Vol-7, Special Issue-Number5, 2016, pp1413-1424 http://www.bipublication.com

Research Article

Effect of internal factors of a company on decisions of capital structure of the

companies accepted at Tehran stock exchange

Keyvan Farahzad Touli1 and Azim Aslani2

1Department of Accounting, Rasht Branch,

Islamic Azad University, Rasht, Iran ([email protected]) 2Department of Accounting, Lahijan Branch,

Islamic Azad University, Rasht, Iran ([email protected])

Corresponding Author: [email protected]

ABSTRACT

Decision making about capital structure was one of the most challenging problem for companies but it is the most vital decision about continuing their life. Different studies show that capital structure of companies has determining role at decisions of investment. In this research effect of internal factors of a company on decisions of capital structure of companies accepted at Tehran stock exchange has been studied. This research regarding classification of research is applied based on the goal and regarding data collection it is descriptive research. For data collection field method and information bank of new strategy and fiscal statement of companies like balance sheet and profit and loss statement has been used as tools of research. Descriptive statistics method of this research based on statistics of tendency to the center and inferential statistics is based on panel data. Statistical society of research is all companies accepted at Iran stock exchange that 112 companies were chosen regarding limitations of research for testing hypothesis of research. In order to consider the effect of independent variable on dependent variable two hypotheses were tested. For data analysis software of Views version 9 was used. Consideration of the effect of independent variable on dependent variables showed that there is meaningful relationship between internal factors of a company and ratio of short-term and long-term debts.

Keywords:capital structure, long-term debt, short-term debt, internal factors of a company

INTRODUCTION

The most important and effective factor at economic development and social welfare is capital; by making and developing capital markets, economic cycles of any society is working and lead to economic promotion. In this direction development of stock exchange market and active presence of experts and financial analyzers in this market is preceding factor at mechanism of devoting efficient capital and economic promotion in the country. Undoubtedly

main anxiety of managers. It can be said that one way of decreasing conflict between benefits of owners and managers is using structure of optimized capital that increases company’s value (Abbaszadeh and Rigi, 2010). The main goal of companies’ management is maximizing wealth of stockholders in corporation. Financial decisions of management for improving financial situation of a company is important but unaware decisions can lead to company’s failure(Hejazi and Khademi, 2013).

Decisions of financial supply and investment in companies are decisions that are made by foresight. In financial decisions company uses considered payment to be able to do his commitment against suppliers of financial resources in future (Nazaripour et al, 2010). Significant differences among capital structure of active companies exist at different industries. Due to existence of some effective factors on decisions related to capital structure of a company, judgment by a person that determines capital structure can have important role. Regarding resources of financial supply companies have different risk and output about markets of capital supply. Therefore decisions related to capital structure will have more effective factor at efficiency and credit of companies by suppliers of capital (Ghasemi, 2009).

The most important goal of policies of demining capital structure is distinguishing optimized combination of financial resources for maximizing wealth of stockholders. In this direction awareness of market situation and companies at making policy of capital structure can be proper guidance for managers and other economic decision-makers (Rohi et al, 2014). Because capital structure is as an important variable for relatedness accountinginformation (Ebrahimi et al, 2014). Information of capital structure can be a fundamental factor at decisions pf investors that may be affected by different factors (Moradi et al, 2013). Discussion of capital structure points the way f combining financial supply resources of a company such as short-term debt, bonds, log-term

capital in structure of their capital depends on different factors such as corporate features, economy, viewpoint and goals of managers. Therefore managers are forced to use different factors such as economic factors and corporate features while making decision about optimized combination of capital structure and should pay attention to decisions related to financial supply and effects that these factors have on capital structure. Also financial managers for making proper financial structure should consider internal features of company and regarding these variables maximize company’s value(Baral,2004). Identification of effective factors at choosing capital structure, regarding different variables and conditions helps managers at decision-making about choosing proper capital structure and gives useful information to them (Ahmadpour et al, 2013). Internal factors like ratio of short-term and long-term debt, output of assets and output of equities, fixed assets, size of company,liquidity, company’s risk, financial flexibility and tax shield of depreciation expense affect decisions of capital structure(cekrezi, 2015). In this direction this research is going to show a number of these effective factors on capital structure that 8 internal factors including output of assets, equity, fixed assets, size of company, liquidity, company’s risk, financial flexibility and tax shield of depreciation expense that is expected to affect decisions of capital structure are chosen and their relationship with two ratio of short-term debts and long-term debts that have been seemed as index of assessment of decisions of capital structure are considered and tested that doing this action conforms the main problem of research. Therefore the main question of research has been identified as:

*how is effect of internal factors of companies on decisions of capital structures of companies?

