CARREFOUR ENTERPRISE VALUATION

Afonso Paisana de Vilas-Boas Lebreiro

Project for the conferral of Master in Finance

Supervisor:

Prof. Doutor Pedro Manuel de Sousa Leite Inácio, Prof. Auxiliar

ISCTE Business School, Departamento de Finanças

ABSTRACT

This thesis consists in a global valuation of Carrefour, one of the largest food retailers in the World, using the three most commonly used methods, Discounted Cash Flow (DCF), Economic Value Added – Market Value Added (EVA-MVA) and Multiples.

Since Carrefour is present in three continents and more than fifteen countries, studying its historical presence in terms of market position in each country is crucial to understand how a French retailer became one of the largest and most influent companies in food retail industry.

The business concepts behind its international expansion and the cultural influence that were imposed in many countries through its marketing strategy were one of the keys to success.

Concerning the results of DCF and EVA-MVA Models, they were computed through a projection for the 2013-2017 period, based on a set of assumptions and forecasts that include macroeconomic concepts and financial ratios that support the results achieved.

Using DCF Model, the investment decision is to BUY the stock.

However the relative valuation shows that Carrefour multiples are bellow its benchmark in every key performance indicator. When compared with other similar companies, the Group also presents lower multiples with the exception of P/E, meanings that Carrefour share may be undervalued.

Keywords: Valuation, Retail, Discounted Cash Flow vs Economic Value Added, Market

Multiples

RESUMO

Esta tese consiste numa avaliação do Carrefour, um dos maiores retalhistas do Mundo, usando três métodos de avaliação, Discount Cash Flow (DCF), Economic Value Added – Market Value Added (EVA-MVA) e os Múltiplos.

O Carrefour está presente em três continentes e mais de 15 países, estudar a sua presença histórica em termos de posição de mercado em cada país onde está inserido é crucial para perceber como é que um retalhista francês se tornou numa das maiores e mais influentes empresas de retalho alimentar.

O modelo de negócio por detrás da sua expansão internacional bem como a influência cultural que foi imposta em muitos países através das suas estratégias de marketing foi uma das chaves para o sucesso.

Os resultados dos modelos DCF e EVA-MVA foram atingidos através de uma projeção para o período de 2013-2017, com base num conjunto de pressupostos e previsões que incluem conceitos macroeconómicos e rácios financeiros que suportam os resultados obtidos.

Utilizando o modelo DCF, a decisão quanto a investir é COMPRAR a ação. O modelo dos Múltiplos mostra que a performance do Carrefour é inferior ao valor de referência em todos os indicadores. Quando comparado com outras empresas, o Grupo também apresenta valores baixos, o que significa que acção do Carrefour pode eventualmente estar subavaliada.

INDEX

1 - Introduction_________________________________________________________1

2 - Review of Literature__________________________________________________2

2.1 - Valuation Process_____________________________________________2

2.2 - Discounted Cash Flow _________________________________________3

2.3 - Economic Value Added________________________________________4

2.4 - Multiples____________________________________________________4

3 – Industry in the World _________________________________________________5

3.1 – Global Economy _____________________________________________5

3.2 – Retail Industry History ________________________________________6

3.3 - Challenge of Retailers in future _________________________________7

3.4 – Financial Business____________________________________________7 4 - Carrefour History____________________________________________________8 5 – Internationalization _________________________________________________10 5.1 – Europe____________________________________________________11 5.1.1 – France_____________________________________________11 5.1.2 – Italy_______________________________________________13 5.1.3 – Belgium____________________________________________13 5.1.4 – Spain______________________________________________14 5.1.5 – Portugal____________________________________________15 5.1.6 – Poland_____________________________________________16 5.1.7 – Russia_____________________________________________16

5.2 – South America______________________________________________17 5.2.1 – Brazil______________________________________________18 5.2.2 – Argentina___________________________________________18 5.3 - Asia_______________________________________________________18 5.3.3 – Taiwan_____________________________________________19 5.3.2 - China ______________________________________________19 5.3.3 - India_______________________________________________19 5.3.4 – Indonesia___________________________________________19

5.3.5 – Other Countries in Asia________________________________19

5.4 - Africa _____________________________________________________20

5.5 - Disposals and the European Crisis_______________________________20

6 - Competitors________________________________________________________21

6.1 - E.Leclerc___________________________________________________21

6.1.1 - Competition with Carrefour_____________________________22

6.2 - Casino Guichard Perrachon____________________________________22

6.2.1 - Competition with Carrefour_____________________________23

6.3 – Groupe Auchan_____________________________________________24

6.3.1 – Competition with Carrefour ____________________________25

6.4 – Walmart___________________________________________________26

6.4.1 – Competition with Carrefour ____________________________26

6.5 – Tesco _____________________________________________________28

6.5.1 - Competition with Carrefour_____________________________28

6.6.1 – Competition with Carrefour ____________________________30

7 - Financial Statement Analysis __________________________________________30

7.1 – Profitability Ratios___________________________________________30

7.2 - Risk Ratios _________________________________________________31

7.3 - Liquidity Ratios _____________________________________________33

7.4 – Capital Structure Ratios_______________________________________33

8 – Company Valuation _________________________________________________34

8.1 – Assumptions________________________________________________35

8.1 – FCFF and FCFE_____________________________________________38

8.3 – EVA and MVA_____________________________________________39

8.4 – Multiples __________________________________________________41

9 – Conclusion ________________________________________________________43

References___________________________________________________________45

Annex I - Types of Stores (Glossary) ______________________________________54

Annex II - Carrefour Stores and Sales per Country____________________________57

Annex III - Competitors_________________________________________________59

Annex IV - Market Share________________________________________________60

Annex V – Steady Growth Rate___________________________________________61

Annex VI - Compounded Annual Growth Rate_______________________________63

Annex VII - Income Statement____________________________________________65

1

1 - INTRODUCTION

Before starting this project, the primary question was: Why did Carrefour divested from all its operations in Portugal?

Carrefour sold its business unit in 2007 with no apparent reason for making this decision. Some causes might explain such strategic decision, but in any case the Group did not present them.

Portugal was living a stagnation period in terms of economy since 2000, which might be one of the reasons. Another reason could be the increased and fierce competition in the Portuguese market headed by Sonae and Jerónimo Martins. Taking this in consideration, Carrefour realized that they needed to acquire a local company or invest massively to match Sonae and Jerónimo Martins in a country with low economic prospects. Carrefour policy is to only invest in countries where they can be the leader or one of the leaders. In Portugal, they were a minor player.

On the other hand, their hypermarket concept proved to be successful, an example of this was Carrefour of Telheiras, which was the most profitable hypermarket in the country at that time. It is also important to notice that when the Group decided to sell its business unit to Sonae, they had capacity to grow through the eleven new commercial licenses. These questions and doubts were the primary reasons to choose Carrefour.

