Cross-

Border

Mergers

&

Acqu

is

it

ions

:

Does

Labour

Matter?

Pedro

Forsyth

Bastos

e

S

i

lva

152415027

D

issertat

ion

wr

itten

under

the

superv

is

ion

o

f

Pramuan

Bunkanwan

icha

D

issertat

ion

subm

itted

in

part

ia

l

fu

l

f

i

lment

o

f

the

requ

irements

for

the

Internat

iona

l

MSc

in

F

inance

at

the

Un

ivers

idade

Cató

l

ica

Portuguesa,

and

for

the

MSc

in

Management

Grande

Éco

le

at

ESCP

Europe

Par

is

{page intentionally left blank}

Cross-Border Mergers & Acquisitions: Does Labour Matter?

Pedro Forsyth Bastos e Silva

June, 2017 Supervisor: Pramuan Bunkanwanicha Abstract We implement a 2-state Market Model using a first-order Markov Switching Process to study the generation of abnormal returns in a cross-border M&A setting. We find that emerging market acquirers earn a positive and statistically significant abnormal return of 1,16% when achieving control of frontier market targets, and developed market acquirers earn a positive and statistically significant abnormal return of 1,06% when achieving control of emerging market targets. Furthermore, we propose that labour laws play a significant role in generating abnormal returns in a cross-border M&A setting. When control is acquired, we find that social security law differences between countries are associated with higher abnormal returns in a developed market – emerging market setting, and labour law differences are associated with higher abnormal returns in an emerging market – emerging market setting. We argue that these results reflect efficiency improvements at the level of social security cost reduction and faster employment adjustments to cyclical industries, and effectiveness improvements at the level of the productive output of labour forces, given the managerial expertise of the top management of acquiring firms. Keywords: Cross-Border Mergers and Acquisitions, Emerging Markets, Frontier Markets, Event Studies, Markov Switching Process, Labour Laws

{page intentionally left blank}

Fusões e Aquisições Internacionais: O Contexto Laboral

Importa?

Pedro Forsyth Bastos e Silva Junho, 2017 Supervisor: Pramuan Bunkanwanicha Resumo Este estudo consiste na implementação de um modelo de mercado com recurso a um processo de mudanças de estado de Markov de primeira ordem, com o intuito de estudar a geração de retornos anormais num contexto de fusões e aquisições internacionais. Quando a empresa adquirente se encontra sediada num mercado emergente e a empresa adquirida num mercado de fronteira, verificamos que os acionistas da empresa adquirente ganham um retorno estatisticamente significativo de 1,16% quando adquirem controlo. Quando a empresa adquirente se encontra sediada num mercado desenvolvido e a adquirida num mercado emergente, os acionistas da empresa adquirente ganham um retorno estatisticamente significativo de 1,06% quando adquirem controlo. Nesse contexto, propomos que as leis laborais desempenham um papel fundamental na geração de retornos anormais em fusões e aquisições internacionais. Quando empresas sediadas em mercados desenvolvidos adquirem controlo de empresas sediadas em mercados emergentes, verificamos que diferenças a nível de leis da segurança social estão associadas a retornos anormais mais elevados. Verificamos do mesmo modo que quando empresas sediadas em mercados emergentes adquirem controlo de empresas sediadas em mercados emergentes, as diferenças a nível de leis de contratação estão associadas a retornos anormais mais elevados. Sugerimos que os resultados deste estudo refletem melhoramentos de eficiência ao nível da redução de custos derivados da segurança social e uma maior capacidade de adaptação do nível de contratação a industrias cíclicas, e melhoramentos de eficácia ao nível da produtividade do fator laboral.

Palavras Chave: Fusões e Aquisições Internacionais, Mercados Emergentes, Mercados de Fronteira, Estudo de Eventos, Processo de Mudança de Estado de Markov, Leis Laborais

{page intentionally left blank}

Fusions et Acquisitions Transfrontalières : Le Travail est-il

Importante ?

Pedro Forsyth Bastos e Silva Juin, 2017 Superviseur : Pramuan Bunkanwanicha

Résumé

Cette étude consiste dans l’implantation d’un modèle de marché par le biais du modèle de Markov à changement, dans le but d’étudier la génération de retours anormaux dans un contexte de fusions et acquisitions internationales. Nos recherches trouvent que, lorsque l’entreprise acheteuse se trouve dans un marché émergent et l’entreprise achetée dans un marché frontière, les actionnaires de l’entreprise acheteuse ont un retour anormal, statistiquement significatif, de 1,16%. Lorsque l’entreprise acheteuse est siégée dans un marché développé et l’entreprise achetée dans un marché émergent, les actionnaires de l’entreprise acheteuse ont un retour anormal, statistiquement significatif, de 1,06%. De plus, une fois le contrôle de l’entreprise acheteuse sur l’achetée établi, les lois du travail semblent jouer un rôle fondamental dans la génération de retours anormaux en fusions et acquisitions internationales. Lorsque les entreprises siégées dans les marchés développés acquièrent contrôle sur les entreprises siégées dans les marchés émergents, nous pouvons vérifier que les différences liées aux lois de sécurité sociale sont associées à des retours anormaux plus élevés. De même, lorsque les entreprises siégées dans les marchés émergents acquièrent contrôle sur d’autres entreprises siégées dans les marchés émergents, les lois du travail sont associées à des retours anormaux plus élevés. Finalement, on argumente le fait que ces résultats reflètent l’amélioration efficace des niveaux de réduction de coûts de sécurité sociale ainsi que le développement efficace au niveau de productivité des industries cycliques, et les améliorations effectives aux niveaux de productivité des forces de travail. Mots Clés : Fusions et Acquisitions Transfrontalières, Marchés Émergents, Marchés Frontalières, Étude d'événement, Processus de Commutation Markov, Droit du Travail

{page intentionally left blank}

ACKNOWLEDGEMENTS Over the course of the last five years, I was remarkably fortunate for being given the opportunity to meet incredible people, visit incredible places, and learn incredible things. One page would never be enough to give credit to all of those who, in their own special way, have taught me so many priceless lessons throughout this time, whether it be at a personal, professional or academic level. I would like to start by thanking my dear friends at the Maison du Portugal, who have witnessed first-hand the enormous challenge it is to deal with me when I am trying to write a thesis. They deserve all the recognition in the world for the patience, kind words of support, and love given throughout these intense months. To my fellow Empirical Finance group mates, and to professor José Faias, I owe an enormous debt of gratitude for all I have learned with them. Those were without doubt some of the busiest months of our academic lives, but also some of the most fruitful. This work would not be possible without them. To my CFA grupistas, I also owe a debt of gratitude, for the lessons on group work, cohesion, and dedication, which took us all the way to Chicago. Finally, I would like to dedicate this work to the three most important people in my life. Regardless of my successes and failures throughout these years, I cannot remember a time when you were not there for me. To my mother, who displayed infinite amounts of patience and dedication. To my little brother, who I truly admire for his courage to do what he loves. And especially to my father, who taught me that with hard work anything is possible. It does not take luck to be successful. But it does take luck to have such an incredible family. Thank you.