Theoretical framework and the way of measurement

In current research, output of assets, return on equity, fixed assets, liquidity , company’s risk ,financial flexibility and tax shield of depreciation

expense are considered as the internal factor of company and conform independent variables of research. Dependent variable is decisions of capital structure that for its assessment two ratio of short-term debt and long-term debts have been used. Total model of research for testing hypothesis are as below (cekrezi 2015):

Levit =β0 + ß1ROAit + ß2ROEit+ ß3TANGit +

ß4SIZEit + ß5LIQit + β6RISKit + ß7FLEXit +

ß8NDTSHit+εit

In above model, dependent variable is decision of capital structure that for measuring it financial leverage index has been used(Levit). For

measuring financial leverage two ratio of short-term debt and long-short-term debt will be used. Therefore total model of research is considered in the form of two models. In current research variables of asset output, return on equity, fixed assets, liquidity , company’s risk ,financial flexibility and tax shield of depreciation expense are used as internal factors of a company that for considering the effect of these factors on ratio of short-term debt, regression model(1-1) is used that indicates that effect of asset output, return on equity, fixed assets, liquidity , company’s risk ,financial flexibility and tax shield of depreciation expense on short-term debts(cerkrezi2015): Model(1-1)

SDTAit =β0 + ß1ROAit + ß2ROEit+ ß3TANGit +

ß4SIZEit + ß5LIQit + β6RISKit + ß7FLEXit +

ß8NDTSHit+εit

Ratio of short-term debt=SDTAit

asset output=ROAit

return on equity=ROEit

fixed asset=TANGit

size of company=SIZEit

liquidity=LIQit

company’s risk=RISKit

financial flexibility=FLEXit

tax shield of depreciation expense(non-debt)=NDTSHit

3=β4= β5=β6=β7=β8β2=β1= =βregression

coeficient

ε =standard estimation

In the fallowing the way of measurement of variables of model are presented:

*ratio of short-term debts

Ratio of short-term debt is one index of measuring financial leverage. Financial leverage shows the subject that which part of assets has been supplied by debts and equity. In this research variable of ratio of short-term debt is calculated through total division of short-term debt on total assets(cekrezi, 2015).

*ratio of long-term debt

Ratio of long-term debt is one index of measuring financial leverage. Financial leverage shows the subject that which part of asset has been supplied by debts or equity financially. In this research ratio of long-term debt are achieved through division of total long-term debt on total assets (the same source).

*output of assets

Output of an asset is about efficient management in relationship with using assets, in the direction of profit production that is calculated through annual profit to company’s asset. Output of asset measures ability of a company in creating profit in relationship with total investment in company(Abu-Rub, 2012). In this research output of assets has been considered as index of measurement. Asset output is achieved through division og net profit after tax on total asset(cekrezi, 2015).

*output of equity

Output of equity denotes the subject that who much output is created through investors for investment by them. In this research output of equities is achieved through division of net profit after tax on total equity(the same source).

*fixed assets

Fixed assets are in fact assets that have been bought through companies with the goal of application for a period of time longer than a year since the time of buying. Fixed assets don’t have reselling intention at normal period of trade or

buying and selling. Fixed assets by cycle of useful and limited life will lose their value gradually because of age condition, covering or condition of market. Therefore companies need distinguishing loosing value of their fixed assets along their useful life cycle (Tay, 2009). In current research for calculating variable of fixed assets, we divide fixed assets on total assets(cekrezi, 2015).

*size of company

Size of company is used as a factor of degree of available information that means information of great companies more than small companies (Lin et al, 2015). In this research the aim of size of company is natural logarithm of total asset of company(cekrezi, 2015).

*liquidity

Liquidity shows the ability of a company at doing short-term commitments. In other word liquidity is the relationship between cash that is given to the company in short-term and the cash that a company will need it(Ghadri et al, 2014). In this research variable of liquidity is achieved through division of current assets on current debts(cekrezi, 2015).

*company’s risk

Risk shows the type of failure for achieving goals and is counted a determiner in the direction of profitability’s of companies of financialinstitutes(yurdakul, 2014). In this research variable of company’s risk is achieved through division of standard deviation of profit before deduction of interest and tax on average profit before interest and tax(cekrezi, 2015).