Other reason is the size of the company. Carrefour is one of the most dominants worldwide players in the Food Retail segment. It is a benchmark for all other retailers and a trustful brand for the consumers, a company with more than 50 years of existence. In the end of 2012, Carrefour registered 364.969 employees dispersed by 15 countries.

To value a Group with these features is a real challenge. Each country needs to be studied individually in order to know the Carrefour historical presence and the last events occurred in that country, the competitors and the opportunities to growth or being the market leader.

Framed by the reasons mentioned above, this project focus on the Food Retail Industry and Carrefour reality instead of a deeper study of the models used on Valuation.

2

2 - REVIEW OF LITERATURE

2.1 – Valuation Process

According to Fernandez (2013), the valuation process is very complex and can be done through different models, meaning that the conclusions of each model are usually different because any valuation model uses its own assumptions from the prospects. We cannot extrapolate that there is a model that is clearly better than another, we just can say that the assumptions used in some models are more close to the reality than others.

The valuation of companies is very useful for many purposes and is fundamental for helping shareholders, managers and investors on the decision process. Some examples of how valuation process is extremely important are given bellow.

Valuation is important in M&A deals, when a company is interested to acquire or merge with another company. In this process the buyer will do a valuation of the other company and define the maximum price that he should offer in order to acquire the other company. The target will do the same but in other perspective, to determine the minimum value that should be reached in order to accept the offer. Usually the deal will be done close to the middle point, between the minimum amounts that target is willing to accept and the maximum value that the buyer is willing to offer.

In the case of listed companies, valuation can be used to determine the price of the share and then compare this price with market price, this comparison is fundamental to decide if one should buy, sell or hold the share on the market. It is also important to decide in a case of a portfolio of securities if we should increase or decrease a position. Valuation is also important to compare companies from the same sector. We may have long position in a company and a short position on its competitor, this strategy may allow the investor to make profit in three situations:

1- if the company where investor has the long position rises and the short position drops, so the securities are going in opposite direction with direct benefits from investor that will make profit on both cases;

2- if the long and short position rise, but the increase on the price of the long position is higher enough to compensate the loss on the short position;

3- if the long and short position drop, but the decrease on the price of the short position is higher enough to compensate the loss on the long position;

3 When a company wants to go public, the share value associated has to be determined by valuing the company, in order to define the share price.

Valuation is fundamental for executives of a company or business unit in order to know the value creation coming from the management quality.

The strategic decisions taken by executives that could influence the future of the company, as to acquire, merge, sell or organic growth can also assessed based on the company valuation, as a management tool.

Valuation is also an instrument that assists on strategic planning decisions such as, introduce a certain product in the market, open a subsidiary in some country, exit from a market, etc, in the sense that it stipulates the impact of the decisions in the value

creation or destruction.

Mota et al (2012), Koller et al (2010) wrote about the three models that are most commonly used to value a company: The Discounted Cash Flow Model (DCF), Economic Value Added – Market Value Added (EVA-MVA) and Multiples. In the case of Multiples all the information collected to make comparison must be taken from a database, in this study we use for the purpose Bloomberg, and the selection was based on Fernandez (2013).

2.2 - Discounted Cash Flow Model

The Discounted Cash Flow Model (DCF), values a company based on the evolution of the cash flows that the company will generate in the next years. Usually 5 years, but it can also be used 3 years. More than 5 years create a huge uncertainty relatively to the future investments, future performances and the sensitivity of the financial manager at a time horizon of 7, 8, 10 years is not rigorous and may have serious repercussions, which would conduct to an increase on the level of the bias.

This model is turned to the future and doesn’t contemplate any reference to the present and past performance of the company.

In this Model, two different approaches are used to get the share value, the Free Cash Flow to the Firm (FCFF) and the Free Cash Flow to Equity (FCFE).

4 The FCFF contemplates cash flow available to equity and debt holders, the FCFE just consider cash flow available to equity holders.

Before starting to explain how to get a DCF value, it is important to explain how to get the future cash flows.

To explain the FCFF approach, it is relevant to explain all the steps to achieve the share value.

These steps are explained in the Methodology.

2.3 - Economic Value Added – Market Value Added

The Economic Value Added (EVA) is a model created by Stern Stewart & Co and is exactly the same of the Net Operating Profit After Taxes (NOPAT).

EVA is computed through the difference between the Return on Invested Capital (ROIC) and the cost of this investment that corresponds to WACC, this difference is multiplied by the amount of invested capital. EVA is positive if the ROIC>WACC, in other words if the return is higher than the cost, otherwise it will be negative. EVA is essential to anticipate decisions about future investments and gives transparency between management and shareholders in the decision process. If EVA gives a positive amount, a company is creating value, if EVA gives a negative value, the company is destroying it.

Associated to EVA, Market Value Added (MVA) was created. MVA measures the value originated by the company in the past and the value that company expects to generate in the future. It is correlated to EVA, because it is the PV of the sum of the future EVAs generated every year discounted to year 0. MVA is positive, if the market believes that the company had and will continue to have a return higher than the costs implicit in its investments. MVA is an important rubric to shareholders because it indicates, if the company is creating or not value added, which means that if their money is being well managed.

2.4 - Multiples

Multiples are an alternative evaluation model of DCF and EVA-MVA to value a company. Using several ratios in companies from the same industry/sector or with a

5 specific competitor it is possible to notice immediately in which ratio should the company focus more or if every ratio is above the benchmark/target, it this happens, we must try to find the reason or just to analyse the performance of the other competitors. Multiples, take into consideration the dimension of each company and using them we can take some conclusions about company’s valuation.

Multiples are a very useful tool for shareholders, investors and managers and help them in taking some conclusions about the performance of a company in comparison with other competitors.

Through this method it is possible to verify if there’s a growth potential and also identify risks that a company has taken when compared with benchmark.

There are many multiples that we can use, some of them are specific to each industry, like Price to Potential Customer for Internet companies or Price to Units to value soft drinks and consumer products companies.

3 – INDUSTRY IN THE WORLD

3.1 - Global Economy

The 250 largest retailers in the World represented in 2011 $4.271 trillion of revenues, with an overall growth of 5.1%. More than 80% of them grew on that year.

The global economy is facing a recession in Europe, the main market. The consequences of this recession, first in the periphery countries (Spain, Italy, Greece, Ireland and recently France), have a negative impact on the rest of the other EU economies, as a result of having a common market in EU, which privileged the commercial relations between countries.

A recession is characterized by the difficulty in accessing credit to companies and families, more unemployment, more bankruptcies, less imports and some other problems. The conjugation of all these conditions, lead to a decrease on the purchasing power of consumers that will adjust their consumption necessities, reducing consumption and as consequence, a reduction of investment by companies that will have less profit.

