THE SUPERVISION OF THE CREDIT INSTITUTIONS IN

THE CONTEXT OF BASEL III IMPLEMENTATION

Ciprian-Dan Costea

“Vasile Goldis” Western University of Arad, Faculty of Economics, Satu Mare branch, 26, Mihai Viteazul street, telephone 0728727475, 0740332556, [email protected]

Abstract

In the last years, the supervision of worldwide credit institutions has been turned into a more strong one with a very clear emphasis on strengthening the capital basis of credit institutions and developing new models of supervision of the liquidity indicators, as the crisis-years run, turned to our front the importance of combining the banking management’s capital adequacy resort with the liquidity monitoring one.

Keywords: credit institutions, risk, liquidity risk, liquidity management, effective liquidity, needed liquidity

The announcement of the revised proposal for Basel III, at the end of July 2010, has brought some important changes, even though European nations such as France and Germany had a strong lobby on maintaining less strengthened proposals than on the negotiated framework, and the Basel Committee for Banking Supervision answered by reducing the number of exclusions and by accepting a more satisfying transition period. The document contains many important data that passed unnoticed in the public reports from Romania. At o first look, the document only contains settlements that generally became less strict compared to the preceding variant of the Basel document but there are some issues in the document that are not very clear but they are interesting for the bank media.

In this background we talk mainly about the direct allotting period (grandfathering) on 8 years, very unlikely to be chosen on the basis of a random factor, but rather by taking the massive repairing period, of improving the balance of accounts that most of the important international banks do now into account. And with the new set of rules that are only marginally stricter than the Basel II Agreement, it shows clearly that the central bankers are concerned– both by the global economy and by the situation of the financial system.

The main changes that the new background of the agreement brings into discussion are:

basic capital announced in December, last year: the non-tangible goods (mostly software, in terms of value) and the claims regarding the postponed excise tax. Other parts are now partially reintroduced in the rate of the basic capital, after they were initially removed: the claims regarding the postponed excise tax and the allowance of the investments in common actions of the financial institutions – anyway, for both, and the established limit is of 10% out of the component of common actions of the bank. In the capital of rank 1, the most important is the common capital, that is the investors’ payments realized in the bank business, by means of the social capital, and the rate of the common capital will have to be of 4.5% compared to 2% which is today. The implementation time will be linked to the following timetable: 3.5% starting from the 1st of January 2013, 4% starting from the 1st of January 2014 and 4.5% starting from the 1st of January 2015.

The minimum value of the basic capital increases from 4% to 6% and the implementation period is as follows: 4.5% starting from the 1st of January 2013, 5.5% starting from the 1st of January 2014 and 6% starting from the 1st of January 2015.

So, a strengthening of the basic capital of the bank is tried. From the prudential perspective we appraise the intentions of the international supervision authorities as being positive, even if the banks are not thrilled, because a strengthening of the allocations of resources as capital bases will be necessary, instead of leaving them at the bank’s disposal for commercial activities, but, as far as the capital demands are concerned, they can be decreased as there will be a severe monitoring of the liquidity.

- the redefinition of the leverage ratio: the minimum of the lever effect (the basic capital / goods) is of 3%. After the leverage effects will be followed during 4 years, starting from January 2013, a final proposal will be announced in July 2017, the new settlements will be applied starting from January 2018. There are chances that its value suffers substantial changes.

- it introduces the liquidity coverage ratio: the levels of the run-off rate were decreased, while for the borrowing rate on longer terms (net stable funding ratio), the available term for financing was prolonged. The proposal also includes an answer to the country risk that concerned the market in the last period, a reduction of 15% in certain obligations being included.

- the period of gradual introduction – approximately 8 years. The application of the new norm regarding the covering rate of the liquidity and of the lever effect will start from January 2018. The period of gradual introduction of the new settlements regarding the capital adequacy ratio is not clearly specified, but it is anticipated that a reasonable period of gradual introduction will be allowed.

- the solvability indicator will remain at the value of 8% that it has as minimum request presently.