*financial flexibility

Financial flexibility means power of private unit at supplying cash at short time of receiving information about predicted financial needs or finding proper opportunity for investment(Yung et al, 2015) like cash, short-term investment, business receiving bills, business receiving documents(cekrezi ,2015).

*Tax shield of depreciation expense

goal of determining and direction of move of a company is set toward it that this ratio is determined through creating a kind of balance among benefits resulted from tax shield and cost of bankruptcy (Khaleghimoghaddam and Baghavian, 2006). Variable of tax shield is achieved through division of cost of depreciation of visible and invisible assets on total assets of company(cekrezi ,201).

Research hypothesis

Based on research model, two hypotheses exist regarding cause relationship between model’s variable. These two hypotheses are as below: H1: there is meaningful relationship between internal factors of a company and ration of short-term debt.

H2: there is meaningful relationship between internal factors of a company and ratio of long-term debts.

Method of research and data analysis

Current research is counted applied research regarding classification of research. The goal of applied research is achieving perception or necessary knowledge for determining a tool through which a distinguished need is met.current research s descriptive one regarding classification of research based on the way of data collection that describes features of sample and then generalize these features to the statistical society. Descriptive research includes a set of methods that their goal is describing considering conditions or phenomenon. For data collection field method and new strategy database and fiscal statement of companies like balance sheet and profit and loss statements have been used as tool. Descriptive statistic method of this research is based on statistics of tendency to the center and inferential statistics based on panel data. For data analysis firstly degree of each variable was distinguished based on fiscal statement and then information were described and hypothesis were tested and finally by collecting and data analysis they were ended. Data analysis was done through Eviewl 9

software. Studying statistical society of this research are all companies accepted at Iran stock exchange in studying years by studied conditions. For determining considering samples in this research, regarding number of considering companies, type of their activities and their different sizes is used through systematic omit ionmethod(screening techniques). It means that conditions are defined for convergence of statistical society and some companies were seemed as part of research samples that have had mentioned conditions. Among all considering companies, companies that have had all fallowing conditions during 2009-2013 are considered as sample.

1- Since 2009 be accepted at stock exchange. 2- Required information for research variable in

those companies is available during research period.

3- Not to be part of service companies, financial supply and investment because these companies have capital structure different from other productive companies.

4- Interaction of stock of companies during studying year doesn’t have interaction succession.

5- Fiscal year of the company ends to feb and company don’t change its fiscal year during studding period.

6- Not to be damaging company

7- By acting all above limitations, sample volume of 112 companies during 2009-201(560 companies) are considered as studying samples of this research. Of course this point is necessary that these samples were chosen among 453 companies. For data analysis two statistics have been used:

-index of central distribution like mean, frequency, standard deviation,..are used for describing research variable.

as self-correlation function test is used. For implementing model and testing hypothesisEview version 9 is used.

Testing hypothesis and research findings

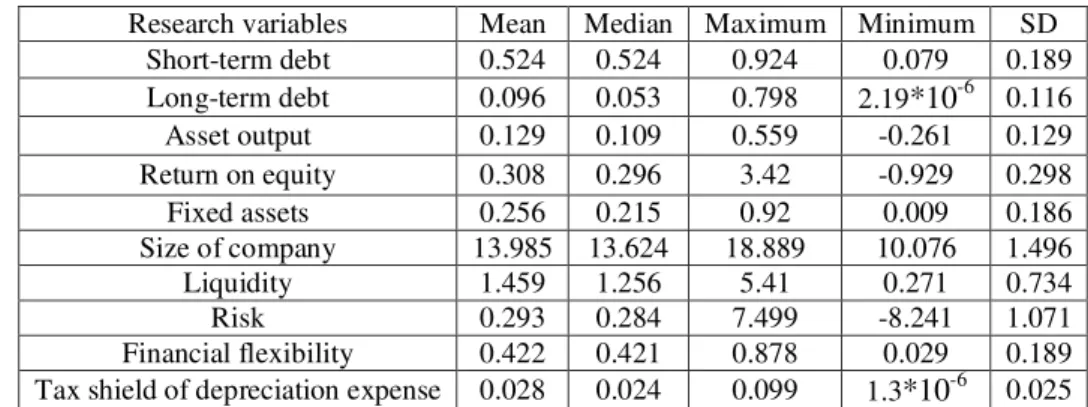

Considering sample during time range of 2009-2013 includes 112 companies. I this section, mean, median (central criteria), standard

deviation, maximum and minimum (dispersion criteria) of used variables were calculated and were mentioned in table 1. It is necessary to mention that after deleting data and ordering them, number of companies-years of variables of research hasfaced little reduction.