{page intentionally left blank}

TABLE OF CONTENTS I – INTRODUCTION ... 1 II – LITERATURE REVIEW ... 6 II.I – Mergers & Acquisitions in Waves ... 6 II.II – Stock and Cash ... 8 II.III – Private Benefits of Control ... 9 II.IV – Transaction Costs ... 10 II.V – Opportunistic Behaviour and Quasi Rents ... 11 II.VI – Ownership and Control ... 11 II.VII – Relationship and Arm’s Length Systems ... 12 II.VIII – Fundamentals of Law ... 13 II.IX – Investor Protection Laws and Enforceability ... 14 II.X – Labour Laws ... 16 II.XI – Theory of Institutional Choice ... 18 II.XII – Electoral Systems ... 19 II.XIII – Strictness of Regulations and Rigid Labour Markets ... 20 III – ECONOMETRIC SCOPE & HYPOTHESIS ... 21 III.I – Event Study Methodology ... 21 III.II – Market Model ... 23 III.III – GARCH Model ... 25 III.IV – 2-State Market Model ... 26 III.V – Over Estimation of Standard Errors ... 27 III.VI – Smooth Transition Autoregressive Model ... 29 III.VII – Hypothesis Formulation ... 30

{page intentionally left blank}

IV – DATA & METHODOLOGY ... 33 IV.I – Data Gathering and Limitations ... 33 IV.II – Calculation of Cumulative Abnormal Returns ... 45 IV.III – Econometric Methodology ... 46 V – EMPIRICAL RESULTS ... 48 V.I – Cross-Border Abnormal Returns ... 48 V.II – The Value of Control in Emerging and Frontier Markets ... 51 V.III – Labour Laws ... 61 V.IV – Robustness Checks ... 66 VI - CONCLUSIONS ... 72 VI.I – Winners in M&A Deals & Value of Control ... 72 VI.II – Labour Laws ... 73 VI.III – Study Limitations ... 76 VI.IV – Future Research ... 76 VII – BIBLIOGRAPHY ... 78

{page intentionally left blank}

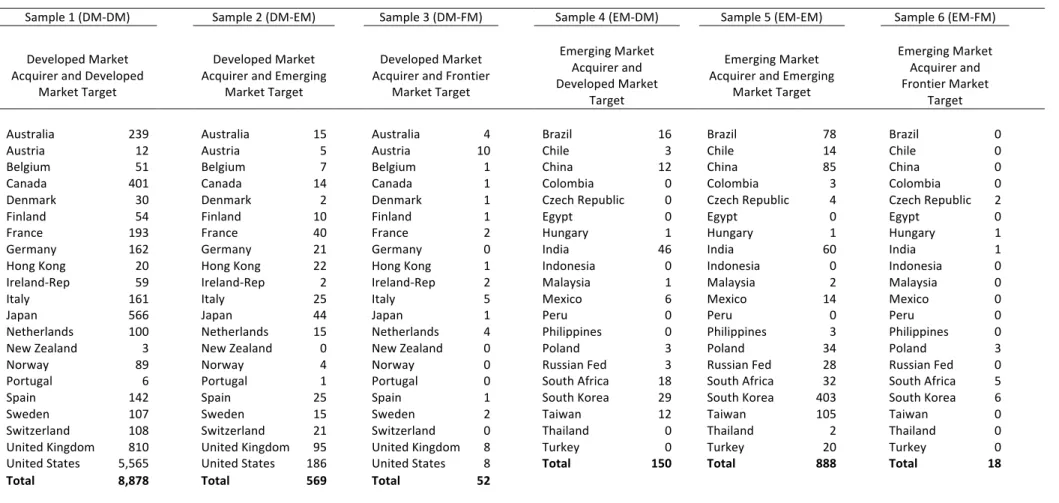

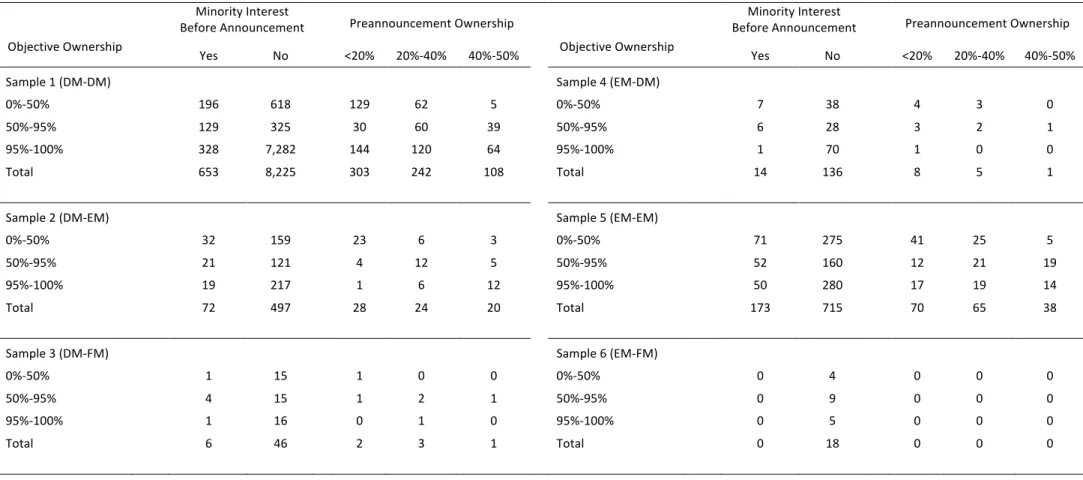

LIST OF TABLES Table 1 – Number of Transactions in each Nation...37 Table 2 – Summary Statistics of Deals, Target, and Acquiring Firms...40 Table 3 – Pre and Post Announcement Ownership Structure...42 Table 4 – Cumulative Abnormal Returns...49 Table 5 – Summary Statistics of Cumulative Abnormal Returns...52 Table 6 –Regression of CAR’s on Control and Frontier & Emerging Markets...56 Table 7 –Regression of CAR’s on Labour Laws...62 Table 8 – Robustness Checks on Control...67 Table 9 – Robustness Checks on Labour Laws...70

{page intentionally left blank}

I - INTRODUCTION

Mergers and Acquisitions is one of the most studied and puzzling topics in the financial literature. It is a relevant subject to understand the behaviour and motivations of all stakeholders of a firm. These include law makers, investors, customers, workers, regulators, suppliers, competitors, creditors, and trade unions. Moreover, it gives top management an essential tool to accomplish many of their strategic goals. The decision to engage in M&A deals has a detrimental impact on the performance of all firms involved. As a direct consequence, it also has a direct and material impact on the wealth of the shareholders, the subsistence of the workers that depend on their jobs, the competitive forces and landscape that define the markets involved, the value generated for customers, the bargaining power of suppliers, the relevance and influence of trade unions, and the value generated for all remaining stakeholders that depend indirectly on those firms. The complexity of each of these impacts becomes exponentially larger when considering cross-border deals. Therefore, understanding the underlying reasons that lead managers to decide upon engaging in mergers and acquisitions is paramount. Two fundamental questions of a practical nature typically arise: who wins with Mergers & Acquisitions, and what are the sources of value?

