Revista

de

Administração

http://rausp.usp.br/ RevistadeAdministração51(2016)299–309

Information

technology

Mobile

social

money:

an

exploratory

study

of

the

views

of

managers

of

community

banks

Moeda

social

no

celular:

estudo

exploratório

sobre

a

percep¸cão

dos

gestores

de

bancos

comunitários

Moneda

social

en

el

teléfono

móvil:

estudio

exploratorio

sobre

la

percepción

de

los

gestores

de

bancos

comunitarios

Eduardo

Henrique

Diniz,

Adrian

Kemmer

Cernev

∗,

Eros

Nascimento

Funda¸cãoGetúlioVargas,SãoPaulo,SP,Brazil

Received23March2015;accepted3February2016

Abstract

Thisarticleaimsto evaluatetheadoptionpotentialofadigital socialcurrencymodelusingmobile phones.Despitethesignificantliterature concerningbothsocialcurrenciesandmobilepayments,therearefewstudieswithafocusonsocialcurrenciesbeingoperationalizedviamobile payments.Animportantaspectoftheliteratureonmobilepaymentsandsocialcurrenciesistherolethatbothinstrumentsmayplayinthefinancial inclusion.DespitetheabsenceoflastingexperiencesforanempiricalanalysisinBrazil,webelievethattheremaybesynergybetweenthesetwo typesofpaymentinstruments.Toevaluatethepotentialofamobiledigitalsocialcurrency,weconductedinterviewswithcommunitybankmanagers, focusingontheirperceptionsofacceptanceofthisinnovativemodelintheircommunities.Asatheoreticalbasis,wearticulatedtheconceptof transformationalframing,originatedfromtheperspectiveofinterpretiveframesofcollectiveaction.Asaresult,weidentifiedatransformational discoursebywhichcommunitybankmanagerscreatenewmeaningsandunderstandingsofthisemergingpaymentsystemmodel.

©2016DepartamentodeAdministrac¸˜ao,FaculdadedeEconomia,Administrac¸˜aoeContabilidadedaUniversidadedeS˜aoPaulo–FEA/USP. PublishedbyElsevierEditoraLtda.ThisisanopenaccessarticleundertheCCBYlicense(http://creativecommons.org/licenses/by/4.0/).

Keywords:Socialcurrencies;Communitybanks;Mobilepayments;Collectiveaction

Resumo

Oobjetivodesteartigoéavaliaropotencialdeadoc¸ãodeummodelodemoedasocialdigitalviacelulares.Apesardaexistênciadeumaliteratura significativatantosobremoedassociaisquantosobrepagamentosmóveis,quasenão háestudos sobremoedassociaisoperacionalizadasvia pagamentosmóveis.Umaspectoimportantedaliteraturasobrepagamentosmóveisesobremoedassociaiséopapelqueambososinstrumentos podemrepresentarparaainclusãofinanceira.Adespeitodainexistênciadeexperiênciasduradourasparauma avaliac¸ãoempíricanoBrasil, acreditamosquehápotencialsinergiaentreessesdoistiposdeinstrumentosdepagamento.Paraavaliaropotencialdeumamoedasocialdigitalvia celulares,fizemosentrevistascomgestoresdebancoscomunitáriossobreapercepc¸ãodeaceitac¸ãodessemodeloinovadoremsuascomunidades. Comobaseteóricaarticulamosoconceitodeframingdetransformac¸ão,originadodaperspectivadeframesinterpretativosdeac¸ãocoletiva.

∗Correspondingauthorat:Fundac¸ãoGetulioVargas,AvenidaNovedeJulho,2029,0113-920SãoPaulo,SP,Brazil.

E-mail:[email protected](A.K.Cernev).

PeerReviewundertheresponsibilityofDepartamentodeAdministrac¸ão,FaculdadedeEconomia,Administrac¸ãoeContabilidadedaUniversidadedeSãoPaulo –FEA/USP.

http://dx.doi.org/10.1016/j.rausp.2016.02.002

Comoresultado,identificamosumdiscursotransformacionalemqueosgestoresdosbancoscomunitárioscriamnovossignificadoseentendimentos sobreessemodelodesistemadepagamentosemergente.

©2016DepartamentodeAdministrac¸˜ao,FaculdadedeEconomia,Administrac¸˜aoeContabilidadedaUniversidadedeS˜aoPaulo–FEA/USP. PublicadoporElsevierEditoraLtda.Este ´eumartigoOpenAccesssobumalicenc¸aCCBY(http://creativecommons.org/licenses/by/4.0/).

Palavras-chave: Moedassociais;Bancoscomunitários;Pagamentosmóveis;Ac¸ãocoletiva

Resumen

Elpropósitoenesteartículoesevaluarelpotencialparalaadopcióndeunmodelodemonedasocialdigitalpormediodeteléfonosmóviles.Aunque existaunaliteraturasignificativatantosobremonedassocialescomosobrepagosmóviles,sonpocoslosestudiosrelativosamonedassociales enoperaciónpormediodepagosmóviles.Unaspectoimportantedelaliteratura,seaconrelaciónalospagosmóvilesolamonedasocial,esel papelqueamboslosinstrumentospuedenrepresentarparalainclusiónfinanciera.Apesardequeapenasexistenexperienciasconcretasparauna evaluaciónempíricaenBrasil,sesuponequehaypotencialsinergiaentreestosdostiposdeinstrumentosdepago.Paraevaluarelpotencialdeuna monedasocialdigitaloperadapormediodemóviles,sellevaronacaboentrevistascondirectivosdebancoscomunitariossobrelaaceptaciónde estemodeloinnovadorensuscomunidades.Comobaseteórica,searticulaelconceptodeframingdetransformación,quepartedelaperspectiva demarcosinterpretativosdeaccióncolectiva.Comoresultado,seidentificóundiscursodetransformaciónenelquelosdirectivosdelosbancos comunitarioscreannuevossignificadoseinterpretacionesdeestemodelodesistemadepagoemergente.

©2016DepartamentodeAdministrac¸˜ao,FaculdadedeEconomia,Administrac¸˜aoeContabilidadedaUniversidadedeS˜aoPaulo–FEA/USP. PublicadoporElsevierEditoraLtda.Esteesunart´ıculoOpenAccessbajolalicenciaCCBY(http://creativecommons.org/licenses/by/4.0/).

Palabrasclave: Monedassociales;Bancoscomunitarios;Pagosmóviles;Accióncolectiva

Introduction

TheemergenceofnewformsoflocaldevelopmentinBrazil, inparticularcommunity banksandsocialcurrencies, madeit possible tolearn alot about alternative economic forms that promotehumanityandsolidarityinplaceofapureconsumption logic(Singer,2009).Ifmoneyis,aboveall,asocialphenomenon (Lietaer&Primavera,2013),socialcurrenciesmaybe under-stood and considered in such a way as tocreate sustainable exchange relationships, thus enabling financial inclusion and theconsequentreductioninpovertyandanimprovementinthe qualityof life of needypopulations. The incorporationof an ICT (informationandcommunication technology) infrastruc-turetotheconceptofsocialcurrenciescouldmakethismeans ofpaymentmoreefficient,thuscontributingevengreatersuccess tothescaleoftheiroperations.

Giventheemergence overthelastdecadeof paymentsvia devices like mobile phones, particularly as an instrument of socialinnovationandpovertyreduction(Duncombe&Boateng, 2009),the opportunityarisestointegrate thesetwo concepts, socialcurrenciesandmobilepayments,whichdespitestill mov-ing along separate tracks have the potential to converge to commonsolutions.Sotheobjectiveofthisarticleistoevaluate theexpectationfortheintroductionofadigitalsocialcurrency modelbasedontheuseofmobilephonesfromananalysisof the discourse of community bank managers whoare already operatingasocialcurrencyintheircommunities.