Table 1: Descriptive index of studying variable

Research variables Mean Median Maximum Minimum SD

Short-term debt 0.524 0.524 0.924 0.079 0.189

Long-term debt 0.096 0.053 0.798 2.19*10 -6 0.116

Asset output 0.129 0.109 0.559 -0.261 0.129

Return on equity 0.308 0.296 3.42 -0.929 0.298

Fixed assets 0.256 0.215 0.92 0.009 0.186

Size of company 13.985 13.624 18.889 10.076 1.496

Liquidity 1.459 1.256 5.41 0.271 0.734

Risk 0.293 0.284 7.499 -8.241 1.071

Financial flexibility 0.422 0.421 0.878 0.029 0.189

Tax shield of depreciation expense 0.028 0.024 0.099 1.3*10 -6 0.025

Testing normality of dependent variables

Jarak-Bara test has been used for consideration of normality of dependent variables. Result of this test has been presented in table 2. Based on this test because sig is bigger than 0.05, distribution of dependent variables is normal.

Table 2: Jarakbara test

Variable Jarakbara test Sig

Short-term debt 1.3648 0.096

Long-term debt 1.1236 0.108

Considering reliability of variables

Fore data analysis, reliability of variables should be considered. Reliability of research variables is mean and variance of variables along time and covariance of variables between different years was fixed. Therefore using these variables in the model don’t cause creation of spurious regression. It means we can use tests like Lovin, Lin and Chu, I’m, pesaran and Shin and diki-foler test. For doing the analysis im, pesaran and Shin test are used. Result of this test has been presented in table 3.

Table3: Results of Reliability test

Variables T statistics Sig

Short-term debt -10.898 0.000

Long-term debt -10.968 0.000

Asset output -12.872 0.000

Return on equity -15.551 0.000

Fixed asset -9.067 0.000

Size of company -9.904 0.000

Liquidity -13.196 0.000

Risk -23.206 0.000

Financial flexibility -12.311 0.000

Tax shield of depreciation expense -10.112 0.000

Regarding table 3 amount of sig of research variables is less than 5% and so all variables in considering period are reliable. Then identification of proper method for data analysis is done.

In the direction of estimating coefficient of model related to testing first hypothesis firstly for determining method of combined data and distinguishing convergence or inconvergence of them chao test and F-limerstatistics are used. Result of this test has been mentioned in table 4.

Table 4: Result of chao test

Null hypothesis F statistic Sig Result of chao test

Using combined data model 11.279 0.000 Null hypothesis is rejected

According to what is seen in table 4, result of chao test shows that obtained probability for f statistic is less than 5%, so for testing this model data are used as board. In the fallowing in table 5 by Houseman test necessity of using method of fixed or random effect is considered.