–their earnings will just have to be revised high because, de facto, they will have to put aside less capital for reserves – the relaxation and the long implementation period of the new requests should cause concern. The fact that the relaxation is rather significant compared to the original version of the document, from December 2009, should cause long term concern in the financial sector, especially in Europe and the USA. Presently, an action of reparatory cosmetics of the balances of accounts is made in these regions, but this process can be revived in a simple manner, by taking a higher risk level and the very low rates regime of the interest into account, and it would be really tempting. On short term, it will obviously have a major effect on the unique institution both from the point of view of the perspective of earnings and from the point of view of the reparation of the balances of accounts. On long term, it attracts serious effects for a new crisis in the financial sector caused by the exaggerated assumption of the risk and, unlike the first crisis, the European and American governments are so indebted that it will be extremely difficult for them to help all the others. In fact, all these aspects can be seen starting from the summer of 2011, and they were taken into account by the entire financial world only when Standard & Poor put down the rating given to the American duties.

The new settlements regarding the lever effect and the covering rate of liquidity will become effective starting from January 2018: the revised proposal foresees that the new settlements regarding the regarding the lever effect and the covering rate of liquidity will become effective starting from January 2018. This transition period (longer than the approximately 6 years foreseen in the Basel Agreement II) seems to be determined by the lack of evidences of a real recovery of the global economy and by the actual situations from various countries, from the perspective of the difficult situation of the budget in the Western sphere. From our point of view, it should generate another type of concern, and that is the fact that the financial sector is less solvent and it will probably remain like this for many years to come, despite the results of the recent stress test, where only a few banks proved to have problems…If this hypothesis is true, a future slowing down curve in the global revival, which is talked about intensely starting from August 2011, could put the financial sector from USA and Europe under a huge pressure. But, it is to point out that banks from the Chinese cultural space strongly come from behind and they will acquire a global power. Even if at their level the Basel III practices won’t be adopted immediately for political and strategic reasons, the good prudential practices will be respected in the meaning of national settlements, and the state’s direct involvement in the holding of shares and their management will be a signal of the direction they will follow. But these banks have a formidable capacity to model and assimilate some local cultures when they have this interest, to rapidly accept the adoption of these standards when they will be present in the spaces where the effects of the background of the capital fitness is assimilated.

Still,from all modifications that Basel III brings, the introduction of the referential regarding the liquidity are the most important and they have a real

So, 2 indicators to measure the liquidity were introduced, one on short term, the other on medium and long term: the rate to cover the liquidity and the rate of the stable net resources.

The rate to cover the liquidity (RAL) includes the actives with high

liquidity level, that are not and won’t be used as collateral in view of the guarantee of some loans, or the actives that are not involved in the in the generation of derivative actives. Its role is to prevent a sudden and consistent exit of liquidities which is realized in a short term. The test scenarios on whose base the analyses regarding this liquidity rate are made stretch on the horizon of 30 days.

The calculation formula of this indicator is as follows (see: Basel Committee on Banking Supervision, Consultative Document, International framework for liquidity risk measurement, standards and monitoring):

Active stock of a high liquidity degree RAL =

---Exits of liquidities in a period of 30 days

The estimation of the exits of liquidities in a period of 30 days has to be made on the basis of a scenario realized by each bank entity. The value of the indicator has to be bigger than 1, in other words, the banks will be obliged to detain liquid actives in order to ensure them against a liquidity shock that could appear as a result of massive withdrawals in the horizon of a permanent period of 30 days. By the expression permanent period of 30 days that I recently used we want to bring into attention the dynamics of the indicator, that is the fact that the credit institutions will have to follow it permanently and whenthe manager of the credit institutions notices that the liquid actives approach the estimated threshold of exits in case of liquidity, they have to take urgent measures in order to balance the implied positions and the minimum level requested.

The hypotheses that the credit institutions have to take into account when drawing stress scenarios in order to estimate the possible exits in the horizon of 30 days are:

- the possibility of the rating reduction of the credit institution; - an exit of proportions of the retail deposits;

- the loss of important sources of financing from other deposits; - increases in the volatility of the financial markets that can affect the positions on derived instruments and a volatility of the markets that cover the accepted guarantees associated to the actives of the bank;

- massive uses of the approved but not-withdrawn credit limits; - the bank’s necessity of liquidity which derives from the necessity for control of the reputation risk;

liquidity, but there is the possibility to use a range of scenarios that can extend this basis depending on the professional reasoning of the bank management and the specific of each bank entity.