To understand who wins with M&A deals, empirical research is typically focused on the event study methodology developed by Fama, et al. (1969). For example, consider the findings of Gregor, Mitchell and Strafford (2001 ). The authors show that M&A deals tend to create value for shareholders. In particular, between 1973 and 1998, the average 3-day window abnormal return for acquirer and target firms combined involved in M&A deals ranged between 1.4% and 2.6%. Furthermore, the authors show that target firms seem to be the clear winners with an average abnormal return of 16% in a three-day event window, which increases to over 24% with a longer-range window. This is the equivalent return an average shareholder would yield over a 16-month period if he invested in a weighted portfolio of US stocks during the same historical period. On the other hand, acquiring shareholders do not seem to capture the same level of value. The authors find that the three-day

abnormal return for the acquiring shareholders is statistically indistinguishable from 0% over a short period event window. These results are puzzling, and therefore generate further questions. First, it is relevant to understand if all types of acquirers and targets experience the same level of abnormal returns. Second, one should consider if the event study methodology implemented is adequate to measure abnormal returns. To answer the first question, the literature is relatively comprehensive. Consider as an example the findings of Chari, Ouimet and Tesar (2010). The authors find that when firms from developed markets acquire a majority stake in firms from emerging markets, there is a statistically significant positive abnormal return of 1.16% for the acquiring firm shareholders. On the other hand, when the same acquirers from developed markets acquire firms from developed markets, abnormal returns are undistinguishable from 0%.

To answer the question regarding the measurement of abnormal returns, the literature is not so comprehensive. Specifically, research is typically based on the framework proposed by Fama, et al. (1969). Although the methodology to test the significance of abnormal returns has been enhanced multiple times, less attention has been given to the estimation period. One of the most important considerations is the potential for contamination of the estimation period from unrelated events. Recently however, more attention has been given to this issue. Consider the work of Aktas, Bodta and Cousin (2007). The authors propose a 2-state Market model based on a Markov Switching Process. The authors show that this alternative provides superior performance, both in terms of specification and in terms of power, when compared to the classic market model.

Finally, understanding the sources of value generated by M&A deals is arguably one of the most relevant questions empirical research can answer from a practical standpoint. The literature is again comprehensive in this regard. In particular, research has focused on both valid and dubious reasons that motivate top management to engage in M&A deals. Valid potential reasons include restructuring

benefits, increased market power from reduced competition, synergies, economies of scale, economies of scope, corporate tax economies, improved management, and the purchase of undervalued assets. Dubious reasons include lowering financial costs, risk reduction derived from diversification, increasing earnings per share, and empire building. In the context of cross-border Mergers & Acquisitions, Chari, Ouimet and Tesar (2010) have tackled some of these questions. In particular, the authors argue that the value generation originated from the acquisition of emerging market targets could stem from improved corporate governance. The authors argue further that this is likely to be an even more critical factor in an intangible asset production context. Corporate governance practices are largely driven by legal and institutional features, and often have a significant impact on the potential for cash flow generation. This is especially critical in emerging economies: by bringing the acquiring nation firm’s governance capabilities to an emerging market, the potential for incomplete contracting is reduced. Asset intangibility is also an important source of value generation in cross-border M&A deals. In particular, Brynjolfsson and Hitt (2003) argue that the potential return on capital invested in computer power is more than 24 times greater than the returns of common PPE investments, and Haussman and Sturzenegger (2006) argue that a considerable portion of the missing value of the book value estimate of foreign assets in emerging markets which are acquired by developed market firms is precisely derived from intangible assets. Clearly, the two critical topics of the findings of Chari, Ouimet and Tesar (2010) are the role that the legal environment and contract enforceability play in the value generation process of acquiring firms. Finally, Chari, Ouimet and Tesar (2010) also find that acquiring a majority stake in the target firm is a critical factor to generate positive abnormal returns for the acquiring firm. Although the authors consider the hypothesis that value generation stems from the identification of undervalued assets in emerging markets, they argue that if that was the source of value, then investors with no corporate control should also realise positive abnormal returns. This seems not to be the case.

The findings of Chari, Ouimet and Tesar (2010) prompt a third question of important practical application. Within the context of the legal environment of different

countries, what specifically leads acquiring firms to realise positive gains? For example, Rossi and Volpin (2004) study the determinants of M&A with an emphasis on law differentials. The authors find that M&A activity is significantly higher in economies with good accounting standards and strong shareholder protection. The authors also find that in cross-border deals, the target firm typically originates from a market with weaker investor protection legislation, which suggests that cross-border deals also play a governance role. This is consistent with the argument of Chari, Ouimet and Tesar (2010).

The M&A literature is vast. The significance of empirical research for practical applications is considerable. Specifically, top management and law makers have a clear interest regarding the sources of value creation in M&A deals. Not only do the decisions to engage in these deals have important economic impacts, in particular for the customers and managers of the firms involved, but it also has a very real and significant impact on the job creation and destruction of the firms involved. Even more dramatic, the liberalization of cross-border M&A deals is likely to have a material impact on the expected rights of workers who rely on their jobs for their subsistence, since firms from certain markets can potentially be influenced by the legal and corporate governance practices of international acquirers. In that context, this work is a small attempt to make a contribution to the literature of M&A, with an emphasis on the role that the legal environment has on the value creation process. In particular, we focus on three different dimensions. First, we make a considerable augmentation to the sample used by Chari, Ouimet and Tesar (2010). To that end, we consider not only countries from developed and emerging markets, but also from frontier markets. We also increase and update the time-span of the sample from between 1991 and 2003, to between 1994 and 2013. Second, we implement a 2-state market model based on a Markov Switching process to measure abnormal returns and compare these results with a simple market model approach. In particular, Aktas, Bodta and Cousin (2007) show that a 2-state market model provides superior estimation results both in terms of power and specification. Finally, building on the findings of Chari, Ouimet and Tesar (2010) regarding the relevance

of improved corporate governance and contract enforceability in intangible asset intensive industries, we propose a more specific source of value in cross-border M&A. In particular, we explore the role that labour laws have in the context of value generation. If it is true that Asset Intangible intensive industries mean that contract enforceability is important to generate value for firms, then labour intensive industries can also potentially yield abnormal returns in settings where labour laws are more favourable for profit generation and flexible adjustments. Specifically, Coase (1937) argues in his flagship work that a firm is nothing more than a collection of contracts. In that sense, the potential for contract enforceability, and therefore law enforceability, should have a direct link with the potential for abnormal return generation. But simultaneously, and critical to this work, the potential for contract adjustments should also prove critical to the value generation of firms in the form of efficiency improvements to the various productive forces of a company.

