Professional paper

Ivana Prica

Faculty of Economics, University of Belgrade, Serbia

Jelica Petrović Vujačić

Faculty of Transport and Traffic Engineering,

University of Belgrade, Serbia

Financial Services Liberalisation in

Transition Countries and the Role

of the WTO

Summary: While a bulk of economic theoretical and empirical research deals

with various aspects of financial liberalisation, there is far less research de-voted to the measurement of financial liberalisation. In this paper we calculate an index of financial liberalisation in 18 transition countries in the Central, East-ern and South-East Europe (CESE) and the Commonwealth of Independent States (CIS). This index was previously developed in works of Aaditya Mattoo (1999) to measure financial liberalisation that the WTO member countries have committed to. We make a slight modification to scaling to take into account the specific aspects of CESE and CIS countries and also apply the index to a non-WTO member (Serbia) using its currently applied regime. In this paper we will examine the influence of the General Agreement on Trade in Services (GATS) framework on liberalisation commitments in financial services sector in the target countries.

Key words:Financial services, Financial liberalisation, Transition, WTO.

JEL: G15, G21, G22, G28.

1. The General Agreement on Trade and Services (GATS)

GATS was negotiated during the Uruguay Round (1986-1994) and is the first and only set of multilateral legally-enforceable rules that govern international trade in services of 149 country-members. Similar to the General Agreement on Trade and Tariffs (GATT), GATS encompasses the following three elements: general rules and disciplines, Annexes to regulate sector specificities and the Schedule of Specific Commitments that show specific obligations a particular Member has undertaken in the particular service sector. Unlike GATT, GATS has a specific fourth element: List of Article II (MFN) exemptions. This list shows the sectors in which the Member is temporarily not going to apply the Most-Favoured Nation (MFN) principle of non-discrimination legally-enforceable rules that govern international trade in services of 149 country-members. Many countries have made use of this exemption: the EU for audio visual services, non-life insurance and canal transportation, the US for finan-cial services and pipeline transportation and most OECD countries for air-transportation.

The generally accepted definition of trade in services, as provided in Article I, Paragraph 2 of the GATS, recognizes this specific aspect of services and defines trade in services by way of four services supply modes:

Mode 1: Cross-border Supply – The services are delivered across the coun-try border, the service provider resides abroad while the consumer remains in the home country, similar to trade in goods (e.g., when financial credit is extended or insurance policy purchased from a bank/insurance company located abroad);

Mode 2: Consumption Abroad - The consumer travels into the country in which the services are delivered by the foreign services supplier (e.g., ob-taining financial services when travelling abroad);

Mode 3: Commercial Presence - Service supplier of one country supplies a service in another country by establishing, through foreign investment, a commercial presence in that country (e.g., commercial presence of foreign banks or insurance companies);

Mode 4: Presence of Natural Persons - This applies to the temporary movement of individuals (which are natural, not legal persons as is the case in the previous mode) and arises when a service is delivered in a for-eign market; these individuals may be independent service providers (such as consultants), or foreign employees of a service-supply company (e.g., solicitation on domestic territory of insurance products by agents from a foreign country, foreign manager of a domestically-established bank).

According to Rudolf Adlung and Martin Roy (2005), the estimates of the Sta-tistical Division of the WTO Secretariat are that mode 3 (commercial presence) has more than 50% share of total service trade value, while mode 1 (cross-border supply) and mode 2 (consumption abroad) account for 30% and 15% of the total value of service trade.

of tariff protection. The application of the GATS is not confined to product-related measures, as provided for under the GATT, but covers producer-related laws and regulations as well, as discussed in Adlung and Roy (2005). Counterbalancing its broader coverage in terms of economic transactions and permissible policy measures, GATS allows use of virtually any conceivable trade instrument (from supply quotas to discriminatory subsidies).

The level of the foreign trade in services liberalisation is weighed against the restrictions of Market Access (MA) or National Treatment (NT) for each of the four service supply modes and for every service sector. Concrete liberalisation commit-ments of a WTO member country, defined against this framework, are entered into that country’s Schedule of Specific Commitments (the Schedule) related to GATS, through which it commits to a particular level of liberalisation in trade in services. The MA and NT commitments are scheduled applying the positive listing approach. Only those sectors specifically listed are covered by the liberalising provisions in the Schedule.