Table 5: Result of human test

Null hypothesis Chi-square test Sig Result

Using random effect model 33.854 0.000 Null hypothesis is rejected

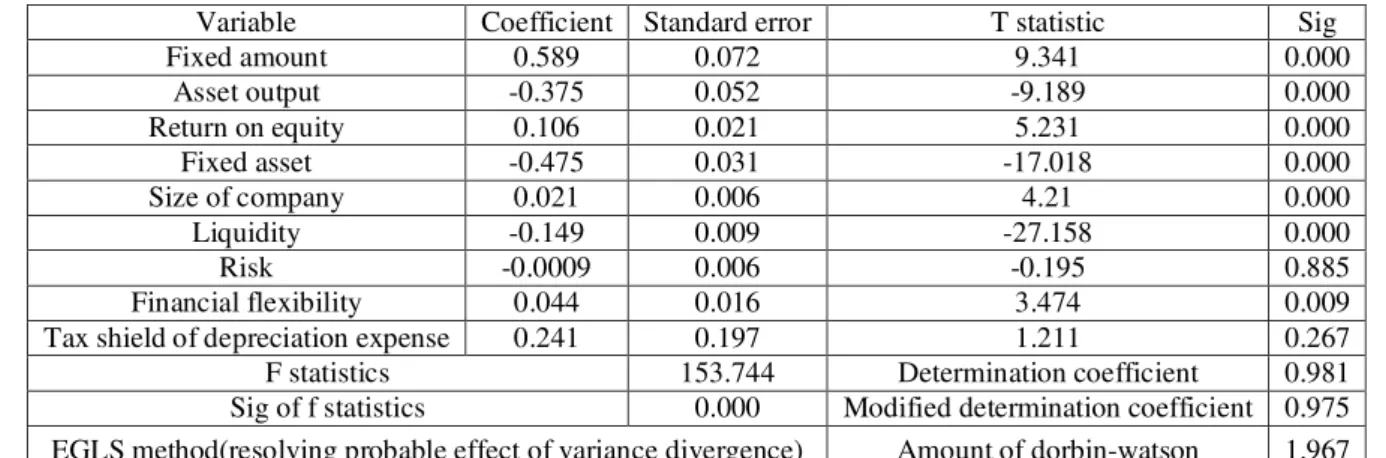

Regarding table 5 sig of Housman test is less than 0.05, so for estimating coefficient of mentioned model fixed effect model us used. Result of testing mentioned model by using fixed effect model and estimating generalized least square method) EGLS) has been presented in table 6.

Table 6: result of first hypothesis

Variable Coefficient Standard error T statistic Sig

Fixed amount 0.589 0.072 9.341 0.000

Asset output -0.375 0.052 -9.189 0.000

Return on equity 0.106 0.021 5.231 0.000

Fixed asset -0.475 0.031 -17.018 0.000

Size of company 0.021 0.006 4.21 0.000

Liquidity -0.149 0.009 -27.158 0.000

Risk -0.0009 0.006 -0.195 0.885

Financial flexibility 0.044 0.016 3.474 0.009

Tax shield of depreciation expense 0.241 0.197 1.211 0.267

F statistics 153.744 Determination coefficient 0.981

Sig of f statistics 0.000 Modified determination coefficient 0.975

EGLS method(resolving probable effect of variance divergence) Amount of dorbin-watson 1.967

Regarding result of table 6 since t statistics of the variable of asset output is bigger than -1.965 and its sig is less than 0.05, there is meaningful and diverse relationship between asset output and ratio of short-term debt of companies accepted in Tehran stock exchange. So this result is in the direction of first hypothesis based on existence of relationship between internal factors of company and ration of its long-term debt.

On the other hand since t statistic of the variable of return on equity is bigger than +1.965 and its sig is less than 0.05, there is meaningful and direct effect between return on equity and ratio of short-term debt of companies accepted at Tehran stock exchange. So this result in in the direction of first hypothesis based on the existence of relationship between internal factors of company and its short-term ratio.Also regarding that t statistic of the variable of size of company is bigger than +1.965

and its sig is less than 0.05 there is meaningful and direct relationship between fixed assets and ratio of short-term debt of companies accepted at Tehran stock exchange. Therefore this conclusion is in the direction of first hypothesis based on existence of relationship between internal factors of company and its short-term debt.Regarding table 6 since t statistic of the variable of liquidity is bigger than -1.965 and its sig is less than 0.05 there is meaningful and diverse relationship between liquidity and ratio of short-term debt of companies accepted at Tehran stock exchange. Therefore this conclusion is in the direction of first hypothesis based on existence of relationship between internal factors of company and its short-term debt.

and ratio of short-term debt of companies accepted at Tehran stock exchange. So mentioned result is in conflict with first hypothesis.

On the other hand since t statistic of the variable of financial flexibility is bigger than +1.965 and its sig is less than 0.05 there is meaningful and direct relationship between financial flexibility and ratio of short-term debt of companies accepted at Tehran stock exchange. Therefore this conclusion is in the direction of first hypothesis based on existence of relationship between internal factors of company and its short-term debt.It should be mentioned that t statistic of the variable of tax shield of depreciation expense is less than ±1.965 and its sig is bigger than 0.05 there is meaningful relationship between tax shield of depreciation expense and ratio of short-term debt of companies accepted at Tehran stock exchange. Therefore this conclusion is in conflict with first hypothesis.

Statistic of Dorbin-watson of the model is 1.967 that exists between 1.5 and 2.5. Also sig of f

statistic is 0.000 that is lower than 0.05 and shows significance of model. Another point that is noticeable in table 4-7, is modified determination coefficient of the model. Amount of modified determination coefficient of used model is 97% that shows 97% of changes of dependent variable is explaining through independent variables that Is acceptable amount. It should be mentioned hat using EGLS method leads to resolving heteronomy effect of probable variance.