The remainder of this work is organized as follows: Part II reviews the literature concerning Mergers & Acquisitions and the International Corporate Legal Environment; Part III details the scope of this work, with a particular emphasis on the research question addressed and the various econometric methodologies employable in the measurement of abnormal returns; Part IV provides specific details regarding the data usage and treatment, as well as the econometric methodology employed; Part V presents the empirical results and a detailed interpretation; Part VI presents the concluding remarks.

II – LITERATURE REVIEW

This section provides a brief overview of the literature concerning Mergers & Acquisitions and the international contracting and legal environment of different countries. Regarding Mergers and Acquisitions, our goal is dual. First, we provide some historical context about the industry trends. Second, we provide an overview of important empirical studies both in the context of sources of value creation in M&A deals, and in the context of already known stylized facts. In what concerns the international contracting and legal environment, the literature is extremely broad and often not even indirectly relevant for this work. Therefore, it is not our goal to provide an exhaustive overview of the topic. Instead, we focus on the contracting and legal environment with a focus on labour laws. II.I – Mergers & Acquisitions in Waves The study of M&A deals over the past century has revealed two important facts: M&A occurs in waves, and deals tend to cluster by industry (Gregor, Mitchell and Strafford 2001 ). We briefly present a historical overview of the defining characteristics of each wave.

The first wave occurred between 1893 and 1904 and was marked by horizontal mergers. This resulted in the emergence of large conglomerates and monopolies which targeted economies of scale. This period coincides with the rise of manufacturing and transportation giants in the US such as the Standard Oil Company and the United States Steel Corporation. The second wave lasted from 1915 through to 1929. The literature suggests that the second wave of Mergers & Acquisitions was triggered by governmental intervention to reduce anticompetitive clustering and monopolistic behaviour. As a result of this intervention, large firms adjusted and began engaging in vertical integration acquisitions, which resulted in the surfacing of Oligopolies. Oil companies such as The Standard Oil Company expanded their activity to include retail and marketing

activities. The manufacturing industry led the second wave of M&A in terms of deal volume. The third wave spanned from 1955 to 1970 and was driven mainly by diversification attempts. This wave resulted in the creation of large conglomerates, since companies were looking at ways to diversify their income stream. The reasoning of this was to create internal capital markets. The fourth wave started in 1974 and lasted until 1989. This period is marked by a rise in hostile takeovers, with over 14% of deals being considered as aggressive (Gregor, Mitchell and Strafford 2001 ). In particular, corporate raiders were often aided by investment bankers who provided large amounts of cash and financing to support their client’s takeover bids. The stock market crash of 1987 was the first signal that easy access to credit was leading to unsustainable capital structures, and ultimately ended the fourth wave. The fifth wave started in 1993 and lasted until the turn of the new millennium in 2000. M&A deals in this period were to a large extent driven by the dotcom bubble. The fifth wave is also marked by a reduction in hostile takeover attempts, with only 4% of deals being aggressive, an average of just one bidder, and only 1.2 rounds of bidding on average (Gregor, Mitchell and Strafford 2001 ). During this period, large conglomerates were formed once again, and cross-border M&A began sprawling considerably. The opening of borders facilitated the potential for Foreign Direct Investment and opened the doors for multinational corporations to expand their overseas reach. During this period, oil companies such as Exxon Mobil, and pharmaceutical and automobile companies also engaged in large deals.

The sixth wave lasted from 2003 to 2008, and was driven by an increase in Private Equity activity. This was in turn driven by globalization efforts and facilitated access to capital. The sixth wave also saw an increase in the usage of Leveraged Buy-Outs. Globalization however was the main propeller of this wave, which heavily contributed to cross-border deals. In particular, firms have focused on expending

their global reach. The sixth wave ended during the onset of the global financial crisis of 2008. The seventh and current wave of M&A started in 2011. It is being driven by cross border deals originated from emerging economies such as Brazil, Russia, India, South Korea, China, and South Africa.

We make a final comment regarding industry clustering. Although M&A activity tends to come in waves, each one tends to be different in terms of its industry composition. This suggests that a significant portion of the M&A activity is generated from industry-level shocks (Gregor, Mitchell and Strafford 2001 ). Some of these include technological innovations, supply shocks, and most importantly, deregulation. In particular, the latter creates substantial investment opportunities in specific industries, and potentially countries, as it removes barriers that would otherwise keep those industries artificially disperse. II.II – Stock and Cash Managers typically finance M&A deals with cash, equity or a combination of both. The decision of to pay in either way produces a significant impact on the performance of the shares of both the acquiring and target firms. In particular, this decision is viewed by financial markets as a signal of the views of top management regarding the future performance of the firms involved in the deal. There is a large body of literature concerned with the choice of financing methods in M&A transactions. For example, Gregor, Mitchell and Strafford (2001) show that during the 1990’s, over 70% of deals involved stock compensation, and 58% were exclusively financed with stock. The authors note the simultaneous drastic reduction in hostile takeovers. Myers and Majluf (1984) argue that deals financed with stock offerings seem to have fundamentally different value effects when compared to cash only offers. In effect, the authors suggest that stock offers represent a simultaneous equity issue and a merger.

The literature suggests that managers have more information about their firms than the broader market. This is consistent with the semi strong form of the market efficiency hypothesis. Specifically, the hypothesis states that insider information is not incorporated in the share price. As a consequence, if managers issue equity to finance an acquisition, this is viewed as a signal that the share price is overvalued. As a consequence, efficient markets will bid to lower the share price of such a firm (Myers and Majluf 1984). II.III – Private Benefits of Control The findings of Chari, Ouimet and Tesar (2010) are based on the important principle that control is acquired. The authors suggest that positive abnormal returns can be originated either from better corporate governance practices or by improved contract enforceability. However, the authors find that abnormal returns are only significant if a majority stake is acquired.

Research has also focused on the private benefits that shareholders can extract from target firms when they acquire control. This could be an alternative explanation for the generation of abnormal returns. Although the effects of ownership on the potential for shareholders to earn private benefits will not explicitly be dealt with in this work, it is closely related to the topic of Mergers & Acquisitions, and in particular with contracting and cross-border M&A. Private benefits of control are clearly associated with emerging economies (Dyck and Zingales 2004). Both legal and extra-legal mechanisms are essential for managers to capture these benefits. The literature is poor in attempts to precisely define what constitutes private benefits of control, and to estimate how large they are. One of the biggest challenges for researchers is that often shareholders will only harness the value of the private benefit if it is non-verifiable (Dyck and Zingales 2004). Currently however, there are at least two methods that attempt to quantify the value of these benefits.

The first method is proposed by Barclay and Holderness (1989). The authors sugest using the difference between the price per share paid and the price per share in the market. In particular, the authors argue that the price paid reflects not only the cash flows stemming from the ownership of the underlying business, but also the private benefits of controlling it. On the other hand, the market price reflects exclusively the cash flow benefits of non-controlling shareholders. The second method is developed by Zingales (1995). The author suggests using the information contained in different classes of shares to compute the value of control. Specifically, the expected price a shareholder is willing to pay for control can be estimated, which should reflect the private benefits they expect to receive.