Todoso,weshallanalyzethediscourseofthemanagersof thirteencommunitybanks,basedontheconceptof transforma-tionalframes(Benford&Snow,2000).Thearticleisdividedinto aninitialdiscussionaboutcommunitybanks,socialcurrencies andmobilepaymentswithinthecontextoffinancialinclusion, followedbyapresentationoftheconceptofindividualframing

(Goffman, 1974)andcollectiveactionframing (Snow,Soule, &Kriesi,2008).Finally,ananalysiswillbecarriedoutofthe potentialofmobiledigitalcurrenciesandhowtheyfitwiththe discourseofcommunitybankmanagers,withregardtoa trans-formationalappropriationlogicoftheirmeaningandtheuseof mobilepaymentslikedigitalsocialcurrency.

Communitybanks

Createdwiththeobjectiveofcontributingtotheprocessof financialinclusion,communitybanksarenot-for-profit institu-tions,whichprovidefinancialproductsandservicesthatsupport the development of local economies in needy communities (Freire, 2013).In Brazil, despite notbeing supervisedby the Central Bank,community banksare legallyauthorized inthe country bythe Law 9.790, of March23, 1990,which autho-rizes themtopromotenon-profitableexperimentationintrade andcreditbymeansofalternativeproductionsystems.Theyare authorizedtoformpartnershipswithotherpublicorprivate enti-tiesinordertopromotefinancialinclusioninthecommunities inwhichtheyoperate.

The first community bank in the country, Banco Palmas, startedoperatinginJanuary1998intheConjuntoPalmeira,a housingcomplexwith30,000peoplelocatedontheoutskirtsof Fortaleza,thecapitalofthestateofCeará,withaninitialcapital ofR$ 30,000(orUS$26,000atthetime)(Jayo,Pozzebon,& Diniz,2009).

consistedinaso-called“solidaritynetwork”,whichstartswitha focusonthecommunityandtheneighborhood’ssocialcapital. Right from the outset, Banco Palmas established itself as amodelCommunityDevelopmentBank,especiallybecauseof twopartnershipsthatoccurredin2004and2005,andthathelped extenditsmethodologytovariousotherregionsofthecountry. ThefirstofthemwaswithSENAES,theNationalDepartment of SolidarityEconomics of the FederalGovernment, andthe second withBanco doBrasil, oneof the biggest commercial banksinthecountry(Garcia,2012).

Oneof the fundamental elements of the community bank model disseminated by Banco Palmas is the use of a social currency.Whereas,on the onehand,microcredithadalready establisheditselfasanalternativeforcombattingpovertyand, ontheother,the useof socialcurrencies (alsocalled comple-mentaryor alternativecurrencies) provedtobe aninteresting strategyinthisfield,thecombinationoftheuseofasocial cur-rencyjointlywithmicrocreditwasthegreatinnovationbrought bythisBrazilianmodelforstrengtheningthelocaleconomyand financialinclusion(Singer,2009).

Socialcurrencies

Acommon characteristicofthe modeladoptedbymostof themorethan100communitybanksthatoperateinBrazilisthe useof socialcurrency(Neivaetal.,2013).Despitebeing rec-ognizablythe resultof variousinternationalexperiences with differentpurposes(Michel&Hudon,2015),communitybanks inBrazilplayedaleadingroleinspreadingthesocialcurrency model (Siqueira,Mariano, &Moraes,2014). Designed tobe apayment instrumentwithcirculation restrictedtoa particu-largeographicregion,socialcurrenciesareusedbycommunity banksforfinancingsmalleconomicactivitieswithinthe commu-nityinwhichtheycirculate,withafocusonencouraginglocal developmentandsocialtransformationbyprotectingthe econ-omyandlocalculturalprocesses (Blanc,2006;Franc¸aFilho, 2004;Freire,2013;Lietaer&Primavera,2013).

Withthispurpose,themicrocreditmodeladoptedbythe com-munitybanksusesa“proprietarycurrency”whichcirculatesin parallelwith the official currency. In the case of Banco Pal-mas,forexample,thiscurrencyisthe“Palma”,whichcirculates jointlywiththe“Real (R$)”,andis widelyacceptedbylocal traders.ThesesocialcurrenciesarebackedbyReaisona one-for-onebasis,whichmeansthatforeveryPalmaincirculationin thecommunitythereisoneRealheldascollateralinreserveasa guaranteeoffreeconvertibility.Someexamplesofsocial curren-ciesadoptedbycommunitybanksare:theMaracanãCastanha, Cocal,Guará,Girassol,Pirapire,TupiandSol(Freire,2013).

Mobilepaymentsandfinancialinclusion

In parallelwith butunrelated tothe community bank and socialcurrencymovement,theevolutioninmobilepayments– digitalpaymentsbymobilephone–hasalsobeendiscussedas animportantdriveroffinancialinclusion,particularlyin devel-opingcountries(Duncombe&Boateng,2009;Dancey,2013; Schulze,2014;Albuquerque,Diniz,&Cernev,2014).Themain

argument for consideringmobile payments as being a driver of financialinclusionliesinthefactthatmobiledeviceshave widerpenetrationthanbankaccountsindevelopingcountries, making them,therefore, an attractive alternative tothe prob-lemofbankaccessamongthelowincomepopulation(Bader& Savoia,2013).

JustasthecommunitybanksinBrazilandtheirsocial cur-rencies took their inspirationfrom Banco Palmas, the useof mobilepaymentsasaninstrumentofsocialinclusionislargely inspiredbythecaseofM-PESA,afinancialservicemade avail-able inKenya by mobilephone operatorSafaricom. By way ofM-PESA,millionsofKenyanswithrestrictedaccesstothe traditionalfinancialsystemcarryoutvariousservicesthatused to be exclusivetobanks, using their mobile phones (Jack& Suri,2011;Mas&Radcliffe,2010;Schulze,2014).Theservice allowsuserstotransfermoneyandcarryoutothersimple finan-cialservicesatminimalcostandwithoutrequiringaformalbank account(Chandy,Dervis,&Rocker,2012).However,despitethe successofthemobilepaymentmodelinKenya,itisnotknown up towhatpointthe successof the M-PESAinitiativeis not duetoasetofextremelyspecificfactorsandconditions(Mas &Morawczynski,2009),whichwouldmeanthat implementa-tioninotherlocations,andspecificallyinBrazil,wouldneeda differentbusinessmodel(Schulze,2014).

Atthesametime,wehaveanimportantculturalquestionof heavymobiletechnologyuseinBrazil,whichcouldbea posi-tivefactorfortheadoptionanddevelopmentofmobilepayments withinthe contextof financialinclusion.AccordingtoTeleco (2015),thedensityofmobilephonelinesper100inhabitantsin July/2015was137.6,aratethatishighevenincomparisonwith othercountries.DatafromtheITU(2013)showthatdeveloped countrieshaveadensityof123.6,comparedwith84.3for devel-opingcountries.Theworldaverage,initsturn,is91.2,while regions likeAfrica haveadensity of 59.8 andthe Americas, 105.3.

Despitethe fact that boththe useof socialcurrencies and mobilepaymentsmightrepresentanimportantroleinthe pro-cessof financial inclusion,thereare fewstudiesthat link the synergypotentialthatexistsbetweenthesetwoinstrumentsof payment.Inoneoftheserarestudies,Ramada-Sarasola(2012)

arguesthattheadoptionofmobilepaymentmethodsatthelocal level mayincrease the speed of currency circulation and the localmonetarymultiplier,thusallowinggreaterlocaleconomic developmentandsorepresentinganalternativetothetraditional financialsystem.