6 The European recession has a collateral effect on the countries that have intensive relationships with European economies. Big economies as US, Brazil, China and Japan are decelerating its growth as a consequence of that problem, suffering reductions in their exports to Europe. As an ultimate effect of this problem, the performance of US, Brazil, China and Japan neighbor countries will suffer with slowdown of them.

3.2 - Retail Industry History

On the beginning of 1960, Carrefour created the “hypermarket” concept. This concept was followed by many other players. Hypermarkets, has more area in comparison to supermarkets, and sell food products, but also non-food products. During the years, the retailers had a huge growth, but when this growth started to slow down, they started to acquire and merger with other competitors in order to still gain market, as consequence the market became more concentrated, but nevertheless this concentration were more intensive in the US market.

Europe is the largest market in the World, but European market is composed by many countries, which complicated the concentration of the market (each country has local players that usually has strong market share as consequence of being in that market since the beginning) which create many difficulties to achieve economies of scale when compared to US market. Based on this and also the fact that European market was more consolidated, in the beginning of 70’ the retailers started to open subsidiaries abroad. The succeed internationalization of retailers in countries with different cultures and different ways to work, obliged the retailers to decentralized its business.

In US market, the concept that revolutionaries the industry was the “discount retail”. This concept appeared in the 50s. At this time, the retailers were starting to use TV to do advertisement. Discounters practice low prices, which are possible thanks to lower margins and operating costs, when compared with general stores.

In the 70’s, the expectations around the industry were very high and many local and regional players rose, which make the average growth were just 9%. In the 80’s the appearance of new competitors continue and pulled the prices down and made pressure to reduce the costs. This environment led to mergers and acquisitions, in order to gain scale and reduce costs and prices. In this decade the average growth was 7% per year.

7 Between 1986 and 1993, the top 5 retailers increase their concentration in 10%, 62% to 72% in terms of sales.

3.3 - Challenge of Retailers in future

Retail Industry is a privileged industry, food is essential for living and every person needs to eat, which means that this sector is one of the last, to suffer with the recession.

The Retail Industry is in the middle of a technological revolution, a huge proportion of population from Europe and US already have smart phones and computers with internet accessing, this means that they will start to use another shopping channels. The retailers that will survive in the future are the ones that have the most appellative websites, strong merchandizing and marketing, an easy form to buy and a very effective distribution, the last but not least they must have the capacity to satisfy the expectations of consumers. In terms of costs, this new channel implies less labor and structural costs. The price is important, but in many cases is not relevant, the way that the products are presented can make the difference.

Physical supermarkets, hypermarkets and convenience stores will keep being used by populations, but on the other hand this new way to buy products requires less time and is more practical if it is done correctly.

The mobile applications channel contributes with 5.1% of the whole retail sales, it is expected to achieve 17% to 21% of total sales in 2016.

The advertising on social networks like Facebook or Twitter is essential and is another channel that should be explored by retailers in order to be connected and close to the costumers or possible consumers.

A very flexible IT department is vital to have a strong presence in all these digital channels that are now available to retailers. The capacity to solve, find and create solutions is the key to be a leader in the retail sector over the next years.

3.4 - Financial Business

It is important to refer that this specific industry is also a financial business. Carrefour is a main player in the modern distribution concept, receiving immediately from the consumers just after the purchase, but they have a medium-term payment along

8 suppliers, which can vary between 60, 90 or more days. This unusual advantage of this industry, when comparing to the majority of the other sectors, make the difference in terms of liquidity, which means that they can use the “suppliers account”, to leverage other activities (acquisitions, marketing, etc) and even receive interests for having huge amounts of money in their bank accounts.

4 - CARREFOUR HISTORY

Group Carrefour is a French multinational company in the retail sector. It was created in 1959 by Marcel Fournier, Denis Defforey and Jacques Defforey.

Carrefour opened its first store in 1960 in Annecy, Haute-Savoie and in 1963 they created the first hypermarket in Sainte-Geneviève-des-bois outside Paris with a sales area of 2500 square meters. This store was revolutionary in the sense that it was very well accepted by French consumers and had the impact of changed their consumption patterns. The media classified this store with the name “hypermarket”, based on its unusual large size. After this first impact is passed way, Carrefour started to open more hypermarkets around the country. Sales grew a lot in this time, mainly the sales of the non food products, which in the first years reached 50% growth every year.

In the beginning of 70’s, Carrefour turned to “malls”, it was also a new concept, which includes hypermarkets, food stores, cloth stores, etc. During this decade the goal was expand the business in France. In 1969, they started to operate in Belgium, which was the first step of its internationalization. The expansion to other markets has been very fast and lead Carrefour be the largest retail group in Europe and the second around the World, just behind Wal-Mart, working in Europe, Asia and South America. In the 70’s, Carrefour became a publicly company, when get in the CAC40.

Carrefour was one of the first companies in food retail market that start to internationalize, this decision was very important and transform Carrefour in a global company with a global brand. This decision gives them a competitive edge against competitors in terms of economy of scale, brand position, consumer’s confidence, access to new products, different raw materials.

9 This internationalization process was the main responsible for the business growth of Carrefour in the 80’s and 90’s. In the meantime they continue to open stores in France and consolidated the first position as market leader.

In the first decade of the millennium, the company started to face fierce competition in France, mainly from Leclerc, in the rest of Europe they open business units in some Eastern countries, which were facing high growth rates and population was increasing the purchasing power. In Western Europe countries, the financial crisis of 2008 had a huge impact on the consumption patterns, due the increase of unemployment and in some cases economic recession. Outside Europe, Carrefour suffer an increase of competition in countries like Colombia, Mexico and Japan, mainly from Tesco and Wall-Mart which acquired domestic companies and began reducing prices. Carrefour was forced to decrease prices and lower margins in order to follow the other companies. After some years they took the decision to close or sell the business unit in those countries.

In January 30 of 2012, George Plassat was nominated to CEO of Group Carrefour. Plassat was CEO of Vivarte SA, a company owned by Carrefour and Groupe Casino since 2000. It was also CEO of Carrefour Spanish unit during two years and worked fourteen years in Groupe Casino. Plassat became the CEO of Carrefour after three years of governance by the Swedish Lars Oloffson (January 2009 – January 2012).

Oloffson’ governance was not succeeded because some of its controversial decisions, DIA span off, the failure in the merger between Carrefour Brazilian subsidiary and Grupo Pão de Açucar through it holding Cia, the idea of listed 25% of Carrefour properties in CAC, which never happened because of the lack of consensus in the board and investors as well as unions opposition. All these issues and others ended up in bad results across the years in terms of sales and ultimately in the constant decrease of profits and dividends. The investors lost their confidence in Carrefour board and penalized the share price. During these three years, Carrefour shareholders lost about €7 billion in CAC.