The literature argues that there are two important mechanisms to circumvent the negative effects on capital market efficiency of private benefits: legal, and extra-judicial. In particular, non-controlling shareholders can use legal mechanisms to sue top management. Alternatively, labour pressure and competition, as well as the development of media and communication, can all act as important detrimental factors in the appropriation of private benefits. Further to the existing literature, we suggest that the negative impact on a firm’s image can overwhelm the potential private benefits of control in such a way that the cash flow generation from the business itself is even more negatively affected by bad publicity and lack of employee productivity than the gain from harnessing the private benefits. II.IV – Transaction Costs Transaction costs are a critical component of contracting and as a consequence of M&A deals, which in turn are a central piece of this work. In particular, the literature argues that if transaction costs were negligible, then economic activity in its broadest sense would be irrelevant since competitive organizational advantages would be eliminated by costless contracting (Williamson 1979). Moreover, the literature seems to be consensual in the argument that opportunism is paramount in the study

of transaction costs, and that these are especially important when dealing with human and physical capital transactions. Several dimensions have been identified as central to transaction cost definition. Of these, we highlight the importance of uncertainty, the frequency of exchange, and transaction-specificity.

II.V – Opportunistic Behaviour and Quasi Rents

Coase (1937) argues that a firm is a collection of implicit and explicit contracts between managers and stakeholders. The author argues that contracting costs must be clearly defined when considering vertical integration. As a consequence, efficient decisions by top management might lead them to intrafirm rather than interfirm transactions (Alchian, Crawford and Klein 1978). Moreover, it is relevant to consider not only the explicit costs of interfirm transactions, but also the post-contractual costs originating for example from opportunistic behaviour. This is an exhaustively discussed subject in the literature. In particular, post-contractual opportunistic behaviour can be defined as the risk that contracts will not be honoured, even after every contingency has been accounted for. Alchian, Crawford and Klein (1978) argue that one of the most likely scenarios capable of producing opportunistic behaviours are quasi rents. Specifically, a quasi-rent is a temporary rent that arises from temporary phenomena such as short run barriers to entry. The same authors further argue that to circumvent opportunistic appropriation of quasi rents managers have two solutions: further contracting, or vertical integration. It is interesting to note that in this case, contracting costs are likely to increase, leading to the probable outcome of vertical integration to reduce the potential for opportunistic behaviour. II.VI – Ownership and Control

Another important subject in the literature, in particular related to corporate governance, is the separation between ownership and control. It is important to note that organizational imperatives are not the only factor that influences how ownership and governance structures within a firm are defined. In particular, the political and social environment in which a firm is based define the legislative and cultural bodies which ultimately dictate how these aspects of governance must

shape themselves. In effect, these predicaments affect which firms and which ownership structures will survive and which are ultimately headed for failure (Roe, Political Determinants of Corporate Goveranance 2003). In American Corporate Governance practices, a principal-agent model is employed. As a consequence, owners are separated from managers. However, a key issue of interest alignment surfaces. Managerial agendas can differ from shareholder agendas (Roe, Political Determinants of Corporate Goveranance 2003). In contrast to this model, several Continental European countries employ concentrated ownership structures. They do so to avoid misalignment of incentives, which are harder and costlier to solve through typical legal mechanisms in those countries. Moreover, politics can influence the decisions of managers in terms of employment, or other strategically important considerations that will deviate them from their profit maximizing objectives. This interference has important consequences at the level of capital usage for non-efficient purposes, and ultimately imposes an added barrier to the alignment of incentives between managers and shareholders. II.VII – Relationship and Arm’s Length Systems The interaction between stakeholders and the institutions they represent define the financial markets in which they operate. As a consequence, financial markets can be considered as functioning under a relationship system, or under an Arm’s length system. The primary goal of a financial market is dual. In particular, it exists to efficiently allocate resources to the most productive uses, and to ensure that the financier is adequately compensated. Therefore, it is relevant to discuss the importance of financial markets in a wider spectrum, rather than remaining limited to Mergers & Acquisitions, which is just one of many interactions possible in those markets. We follow Rajan and Zingales (1998).

A financial market operating under a relationship system ensures that the financier will be adequately compensated by granting him power over the entity which is financed. In its simplest form, the financier is given ownership of the firm. In a more

complex form, by retaining monopolistic power over the firm, whether it be in the capacity of a sole customer, or major supplier, the financier retains substantial influence over the firm and in effect, controls it. However, granting a monopoly like structure of power is likely to require the creation of artificial barriers to entry, for example, of new customers or new suppliers. An example of such barriers is regulation, which considerably increases the costs of entry for other competitors.

In contrast, financial markets can operate under an Arm’s length system. In this case, the financier will be protected by explicitly defined contracts, which makes institutional relationships worth less. It is important to note that while relationship based systems thrive in environments with poor legal definition, the arm’s length system depends on the enforceability of contracts. A relationship based system depends on reputation and honour. An arm’s length system depends on the unbiased enforcement of contracts by courts of law. II.VIII – Fundamentals of Law We present a comprehensive overview of the founding law principles and traditions. These have become more specific and complex over time, and ultimately define today’s legal international paradigm. We follow La Porta, et al. (2000).

Laws and regulations are mostly not written from origin, but are instead adapted from a set of families and traditions. There is no unanimity amongst scholars and legal researchers regarding the criteria used to classify legal families. Nevertheless, some of the frequently used criteria include the historical background and development of the legal system under analysis, the theories and hierarchies of the sources of law, the working methodology of jurists, the characteristics of the legal concepts employed by a specific system, the legal institutions of the system and the divisions of law that are employed within the system. Given this set of criteria, and focusing on commercial law, we can define two key groups: civil law, and common law.

Civil law is the oldest legal tradition in the world and originates from Roman law. Specifically, it relies on legal scholars to interpret its rules. Within civil law, one has three historically distinct streams: the French, the German, and the Scandinavian. The French Civil Law finds its roots under Napoleonic France in 1807, and quickly expanded to Belgium, The Netherlands, Poland, Italy, and West Germany. During the colonial era, France extended its legal influence across to East and Northern Africa, Indochina and Oceania. Currently it overreaches Luxembourg, Portugal, Spain, and Italy. The German Civil Law was created in 1897 after the German Unification. It had severe implications on the legal structure of Austria, Czechoslovakia, Greece, Hungary, Italy, Switzerland, Yugoslavia, Japan and Korea. The Scandinavian Civil Law is less derived from Roman Law, but still defines the legal structure of most Nordic Countries.