Accordingtothisregulation,“theBrazilianCentralBank,the National MonetaryCouncil,the Ministry ofCommunications andtheNationalTelecommunicationsAgencywillencourage, within thescope of their competences,financial inclusion by wayoftheparticipationofthetelecommunicationssectorinthe supplyofpaymentservicesand,basedonperiodicassessments, theywillbeabletoadoptmeasuresforencouragingthe develop-mentofpaymentarrangementsthatuseaccessterminalstothe telecommunicationservicesthatarethepropertyoftheuser.”

Therefore, it is tobe expected that therewill be astrong growthintheuseofmobilepaymentsinBrazil,mainlyaimed atincludingthatlayerofthepopulationthattodayhasnoaccess tofinancialservices.

The useof mobile payments alongwith asocial currency might represent an innovative and transformationalpath that hasnotyetbeenseeninanyexperimentthathasbeenstudied, eitherinvolvingmobilepaymentsormicrofinance.Itisprecisely theperceptionoftheappropriationofthediscourseofthistrend thathasbecomefashionableinthecountryamongsomeofthe mainmanagersofcommunitybanksinBrazil,which,sincethe originsof themodel disseminatedbyBanco Palmas,hashad technologyandapartnershipwiththebankingsectoraspartof itsDNA,whichthisstudytriestounderstand.

Narratives,individualframesandcollectiveaction frames

In harmony with the study of a possible digital currency functioningasasocialcurrency,weneedtounderstandthe per-ceptionofthepossiblefuturemanagersofthesecurrenciesin communitybanks.Literatureshowsthattheadoptionofmobile paymentsmaygaininscaleinsuchawayastobeusedbythe wholepopulationandalsoforlocaldevelopment(Chandyetal., 2012;Dancey,2013;Mas&Radcliffe,2010;Ramada-Sarasola, 2012;Schulze,2014),whichmakestheanalysisofthediscourse of the managers of community banks particularlyinteresting fortwoadditionalreasons:(1)understandingthepotentialand the expectationof theuse of thenewtechnology as adigital socialcurrency,modernizingtheuseofthepapercurrencies cur-rentlyusedbycommunitybanksandcreatingcollectiveformsof cooperationbetweenthem;(2)understandingtheperceptionof managerswhodealwithneedycommunitiesinwhichthe pop-ulationisalreadymorefamiliarwiththeconceptsoffinancial inclusion,startingfromtheassumptionthatcommunitybanks canbearelevantcollectiveplayerforadoptingthetechnology ofmobilepayments.

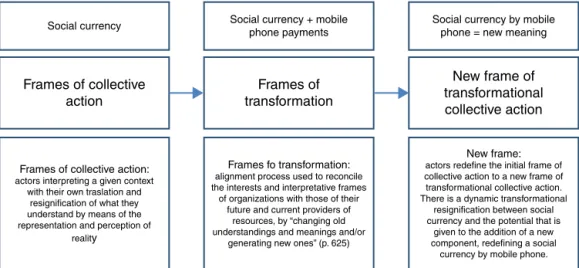

Therefore,as the theoretical basisfor our study,we focus on the mechanism calledtransformational framing, proposed byBenfordandSnow(2000).Thename‘framing’isgivento theworkofconstructingmeaningwhichoccurswithinthe col-lectiveactionlogicofsocialmovements(Gamson,Fireman,& Rytina,1982;Snow&Benford,1988;Snow,Rochford,Worden, &Benford,1986).

Thisconcept,whichisusedinotherareasofknowledge,was alsoknown through thestudiesof Goffman(1974)in sociol-ogy,whodefinesframesas interpretativeschemesthat enable individuals“tolocate,perceive,identifyandlabel”occurrences

within theirlivesandtheworldinwhichtheylive(p.21).In other words, framesare the wayin whichwe see the world, theframing,inthealmostphotographicsenseoftheword,with whichweseerealityandwithwhich,basedonacertainangle, wecreatemeaningandinterpretationsofit.Theyarecognitive structuresthatmoldtherepresentationofrealityandthe percep-tionof it,whichmayendupbeingunconsciouslyconstructed anddisseminatedinsociety.

Snow etal.(2008),however,distinguishframesfrom col-lective actionframes for interpretingday-to-day happenings. Accordingtotheauthors,collectiveactionframesmayhavethe sameinterpretativefunctionastheframesdefinedbyGoffman (1974),butwiththisoccurringbywayoffunctions,likefocusing onandthearticulationandtransformationofaparticularobject of orientation,linking differentpointsofasituation insucha wayastofocusonaparticularpreferentialaspectofmeanings, oronanarrativelanguage,tellingonestoryinsteadofanother. In otherwords,inthiscasetheintentionalityoftheplayersis assumedintheconstructionofthediscoursethroughtheirown translationsandresignificationsofwhattheyunderstandbythe representationofrealityandtheperceptionofit.

Along thesamelines,BenfordandSnow(2000)state that frames of collective action are “intended to mobilize poten-tial membersandconstituents,togainthesupportof viewers and observers, and to demobilize antagonists” (p. 614). For them,thereareseveralprocessesanddynamicsofframing,and between them there istransformational framing, whichis an alignmentprocessused inordertoreconcilethe interestsand interpretiveframesoforganizationswiththoseoftheircurrent andfutureresourceprovidersby“changingoldunderstandings andmeaningsand/orgeneratingnewones”(p.625).

Johnston(2002)establishessomekeyelementsfor frames, suchascontent,cognitivestructure,sharingbydifferent individ-uals,fixedandemergingelements,andtheirtext-based,spoken or written structures,in ordertorepresent symbolsand their structures.

Underadifferentconceptuallens,Maurer(2012)hadalready dealt with the issue of the distinct narratives and stories he discoveredininternationalexperiencesofadoptionand imple-mentationofmobilepayments.Theauthorstatesthathefound somerecurringstoriesandnarrativesusedtojustifyandexplain theuseofmobilepayments,someofwhicharemore transfor-mationalinnatureandthatsawmobilepaymentsasatoolfor fightingpovertythroughfinancialinclusion,whileotherswere morecommercial,seeingthemasanopportunity,forexample, formultinationalcompaniestopenetratemarketsatthebaseof thepyramid,whichisinlinewiththediscussionofPrahaladand Hammond(2002).

Social currency Social currency + mobile phone payments

Social currency by mobile phone = new meaning

Frames of transformation Frames of collective

action

Frames of collective action: actors interpreting a given context

with their own traslation and resignification of what they understand by means of the representation and perception of

reality

Frames fo transformation: alignment process used to reconcile the interests and interpretative frames

of organizations with those of their future and current providers of

resources, by “changing old understandings and meanings and/or

generating new ones” (p. 625)

New frame: actors redefine the initial frame of collective action to a new frame of transformational collective action. There is a dynamic transformational

resignification between social currency and the potential that is

given to the addition of a new component, redefining a social currency by mobile phone.

New frame of transformational collective action

Fig.1.Theoreticalframeworkusedbasedontheconceptsofframes.

theirroleascollectiveplayers,and,basedonthis,toinvestigate thediscourseadoptedbythemanagersofdifferentcommunity banksinBrazil.

Therefore,thisarticle brings togetherthe concepts of col-lective action frames and transformational frames to discuss atransformationalcollectiveactionframe,whichisthe resig-nification of ourunderstandingof old understandings as new understandingswithinanewcollectiveactionframe,asshown inFig.1.

What we seek to observe through this conceptual lens is whether the discourse of the interviewed managers of com-munity banks regarding the use of digital social currency is grounded within the transformational logic of creating new meaningsandunderstandings as proposedbythe transforma-tionalframingconcept.

Methodologicalapproach

Giventhevirtualabsenceoflong-termexperiencesof digi-talsocialcurrenciesandofpublishedstudiesonthisinteresting socialinnovation,thisarticlespeculatesonthepotential integra-tionofaplatformformobilepaymentswithasocialcurrency system (Dahlberg, Guo, & Ondrus, 2015; Diniz, Cernev, & Albuquerque,2013).

