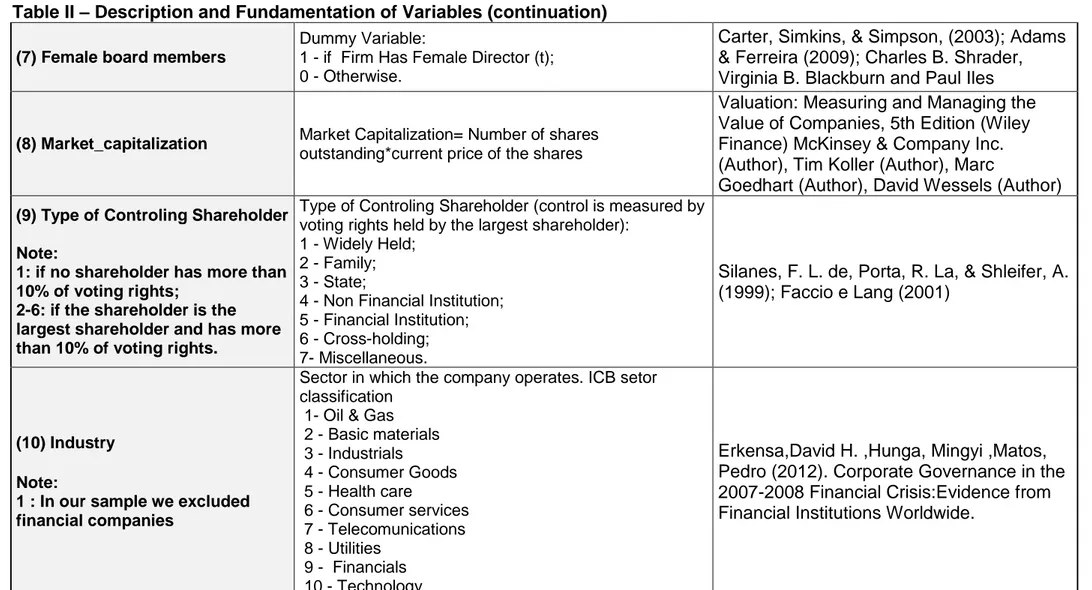

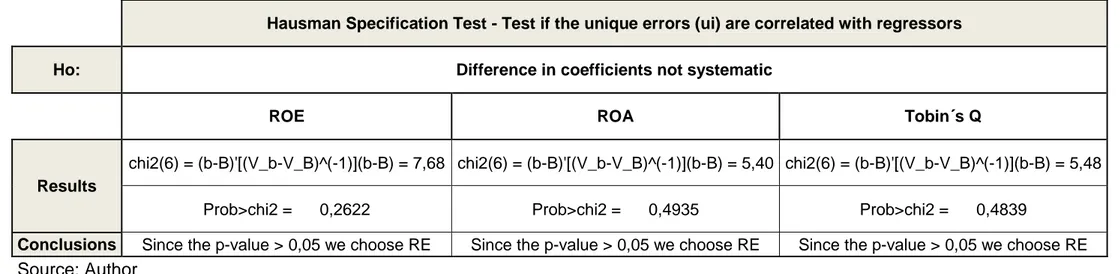

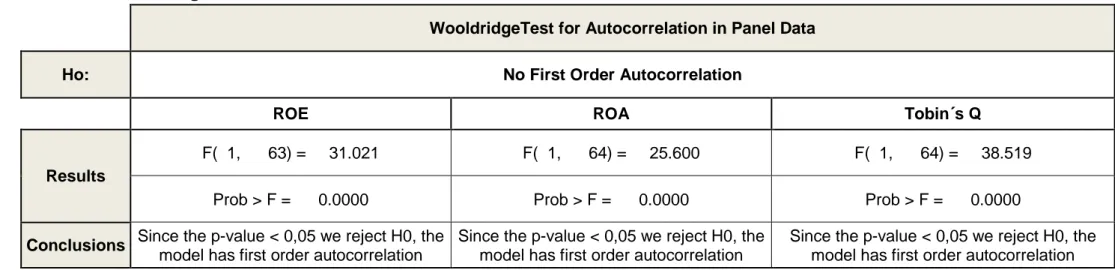

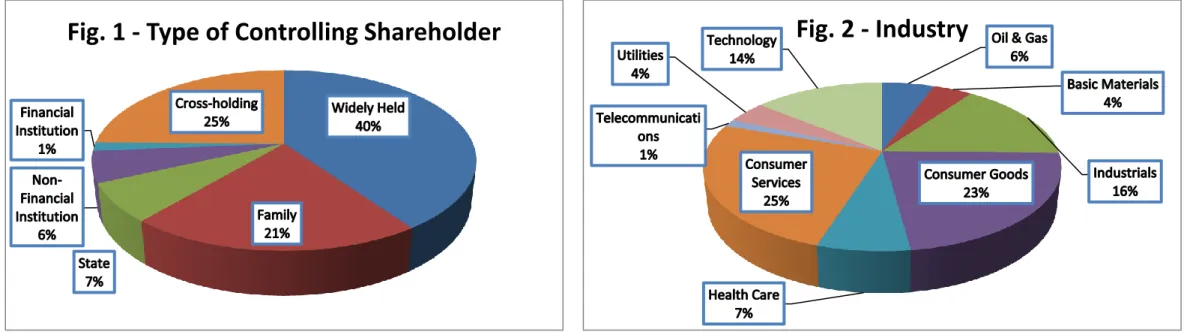

Corporate governance and performance measures : the French case

Texto

Imagem

Documentos relacionados

[...].usamos a expressão gênero textual como uma noção propositalmente vaga para referir os textos materializados que encontramos em nossa vida diária e que apresentam

Os tempos médios de segregação do alvo entre as situações de cores sólidas e do Mosaico 1 não diferiram significativamente, indicando que os

Ousasse apontar algumas hipóteses para a solução desse problema público a partir do exposto dos autores usados como base para fundamentação teórica, da análise dos dados

Quanto ao caráter político das esterilizações, evidenciamos algumas indicações da conexão eleição-ligação de trompa. Consideran- do todas as laqueaduras do período 1986-1995,

The probability of attending school four our group of interest in this region increased by 6.5 percentage points after the expansion of the Bolsa Família program in 2007 and

In Chapter 2 we derive the minimum hop count probability distribution in one- dimensional networks, assuming that the location of the source and destination nodes are known and

1.1.1 - Objetivos O objetivo geral desta pesquisa é determinar os efeitos das combinações função-custo / algoritmo-de-busca no erro de classificação do sistema de controle

In the analyses performed, a negative relationship between the cost of non-audit services and corporate governance was found, i.e., good governance practices tend