In what concerns Common Law, this stream is widely based on English Law. Precedents from legal decisions are typically at the core of common law development, as opposed to the contribution of scholars in the civil law case. Common law has shaped the legal system of the British colonies of the United States, Canada, Australia and India. II.IX – Investor Protection Laws and Enforceability In what concerns the study of Mergers & Acquisitions, it is relevant to analyse the effectiveness of civil and common laws from an investor protection and corporate governance point of view. Regarding Investor rights, civil laws tend to yield poor protection when compared to common law countries. French civil law countries give investors the poorest protection rights. Regarding enforceability, Scandinavian and German civil law

countries tends to outperform the rest. Again, French civil law countries rank the lowest in terms of law enforceability.

It is important to note that weak protection countries have alternative means to cope with their legislative paradigm. Specifically, La Porta, et al. (2000) proposes two solutions: either better enforceability, or bright-line rules. Empirical research shows that better enforceability does not seem to be an adequate solution to circumvent the negative effects of poor legal protection. On the other hand, these countries can implement bright-line rules, which are mandatory standards introduced to retain and distribute capital to investors, and which limit managerial expropriation. For example, only French civil law countries have mandatory dividend policies. As a result of weak investor protection, often weak legal protection countries exhibit higher ownership concentration. In particular, more concentrated ownership is found to lead to incentive creation for managers to work and for investors to monitor their managers. In what concerns corporate governance, there is a wide-ranging body of literature concerning this topic. Once again, we follow La Porta, et al. (2000) to describe the relevance and impact of investor protection laws on corporate governance. These laws are relevant in this context for at least two reasons: due to extensive expropriation potential of minority shareholders by controlling shareholders, and because of manager incentive misalignment. Specifically, minority investors always face the risk that the returns on their investments will never materialize. This can take multiple forms, ranging from the literal theft of profits to the manipulation of internal transfer prices, at lower than market prices. The resulting asset sale and investor dilution is legal in most jurisdictions, hence the weak investor protection. However, it has a materially negative impact on the wealth of those same shareholders. From the theory that debt and equity are claims to cash flows from a collection of projects that constitute a firm, a key question arises: what is the motivation of managers to actually give those streams of cash flows to minority investors? The literature presents two models that take into account this paradigm. Specifically, in the first model, Jensen and Meckling (1976) argue that the transfer of

cash flows from projects to investors cannot be considered certain, since managers will use them for their own benefit. Financial contracts are viewed as contracts that yield rights to the underlying cash flows. The limitation on expropriation is the residual equity ownership by entrepreneurs that enhances their interest in dividends (La Porta, et al. 2000). In the second model, Hart (1995) focuses on the power differential between investors and managers, and focuses on the difference between contractual and residual rights. The model specifies that investors only receive cash flows because they have power, and not because it is their underlying right.

In any case, the importance of both the quality of the laws and the potential for their enforceability is paramount. If law enforceability does not work adequately, or if those laws do not exist in the first place, then external finance through equity or debt will be impacted. II.X – Labour Laws This work focuses on the role of law differentials across countries in relation to the generation of abnormal returns for shareholders. Within the international legal paradigm that concerns labour, specific sets of laws exist, which are relevant for this study. We follow Botero, et al. (2004).

In most countries, laws concerning employees fall into three categories: Employment Laws, Industrial and Collective Relations, and Social Security. Employment laws define individual employment contracts. Industrial and Collective Relations laws define the ability to bargain and govern collective agreements between employees and employers. Finally, social security laws deal with the social response to the needs and conditions of human capital, which have a significant impact on their current and future quality of life, including aspects related to death, illness, retirement or unemployment.

Employment laws fundamentally define the relation between the employer and the employee, regarding all terms and conditions, rights and obligations, and

contingencies that each party is subject to. Moreover, it includes a list of reasonable causes for termination. Legal regulation may also limit the freedom of dismissal by requiring union agreement, the public employment service or a labour inspector or judge. Some countries can go as far as requiring rehabilitation programmes such as retraining prior to dismissal. The cost of dismissal is also covered by employment laws, with some legislation requiring lengthy period of time notice prior to actual dismissal, as well as severance packages.

Industrial and Collective Relations laws are specifically concerned with protecting workers from their employers. In particular, this type of law governs a balance of power between labour unions and top management. There are three sub-types of Industrial and Collective Relations laws. These are collective bargaining laws, participation of workers in corporate management, and collective dispute regulation. Collective bargaining refers to the ability that countries give to collective employee associations to bargain certain employment terms and conditions, through means of unions. Some countries include in their collective bargaining laws the requirement that hiring is done only under from a pool of candidates that belong to specific labour unions. This phenomenon is referred to as a closed shop. Regarding worker participation in management, the body of regulation is focused on including workers in the board of directors of a company. Finally, regarding laws of collective disputes, these cover legal strikes, restrictions to strikes, employer defence options, compulsory arbitration, and the constitutional cover to strikes.

Social security laws are concerned with issues related specifically to old age, disability, death, sickness, and unemployment. Botero, et al. (2004 ) measure these variables based on the generosity of pensions vis-à-vis the worker’s life expectancy, the age of retirement, the percentage of the monthly salary that is deducted for pension purposes, and finally the level of protection that the pension system provides to retired individuals.

II.XI – Theory of Institutional Choice Institutional choice theory is paramount to explain the choices of countries regarding their legal systems. Botero, et al. (2004) argue that there are three major theories concerning a country’s institutional choice: The Efficiency theory, the Political Power theory, and the Legal theory. The efficiency theory was proposed by North (1981) and Demsetz (1967). It suggests that the choice of an institution is based on efficiency considerations only. That is, it holds that there are fixed costs to set up institutions at start, therefore it is only rational to support them when the potential benefits surpass costs. The efficiency theory can be specified further. First, one can consider the distinction between regulation and social insurance. That is, social insurance can potentially deal in a more efficient way with market failures in countries with lower social margin costs of tax revenues. This means that poor countries must regulate to protect workers from being fired or mistreated, while wealthy countries can rely on insurance to reduce this risk, which in itself is financed by taxation. Second, the other subclass of the efficiency theory states that the main cost of regulation is the potential for abuse of the regulated firms by governmental institutions. The political power theory states that the ultimate goal of institutions is to transfer resources from those without political power to those with access to it. In particular, it moves away from the perception of efficiency maximization. According to this theory, institutions are inefficient on purpose. More specifically, there are two distinct theories, one of which states that the main political decision process is the election, meaning that it is those who win them that shape the legislative context of a nation, and the second theory states that laws are actually shaped by the influence of interest groups. It is relevant to mention that the political power theory is viewed in the literature as being the main explanation of labour regulations. That is, based on the electoral theory, regulation protects workers through socialist measures, and based on the interest groups theory labour regulations are the result of pressure

from organized trade unions and other groups with the aim of collectively protecting workers.