Thus,thisstudyevaluatesthepotentialofthecombineduse ofasocialcurrencywithmobilepayments,whichwewillcall digitalsocialcurrency.Forthis,theresearchmethodconsisted ofsemi-structuredinterviewswiththemanagersofcommunity banks,whichoperatewithsocialcurrenciesinpoor communi-tiesinBrazil. Theseinterviewswere conducted withthirteen managersfromfivestates(AM,CE,ES,APandSP)plusthe FederalDistrict,whowere presentduring theThird National MeetingoftheBrazilianNetworkofCommunityBanksheldin Fortaleza,betweenMarch12and15,2013.Allinterviewswere recordedinaudioandvideoandlastedfrom40mintoonehour.1 Intervieweeswereselectedaccordingtotheiravailability,butin

1 A10minvideobased onan editionof theseinterviewsis availableat

https://www.youtube.com/watch?v=-YAiv5EFtoo.

Table1

Profileandgeographicaldistributionofinterviewees. Territorialscopeand

sampleused

13communitybanks 14respondents

CommunityBanksof6 unitsofthefederationin4 regionsofthecountry: AM(1),SP(5)CE(4), ES(1),DF(1),AP(1) Profileofrespondents Managersof

communitybanks

Allrespondentsare residentsofpoor neighborhoods,where theirrespective communitybanksare located.Therewerefour menandtenwomen,with apparentagesranging between25and70years

Source:theauthors.

allcaseswecheckedwhetherthecommunitybankatwhichthe respondentworkedhadbeenoperating withsocialcurrencies foratleastoneyear(Table1).

The interviewsfollowedafive-topic script: (1) social cur-rencyuseinthecommunity,(2)difficultiesinthemanagement ofpaper-basedsocialcurrency,(3)mobilephoneuseinthe com-munity,(4)thepotentialofusingmobilephonesforpayment,(5) potentialacceptanceof amobilephone-basedsocialcurrency. Thesefivetopics,whichmadeupthebasicscriptofthe inter-view,aimedtoputintocontextanobjectthatdoesnotexistyet forthesemanagers–the mobilephone-basedsocialcurrency. Wetried,therefore,tocapturehoweachintervieweedeveloped their ownconceptionof thisimaginaryobject, basedontheir experiencesatworkwithpaper-basedsocialcurrencies,which actuallydidexistforallofthem.

terms,on how theplayers seeandperceive theusefulness of amobilephone-basedsocialcurrencythroughthelensoftheir ownworldviews(relyingontheconceptofframes),ratherthan tryingtoassesstheperceptionsofcompatibility,safety,usability, amongotherconcepts,thatwouldbeaddressedusingTAM.

Themethodologyusedinthisstudy,therefore,aimsto under-stand how old concepts are resignified into new ones based on theinterviewees’ discourse. Thisis whyit was correct to adoptdiscourseanalysistechniques,becausewewanttoidentify relationshipspermeatedbymechanismsthatarehiddenwithin language(Cappelle,Melo,&Gonc¸alves,2011).Toidentifythe “transformationaldiscourse”embeddedintheincorporationof anewtechnologyhithertounknownbytheinterviewees,thetext ofeachinterviewwasanalyzedseparately.Then,thepassages thatcouldbegroupedintooneofthefivetopicspresentedabove wereselected,inordertohighlighttheviewsofcommunitybank managersaboutthepotentialofdigitalsocialcurrencyintheir communities.

Themanagers’discourses

Basedonthe interviewswithcommunityleaders,we were abletocollectarangeofperceptionsonwhattheythinkabout thisinnovative wayof coupling socialcurrencies andmobile payments. In the interviews,the managers discussedthe role theircommunitybanksplayedinlocaldevelopment,andhow social currencies helped keep money circulating in the com-munity, aboutthe difficultiesof managingpaper-based social currency,abouttheuseofmobilephonesandthepotentialfor theadoptionof mobilephone-basedpayments andsocial cur-rency.Thefollowingareselectedstatementsbymanagersonthe topicscoveredintheinterviews.

Ontheacceptanceofsocialcurrency

Intheirdiscourse,communitybankmanagersclearlypresent howtheyseetheroleofsocialcurrenciesintheircommunity:

Manager–BancoLiberdade(AM):

”Thewealthweproducedherewasusuallygoneawayand ourcommunityremainedpoor.Nowwe’vebeenrunningthe bankforayearandahalf,andthe{social]currencycame tokeepthiseconomy[locally].”

Manager–BancoApuanã(SP):

” With the social currency the community’s going to buy thereinthat[local]market.It’snotgoingtogotothatbig market,which,apartfrombeingfaraway,wouldmeanthat [thewealth]wouldleavethecommunity. They’re goingto sellmoreandthestorekeeper’sgoingtoearnmoreandhis businessisgoingtogrow.”

Accordingtothemanagers,althoughthe benefitsof social currencyweredemonstrable,theyneededtoworkhardto pro-moteits acceptanceinthe community.Oneof thestatements clearlyillustratestheinitialmistrust:

Manager–BancoTonato(SP):

“Otherpeoplesay‘whyinventthisothermoneyifwealready haveamoneythatisthereal?”

Thisdistrustthatcustomershadwasgraduallyovercome,as acceptanceofthesocialcurrencygrewamongmerchants:

Manager–BancoOrquídea(SP):

“Ifyouhavethreeshopkeeperswhoagreedtouseitandten peopleinthecommunitywhounderstoodit...thatsetoffa

processthatwentfromonetotheother,andtodaywehave severalpeoplewhoseekoutthe[community]bank.”

Inadditiontobeingessentialtothestrategyfor disseminat-ingthesocialcurrency,theallianceofcommunitybankswith localmerchantshelpedensurenotonlytheadoptionprocessbut also hadamultiplierandeducationaleffectonthe restof the community:

Manager–BancoLiberdade(AM):

“There’sa samba-schooltherethatwasthemainpartnerand was also oneofthefirst toaccept the[social] currency. You canbuy drinkswiththe currency,youcanbuyyour Carnival costumes(...)andthatdroveacceptanceofthecurrency.”

Manager–BancoPauloFreire(SP)

“Nowthemerchants acceptthe currency.Wehave agood portfolio ofmerchants whoaccept it.Andthey themselves promoteit, explaintopeople thattheobjective istobring wealthtotheneighborhood.”

Manager–BancoTupinambá(PA)

“There’s very good acceptance of social currency in the community. Why?Because the social currencyis guaran-teed,there’safundbehindit.(...)Theydon’tfinditdifficult

toacceptsocialcurrency.Evenestablishmentsthatarenot registeredacceptit.”

Onthedifficultiesofmanagingpaper-basedsocialcurrency

Managersalsorecognizethat,despiteitsadvantagesforthe community,paper-basedsocialcurrenciespresentclear manage-mentdifficulties.Itisevidentfromtheinterviewsthatthefact thatthecurrencyispaper-basedhindersadoption:

Manager–BancoSertanejo(CE)

“Currentlywe’rehavingaproblemwiththesocialcurrency becauseofthematerialit’smadeof.It’snotthesocial cur-rencyitselfthat’srejected–it’sthematerial.”

Manager–BancoJuazeiro(EC)

“Thefactthatit’sasmallandfragilepieceofpapercauses distrust.(Theywanttoknow)howlongit’sgoingtobevalid for,orifsomeonekeepsitlockedawaysomewhere,whether they’llbeabletoexchangeitinthefuture?”

Manager–BancoPadreQuiliano(CE)

“Therewerepeoplewhosaid‘Oh,it’snotcoolbecause...the

perfectlyOKafterwards.SoIthinkthatthefewpeoplewho didn’tacceptitwasbecauseofthequality.”

