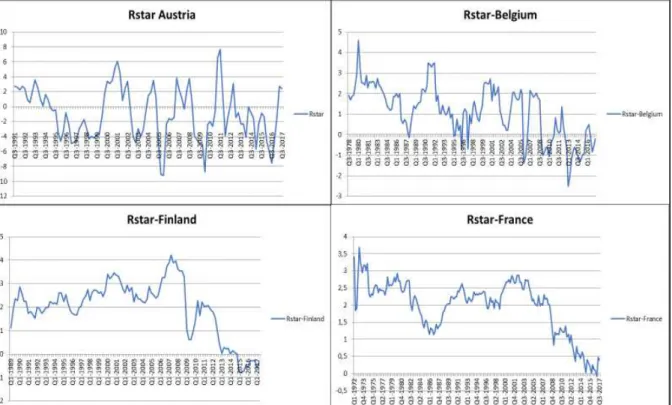

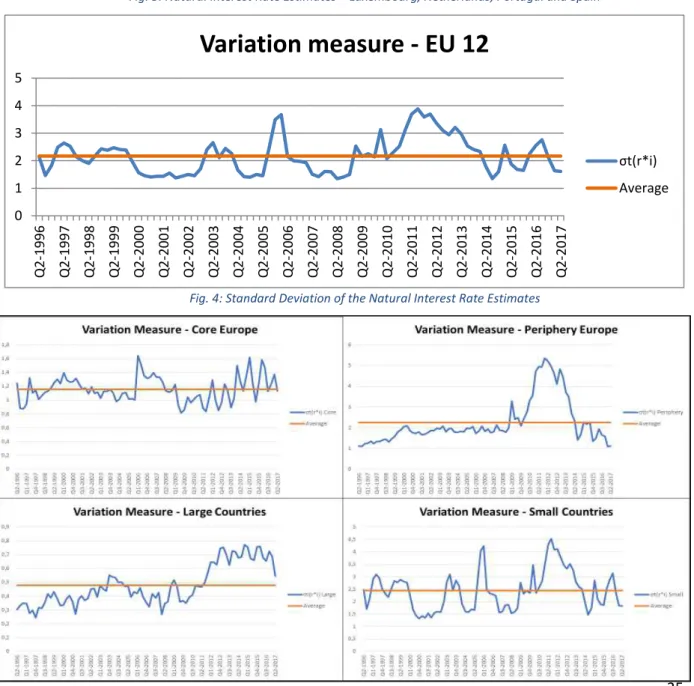

Differences in Natural Interest Rates in the Eurozone

Texto

Imagem

Documentos relacionados

As principais conclusões deste trabalho são de que: a) as referências teóricas analisadas indicam que o movimento em prol do desenvolvimento social pode ser considerado uma ação

Extinction with social support is blocked by the protein synthesis inhibitors anisomycin and rapamycin and by the inhibitor of gene expression 5,6-dichloro-1- β-

Objectivos: sensibilizar os alunos, do curso de licenciatura em Terapêutica da Fala da Faculdade de Ciências da Saúde da Universidade Fernando Pessoa - Porto, para a importância

The data revealed that the informal caregivers presented higher levels of emotional distress, feelings of sadness and daily working hours (19.8 hours) compared to the

Sendo o acesso ao transporte público realizado maioritariamente através do modo pedonal, na maior parte das cidades europeias e, inclusive em Madrid, torna-se

Com a elaboração da Política Nacional de Habitação ( pnH ) em 2004 (definindo as diretrizes e instrumentos), do Sistema Nacional de Habitação em 2005 (estruturado a partir de

Os debates foram moderados por Miguel de Castro Neto, Subdiretor da NOVA IMS – Information Management School e Coordenador da NOVA Cidade – Urban Analytics Lab, e tiveram

According to Nelson and Plosser, and now using the Beveridge-Nelson decomposition, this means that the Por- tuguese output has a stochastic Trend and a small