We have examined WTO commitments in financial services in 17 CESE and CIS countries that are WTO members. This analysis encompasses the following fi-nancial service sectors:

i. Insurance and insurance related services, i.e. (i) to (iv) according to the An-nex 5.(a);

ii. Banking services, which comprise sub-sectors (v) to (ix) in 5.(a) of the An-nex; and

iii. Other financial services (securities, money broking asset management etc), or sub-sectors (x) to (xvi) of the Annex 5(a).

Only the first three modes of supply, cross-border, consumption abroad, and commercial presence, were taken into account. Limitations to mode 4 (movement of natural persons) are based on different set of regulations and the scope of mode 4 is not at all significant for the financial services sector. Residency requirements for employ-ees and management bodies that were listed as mode 3 limitations in some Schedules were not taken into account either.

2. Numerical Evaluation of the Financial Services’ Liberalisation

Scope

The commitments in the banking and insurance sectors summarized in Table 1 were used to calculate the liberalisation indices in financial services sector. This was per-formed using the methodology that was first developed by Mattoo (1999) and conse-quently applied in a number of studies, such as Mattoo, Randeep Rathindran, and Arvind Subramanian (2001), Alexei Kireyev (2002), Ramkishen S. Rajan and Gra-ham Bird (2002), Rajan and Rahul Sen (2002), Phillipp Harms, Aaditya Mattoo, and Ludger Schuknecht (2003), and Li-Gang Liu (2005).

with the above analysis and in accordance with the model set out in Mattoo (1999). Regarding Serbia, since it is not a WTO member (hence does not have a Schedule) the liberalisation indices were calculated on the basis of its currently applied regula-tory regime. On one hand, this means that without changing the current regime, Ser-bia cannot have a higher liberalisation index. On the other hand, it is possible and quite probable that during negotiations for accession Serbia would be expected to commit to a higher level of liberalisation compared to the current regime, meaning that the WTO membership would result in a higher liberalisation index (effectuated by the appropriate regulatory change). In short, results for Serbia would not be di-rectly comparable to those of the other countries if the currently applied regime in those countries significantly differs from the commitments in their respective Sched-ules.

2.1 Methodology

The liberalisation index created by Mattoo, and used in this research, belongs to a class of frequency measures of a degree of services liberalisation. These measures were originally constructed simply to reflect the frequency of appearance of commitments in the WTO Schedules and have since evolved in two directions. These are: (1) creation of sophisticated scales of restrictiveness to capture different types of restrictions and to provide adequate measure of the level of restrictiveness of each (sector-specific) meas-ure; and (2) development of different weighing schemes to form an adequate aggregate measure.

One of the first researches to develop a sophisticated frequency measure for fi-nancial services sector is that of Mattoo (1999). He created a liberalisation index, sepa-rately for banking and insurance sectors, which runs in the interval [0,1]. The index is calculated based upon the WTO commitments by identifying the most restrictive measure by mode of supply and by service sub-sector. Each measure is then assigned a restrictiveness score, according to a restrictiveness scale that was developed to capture the specificities of both the observed sectors and the country pool. Each restrictiveness score is then weighted, using weights to capture the relative importance of a particular mode of supply of a particular sub-sector, to obtain a sector-specific aggregate measure dubbed the liberalisation index.

The scope of analysis is limited to two sub-sectors of direct insurance: life in-surance and non-life inin-surance, and two sub-sectors in banking: acceptance of depos-its and other repayable funds from the public (acceptance of deposdepos-its), and lending of all types including consumer credit, mortgage credit, factoring and financing of com-mercial transactions (lending).

many countries impose restrictions on legal form of entry—e.g., it is required that a domestic entity be founded (no business can be conducted through affiliate offices) and the appropriate score value is 0.75.

After we assigned the restrictiveness score for each of the two types of ser-vices and for each of the three supply modes investigated, what we needed was a suitable means (e.g., weighting scheme) to aggregate the data.