Eventhecirculationofsocialcurrencyisseverely compro-misedbythepoorqualityofprintingonpaper:

Manager–BancoSertanejo(CE)

“WeexchangethecurrencyfortheReal,butwhenthe cus-tomerusedtoarriveatthemarkettodotheirshopping,the shopkeepercouldn’tpassonthecurrencyaschange–others wouldn’tacceptit.Why?Becauseofthematerial.Soatthe endoftheafternoon,theshopkeeperwouldcomeandchange the‘sabiá’(‘thrush’)–ourcurrency–backintoreaisagain.”

Manager–BancoTupinambá(PA)

“Oneofthedifficultieswefacewithbusinessesistheir pass-ing on the currency[as change], makingit circulate. The currencyreachestheestablishmentandfromthereitreturns tothecommunitybank.”

Manager–BancoTupinambá(PA)

“Making him understand that when he pays an employee partly in social currency then that currency stays within thecommunity.Makinghimunderstandthatwhenhegives the socialcurrencyas change, he’s sending it backtothe establishment.”

Onthedisseminationanduseofmobilephonesinthe communities

The widespreaduse of mobile phones,particularly smart-phones withInternet access,is an evidentreality eveninthe poorest communities (Teleco, 2015), like the ones in which therespondentslive.Theuseofgames,messagingandsocial networks has been positive for the dissemination of mobile devices:

Manager–BancoTupinambá(PA)

“Today,talkingisthelastthingyoudoonamobilephone. Peopleuseita lottosendmessages,the internetisuseda lot...peopleusemobilephoneinternetalot.”

Manager–BancoSertanejo(CE)

“Theyusetheinternet,games,textmessages...it’susedin

so manyways,somanymessages.Peopleuseitinagreat varietyofways,don’tthey?”

Manager–BancoOrquídea(SP)

“Todaywhatpeoplemostfocusonwiththemobilephonethat hasAndroid,allthoseapparatuses,istogoonFacebookand playgames.Weknowthatmobilephonesarecapableofmuch morethanthis.”

Onthepotentialofusingmobilephonesforpayments

Whenaskedabouthowtheyseetheuseofmobilephonesasa meansofpayment,intervieweeswereveryoptimisticregarding thepossibilityofadoption:

Manager–BancoOrquídea(SP)

“Itwouldbewonderful!Why?Becausethesepeople,instead ofhavingtocometothebanktopay,theycoulddothaton their phone. Seehow cool that is.That’s a breakthrough, that’sfantastic.”

Manager–BancoPauloFreire(SP)

“Ah, look, I think it wouldgo down well. It wouldmake yourlifeeasier.Insteadofwalkingaroundwithtwoorthree cards,youjusttakeyourphoneandmakeyourpayments.I thinkthey’dacceptthatwell.”

Manager–BancoTonato(SP)

“Nowadayswe’realwaysinarushright?Soif youcould makeapaymentoverthephone,andit’spossible,Ithinkthat wouldbegood.”

Onthepotentialforacceptanceofamobilephone-based socialcurrency

Intervieweeswerealsoclearlyoptimisticaboutthepossibility ofamobilephone-basedsocialcurrencybeingadopted, espe-ciallyifcommunitybanksbecomeleadersinthedissemination of thisinnovationthat turnsthe mobilephoneintoapayment instrument:

Manager–BancoLiberdade(AM)

“Ifwestart,ifthisideastartsoffinthecommunitybankand beginstospreadthroughthecityit’llbeagreatstepforward economicallyforthecommunityandthecityasawhole.”

Manager–BancoSertanejo(CE)

“Weliveinanageoftheconstantpursuit ofdiversityand innovation.That’sthewayIseeit: ifsomeoneturnsupin mytownpayingforthingsonthephoneforeverybodytosee, thatwillattractattention,morepeoplewilladheretoitand itwillexpandquickly.”

Manager–BancoTupinambá(PA)

“Ithinkwiththemobilephoneadoptionisgoingtobemuch fasterthanitwaswiththesocialcurrency,whichwasanew concept.Theyalreadyhavemobilephones!”

Manager–BancoTupinambá(PA)

“Theguaranteeisgoingtobethatthecreditwillenterthe person’sphone.Sowho’s itgoingtobe goodfor?It’ll be goodfor the store,that’s goingtosellmore. It’llbe good forthecommunitythat’sgoingtohaveresourcestobuythe thingsitneedsimmediatelyrightthere.”

Manager–BancoUniãoSampaio(SP)

“Ithinktheissueoftechnologytodayattractsalotofattention fromtheyoung.Whenyoushowthemthetechnology,they becomeinterested, and that’s often a means toget into a discussionaboutotherpoliticalissues,suchasthesolidarity economy.”

Manager–BancoEstrutural(DF)

wouldworkbetterthanhavingtogotothebanktogetthe currency.”

Manager–BancoTimbaúba(CE)

“The problem wouldn’t be convincing people touse it – the questionwouldbe whethertheir financial situationwouldbe goodenoughtohavecreditintheirphonestospend.”

Manager–BancoTupinambá(PA)

“Everybodyhasamobilephone,that’sawell-knownfact,so it’snotdifficult.Thecreditcardisnotsoeasytogetholdof, butamobilephoneis.Solet’ssayyoutalktoaconsumerin acommunitythathasacommunitybankandthatcommunity hasadifferentwayoflookingattheeconomy,becausethey haveatooltherethat’sdifferent.Andsoyoucomeinwitha newtoollikethisone,whichIalreadyhave,andIonlyneed toaddsomethingsoIcanuseit.Thisisveryinnovativeand Ibelievethatinourterritoryitwouldbehugelysuccessful.”

Manager–BancoSol(ES)

“Merchantsalwaystalkedalotabouthowthey’dliketohave aspecificcreditcard,oracurrencyorcardthatisdigitaland notjustthesocialcurrency.Commerceandmerchantswould likeitalot,andIbelieve,basedontheconversationswith theforum[themechanismbywhichthecommunitymanages thebank]thatconsumerswouldlikeittoo.”

Discussionoftheresults

Animportantaspectofthisstudyisourfocusonthe opin-ionsoftheparticipantsonthedemandside.Althoughwehave notconsideredcarryingoutanadoptionstudy,sinceatthetime weconductedourstudytherewerenoexperienceswitha suffi-cientlylonghistorytobeanalyzedfromthisperspective,wehave assessedthepotentialofamobile-baseddigitalsocialcurrency basedontheopinionsandviewsoflocalplayerswhowouldbe involvedinbuildingamodelofmobilepayments.Theopinions oftheselocalplayerswereregisteredthroughinterviewswith managersofcommunitybanks,whowereaskedtoevaluatethe potentialofmobilepaymentsthatincorporatethefunctionality ofsocialcurrency.

Consideringtherelativescarcityofcasesthatcombinesocial currenciesandmobilepaymenttechnologies,themanagers’ dis-course was very positive regarding the potential acceptance of a mobile phone-based social currency in their communi-ties. In a way, this contradicts the literature on technology adoption and, more specifically, on the adoption of mobile paymentsanddigitalcurrencies(Dahlbergetal.,2015; Liébana-Cabanillas, Sánchez-Fernández, & Mu˜noz-Leiva, 2014; Xin, Techatassanasoontorn,&Tan,2015),whichhighlightsadoption byvariousplayersintheecosystemasanimportantconstraint, especiallywhenitinvolvestechnologyinnovations.

Moreover, in the discourse of community bank managers there was no manifestation of their concern about possible difficultiesfor adopting or using thismodel in their commu-nitiesinthefuture,evenwhentheywereencouragedduringthe interviewstoconsiderthepotentialproblemsthattheadoption processmightface.Onthecontrary,theprevailingopinionwas

thattheintroductionofadigitalsocialcurrencycouldbequick andeasyandwouldcontributetosolvingexistingproblemsin themanagementofapaper-basedsocialcurrency.