Thereforeregarding all above explanations we can say that there is meaningful relationship between internal factors of company and ratio of short-term debt and so the first hypothesis is confirmed.

Testing second hypothesis of research

In the direction of estimating coefficient of model related to testing second hypothesis firstly for determining combined data method and their homogeneity or heterogeneity chao test and F limer statistic are used. Result of this test is in

table 7.

Table 7: Result of chao test

Null hypothesis F statistics

Sig Result of chao test

Using combined data model 7.258

0.000 Null hypothesis is rejected

According to what is seen in table 7, result of chao test show that obtained probability for f statistic is less than 5%, so for testing this model data are used in board form. In the fallowing in table 8 by implementing houseman test necessity of using fixed or random effect method is considered.

Table 8: result of houseman test

Null hypothesis Chi-square statistics

Sig Result

Using random effect model 18.963

0.033 Null hypothesis is rejected

Regarding table 8 sig of houseman test is less than 0.05, so for estimating mentioned coefficient of model we should use fixed effect model. Result of testing mentioned model by using fixed effect model and EGLS has been presented in table 9.

Table 9: Result of second hypothesis

Variable Coefficient Standard error T statistic Sig

Fixed amount 0.134 0.038 4.362 0.000

Asset output -0.182 0.034 -6.853 0.000

Return on equity 0.038 0.016 2.961 0.000

Fixed asset 0.184 0.026 10.321 0.000

Size of company -0.009 0.008 -3.365 0.000

Liquidity 0.074 0.006 7.875 0.000

Risk 0.006 0.004 1.81 0.071

Financial flexibility -0.026 0.007 -3.657 0.000

Tax shield of depreciation expense -0.291 0.154 -1.974 0.046

F statistics 31.201 Determination coefficient 0.904

Sig of f statistics 0.000 Modified determination coefficient 0.874

Regarding table 9 since t statistic of the variable of asset output is bigger than -1.965 and it sig is less than 0.05, there is meaningful and diverse relationship between asset output and ratio of long-term debt of companies accepted at Tehran stock exchange. Therefore this result is in the direction of second hypothesis based on existence of relationship between internal factors of company and its long-term debt.On the other hand since t statistic of the variable of return on equity is bigger than +1.965 and it sig is less than 0.05, there is meaningful and direct relationship between return on equity and ratio of long-term debt of companies accepted at Tehran stock exchange. Therefore this result is in the direction of second hypothesis based on existence of relationship between internal factors of company and its long-term debt.

Also since t statistic of the variable of fixed asset is bigger than +1.965 and it sig is less than 0.05, there is meaningful and direct relationship between fixed asset and ratio of long-term debt of companies accepted at Tehran stock exchange. Therefore this result is in the direction of second hypothesis based on existence of relationship between internal factors of company and its long-term debt.Also regarding that e t statistic of the variable of size of company is bigger than -1.965 and it sig is less than 0.05, there is meaningful and diverse relationship between size of company and ratio of long-term debt of companies accepted at Tehran stock exchange. Therefore this result is in the direction of second hypothesis based on existence of relationship between internal factors of company and its long-term debt.

Regarding table 9 since t statistic of the variable of liquidity is bigger than +1.965 and it sig is less than 0.05, there is meaningful and direct relationship between liquidity and ratio of long-term debt of companies accepted at Tehran stock exchange. Therefore this result is in the direction of second hypothesis based on existence of relationship between internal factors of company and its long-term debt.

This is whereas t statistic of the variable of risk is less than ±1.965 and it sig is bigger than 0.05, there is meaningful relationship between risk and ratio of long-term debt of companies accepted at Tehran stock exchange. Therefore mentioned result is in conflict with second hypothesis. On the other hand since t statistic of the variable of financial flexibility is bigger than -1.965 and it sig is less than 0.05, there is meaningful and diverse relationship between financial flexibility and ratio of long-term debt of companies accepted at Tehran stock exchange. Therefore this result is in the direction of second hypothesis based on existence of relationship between internal factors of company and its long-term debt.

It should be sad that t statistic of the variable of tax shield of depreciation expense is bigger than ±1.965 and it sig is less than 0.05, there is meaningful relationship between tax shield of depreciation expense and ratio of long-term debt of companies accepted at Tehran stock exchange. Therefore this result is in the direction of second hypothesis based on existence of relationship between internal factors of company and its long-term debt.