There are heated discussions in the Basel Committee regarding what needs to be added to the liquid actives. As I have mentioned, the liquid actives are the own money, short term placements, the treasury bonds with maturity of less than 1 year, the obligations and the municipal obligations with maturity of less than 1 year. In the Basel Committee it is appreciated that amongst the liquid actives are:

- the money;

- the reserves at the National Bank, until the limit at which they can be withdrawn from the Central Banks;

- bonds that can be sold, representing claims regarding or claims guaranteed by sovereign entities, Central Banks, governmental entities of public interest that are not central, the Bank of International Settlements, the International Monetary Fund, the European Commission, if the following criteria are fulfilled: they have a risk degree associated to 0% according to the Basel II classification, there is a significant reacquisition market, the bonds are not issued by banks or financial entities.

- actives representing governmental duty or duty of the Central Bank, in the national currency of the country where they activate or in the currency of the mother bank, if we talk about subsidiaries of the international banks.

Presently, the possibility of extension of these positions of actives with big liquidity there are in international debate, by including the following elements in them:

- corporate obligations: it is proposed that the value of the stock of actives of the nature of corporate obligations be decreased with values between 20% and 40% according to the rating of the corporation and

- guaranteed obligations: that is those obligations that are issued by a bank and are the legal object of a public supervision with the purpose of protecting the owner of this type of obligations, and in this case the proposal of decreasing the value of these obligation with percents between 20% to 40% remains valid.

We appreciate the efforts of the Committee for Banking Supervision as being positive, but we consider that the most liquid actives will remain the own money and the sums from the current accounts of the credit institution from the central bank, because they reflect the liquidity itself and they can’t generate liquidity loses, that is a cost who would reduce their value or the possibility of emergence of loses as a result of the capitalization at a lower price than the initial investment. This fact is possible though in the case in the case of the actions that are considered short term placements, in conditions of volatility of the markets. Their value can suffer consistent loses so there is no more predictability of the course of those bonds that even if you could make liquid, you get lower values than the acquisition price diminishing the liquidity of the credit institution that is subject of this operation in this way. For this reason, the Committee for Banking Supervision introduced that some capital bonds be considered as actives with high liquidity degree among the requests, request that in the history of the last 10 years or in periods of stress of markets a difference of more than 40 basic points hadn’t existed (for example in the case of corporate or guaranteed obligations, as haircut, that is the decreasing of value to be realized with a correction coefficient of 20%) between the asked priced and the offer price, in other words between the bid-ask quotation on the screen of the stock market.

As far as the liquidity exits are concerned, the term of net liquidities exits (ENL) is reflected by the difference between the cumulated money exits (EL) and the cumulated entries (IL) of money in profiled stress parameters and the established time horizon, for example, the recommended duration of 30 days.

So,

ENL = EL– IL

In the hypotheses to construct the scenarios that affect the exits of liquidities, we have the drastic reduction of retail deposits. The Committee for Banking Supervision considers that the retail deposits have to be deprived on two landings (see: Basel Committee on Banking Supervision, Consultative Document, International framework for liquidity risk measurement, standards and monitoring): - stable deposits that will have to be considered that they have migration potential outside reflected by the adjustment coefficient of 7.5%. It is also appraised that these deposits are owned by the clients that have a special relation with the bank, retrieving now, the correlation with the aspects that we specified when characterized above in our research the stable deposits.

- unstable deposits, to which a bigger migration coefficient is associated, of 15%, and that present a higher potential to generate liquidity exits from a bank entity in this way.

pieces of information from the annual financial situations and reasoned by the management of the credit institutions. We agree that this be done, which is the responsibility of the National Bank, but we don’t consider that a segmented approach from the perspective of the difference between the deposits in Lei and those in currencies is necessary in our country because the Romanians still have confidence in currencies such as EURO, USD in order to save money. The possible migrations in the conditions of the decreasing of the value of the mentioned values will be able to take place by the conversion of these deposits into deposits in the national currency.