Onethingallthesediscourseshaveincommonisthatthey illustrate atransformational view, as all thesemanagers start fromtheassumptionthatthemobilephonewillserveasameans ofpaymentforasocialcurrencywhoseprimaryfunctionisto transformanddevelopthecommunity.

Theviewistransformationalbecauseitmanagesto translit-erateconceptsthroughtheresignificationofwhatconstitutesa socialcurrencytowhatamobilephone-basedsocialcurrency mightmean,byinsertingideologicalandtransformational fac-tors. Managersof community banksrecombine andresignify theconceptsofsocialcurrencyandmobilephonepaymentsto createanewframeoftransformationalcollectiveactionofwhat amobilephone-basedsocialcurrencywouldbe.

To emphasizethecontributionofthisstudyas havingable toidentifyanewmeaningformobilepayments,wecanmakea comparisonwithMaurer’s(2012)work,inwhichitissuggested thattherearefourdistinctdiscoursesontheuseofmobilephones as ameansof payment.Maurer(2012)suggeststheexistence offourdiscoursesthatseekto“framethediscussion”ofmobile paymentsprojects.

ForMaurer(2012),thefirstdiscourseiscalledthe “Empower-mentStory”andisvoicedbythosewhoseemobilepaymentsasa waytoempowerthepoorwithmobiletechnologies.Thesecond discourse is calledthe “MarketShareStory”, whichemerges from the visionof those whowant toexpand the market for existingservicesonmobileplatforms.Thethirdisthe “Com-moditizedPaymentSpaceStory”,andarisesfromconcernabout theprofitabilitymadepossiblebysmalltransactionsgenerated bymobilepayments.Thefourthdiscourseisthe“TulipStory”, fromthosewhobelievethatthereissomeexaggerationregarding theadoptionofmobilepayments,whichisprobablylikelyonly tooccur atsomepointinthefuture. Althoughthe analysisis grounded inothermethodologicalstrategies, thesediscourses were identified fromalogicthat thisarticlecalled“framing” becauseitaimsto“frame”thediscussiononmobilepayments projects.

Noneofthesefourdiscourses,however,incorporatestheidea ofsocialcurrencythatwasinvestigatedinthestudypresented inthisarticle.Thisnewdiscourse,whichcanbegatheredfrom the interviews withcommunitybank managers,identifies the resignificationofwhatmobilepaymentscanbewhencombined withatransformationallogicaimedatcreatingsocialoutcomes notonlylinkedtotheireconomiccharacteristics,butalsotothe logicofthesolidarityeconomyincorporatedintothepracticeof communitybanks.Table2showsthefourdiscoursespresented byMaurer(2012)withrespecttomobilepayments,plusafifth discourse–thatofthecommunitybankmanagers.

Table2

Framingofdiscoursesonmobilepayments. Discoursesonmobile

payments

Description

Empowermentstorya Mobilepaymentsallowthepooresttohave

accesstomoneyandcapital,leveragingthe tremendouspenetrationofmobilephonesin developingcountriesvs.therelativelylow penetrationoffinancialservicesinthese countries

Marketsharestorya Mobilepaymentscanreconfigurethemoney transfermarkettoprovidefinancialaccesstoall, expandingthemarketbyincludingthoseatthe baseofthepyramid

Commoditized paymentspace storya

Focusesonchangingthebusinessmodelto fee-basedfinancialservicesand

telecommunications,takingadvantageofthe factthatmillionsofpoorpeoplearoundthe worldperformvarioussmalloperationsdaily Tulipstorya Viewthatsomeplayersholdwherebymobile

paymentsarejusta“fad”thatisunsustainable bothintermsofprofitabilityandintermsof povertyalleviation

Transformational collectiveaction (newdiscourse identifiedamong communitybank managers)

Thediscourseofcommunitybankmanagers,but adding‘socialcurrency’asatransformational factorto‘mobilepayments’,givingnew meaningtobothconcepts

a Source:AdaptedfromMaurer(2012).

meaningtothediscourseofdigitalsocialcurrenciesinsucha waythatthelatterfitintoatransformationalframethatfavors theiruseforlocaldevelopment.

Theinterviewedleadershighlighttheroleofsocialcurrency inthe localdevelopmentoftheir communities,as wellas the work carried out by community banks for its dissemination andacceptanceamongresidentsandmerchants intheir com-munities.However,theyalsorecognizethattheuseofprinted paper-basedsocial currency creates several operational prob-lemssuchashighcostofissuance,lowdurabilityoftheprinted bills, billmisplacement andtheft,besides allthe other trans-actional costs involved in the management and supply of a physicalmeansofpayment.Accordingtothem,theseproblems ofpaper-basedsocialcurrencieslimittheirfunctionasameans ofpaymentandtherebyreducetheirpowertotransformlocal economies.

However,accordingtotheinterviewees,amajorproblemof socialcurrencyrelatestoitsphysicalmedium.Papernotesare expensive,spoilquickly–resultinginahighreplacementcost –canbelostorstolen,needtobeproducedbyspecialized prin-terswithsafeguardsagainstcounterfeiting,requiresophisticated laborandlogisticstodistributedifferentamountsofthevarious notesofdifferentface-value(e.g.2,5,10),amongother prob-lems faced bymanagers of communitybanks. Managingthe supplyofaphysicalmeansofpaymentresultsinhighoperating costs.Moreover,being physicalnotes, theylackthe scalabil-ityofvirtualmoney,asthereisinanormalbankaccount,for instance.Digitalcurrenciesalsowouldallowforimprovements

increditmanagement,basedoninformationonthecirculation ofthemoneyamongpeopleandwithinthateconomy.

Despitethesedifficulties,theseleadersexpressedtheir con-fidenceinthesocialcurrencymodelandbelievethatadigital version,particularlyifimplementedviamobilephone,couldbe animprovement,reducingsomeoftheproblemsthatoccurwith theprintedversion.Thus,thesemobiledeviceswouldfunction asadigitalsocialcurrency,allowingboththetransferofmoney from peopletopeople(P2P) as wellas thepayment of bills, transfersfrominstitutionstopeople,suchasfromthe commu-nity bankitself toits customers(B2P), or fromcustomersto localstores(P2B).

Thediscoursesoftheinterviewedleadersreinforcetheneed toimplementadigitalsocialcurrencymodelthatmakessense intheircommunitiesand,unusuallyforinnovationsinvolving relevanttechnologicalleaps(Dahlbergetal.,2015),theyfavor theinclusionofthecurrentmodeltothemobilephoneplatform. When assigning newidentities andmeanings to thisconcept of digitalsocialcurrency,theypointtoanalternativethat has notyetbeenconsideredbyotheractors,whohavebeenunable tofindaviablemodelfortheeconomicinclusionofBrazilian low-incomegroupsviamobilepayments.

Itisalsoworthnotingtheabsence,intheinterviewees’ dis-courses,ofconcernaboutpossiblerestrictionsandproblemsthat couldarisewiththistypeoftechnologicalsolution,afactthat mayalsoreflectalackofexperienceofthesemanagersinthis subject andtechnology, inaddition tothe absence of amore concretebusinessmodelandtechnologysolution thatpermits amoretangibleassessment oftheprosandconsof this inno-vation.Identifyingthisinitialacceptance,however,showsthere isbothpotentialdemandand,importantly,non-rejectionwithin anypossibleadoptionandintroductionprocess.

Asmobilephonesarewidelyusedinthepoorcommunities inwhichcommunitybanksarelocated,accordingtothe inter-viewedmanagers, potentialusersalreadyseemtobe familiar with a wide variety of mobileapplications, which facilitates theadoptionof newfunctionalities,aswouldbethecaseofa paymentapporpaymentcommandsonthedevice.Interviewees saidtheyweresupportive of theconcept of mobilepayments and,although theystill donothaveaclearideaofhowtogo aboutitandofthepossibledifficulties,theyapproveofmigrating fromthecurrentmodelofsocialcurrencytoamobilepayment platform.