Dorbin-watsonstatistic of the model is 1.868 that locates between 1.5 and 2.5. Also sig off statistic is 0.000 that was less than 0.05 and shows meaningfulness of the model. Another point that is noticeable in table 9 is modified determination coefficient. Amount of modified determination coefficient used in the model is 84% that shows 87% of changes of dependent variable isexplained by independent variable that is acceptable amount. T is necessary to say that using EGLS method leads to resolving heterogeneous effect of probable variance.

Therefore regarding all above explanations it can be said that there is meaningful relationship between internal factors of company and long-term debts and so second hypothesis is confirmed.

Applied suggestions

structure combination of financial supply resources of investment projects (debt and equity) Is explained. Determining factors of capital structure are divided into two groups; internal factors that root from nature and features of company’s activity, such as profitability, assets structure, growth opportunity, size and fluctuation. External factors that root from features of environment like rate of interest, credit policies of government, banks and credit institute. Companies while making financial decision for increasing outputshould seem a number of external and internal factors. Operational features of company that is known as internal factors affect output of company. Internal factors are controlled by company and can affect them. On of the most important internal factors of company are capital structure, profitability, size of company, ability of management, visible assets and cash management. Therefore determining capital structure is one important case that financial managers face for achieving financial goals. Companies are going to maximize company’s value through best determination of capital structure. Due to existence of some effective factors on decisions related to capital structure of a company, judgment done by a person who determines capital structure has high importance in between. In case judgment of deciding people about degree f importance of these different factors affecting capital structure is different then capital structure of two similar companies can be different. These effective factors were psychological, complicated and qualitative to much degree and since capital markets weren’t complete and decisions may accompanied by insufficient knowledge, so it doesn’t fallow an accepted theory. Generally companies are interests to supply all required financial resources for investment through least cost. Companies are forces to plan their primary capital while establishing private units and then for investment need supplying cash decision of capital structure are affected. So in the fallowing some suggestions are presented:

-it is suggested stockholders pay attention to performance of managers at using assets and resources of companies and increasing utilization properly in order to increase power of company’s competition in the market.

-capital structure affect competitive power f companies in other word companies that have used their capital structure from long-term debt for supplying their resources have devoted more share of market to themselves therefore It is suggested for increasing competitive power use long-term debt like bond in financial supply. -it is advised according to hypothesis of capital structure managers of companies by proper growth opportunities should choose less leverage’ because if they increase degree of their external debt, they are not able to use advantage of opportunities of their investment.

-financial analyzers, investors and financial managers of stock can use ratio of debt to equity for a sign of financial health of company. So in companies that they have proper financial ability companies that have sale growth as financial situation os better ratio of debt to equity increases.

Some suggestions

-in this research regarding structure of ownership of companies that is family ownership and non-family ones division is not done and in case of dividing companies based on structure of ownership t was possible to change result of research. Therefore it is suggested in future research model is tested regarding structure of ownership of companies and obtained result is compared by result of current research.

-cases mentioned in text of financial cases hasn’t been modified through inflation effect and since business units have different times of establishment and they have acquired their asses at different times so quality of comparative capability

Of cases can affect research result and accompanies generalization of result with limitations. Therefore it is suggested research model in companies that are close to each other regarding time of establishment be tested in order to control effect of unmodified inflating.

REFERENCES:

1. Ebrahimi, Kazem; Bahraminasab and SalehiKashkoli, Ashraf(2014). Considering effect of capital structure on relatedness of accounting information. Thesis for getting M.A degree at semnan university-faculty of economy and administrative sciences

2. Ahmadpour, Ahmad, Rasekhi, Saeid, and nasirighalesari, seyyedehZahra(2013). Effect of information quality on liquidity risk, scientific research quarterly of management accounting and aouditing(2(5), 85-98.

3. Aslani, Azom and Haghi, sara(2014). Considrin effect of inflexibility of costs and capital structure at Tehran stock exchange. Thesis for getting M.A degree at Islamic Azad university of Garmiuit-faculty of accounting and management.