The third theory of institutional choice is the legal theory. This is based on the difference between legal traditions surfacing from differences between the civil and common law paradigms described previously. Specifically, the legal theory states that countries with distinct legal traditions use different institutional technologies for social control of business (Djankov, Glaeser, et al. 2003). The legal theory says that countries using common law principles tend to rely on contracts more heavily. On the other hand, civil law countries rely more heavily on regulation. This means that civil law countries will tend to regulate labour markets more intensely under the legal theory. The empirical evidence produced by Botero, et al. (2004) suggests the validation of the legal theory. The authors argue that patterns of regulation across countries are widely derived from their legal structure, which as discussed previously was originated from key historical systems – the civil and common laws. II.XII – Electoral Systems The following is a discussion of major international electoral systems. If it is true that the legal theory is shown to explain each nation’s institutional choice, then it is also true that labour laws in particular are shaped by the political power theory. Therefore, it is relevant to explore the process of elections in more detail. In particular, we present the Majoritarian and Proportional Electoral Systems. These systems are relevant in the context of investor and employee protection laws. The literature provides a comprehensive overview of the subject. We follow Pagano and Volpin (2005). A proportional electoral system is best described as giving the party with the most absolute number of votes victory of an election. Under this system, the importance of each party in terms of their influence on the final election result is dependent on

its demographic importance and its ideological cohesion. On the other hand, in a majoritarian electoral system, it is the party that gathers the biggest number of districts that wind a specific election. The authors predict that investor and employee protection laws should be negatively correlated, and moreover that proportional systems should be associated with a focus on optimizing the needs and preferences of both employees and investors outcome. On the other hand, a majoritarian system should be focused on a non-corporate outcome. II.XIII – Strictness of Regulations and Rigid Labour Markets

We make a brief theoretical mention to the concept of rigid labour markets and relate it to the strictness of regulation enforcement. We follow Nicoletti, Scarpetta and Boylaud (1999) and Forteza and Rama (2001).

Rigid labour markets are relevant to this work due to its economic foundation, which can shed light into the context of value creation across borders. In particular, consider economic reform. The rigidity of labour markets will lead to a reduction in competitiveness, whereas flexibility should lead to cost adjustments, which are adequate to maintain industry competitiveness. This is to say that the adjustment process of resource reallocation takes much longer under rigid market conditions, which is inefficient. This can potentially be a key source of value for firms in a cross-border context.

Economic reform tends to be either political or economic in its foundations. Specifically, it is the economic argument that suggests that labour markets should not be regulated, and thus made flexible. Minimum wages, mandatory benefits, and other special benefits increase the complexity and rigidity of labour markets. On the other hand, the political argument suggests that labour markets should be more heavily regulated, and specifically the government should play a role in terms of compensating employees affected by economic reforms. The aim of these mandatory regulations is often not to allow individuals to fall into a situation of poverty, even if that leads to efficiency losses in the economy at an aggregate level.

III – ECONOMETRIC SCOPE & HYPOTHESIS

Chari, Ouimet and Tesar (2010) find that developed market acquirers gain a statistically significant and positive abnormal return of 1.16% over a three-day event window, when the target firm is based in emerging markets and control is acquired. This result is puzzling in the context of the broader literature. Specifically, Gregor, Mitchell and Strafford (2001) find that over a sample of 7,376 M&A observations between 1973 and 1998, the acquirer abnormal return is statistically indistinguishable from 0% at conventional levels. With this work, we attempt to explore two key aspects of cross-border M&A. First, we implement an alternative methodology to measure cumulative abnormal returns, which takes into account the problem of contamination of the estimation period, and compare those results with a simple market model. Second, we study the importance of labour laws in the context of value generation for the acquiring firm. Although the goal is to be as thorough as possible at each stage of this study, there are methodology and data limitations that narrow the scope of what can be presented. These present an opportunity for further studies, and are thus discussed in this section in some detail. In this section, we also formulate our hypothesis. III.I – Event Study Methodology The event study methodology is an essential tool for empirical research in finance. The literature often uses the framework developed by Fama, et al. (1969). It has at least four key steps. First, the definition of the event to be studied and the selection of securities. Second, the specification and estimation of a reference model. Third, the computation of abnormal returns. And finally, the testing of hypothesis. In what concerns each of the above-mentioned steps, there are key challenges to tackle. As an example, when defining an event, it is crucial to identify the correct date when it happened. For example, when considering M&A event studies, one must select the announcement date of the merger, and not the execution date. Even more complex,

if one suspects of information leakage, then the effect of this new piece of information will be incorporated in the stock price even before the announcement date. The definition of the time period during which an event occurs is referred to as the event window. The more uncertain one is about the specific date of the event, the larger the event window must be, and as a consequence the less precise the impact of that specific event on the security’s will be when performing hypothesis testing. The goal is to incorporate the complete effect of the event on any given security, while simultaneously minimizing as much as possible the event window in order to maximize the power of the tests performed later.

The second step of the event study methodology involves the specification and estimation of a normal return generating model. In this stage of the event study methodology, the larger the estimation window, the more robust the model results will be. In the third stage, cumulative abnormal returns must be computed. This process is straightforward and the literature is relatively consensual in its implementation. In the fourth stage, statistical tests of significance are performed. The literature provides a variety of tests of statistical significance, which we present in detail in section IV. The specification of a normal return generating process in the second phase of the framework of Fama, et al. (1969) can follow a variety of methodologies. Historically, these have typically ranged from a constant mean model without any underling theory of asset pricing, to the more common employment of a market model. The common feature to every model however is the assumption that the estimation period is fully normal, meaning, no outlier events have been announced during that period which can distort the true normal return generating process of a given security. Only recently has research been dedicated to tackle the method of estimating abnormal returns, taking into account the serious issue of contamination. In what follows, we start by presenting the classic market model in the context of event studies. We also present alternative methodologies that are shown to have dramatically improved power versus the classic market model. We follow Aktas, Bodta and Cousin (2007).

III.II –Market Model

The market model is commonly implemented in the context of event studies. It is simple to implement, and has no underlying theory of asset pricing, such as the CAPM. The market model is given by

R",$ = α"+ β"R),$+ ε",$ (1)

where R",$ is the return of firm j at time t, R),$ is the market return at time t, and ε",$

is the residual of firm j at time t. The coefficients α" and β" are estimated by OLS.

With this, an abnormal return is defined as a return which would not be forecast by equation (1). Specifically, the abnormal return of each stock i at moment t will be equal to ε",$. It is important to note that for multiple statistical tests of abnormal

returns, it is assumed that the ε",$ term is iid. This is clearly not the case given

empirical evidence, and presents a key weakness of the typical parametric tests used. Over time, several statistical tests have been developed to test the significance of abnormal returns. We explore the BMP and the Beta-1 tests. Before, we clarify the notation used henceforth. The estimation window begins in moment t and ends at moment T. The event window begins at moment – 1 and ends at moment +1, with the event date occurring at moment 0. Finally, each sample is composed of N events. The BMP test was first introduced by Boehmer, Musumeci and Poulsen (1991). In particular, the BMP test takes advantage of the estimated cross section variance of the standardized abnormal returns as opposed to simply using the theoretical variance (Aktas, Bodta and Cousin 2007). First, the test requires the computation of standardized abnormal returns 234,5= 678,9 :; <=?@A> = (CD,E@CD)G (CD,A@CD)G ? AH> (2)

where 234,5 is the standardized abnormal return of firm j at moment 1, I34,5 is the

abnormal return computed using the market model presented in equation (1), 2J is

the standard deviation of the error term of equation (1) during the estimation period

t to T, 3K,L is the market index return at the event date, and 3K is the average

market return during the estimation period. Cumulative standardized returns are then computed as M234 = 5 234,5 N5 (3) The BMP test is then computed as OPQR = > S S8H>T:78 > S(S@>) :78N UC8 S S VH> G S 8H> 9 @9 (4) A key disadvantage of the OPQR test is the potential for cross-sectional correlation. On the other hand, the test presents multiple strengths. These include the reduced impact of the underlying distribution of abnormal returns given the standardization of the returns, and the fact that the test takes into account serial correlation.