The mission of Plassat is to recover the investors’ confidence, reduce the debt burden in order to still have a strong position in Europe. Debt issues have been the main concern of European Governments in the last years, consequently it influenced the companies capacity to issue debt in the market or borrow in the Banks. Another mission that

10 Plassat has to face is to reverse the trend of sales which has been declining in the Western Countries (France, Italy, Spain) mainly explained by the strong competition of the convenience stores and supermarkets established in the residential zones by its competitors. Carrefour has also convenience stores and supermarkets, but it is known by its hypermarkets.

At the end of 2012, Carrefour counted with 9994 stores around 33 countries, including 3454 supermarkets, 1366 hypermarkets, 5010 convenience stores, hyper cash stores and 164 cash & carry. [See Annex II – Carrefour Stores and Sales per Country)

These all kind of stores commercializes food and non-food products.

5 - INTERNATIONALIZATION

The Group Carrefour started being interested on expanding its business abroad, after a law has been imposed by French Government in 1963 that restricted the development of large new stores.

The entrance in many countries happened through the acquisition of a local company or through the constitution of a business unit. In the specific case of retail the multinationals started with the opening of one or two stores in strategic cities, capitals or very important cities where the local population has more purchasing power. After being implemented, the strategy for company like Carrefour or Wall-Mart is always become the leader or be on the restricted list of the two or three largest retailer in those countries. For these giant companies be a leader is the most important aspect that guaranteed the survival as one of the main the players in this business. They want to be a leader or the leader in all market where they are inserted, this means have a very well defined strategy when they get in a country. Usually Carrefour entered in a country through a local partnership, because all the countries even the undeveloped countries have their own local retailers that have are the leaders before the multinationals get in their countries, so the only way to entered in those countries is acquiring one or two of this local retailers that don’t need to be the most important, but have potential to grow and have a important position in some region of the country where the Group doesn’t have and would to have representation. Growth organically is very important when a company is established in the market, but try to growth organically starting with no

11 expression is very difficult and takes many years and big investment in advertising in order the potential costumers started to identify with the name of the brand and the products that is offering.

5.1 - EUROPE

Europe is the continent where Carrefour has more expression with 73% of its business, concentrated in 7 countries directly and in 6 countries indirectly in the format of franchisees. Europe is the wealthiest economic zone in the world, it is a small continent when compared with other continents, but it has many countries, several languages and multi cultures. With the constitution of the European Union that aggregated 27 countries, many barriers disappeared and facilitated the internationalization of many companies and allowed the expansion of Carrefour throughout Europe.

In 2012, the performance of Carrefour in Europe was affected by the economic crisis that affected the Continent. Generally, every country dropped their revenues with exception to France and Belgium that registered a small growth. On aggregate terms the revenues in Europe dropped 0.88%. It is evidence that Europe, mainly western of Europe is a mature market and the position of Carrefour in Europe is a leadership one. Based on this, it is very difficult to grow organically, just through mergers or acquisitions, but with a leadership position it has many restrictions mainly from the European Commission to acquire more competitors.

5.1.1 - France

The Group Carrefour was born in France and is the largest food retail company in the country. It has 4635 stores, this mean that 46.37% of the all stores are in France. Across the years the company has been acquiring local competitors.

In 1991 acquired 10% of Picard Surgelés and increased in 1994 to 79%, leader in frozen food retail, paying an amount of €140 million, but in 2001 the company sold out 73.89% of its position in Picard Surgelés for €624 million.

In 1996, the firm acquired 42% of Societe GMB that controls Group Cora, a retailer that operates mainly in France and Belgium. In 2001 the Group was obliged to sell the 42% that they owned on Societe BMG as a result of merger between Carrefour and Promodès. The European Commission expressed concerns about this minority position

12 on BMG that could influence and block management decisions of its competitor Cora and also having access to strategic business information. Based on this concern the Commission imposed to sell that position.

In 1997, the Group signed an agreement with Guyenne & Gascogne , Coop Atlantique and the Chareton Group for the implementation of the Carrefour brand on their 16 hypermarkets, but these groups keeping the management of the stores.

In 1998, Carrefour acquired the totality of Comptoirs Modernes that they already owned 23%, the amount paid by the Group was $2.38 billion through cash and stock. Comptoirs Modernes was a local rival that operated in France and Spain.

In 1999, Carrefour executed a non-hostile takeover on Promodès of €16 billion, with Carrefour offering 6 shares for each 1 share of Promodès. The combined firm would have €49 billion of market capitalization and a labor force near of 250,000 workers. This company was the biggest competitor of Carrefour in France and in some other markets. The implicit synergies were relevant, on the areas that Carrefour was strong and Promodès weak, and the opposite. Carrefour was the fifth largest retailer in Europe and Promodès occupied the seventh position, but the merger of the two companies would make them the second biggest retailer in the World, meaning that this merger originated the most important retailer in Europe, exceeding the German retailer Metro AG, the biggest retailer of Europe at that time and second biggest in the World.

The main reason pointed out was the difficulty for both companies to growth domestically. Another reason, but non-official was Wall-Mart, the biggest retailer in the World. At this time, Wall Mart started to enter in Europe and was trying to gain market share in the main countries acquiring local retailers in Germany and UK in the previous years. They were looking for a takeover of a French retailer.

The merger was accepted by the European Commission in January 2000, but with some restrictions because with this merger the new company would be the leader in France (27% of market share) and Spanish market (26% of market share). The most important requirement that the Commission imposed was as I referred above, the settlement of 42% of capital in BMG, and some commitments with suppliers and producers of both companies, for a period of time defined by the Commission and the French and Spanish

13 Competition authorities. By the end of this year, 14 supermarkets and 7 hypermarkets were closed in France.

In 2004, Carrefour implemented an investment plan concerning the increase of the sales area, with the opening of 914 stores in France, and 793 abroad.

On 2012, Carrefour acquired Guyenne & Gascogne, a company in which Carrefour had a long partnership in the naming of the stores. Guyenne & Gascogne had 37 stores in the southwest of France, a zone where Carrefour wanted to increase its position. The amount involved in this acquisition was €370 million.

In terms of market share, Carrefour in 2010 was the company with larger market share, but it had Leclerc competing for the first position. [See Annex VI – Market Share: Table 21]

5.1.2 - Italy

After France, the country in Europe where Carrefour has more stores is Italy with a total of 1218 stores. The Group started to operate in this country in 1993 and has a large expression in the convenience stores with more than 700 around the country. In terms of revenues the contribution of this business unit is around €5.1 billion. In 2012 the revenues suffer a fall of 5.8%, as result of the European crisis that had a huge impact on the reduction of consumption.