Aninterestingpointthatcanbeseenfromtheinterviewsis the very confident discourse regardingthe potential adoption ofmobilepaymentsingeneral,andofdigitalsocialcurrencies inparticular within their communities. Even thoughthey are unfamiliarwiththesubjectbecauseitisimmaterialtothemand notsupportedbyanyconcreteexample,whenquestionedabout thepossibilityofsuchamobilepaymentsystembeingadopted, their discoursehasclearsignsof transformational resignifica-tion,appropriationandofthecreationofitsownidentityforthis digitalsocialcurrencymodel.

representdifferentregionsofthecountryandhavearelatively largeuser-base,inordertohaveatransformationalcollective action,wouldbetoallowtheuseofadigitalsocialcurrencythat wasatthesametimecommontobanksintermsof infrastruc-ture,andthat wouldpossiblyenableexchangesandsynergies betweenthedifferentcommunities,without,ofcourse,giving uptheirlocalcirculationcharacter,buthaving lower manage-mentcostsandaneasierandpossiblyintegrated,moneysupply management.

In parallel,the use of mobilepayments as adigital social currencywouldenablethecreationofadatabasewitharecord offinancialtransactionsandpatternsofspendingthatwouldbe largerandmorepracticalthananythatexisttodayforthe man-agersofcommunitybanks,enablingmoresophisticatedlending andriskmanagement,besidescreatinganunderstandingof com-munitymoneyflowsthatwouldpermitproductioncredittofocus evenmoreonmeetingthedemandsofthepopulation.Thiscould enableflexiblecreditofferings,evenfromformalfinancial insti-tutions,aswellasotherfinancialservicessuchassavingsand insurance,giventheaccesstofinancialinformationonspending andconsumption.

Finalconsiderations

Thisstudyevaluatedthepotentialofamobilesocialcurrency from theperspective of the managers of someof the leading communitybanksinBrazil,inadditiontoobservinghowthis technologycanbeappropriatedandredefinedintheirdiscourse inordertoprovideanalternativetotheclassicmechanismsfor financialinclusion.

The studyalso allowsonetospeculateonthe transforma-tionalpotentialandthepositiveoutlookregardingthecoupling ofamobilepaymentsplatformwithasocialcurrencysystemand suggeststhatfurtherresearchbedoneinordertobetter under-standadoptionfactorsandpossiblemodelsforimplementation ofmobilepaymentprojectsforfinancialinclusion.

The theoretical model used – collective transformational framing–asproposedbyBenfordandSnow(2000),allowedus tocapturetheessenceoftheinterviewedmanagers’discourses, focusingonhowtheyconstructedmeaningwithinthecollective actionlogicofthesocialmovementstowhichtheybelong.The choiceofthistheoreticalmodelwasalsoappropriatebecausewe aredealingwithanobject,digitalsocialcurrency,whichdoes not actuallyexist andwhoseanalysis could onlybecaptured throughaconceptuallensthatcouldidentifytheelementsthat areonlyintheimaginationofthoseinterviewed.

Thecontributionsof the studypresented inthisarticleare oftwo categories.Thefirst,ofatheoreticalnature,istohave employedamodel thathadnotyetbeenappliedtostudiesof mobilepaymentsorsocialcurrencies.AsstatedbyBenfordand Snow(2012:615),framesofcollectiveactionaredesignedtobe usedtosharetheunderstandingofsituationsthatareproblematic and“inneedofchange”.Usedasaninstrumentforalternatives tocreatemobilizationconditions,thisconceptwasusedinthis studyasatooltopromotereflectionontheadoptionofatoolthat hasapotentialchangeimpact.Inthisrespect,therefore,thereis

somedegreeoftheoreticalinnovationinthewayweappliedit here.

The secondcontributionis ofapractical nature.This con-tribution allows us toevaluate the degree of opennessto the digitalsocialcurrencymodelbymanagersofcommunitybanks, whoalreadyoperatewithapaper-basedsocialcurrency.Upon hearingthestatementscollectedintheinterviews,itis impos-sible toreach anythingotherthanafavorableviewregarding initiatives topromoteexperimentswithamobilephone-based digital social currency.Of course,onlypractical experiments willallowustohaveaclearassessmentoftherealpotentialof thismodel.

Limitationsofthisstudy,whileimportant,donotinvalidate its exploratory nature. First, we interviewed only one group of players among the several who should be involved in a real deployment process.Although the managers of commu-nity banksareagroupofcritical importance,itisimpossible to form acomplete opinion of the model’s potential without hearingotherstakeholders,especiallycustomersandmerchants – the usersof thismodel;andcompaniesthat would provide the technical support for the operationalinfrastructure of the digitalsocialcurrency,aswellascardandmobileoperators– externalagentsthatcouldinfluencetheimplementationprocess. Anotherpossiblelimitationisthatdatacollectionwasthrough spontaneousinterviewsduringaneventthatinvolvedthe pres-enceofmorethanonehundredcommunitybanks.Apparently, thosewhovolunteeredtoparticipateintheinterviewswerethe managers ofthemostactivecommunitybanks,withthemost extensivecasesofsocialcurrencyimplementation.Itisknown that therearemanyothercommunitybanks(ourinterviewees representonlyabout15%oftheentirepopulation)andwe can-nottellwhetherthosewhowereleftoutsharetheviewsofthose whowereinterviewed.

Futurestudiesrelatedtothissubjectcouldinvolvetheplayers absentfromthisstudy,butcouldalsofurtherexpandthe con-ceptsinvolvedinthediscussionoftheadoptionofdigitalsocial currencies,employingtheoriesandconceptualapproachesthat couldprovideabroaderviewofthisprocess,whichisinevitably verycomplexandrequiresthecoordinationofplayerswithvery diverseinterests.Oneaspect thatshouldnotbeoverlookedin futurestudiesisthediscussionofhowmobilephone-based dig-italsocialcurrencieswill(orwillnot)succeedinmaintaining thecharacteroffinancialinclusionandlocaldevelopmentthat seemobviousintheirpaper-basedversions.

Conflictsofinterest

Theauthorsdeclarenoconflictsofinterest.

References

Albuquerque,J.P.,Diniz,E.H.,&Cernev,A.K.(2014).Mobilepayments:A scopingstudyoftheliteratureandissuesforfutureresearch.Information

Development,http://dx.doi.org/10.1177/0266666914557338

Bader, M., & Savoia, J.R. F. (2013). The logistics of banking distribu-tion:Trends,opportunitiesandfactorsforfinancialinclusion.Revistade

Administra¸cão de Empresas, 53(2), 208–215. http://dx.doi.org/10.1590/

Benford,R.D.,&Snow,D.A.(2000).Framingprocessesandsocialmovements: Anoverviewandassessment.AnnualReviewofSociology,26,611–639. Retrievedfromhttp://www.jstor.org/stable/223459

Blanc,J.(2006).Lesmonnaiessociales:unoutiletseslimites.Introduction générale.InJ.Blanc(Ed.),Exclusionetliensfinanciers:Monnaiessociales,

rapport2005–2006(pp.11–23).Paris,France:Economica.Retrievedfrom

https://halshs.archives-ouvertes.fr/halshs-00085784

Cappelle, M. C.A., Melo, M. C.D. O.L., & Gonc¸alves, C. A.(2011). Análisedeconteúdoeanálisedediscursonasciênciassociais.Organiza¸cões

Rurais&Agroindustriais,5(1).Retrievedfromhttp://revista.dae.ufla.br/

index.php/ora/article/download/251/248

Chandy,L.,Dervis,K.,&Rocker,S.(2012).Clicksintobricks,technologyinto transformation,andthefightagainstpoverty.InBrookingsblumroundtable onglobalpoverty.Aspen,CO:BrookingsInstitution.

