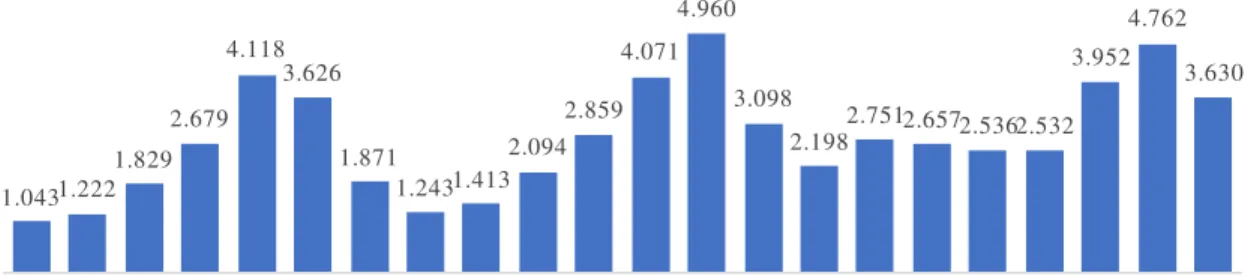

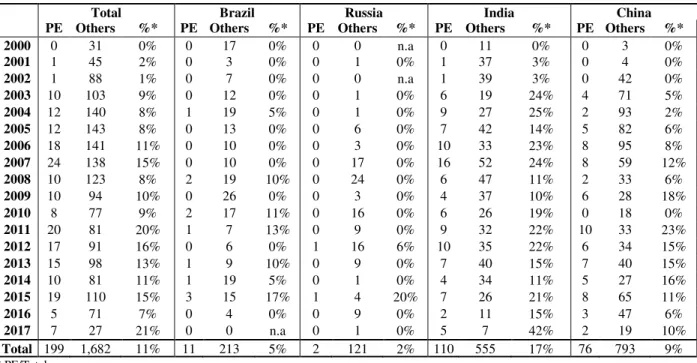

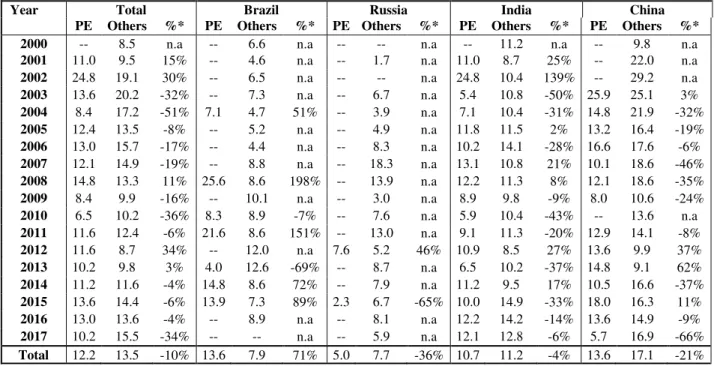

The importance of the acquisition process in Private Equity deals

Texto

Imagem

Documentos relacionados

Al realizar un análisis económico de Puebla, se busca interrelacionarlo con los niveles de competitividad, tratando de espacializar las principales actividades económicas de la

A recolha de informação teve como suporte um questionário, elaborado com base na pesquisa bibliográfica sobre a temática, constituído por questões de caracterização

Entre 1851 e 1875 deu-se um grande movimento de chineses (cules) emigrados para a América Latina, maioritariamente para o México, Chile, Peru e Cuba, em consequência

Construção de árvores filogenéticas empregando as sequências dos prováveis genes TTSS de DAEC As sequências nucleotídicas dos prováveis genes escD, espA, espD, espB, cesD2, escF

Desta forma, a despeito de sua maior visibilidade relativa quando comparado com o imposto indireto - pela diferença de magnitude, visto que a carga

Com o presente trabalho pretendeu-se contribuir para o conhecimento das condições de preparação das refeições em cantinas escolares do Município de Penafiel, através da

O questionário é composto por 04 blocos: a) Identificação do profissional – questões 01, 02, 03, 04 e 05 (abordando data de preenchimento do questionário, sexo, tempo em

(…) A arte, com o quer que a definamos, está presente em tudo o que fazemos para agradar os nossos sentidos.” Assim, a Arte permite que a expressão ocorra por uma via não- verbal, o