In 2009, the Group occupied the third place in terms of market share, having Coop. Italia and Conad ahead. [See Annex VI – Market Share: Table 23]

5.1.3 - Belgium

Carrefour is officially in Belgium since 2000, but in 1969 opened a store in Belgium. This store symbolizes the first step of Group internationalization. It is the third country in Europe where Carrefour has greater presence with 714 stores. In 2000, Carrefour assumed the control of GIB Group, a Belgium retailer. The revenues in 2012 were around €3.9 billion which represented an increase of 2.3%, which contrasted in general with the performance of the Europe as whole.

14

5.1.4 - Spain

The Group established in Spain in 1973, on its beginning of internationalization. On April 2007 Carrefour acquired Plus Supermercados, the Spanish operation owned by German retailer Tengelmann for €437 million.

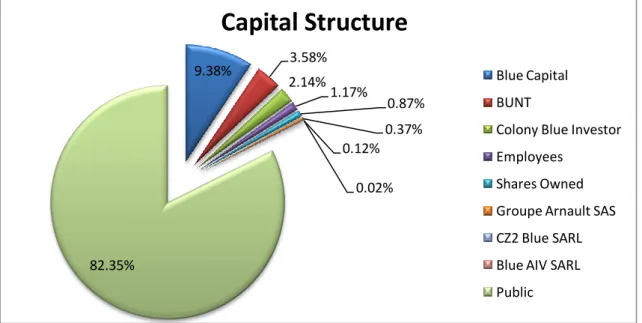

Between 2000 and 2011 the company was owned of DIA, this company was owned by Promodès until merged with Carrefour. DIA is a Spanish company and the third largest discounter group in the World, after Germans Aldi and Lidl. On July of 2011, Carrefour took the decision of executed a spin off over DIA and listed in the Madrid Stock Exchange. DIA represented

The analysts interpreted this spin off as way to calm down Blue Capital, which combines Colony Capital and Groupe Arnault, this fund owned 13.5% of the Carrefour’ capital and 20% of voting rights. The fund since 2007, lost approximately 40% of the value, which mean that this spin off would give them an extra dividend that would compensate their losses. Another explanation was the three profit warnings that Carrefour suffered since the previous year. In order to don’t harm DIA development. Carrefour came to the conclusion that separation would be the best decision. The Group was also thinking on spin off 25% of its property assets but was set aside with opposition of investors, unions and some shareholders. With such decisions, the Group has as strategy focus on its recovered.

The value transacted in DIA’ spin off was € 2.3 billion. Bellow the Carrefour valuation for the company which was around €4 billion. Carrefour shareholders received one Dia share for each Carrefour share held. In 2011 as a reflex of this sold, Carrefour distributed dividends of 807 million.

Carrefour in Spain accounts with a total of 392 stores and after France is the country in Europe where the revenues are higher, €8 billion. In 2012 the revenues fall 4.8%.

In 2011, Carrefour occupied the second place in terms of market share, just behind Mercadona, with 14%. [See Annex VI – Market Share: Table 22]

15

5.1.5 - Portugal

Carrefour initiated its operation in Portugal in 1992 with the opening of 2 hypermarkets. During 15 years, the Group increased its position with the opening of more hypermarkets.

In 1999, Dia was acquired by the Group. Dia is a Spanish company that had a leader position in hard discount on the Portuguese market. With this aggregation, Carrefour started to operate in two different areas of retailing: hypermarkets and hard discount. In terms of branding the two areas were kept separated, in the hypermarkets with name “Carrefour” and in the hard discount stores with the original name “Minipreço”.

When Carrefour merged with Promodès in 2000, the result of this merger was the creation of the second largest retailer in the World. Promodès had a minority position of 21.36% in Sonae, Portuguese retailer and market leader. Since 2000, Carrefour became the holder of that position which increased to 22.4%.

In 2004, they decided to sell the 22.4% they owned in Sonae for €345 million. Both companies were competitors in Portugal and Brazil and this position was not a strategically one and could be prejudicial for possible partnership, mainly in Brazil.

After 15 years operating in Portugal, Carrefour decided to sell the operation in Portugal in July of 2007, with the settlement of 12 hypermarkets and 9 oil stations for €662 million. On the other hand, the Group maintained its hard discount sector, with “Minipreço”.

The Group decided to focus on the markets where had a leadership or strong market share position, and exit from the countries such as Portugal where had small market share.

At this time (2007), the Group had 11 licenses approved to build new commercial spaces. Taking into account the 11 licenses approved it is a strange exit from Portugal. With these licenses, Carrefour could increase its market share. If we add the Carrefour hypermarkets with Minipreço hard discounts, the Group would achieved the third place in terms of market share.

16 In 2010, appeared the rumor on French media that Carrefour was interested to sell the 524 Minipreço stores for €800 million.

In 2011, with the Spanish DIA’ Spin-off, Carrefour exited completely from Portugal, as a result of Minipreço has always been from Dia.

5.1.6 - Poland

The Group started to operate in Poland in 1997 and is owner of 542 stores. In 2006 Carrefour acquired the Ahold Polska, the Polish operation owned by Dutch retailer Ahold, for €352 million, which held of 179 supermarkets, 15 hypermarkets and 4 oil stations.

In what concerns market share, Carrefour is far of being market leader, occupying in 2010 the fifth place, behind Jerónimo Martins, Metro Group, Tesco and Group Eurocash. [See Annex VI – Market Share: Table 24]

5.1.7 - Russia

In June of 2009 Carrefour opened its first store in Moscow, after 2 years of search in the country. Very soon another store was open and when it was supposed to prepare to open the third one, the company announced that it will leave from Russia. The analysts interpreted this decision as a result of the failure in the acquisition of Russian retailer Sedmoi Kontinent and shareholders pressure to focus on the core business (Western Europe) was the reason for exit. The reasons pointed out by the Group, were inadequate growth and lack of acquisitions opportunities. They came to the conclusion that they would not have any chances to be the largest retailer in the country. In the same year, on February Carrefour made an offer to Seventh Continent of $1.25 billion, but it was refused by the shareholders of that company. Russia is a complicated country to invest,

17 it has a lot of corruption and is very bureaucratic. Carrefour had many bureaucratic problems to open the first store in Moscow, when it did not get a license to sell alcohol, this aspect could be one more reason to exit. The company is still operating until the group find out a buyer.

Carrefour has a small presence in Turkey (1993) and Romania (2001) with more than 100 stores.

Although the small presence of Carrefour in Turkey, it is the fourth largest food retailer. [See Annex VI – Market Share: Table 25]

5.1.8 - Other Countries

In Europe there are some countries where its presence is just through franchisees such as Greece, Slovakia, Albania, Bulgaria, Macedonia and Cyprus.