The loss of some important sources of financing from other deposits refers to the money exits that appear from the deposits constituted by the non retail clients and that don’t have guarantees through which the banks prevent their migration attached. In the case of the clients from small and medium sized companies, the approach will be identical to that of the retail deposits, implying the same diminishing coefficients; we will have a migration coefficient of 25% in the case of the deposits constituted by corporate institutions, sovereign funds, central banks, international institutions, entities of public interest, and if the funds are not kept in the accounts of the credit institution for operational purposes we will have the 75% coefficient, a fact that reflect the bigger migration possibility of those resources. The coefficient fully covers the value of the resources, reflecting the possibility of their immediate use by these clients in the case of funds coming from banks, insurance societies, special vehicles like those operating with derived instruments.

The volatility of the markets affects the liquidities as I have mentioned but the capacity to liquidize is not affected in the case of some instruments owned by the banks, and the risk of random production of a phenomenon of liquidity exit is excluded, in this case the example being the owned government bonds, and other bonds that can be sold by the nature of the actions that the credit institutions have in their portfolio.

at its disposal in the calculation of the money entries, a fact that is totally justified from our point of view, for safety reasons.

The rate of the stable net resources is that indicator that additionally

introduces a liquidity control on medium and long term. By means of this indicator, the Committee for Banking Supervision proposes itself to establish the necessary minimum level of liquidity starting from the liquidity characteristics of the bank actives, in the horizon of a calendar year, so of a annual financial exercise. The necessity of the emergence of the control of the stable liquidity appeared as a result of the manifestation of the financial crisis, and it is hoped for that a correlation between the actives and the realized investments, even in the derivation instruments and the resources that represent the basis for the financing of the activity exists in each credit institution through this indicator.

The net stable funds (NFS) is calculated as report between the stable financing resources (RSFD) and the necessary for financing on medium and long term (NFML) (see: Bank for International Settlements, Basel Committee on Banking Supervision, Consultative Document, International framework for liquidity risk measurement, standards and monitoring, April 2010):

RSFD

NSF = --- * 100, NFML

It is asked that the value of this indicator be bigger than 100%.

The available stable resources for financing reflect the sum between the own funds and the obligations that have a date of payment bigger than 1 year, also including here the quota from the stable deposits that have maturity bigger than 1 year and that are expected by means of the exercise of professional reasoning of the managerial team to remain at the bank’s disposal more than 1 year. The role of this indicator is to offer a measure of the stability of the liquidity of a credit institution, in conditions of stress scenario which supposes that the bank faces and the investors and the client become concerned by:

- a significant profitability decline, even the emergence of loses, as a result of the accentuated manifestation of the credit risk, the operational one, the market risks and other risks that affect the bank entities;

- the possibility of the decrease of the rating of the credit institution by a significant and internationally recognized rating agency;

- other events that question the bank’s reputation or its attitude as borrower.

coefficient is defined by the supervision institution, reflecting the quota of the actives that needs to be covered with stable resources. The rule is that as the liquidity degree associated to the active is bigger, the value of the coefficient decreases. It is appreciated that these coefficients are parameters that approximate the quota from a bank active that cannot be monetized by capitalization in the form of sale, of use as collateral in an accepted estimation period and established at 1 year.

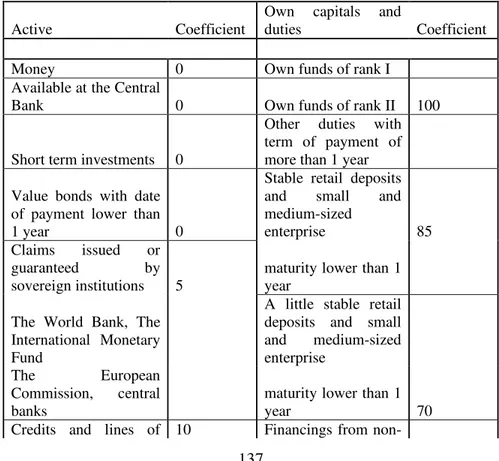

In the analysis of the rate of the stable net resources, the contraposition of the elements of the active with those of the own capital and duties, adjusted with the afferent coefficients in order to determine the net value, are of a very big importance. This analysis is equivalent to the analysis of the working capital from the firms’ micro-economy. So, we will try to counter the elements of the active with those of the own capital and duties, on the basis of available data, to reflect the adjustment coefficients established by the Basel Committee on Banking Supervision (see table number 1).