Alternatively, the Beta-1 test can also be used. The test has the disadvantage of assuming that abnormal returns are normally distributed. On the other hand, the test does not use data from the estimation window, thus reducing the potential for bias derived from contamination. We note however that this bias will already be incorporated in the estimation of abnormal returns. The Beta-1 test takes the form OWXY − 1R = > S S8H>T678 > S(S@>) 678N \C8 S S VH> G S 8H> 9 @9 (5) where MI34 = 5N5I34,5 (6)

Alternative testing procedures not used in this work are extensively covered in the literature. As an example, consider nonparametric alternatives such as the RANK test (Corrado 1989), which does not assume an underlying distribution of abnormal returns and attempts to neutralize the impact of extreme outliers, or the sign test (Cowan 1992), which accounts for the skewness of returns. III.III – GARCH Model The generalised conditional heteroscedastic model was first introduced by Bollerslev (1986). Specifically, the model eliminates the unrealistic assumption of time-invariant volatility of security returns. The practical application of time-varying volatility in the context of event studies is relatively intuitive. In particular, Savickas (2003) suggests the implementation of the time-varying framework of Bollerslev (1986) with an incremental dummy term to capture the event induced abnormal return. The author suggests implementing the return generating process

34,] = ^4 + _43K,] + `4a4,]+ b4,] , b4,] ~d(0, fg) (7)

where 34,] is the return of firm j at moment t, 3K,] is the return of the market index

at moment t, a4,] is a dummy variable that assumes the value of 1 if X ∈ − 1, 1 and

0 otherwise, and b4,] is an error term which is assumed to be normally distributed. The time-varying variance is then given by f4,]g = i 4 + j4f4,]N<g + k4b4,]N<g + l4a4,]+ m4,] (8) where f4,]N<g is the lagged estimate of the variance term, b 4,]N<g is the lagged squared error term from equation (7), a4,] is the same dummy variable presented in equation

(7), which takes the value of 1 if X ∈ − 1, 1 and 0 otherwise, and m4,] is an error

term. The coefficients ^4, _4 , `4 i4, j4, k4, and l4 are estimated by maximum

likelihood. Under this specification, Savickas (2003) argues that `4 captures the

time-varying variance. After standardizing the `4 term, statistical testing is then performed using the BMP test presented in equation (4). As contamination related increases in variance are permanent under a time-invariant paradigm, the GARCH (1,1) model provides an interesting alternative which could theoretically reduce the significance of such events when performing testing.

However, Aktas, Bodta and Cousin (2007) find that under a simulation of contamination of events, the GARCH methodology clearly lags in terms of power and robustness, when compared to other alternative procedures, such as the market model. III.IV – 2-State Market Model The third alternative to estimating abnormal returns is the construction of a state dependent market model. The presence of unrelated abnormal events during the estimation period will lead to permanent increases in volatility under the classic market approach. As a consequence, testing will likely be downwards biased due to an upward bias in the estimates of standard errors (Aktas, Bodta and Cousin 2007). To circumvent this issue, the authors suggest implementing a 2-state version of the market model presented in equation (1). Such a model follows the methodology first proposed by Hamilton (1989), who develops a return generating process modelled by a first-order Markov Chain Process. Specifically, the model is presented as 34,]= ^4,<+ _4,<3K,] + m4a4,]+ b4,],< 34,]= ^4,g+ _4,g3K,] + m4a4,]+ b4,],g , b4,],n~d(0, f4,],ng ) (9)

where ^4,n, _4,n, and b4,],n, o ∈ 0,1 are state dependent variables, and m4

is a non-dependent variable, all of which are estimated by maximum likelihood. This allows for the specific incorporation of event induced volatility. In effect, the model results in a low variance state, which is analogous to a normal level of volatility, and a high variance state, which is analogous to unexpected events during the estimation period. As a consequence, one has f4,],gg > f4,],<g where k=2 corresponds to a state of

abnormal variance. The theoretical transition between states is governed by a first-order Markov Process, which yields a transition matrix p<< 1 − pgg 1 − p<< pgg (10) where pr,s = p S$ = m S$N<= n) is the conditional probability of changing from state n to state m. Specifically, note that the transition from n to m only depends on one previous state. The unconditional probability of each regime is given by p S$= 1 = <NvGG gNv>>NvGG p S$= 2 = <Nv>> gNv>>NvGG (11) To test the significance of the abnormal returns yielded by equation (9), the TSMM test can be constructed x2PPR = > S S8H>T:78 > S(S@>) :78N UC8 S S VH> G S 8H> 9 @9 (12) where the standardized abnormal return is computed as 234,5 = y; z{(y8) (13) and M234 is computed as in equation (3). III.V – Over Estimation of Standard Errors If the true return generating process is given by a 2-state Market model, then the OLS estimators of a single state model are biased (Aktas, Bodta and Cousin 2007). In particular, the authors show that a 2-state return generating process based on a first order Markov Chain Process provides superior results both in terms of power and robustness when compared to the simple market model introduced by Sharpe (1963). Moreover, Aktas, Bodta and Cousin (2007) argue that if the true return

generating process is given by two states, then using a one state model will result in overestimation of the standard errors of the abnormal returns.

We follow the demonstration of Aktas, Bodta and Cousin (2007) regarding the overestimation of standard errors under a single-state specification. Consider initially that a firm’s return generating process is given by equation (1). The same equation can be written as

R",$=X"b"+ε",$ (14)

where X" is a column vector and b" a row vector of coefficients estimated by OLS.

Given the assumption of homoscedasticity, the covariance of the OLS estimator of equation (14) is given by

COV" b" X")= σ"g(X"ÇX")N< (15)

Consider now that the true return generating process is state dependent, as given in equation (9). Again, equation (9) can by written in matrix notation as

R",$=X"b",<+ε",$,< ,S$=1

R",$=X"b",g+ε",$,g ,S$=2 (16)

Finally, the variance of the residuals ε",$,É can be given by

Eε",$,<ε",$,<Ç| X = σ"g,<I ,S$=1

Eε",$,gε",$,gÇ| X = σg",gI ,S$=2 (17)

where á corresponds to the identity matrix. Note that, as discussed previously, and by definition of the two states, we have that σ"g,g> σ

",<

g , that is, S

$=2 incorporates