5.2 - SOUTH AMERICA

Carrefour began operating in South America in 1975. Carrefour at that time was initiating its internationalization and has presence in Brazil and Argentina.

South America was the first continent where the Group invested. At that time Carrefour was a pioneer in the industry. Almost every countries in South America was underdeveloped and were facing internal conflicts with nondemocratic political regimes, which means that the multinationals were not interested to invest in this markets. The Governments had difficulties to capture foreign investments and they were very receptive to foreign investors such as Carrefour, because they knew that the presence of a Carrefour would transform food retail market in a more competitive market, it will create employee and the countries would receive foreign exchange, at the same time the consumers would have the possibility to access innovative products.

The Group began to enter in Brazil and after then it opens subsidiaries in Argentina and Colombia. The subsidiary in Colombia was close in 2007. Across the years Brazil and Argentina have gained more importance on the results of the Group. In 2012 gave a contributed of 18.5% of total sales. The sales over the years have registered a very solid growth, in 2012 this growth was 12.1%. This impressive growth was possible through the economic growth of Argentina and Brazil in the last years and the continuing

18 consolidation as the leader in both markets, acquiring local companies and grow organically.

5.2.1 - Brazil

Brazil, actually is the third largest retail market in the World, after US and China. It was the second country where Carrefour entered and started with hypermarket format. In 1975, Brazil was undeveloped, so Carrefour takes the advantage of being the first company establishing in the country and gained power in the sector whereas local retailers didn’t represented competition. In the early of 90’ decade other competitors entered in the market, notably US retailers as Wall-Mart. In 2007, the firm bought Atacadão, a Brazilian operator by €825 million. With this acquisition, Carrefour consolidated the second position in this market, just behind Brazilian Pão de Açucar. In June of 2011, Carrefour received a proposal to merge with Pao de Açucar, the merger was very close to go forward when Casino, French competitor of Carrefour and holder of 37% of Pao de Açucar opposed it.

The Brazilian market is the second most important for Carrefour behind French market, in 2012 represented 14.68% (€11.273 billion) of total sales of Group results. [See Annex VI – Market Share: Table 26]

5.2.2 - Argentina

In 1982, the Group entered in Argentina where it has 438 stores. As it happened in Brazil, Carrefour was one the first foreign company bet in Argentina, this allowed to building over the years a consolidated position as a leader of the market. On June 2012, the company acquired 129 stores of Eki, an Argentinean retailer, reaffirming the leadership in the country.

5.3 - ASIA

Asia was the last continent where Carrefour started to operate, but currently operates direct and indirect through franchises in 14 countries.

The operations in Asia are essentially in 3 countries directly, Taiwan, China and India. In Taiwan and China the business has getting bigger during the last years, it is important referred that in Taiwan as some other countries where Carrefour entered sooner the Group is one of the leaders. In India the presence is very redundant. On the Middle East

19 the presence is consummated through franchisees. The contribution of this Continent for the annual results in 2012 was 8.3% and registered a small growth of 0.5%.

5.3.1 - Taiwan

In 1989, Carrefour got into Taiwan with a local partner, Uni President Enterprises Corporation. Taiwan represented the beginning of the operations in Asia. Currently it is one of the biggest food retailers in the country with 61 hypermarkets and 3 supermarkets.

5.3.2 - China

China is the biggest economy in Asia and is facing a high economic growth in the last years, consequently an increase of population consumption. Anticipating this possibility, Carrefour entered in this market in 1995, some years before the economic “boom”. In 2000, Carrefour was considered the main foreign retailer in the country with 218 hypermarkets. In 2010 acquired 51% of Baolongcang, Chinese company that operated with 11 stores.

5.3.3 - India

The entrance in India makes part from the strategy of Carrefour of being in the emerging market called BRIC’s. India is the second most populated country in the World, so it is a market to explore. The entrance took place in 2010 through the opening of one cash & carry, since then more 3 cash & carries were opened, so until now the position of Carrefour in this country is insignificant.

5.3.4 - Indonesia

Until 2012, the Group has a joint-venture in Indonesia where it is owner of 60% in a partnership with local company, PT Trans Retail, a unit owned by CT Corp. On June of 2012 sold the 60% of its position to CT Corp. by €525 million, with this operation the Carrefour came out from Indonesia and the joint-venture become a franchisee.

5.3.5 - Other countries in Asia

As it happens in Europe, in Asia there are many countries where the Group has franchisees with special relevance for Middle East countries such as, Saudi Arabia, Oman, Jordan, Syria, Iraq, United Arab Emirates, Georgia, Kuwait, Qatar and Bahrain.

20

5.4 - AFRICA

In Africa, the presence of Carrefour is merely representative with franchisees in Morocco, Tunisia and Egypt. These countries are on the North of Africa and have the Mediterranean ocean as frontier, so they are very close to Europe. They have a higher level of development when compared with the majority of countries in Africa, but are relatively underdevelopment when compared with European countries. Egypt was a former colony of British Empire and its national languages are Arabic and English. Morocco and Tunisia were former colonies of French Empire and the national language in those countries is French and Arabic, so the relations between France and these countries are very good and across the years ended up with many French companies had open business units in those countries, in the case of Carrefour its presence is just through franchisees.

5.5 - Disposals and the European Crisis

In the last years Carrefour has entered in new markets, but at the same time left other countries. In 2005 the Group sold the businesses in Mexico and Japan, in 2006 did the same in Korea and Czech Republic. In 2007 sold the operations in Switzerland, Portugal and Slovakia. Between 2007 and 2011, the Group didn’t sell any position with exception for Thailand in 2011.

In 2012, Carrefour sold its position in some countries as Greece, with its business being sold for the insignificant quantity of €1. Indonesia, Malaysia, Colombia, Cyprus and Singapore were also sold. As I referred above, Greece, Cyprus and Indonesia are now franchisees.

The strategy behind all this disposals was the fear that a rapid expansion of Carrefour around the world, could led to a neglect situation of the main operations in Europe. These concerns started in 2007/2008 with Subprime and Lehman Brothers default, leading to a major US finance crisis which expanded to Europe in 2009, triggering Eurozone crisis in 2010 with Greek bailout. Europe, the Group strongest business area, meant 73.2% of total sales. This crisis still has strong impacts on the decrease of sales in the European countries, which means that the Group felt the need to change its strategy near the European consumers, adapting to a new reality in order to stabilize the results in those countries and consequently the global results of the company.

21

6 - COMPETITORS

This chapter is reserved to Carrefour competitors. Carrefour has many competitors, but 6 of them are the main competitors of Carrefour in global terms. Three international competitors and three local competitors were chosen.

