The effect of organizational studies on financial risk measures estimation

Texto

Imagem

Documentos relacionados

On analyzing the association between malnu- trition risk and hospitalization, we observed that the frequency of malnutrition and risk of malnu- trition was twice as high in the

Essa ideia da intermitência, por sua vez, como modulações da toada, aparece também no fragmento de mundo chamado “Balada da Rua da Conceição”. Bacellar dá um tom mais

The probability of attending school four our group of interest in this region increased by 6.5 percentage points after the expansion of the Bolsa Família program in 2007 and

Thus, it is presented in the study a theoretical fuzzy lin- guistic model to estimate the risk of neonatal death based on birth weight and gestational age.. Fuzzy

Posteriormente, houve outra tentativa de elaboração de uma política nacional de saneamento através da elaboração do projeto de lei (PL) 4.147/2001, que entre outras

As intervenções multidisciplinares devem ser centradas no doente, ou seja, mesmo doentes com a mesma doença irão experimentar dificuldades muito diferentes relacionadas com

No entanto os efeitos estão directamente relacionados, não apenas com a substância em si, mas também com a sua quantidade e qualidade, bem como com as características

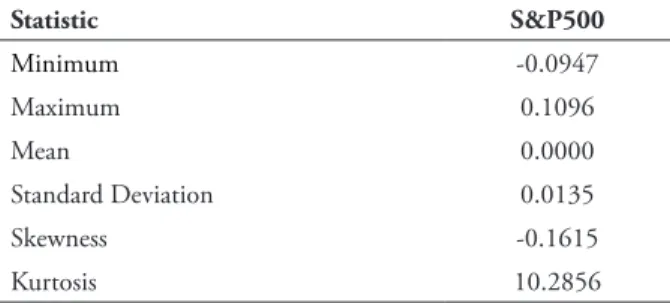

Analysis of the risk factors that determined the portfolio’s ex-ante absolute and relative risk, based on their contributions to risk (%) provided by the Bloomberg factor model..