Dahlberg,T.,Guo,J.,&Ondrus,J.(2015).Acriticalreviewofmobilepayment research.ElectronicCommerceResearchandApplications,14(5),265–284.

http://dx.doi.org/10.1016/j.elerap.2015.07.006

Dancey,K.(2013).Whypaymentsystemsmattertofinancialinclusion: Examin-ingtheroleofsocialcashtransfers.JournalofPaymentsStrategy&Systems,

7(2),119–124.

Davis,F.D.(1989).Perceivedusefulness,perceivedeaseofuse, anduser acceptance of information technology. MIS Quarterly, 13(3),319–340.

http://dx.doi.org/10.2307/249008

Diniz,E.H.,Cernev,A.K.,&Albuquerque,J.P.(2013).Mobileplatformfor financialinclusion:ThecaseofanunsuccessfulpilotprojectinBrazilSIG GlobDevSixthAnnualWorkshop.Milan,Italy:AssociationforInformation Systems.

Duncombe,R.,&Boateng,R.(2009).Mobilephonesandfinancialservices indevelopingcountries:Areviewofconcepts,methods,issues,evidence andfutureresearchdirections.ThirdWorldQuarterly,30(7),1237–1258.

http://dx.doi.org/10.1080/01436590903134882

Franc¸a Filho, G. C. D. (2004). A problemática da economia solidária: um novo modo de gestão pública? Cadernos EBAPE.BR, 2(1), 1–18.

http://dx.doi.org/10.1590/S1679-39512004000100004

Freire,M.(2013).Aimportânciadosbancoscomunitáriosparaainclusão finan-ceira.InInstitutoPalmas,&NESOL-USP(Eds.),BancoPalmas15anos: resistindoeinovando(pp.41–60).SãoPaulo,Brazil:A9Editora.

Gamson,W.A.,Fireman,B.,&Rytina,S.(1982).Encounterswithunjust authority.Homewood,IL:DorseyPress.

Garcia,D.B.(2012).Acontextualizac¸ãoteóricadeBancosComunitáriosde Desenvolvimento.TemasdeAdministra¸cãoPública,4(7).

Goffman,E.(1974).Frameanalysis:Anessayontheorganizationofexperience. Cambridge,MA,US:HarvardUniversityPress.

ITU.(2013).Key2006-2013ICTdatafortheworld,bygeographicregions

andbylevelofdevelopment,forthefollowingindicators..Retrievedfrom

http://www.itu.int/en/ITU-D/Statistics/Documents/statistics/2013/ITU Key2005-2013ICTdata.xls

Jack, W., & Suri, T. (2011). Mobile money: The economics of M-PESA

(WorkingPaper No. 16721). National Bureau of Economic Research.

http://dx.doi.org/10.3386/w16721

Jayo,M., Pozzebon, M.,& Diniz, E. H.(2009). Microcredit and innova-tivelocaldevelopment inFortaleza,Brazil:ThecaseofBancoPalmas.

CanadianJournalofRegionalScience,32(1),115–128.Retrievedfrom

http://www.cjrs-rcsr.org/archives/32-1/Jayo.pdf

Johnston,H.(2002).Verificationandproofinframeanddiscourseanalysis. InB.Klandermans,&S.Staggenborg(Eds.),Methodsofsocialmovement research(pp.62–91).Minneapolis,MN:UniversityofMinnesotaPress.

Liébana-Cabanillas, F., Sánchez-Fernández,J., & Mu˜noz-Leiva, F. (2014). Antecedents oftheadoption ofthenewmobile payment systems:The moderatingeffectofage.ComputersinHumanBehavior,35,464–478.

http://dx.doi.org/10.1016/j.chb.2014.03.022

Lietaer,B.,&Primavera,H.(2013).Moedascomplementares,bancos comu-nitários e o futuro que podemos construir. In Instituto Palmas, & NESOL-USP(Eds.),BancoPalmas15anos:resistindoeinovando(pp. 61–74).SãoPaulo,Brazil:A9Editora.

Mas,I.,&Morawczynski,O.(2009).Designingmobilemoneyserviceslessons fromM-PESA.Innovations:Technology,Governance,Globalization,4(2), 77–91.http://dx.doi.org/10.1162/itgg.2009.4.2.77

Mas,I.,&Radcliffe,D.(2010).Mobilepaymentsgoviral:M-PESAinKenya.

Capco Institute’s Journal of Financial Transformation, (32), 169–182.

Retrievedfromhttp://ssrn.com/abstract=1593388

Maurer,B.(2012).Mobilemoney:Communication,consumptionandchangein thepaymentsspace.TheJournalofDevelopmentStudies,48(5),589–604.

http://dx.doi.org/10.1080/00220388.2011.621944

Michel, A., & Hudon, M. (2015). Community currencies and sustainable development:Asystematicreview.EcologicalEconomics,116,160–171.

http://dx.doi.org/10.1016/j.ecolecon.2015.04.023

Neiva,A.,Nakagawa,C. T.,Tsukumo, D.J.,Braz,J.B.,Silva,R. M.,& Mascarenhas,T.S.(2013).BancoPalmas:resultadosparao desenvolvi-mentocomunitárioeainclusãofinanceiraebancária.InInstitutoPalmas, &NESOL-USP(Eds.),BancoPalmas15anos:resistindoeinovando(pp. 105–178).SãoPaulo,Brazil:A9Editora.

Prahalad,C.K.,&Hammond,A.(2002).Servingtheworld’spoor,profitably.

HarvardBusinessReview,80(9),48–59.

Ramada-Sarasola, M. (2012). Can mobile money systems have a

mea-surable impacton local development? (n.p.). http://dx.doi.org/10.2139/

ssrn.2061526

Schierz, P. G., Schilke, O., & Wirtz, B. W. (2010). Understanding consumer acceptance of mobile payment services: Anempirical anal-ysis. Electronic Commerce Research and Applications, 9(3), 209–216.

http://dx.doi.org/10.1016/j.elerap.2009.07.005

Schulze, L. (2014). The three billion new middle-class opportunity: The successes and technical challenges of mobile financial services in emerging markets. Journal of Payments Strategy & Systems, 8(3), 235–245.

Singer,P.(2009).Finan¸cassolidáriasemoedasocial.Projetoinclusão finan-ceira.pp.69–78.Brasília,Brazil:BancoCentraldoBrasil.

Siqueira,A.C.O.,Mariano,S.R.H.,&Moraes,J.(2014).Supportinginnovation ecosystemswithmicrofinance:EvidencefromBrazilandimplicationsfor socialentrepreneurship.JournalofSocialEntrepreneurship,5(3),318–338.

http://dx.doi.org/10.1080/19420676.2014.927388

Snow, D. A.,Rochford, E. B., Worden,S.K., & Benford, R.D. (1986). Frame alignment processes, micromobilization, and movement partici-pation. American SociologicalReview, 51(4),464–481. Retrieved from

http://www.jstor.org/stable/2095581

Snow,D.A.,&Benford,R.D.(1988).Ideology,frameresonance,andparticipant mobilization.InternationalSocialMovementResearch,1(1),197–217.

Snow,D.A.,Soule,S.A.,&Kriesi,H.(Eds.).(2008).TheBlackwellcompanion tosocialmovements.Oxford,England:JohnWiley&Sons.

Teleco. (2015). América Latina: estatísticas de celular.. Retrieved from

http://www.teleco.com.br/pais/alatinacel.asp

Xin,H.,Techatassanasoontorn,A.A.,&Tan,F.B.(2015).Antecedentsof con-sumertrustinmobilepaymentadoption.JournalofComputerInformation