France has a very large market and was pioneer in the retail industry with the creation of many methods and procedures that are reflect in other countries. Carrefour operations in France represented 46% of its total sales in 2012, which means that in any circumstances the French companies must be included.

Leclerc, as the main competitor in France, it was an obvious choice. Both companies fight for be the market leader, Groupe Auchan, which competes in almost every countries where Carrefour operates and finally Casino, the largest retailer of South America, where Carrefour has its second most important market, Brazil.

In which concern the international competitors, Walmart, Tesco and Metro seemed to be companies that could not be exclude from this analysis. In global terms this three companies and Carrefour make part from the restrictive group of the four largest in the World. [See Annex III – Competitors]

As these companies are huge multinationals that operate in many countries, it was quite impossible to not find in each of them a country where they operate with Carrefour.

There are other important competitors that could be referred but they are not so important than the ones mentioned above. Intermarché is a French retailer and competes with Carrefour in many other countries, Lidl, a German discount group which operates in France, Spain and Italy, very important markets to Carrefour. DIA, the discount retailer which was owned by Carrefour, it is present in Spain, France, Brazil and many other countries. Jerónimo Martins in Poland, Mercadona in Spain, Coop Italia in Italy are some of the many examples that could be provided.

6.1 - E.Leclerc

E.Leclerc is a French multinational company created in 1948 by Édouard Leclerc in Lvry-sur-Seine, close to Paris. As it happens with many companies, Leclerc is controlled and managed by the Leclerc family. Nowadays Edouard sons manage the company.

22 Contrary to other family companies it’s still a private one, which means that its shares are not traded in CAC40 or other index. The fact of being private means that it is not obliged to publish its results every quarter, semester or year, it is not exposed to market speculations and the family has 100% of the company.

Leclerc is a conglomerate, it is known by its supermarkets and hypermarkets, but also it owns gas stations, jewelry stores, travel agencies, cultural centers, etc.

Leclerc has activities in 6 countries (France, Spain, Andorra, Poland, Slovenia and Portugal).

6.1.1 - Competition with Carrefour

Leclerc compete with Carrefour in France, Spain and Poland. In the last two countries the supremacy of Carrefour is uncontested.

In France the situation is totally different, Carrefour and Leclerc are the largest operators and fight to be the leader in terms of market share. Since 1999, when Carrefour and Promodès merged, Carrefour has been the market leader, but since then, Carrefour had focused on its internationalization whereas Leclerc has the objective of being the local leader.

In May of 2012, Carrefour was the leader with 21% of market share, but registered a drop of 1.7% when compared to the previous year, in opposition Leclerc had obtain 18.5% of market share, with 1.1% of growth. The trend over the years has been Leclerc getting close to Carrefour, but as the numbers show, the possibility to surpass Carrefour is close to be a reality.

6.2 - Casino Guichard Perrachon

Casino Guichard Perrachon or well-known as Groupe Casino is a French retailer officially founded in 1898 by Geoffroy Guichard, but it is important to refer that in 1892, Guichard became the owner of a grocery store based in the Casino Lyrique cabaret in Saint-Étienne, France. Casino as a name of grocery stores seems inappropriate, but the explanation came from the store in the cabaret.

23 Casino is present in 7 countries distributed by 3 continents (Europe, Asia and South America), which make this group the third largest French retailer, next to Carrefour and Groupe Auchan, and the twenty second in the World.

The Group in Europe just operates in France, where it has many formats of stores, brands and price segments. The most well-known brands are Casino Supermarchés, common supermarkets, Monoprix which consists in stores that sell a variety of products that include food and non food products, and Franprix which are convenience stores.

South America is the continent where Casino has a higher implementation, operating in 4 countries (Brazil, Argentina, Uruguay and Colombia) and it is considered the largest retailer in this continent.

In Brazil, Casino is the main shareholder of Grupo Pão de Açucar, a consolidated Brazilian company and the largest food and non food retailer in Brazil. In Colombia, Casino is the main shareholder of Grupo Éxito with more than 50%; it is the largest food retailer in the country and has subsidiaries in Uruguay.

In Argentina, they have a subsidiary called Libertad, which is in the fourth position with 24 stores around the country, 15 of them are hypermarkets.

In Uruguay, as it happens in the other countries of this continent, Casino acquired a local company, Disco, in the 90’s and it is the leader of retail industry.

Asia is a continent to explore and Casino has business units in Thailand, Vietnam and in the Indian Ocean it has a unit in Madagascar.

In 2010, the Group acquired the Carrefour subsidiary in Thailand by €868 million for 42 stores. These 42 stores added to the ones of Casino with name Big C to a total of 111 stores.

6.2.1 - Competition with Carrefour

Casino and Carrefour as French companies compete in France, where Carrefour takes a huge advantage with more market share and stores around the country.

In South America, the two companies have subsidiaries in Argentina and Brazil. In Argentina, Carrefour has also a higher position.

24 In Brazil the competition between the French companies had hard moments in 2011, when both companies tried to take the control of Pão de Açucar.

At this time, Pão de Açucar was the second main retailer in South America. Carrefour was the main competitor and proposed to merge with Pão de Açucar, and create the largest retailer in South America, Carrefour being the main shareholder of the new company.

This merger would create a retailer with 27% of market share and sales around $40 billion.

On the other hand, Casino as a shareholder of Pão de Açucar since 1999 with initially 24% and 35% in 2005, considered this proposal hostile and illegal, as it would violate an agreement made by the shareholders in 2005. After this, Casino increased it position and currently is the main shareholder with 46.9% of the shares, 46.3% of shares are free floating.

In Asia, nowadays the two companies have activities in different countries, but in the past they competed in Thailand. As I referred above, Carrefour decided to leave and sell its business unit to Casino.

Groupe Auchan SA is French global retailer founded in 1961 by Gérard Mulliez with the opening of a store in Roubaix, district of Hauts-Champs, the name Auchan came from the same way to pronounce Hauts-Champs.

As it occur with Casino Guichard Perrachon, Auchan is a private company and still manage by Mulliez family, but as it not happen with Casino, this company put available its financial and activity report, which is not usual, but bring transparency to the company.

6.3 - Groupe Auchan

Groupe Auchan is listed in the top 10 of the largest food retailers in the World and it is the second biggest French retailer, next to Carrefour.

Contrary to other competitors that have a huge conglomerate of businesses, Auchan is completely dedicated to distribution business, more than 95% of its sales come from hypermarkets and supermarkets.

25 Auchan is present in 2 continents (Europe and Asia) and 12 countries (France, Italy, Spain, Portugal, Luxembourg, Poland, Hungary, Romania, Ukraine, Russia, China, Taiwan).