4. Pourzamani, Zahra’ jahanshad, Azita, Nemati, Ali and farhoodiZare, Parvin, (2010). Considering effective factors on capital structure at companies, financial accounting and auditing research letter

5. Habibi, Maryam, 2012, considering effect of capital structure on performance of stock companies, M.A thesis at business management field, Alzahra university, faculty of social science and econmy, feb 2012

6. Hejazi, Rezvan and Khademi, Saber, 2013, effect of economic factors and corporate features on capital structure of companies accepted at Tehran stock exchange, journal of

financial accounting research, fifth year, No 2,p 1-16

7. Haghightalab, Bahareh, 2011, considering relationship of capital structure and efficiency of companies accepted at Tehran stock exchange by using data envelop analysis technique, M.A thesis of accounting field at ferdosiuniversity of Mashhad, faculty of administrative and economic science, April 2011

8. Darabi, Roya and Karimi, Akram(2010). Effect of growth rate of fixed assets on stock output, researches of financial accounting and auditing, 99-130

9. Roohi, Ali’ lashgari, Zahra and EshaghiAshtiani,

Mohammadali(2014).considering convergence of capital structure of companies accepted at Thran stock exchange. Thesis for getting M.A degree at Islamic azad university of central Tehran unit-faculty of economy and accounting

10.Zinali, Mehdi and jamalmohammad, shilan(2011),considering effect if capital structure on size, capital output rate and profit of each share of companies accepted at Tehran stock exchange, journl of financial knowledge of analysin stock, 9,43-60

11.Sehat’ saeid and shariatpanahi, seyedmajid and mosaferi Rad, faraz(2011). Relationship of asset output, return on equity of economi value added at insurance industry, journal experimental studies of financial accounting, 9(32), 121-140

12.Abbaszadeh, Mohammadreza and Rigi,)2010). Considering relationship of capital structure and performance of productive companies accepted at Tehran stock exchange by using criteria of economic value added.Thesis for getting M.A degree at ferdosi university of Mashhad-faculty of economy and accounting. 13.Arabsalehi, Mehdi, Moayadfar, Rozita and

Tehran stock exchange. Journal of financial accounting research, 4(3), 70-74

14.Ghaderi, Kaveh’ ghaderi, saman. Ghaderi.Salaholdin, and ghaderzadeh ,seyedkarim(2014).considring effect of liquidity on profitability of companies by approach of testing coast(case study of Iran khodro company).scientific research quarterly, 3(9), 111- 123

15.Ghasemi, Hasan, 2009, considering effect of capital strcture on relationship of ratio of P/E and stock output, M.A thesis of financial management field at universities of Europe, faculty of economic science, feb 2009

16.Ghorbanalizadeh, Roohangiz, 2013, relationship between capital structure and market of companies accepted at stock exchange, M.A thesis of accounting field at sistan and balochestan university, Oct 2013 17.Moradi, mohammadali; jafari, Mehdi and

ghorbanalizadeh, roohangiz(2013). Relationship between capital structure and market of products accepted at Tehran stock exchange. Thesis for getting M.A degree at sistan and balochestan university –faculty of accounting and management

18.Mollanazari, Mahnaz; noorifard, yadollah and GhashghaeiAbdi,shaghayegh(2012).different effect of size of company and type of industry on profitability, financial accounting and auditing research, 4(16), 157-183

19.Nazaripour, Mohammad, Pirozram, Amir and Khazdoozi, Bizhan, 2010, considering effect of capital structure on liquidity of companies accepted at Tehran stock exchange(case study of cement industry) journal of ForoghTadbir, No 20, 8-24

20. Abu-Rub, N. (2012). Capital structure and firm performance: Evidence from Palestine Stock Exchange. Journalof Money, Investment

and Banking, 23, 109-117

21. Baral, K.J. (2004). "Determinants of capital structure: A case study of listed companiesin Nepa"l. The Journal ofNepalese Business

Studies. 1(1):1–13.

22. Çekrezi, A, (2015), Internal Factors which Influence Capital Structure Choice of Albanian Firms, Research Journal of Finance and

Accounting, Vol.6, No.8, pp: 168-176.

23. Lin, Tien-Chu., Kung, Shiann-Far., & Wang, Hei-Chia (2015). Effects of firm size and geographical proximity on different models of interaction between university and firm: A case study, Asia Pacific Management Review, 20, 90-99.

24. Tay, Ink (2009). Fixed Asset Revaluation: Management Incentives and Market Reactions, Lincoln University, Canterbury, New Zealand, 1-111.

25. Yung, Jenneth., Li, Deqing Diane., &Jian, Yi (2015). The value of corporate financial flexibility in emerging countries, Journal of

Multinational Financial Management, 1-45.

26. Yurdakul, Funda (2014). Macroeconomic Modelling Of Credit Risk For Banks, Social