Table number 1. The available stable resources for financing and the necessary of financing on medium and long term

Active Coefficient

Own capitals and

duties Coefficient

Money 0 Own funds of rank I

Available at the Central

Bank 0 Own funds of rank II 100

Short term investments 0

Other duties with term of payment of more than 1 year

Value bonds with date of payment lower than

1 year 0

Stable retail deposits and small and medium-sized

enterprise 85 Claims issued or

guaranteed by sovereign institutions 5

maturity lower than 1 year

The World Bank, The International Monetary Fund

A little stable retail deposits and small and medium-sized enterprise

The European Commission, central banks

maturity lower than 1

year 70

non-credits, other facilities that are

financial corporate partners

Approved and not withdrawn

term of payment lower than 1 year 50 Corporate

unencumbered property obligations 20

The other duties and own capitals 0 with maturity bigger

than 1 year

Minimum rating AA Listed bonds and corporate obligations 50 unencumbered property with maturity bigger than 1 year

1 year and minimum rating

A-Gold 50

Corporate credits with maturity lower than 1

year 50

Retail credits with maturity lower than 1

year 85

The other actives 100

Source: Bank for International Settlements, Basel Committee on Banking Supervision, Consultative Document, International framework for liquidity risk measurement, standards and monitoring, April 2010.

He also reaffirmed thatthe liquidity and not the capital level remains the

decisive factor for the survival of a bank in a crisis period. Two years after the

collapse of the American giant Lehman Brothers, Treichl reminds that the bank had a capital rate of the rank 1 of 11% and it still didn’t make it, so it was not the lack of capital that generated the world economic crisis.

Also linked to the issue of the new agreement that regulates the banks’ capital, the request concerning the conservation reserve of the capital of 2,5% from the total actives, created important debates, because the creditors won’t be able to build this reserve and they won’t be able to pay their dividends. So, a remark that James Wiener, director of the finances and risk practices department of the consultancy firm Oliver Wyman, made is interesting (see: www.zf.ro, 14.09.2010, the article “Will the financial world be a safer place after the harshening of the capital requests? But won’t the rates be affected?): there are substantial modifications concerning the capital requests. The adjustment period to these rules is big, which means that a part from the pressure disappears. But even so, who would want to own a bank that can’t pay its dividends for, let’s say, 3 years? Other novelties regarding the Basel III agreement is the taking of the term institutions of systemic importance into account, even if a possible different application of some standards at their level can’t be realized yet, and also the fact that this agreement doesn’t make a difference between commercial banks and investment banks, and such an approach would represent a progress.

The way in which the settlements will be implemented is very important, having in view the fact that Basel III does not make difference between the classical, commercial banks and the banks that made financial schemes. In Romania’s case, the impact of Basel III will be indirect but it can be quite consistent, influencing the economy more or less.

In the end we have to point out the conclusion that we consider basic: Basel III extends the applicability area of the banking supervision in the most important sphere of the banking management, the liquidity, for the first time, an element on which all pieces of information that are furnished by the credit institutions and an element that is the result of all reached decisions are linked. So, the liquidity in the banking sector is both cause and effect, the liquidity is linked both to the bank actives and to the own capitals and duties and so it has to be a base of all decisions that the management of the credit institutions reach.

Bibliography

Costea Ciprian Dan, Hostiuc Florin, The liquidity ratios and their significance in the financial equilibrium of the firms, The Annals of the Stefan cel Mare University Suceava, volume 9, no. 1(10), 2009

Daschievici Anisoara Niculina, Managementul riscului de lichiditate, pe www.oeconomica.uab.ro,

Basel Committee on Banking Supervision, Consultative Document, International framework for liquidity risk measurement, standards and monitoring

Bank for International Settlements, Basel Committee on Banking Supervision, Consultative Document, International framework for liquidity risk measurement, standards and monitoring, April

***Situatiile financiare intocmite de Banca Transilvania S.A.,

***Regulamentul Bancii Nationale a Romaniei numarul 24 din 15 decembrie 2009 privind Lichiditatea institutiilor de credit,

***www.bnro.ro ***www.bis.org