Starting from America market, Auchan already had business units in America continent. First in US in the 80’s, but as it happen with many European retailers, they end up to decided to leave, if a retailer has the ambition to cover all the country, it needs to have a large scale, so it is essential buy a local company, Auchan didn’t make it. The other problem is to face the nationalism spirit of the population because they always prefer to consume in a local shop, it is very hard for a foreigner imposed their brand in US.

In America they also has been in Mexico, but as the competitors (Wal-Mart, Carrefour and the locals Gigante and Comercial Mexicana) were so strong they took the decision to leave, in Argentina the firm has been presented some years, but in 2007 sell its stores to Wal-Mart.

In Europe, the internationalization process was normal. They started to expand to their neighbor, first Spain (1981) and then Italy (1989). In 1996 the firm expanded to Portugal, Luxembourg and Poland, since then, all the expansions were from East Europe countries, where inclusively they increased its position in 2012, with the acquisition to Metro of 91 Real stores in Romania, Poland, Ukraine and Russia, an investment of €1.1 billion.

In the end of 90’s, Auchan got in Asia, first in China (1999) and then Taiwan (2001) and more recently India (2012).

6.3.1 - Competition with Carrefour

Inside the retailers that I focus my attention, Auchan is the retailer that has more similarities with Carrefour.

With an exception to Luxembourg, Hungary and Ukraine, all the countries where Auchan operates are countries where Carrefour operates or worked in the past, cases of Portugal, Russia (it has a unit, but they are trying to find a bidder to leave).

In all the countries where both companies work (France, Italy, Spain, Poland, Romania, China, Taiwan and India), Carrefour is the leader in terms of market share and in none of them Auchan is close enough to Carrefour to conclude that each afraid the other. In

26 India I didn’t find conclusive number to observe which one has a higher market share, but I know that Carrefour has 2 cash carries and Auchan has 13 hypermarkets, for a question of size I think Auchan has a higher position, but without number I cannot justify such comment.

6.4 - Walmart

Wal-Mart Stores or more recently Walmart, is the largest retailer and private employer (approximately 2.2 million employees) in the World and the third biggest public company. This huge Empire is an American multinational created in 1962 by Sam Walton in Arkansas. In 1972, it was listed in the New York Stock Exchange.

Walmart counts with 8500 stores over 15 countries in 4 continents (America, Europe, Africa and Asia).

Inside retail industry, Walmart is in the business of discount store and warehouse stores, its customers recognized them for the low prices they practice and kindly service.

The strategy on the beginning was opening discount stores in small towns where its competitors were not interested. Walmart started to grow in the small towns without any competitors.

Sam Walton stayed as CEO until 1988. He was very rigorous with costs in order to have the lowest prices in the market, at the same time he rewarded in financial and motivation terms its employees in order to take the best of each employee and also create commitment from them.

On beginning of 90’s, they were operating in 47 states and for the first time they felt the necessity to move abroad. Mexico in 1991 was the first country where Walmart entered, after then got in Canada, Brazil, China, Argentina…in total are 15 countries.

To have a notion about the magnitude of this company, its sales are larger than the sum of Carrefour, Tesco, Metro and Kroger, which are the second, third, fourth and fifth largest retailers in the World.

6.4.1 - Competition with Carrefour

The competition with Carrefour started in the beginning of 90’, when Walmart took the decision to invest in Brazil and Argentina, countries in which Carrefour already

27 operated and later in Mexico and Japan where Walmart entered first. The highlight of this competition occurred when Carrefour merged with Promodès.

At that time, Walmart started to invest in Europe, acquiring a small German retailer and a larger British player. It was clear that the next step would be the acquisition of a French retailer. Carrefour and Promodès were not interested to be the takeover, anticipating such movement they decided to merged in order to block Walmart rush, concentrated the French market and create a large Group that would have the capacity to compete with the largest retailer in the World.

In Brazil and Argentina, Carrefour had an advantage resulted from entering in this market very early, Brazil in 1975 and Argentina in 1982, whereas Walmart entered in both markets in 1994. As Carrefour established many years before and developed its business across the years, since the beginning and nowadays Carrefour has a strong position.

Walmart entered in Mexico in 1991 through a joint venture with local company called Cifra whereas Carrefour got in 1995, in this case Walmart had the advantage of establishing 4 years before and having higher market share. In 2004, Carrefour had $605 million of revenues and Walmart had $1 billion, the competition continued until 2005, when Carrefour sold its 29 hypermarkets.

In the same year Carrefour sold the business in Japan where also competes with Walmart, the conditions were similar to Mexico, but in this unit, Carrefour was losing money and had a small position with just 7 hypermarkets. The official reason for these settlements was the decrease of market share in France, which means that they must focus in France, the main market. The analysts interpreted this sold as giving up due to the strong competition of the largest retailer in the World.

In China, Carrefour launched in 1995, a year after Walmart open its first store. As it happens in all the other countries where both companies operate or operated, the advantage to get in first always defined which one is going ahead. As Carrefour started to operate first in China, it has a higher market share than Walmart.

28

6.5 - Tesco

Tesco is a British multinational company and the third largest retailer in the World. It was founded in 1919 by Jack Cohen in Hackney, East End of London. The first store with name Tesco was opened in 1929. In 1947, Tesco went to be public in the London Stock Exchange. Nowadays, it has 530 thousands of employees all over the World.

As opposed to Walmart and Carrefour which have their own specialization, Walmart is the discount stores and Carrefour is the hypermarkets, Tesco has hypermarkets as well has supermarkets and convenience stores, there’s no predominance in any type.

Across the years Tesco has diversified the spectrum of products that offered to the costumers. Food, non food products, financial services through its Bank, telecommunications, and some other services and goods make Tesco not just a food retail company, but a conglomerate group.

In 1962, Tesco decided to expand the business outside UK, market where they are the leaders, they open a subsidiary in Dublin, after then they have been growing organically and through acquisition. In 1992, they really started its internationalization in France through the acquisition of a small retailer, called Chatteau, but in 2010 they took the decision to leave France.

After France, Tesco initiated a massive expansion, first in the Eastern countries, at that time they were growing after decades under Soviet domain, Hungary (1994), Poland (1995), Czech Republic and Slovakia (1996), in Europe they also have a unit in Turkey (2003). In the end of 90’ they turn to Asia countries, Thailand (1998), South Korea (1999), Malaysia (2002), Japan (2003), China (2004) and India (2008), all this countries with exception to Japan are growing a lot since the end of 90’. In the case of Japan, they pulled out in 2011. In the American continent, they are presented in US (2007). In total they have business units in 13 countries.

6.5.1 - Competition with Carrefour

Tesco competes direct or indirectly with Carrefour in 4 countries, Poland, China, India and Turkey. In the past they competed in Japan, France, Malaysia, Thailand, but in case of Japan both companies exited their units, in France Tesco sold the units, in Malaysia and Thailand Carrefour sold all the operations.