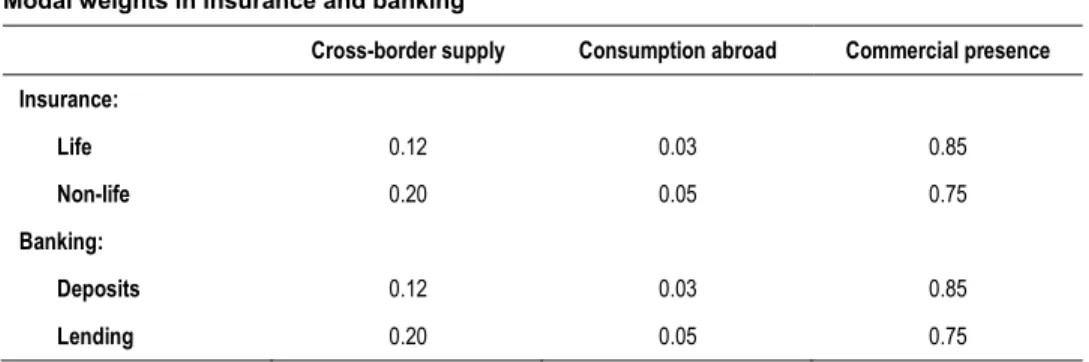

The weighting scheme, which is supposed to define the relative significance of each of the studied service categories, was calculated based on USA foreign trade data. While the restrictiveness scale we developed (see Table 1) is somewhat different to that of Mattoo, the modal weights are the same as the ones employed by this re-search. Both of these are described in Table 1.

Table 1 Modal Weights and Restrictiveness for Calculation of the Mattoo Index of Liberalisation in

Financial Services

Modal weights in insurance and banking

Cross-border supply Consumption abroad Commercial presence

Insurance:

Life 0.12 0.03 0.85

Non-life 0.20 0.05 0.75

Banking:

Deposits 0.12 0.03 0.85

Lending 0.20 0.05 0.75

Restrictiveness scale by commitment type for modes 1, 2 and 3

Restrictiveness score

Limitation type

Modes 1 and 2 Mode 3

0.00 No, or virtually no commitment No commitment, or virtually no commitment

0.10 - No new entry or unbound for new entry

0.25 - Discretionary licensing or economic needs testing for new entry

0.25 - Reciprocity condition

0.50 Partial liberalisation Exemption of certain sub-sectors (e.g., exclusive suppliers)

0.75 - Limitation on the legal form of entry

0.75 - Other minor limitations

1.00 Full liberalisation Full liberalisation

3. Results of Application

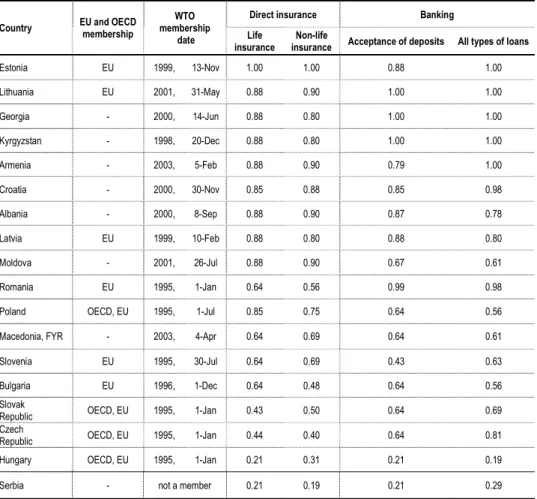

Mattoo liberalisation indices calculated as explained above run in the interval [0,1], where 0 represents the particular sub-sector being fully closed and 1 represents full liberalisation on all modes of supply. By aggregating the scores using the modal weights, we have calculated four separate liberalisation indices for two groups of in-surance services: life inin-surance and non-life inin-surance, and for two groups of bank-ing services: acceptance of deposits and lendbank-ing. We have applied the approach to the information on commitments in 17 countries in Table 2 in the Appendix and on the information on the Serbian applied regulatory regime. The results are presented in Ta-ble 3 in the Appendix. Here we have ranked the countries according to their total liber-alisation level, so that the first country, Estonia, has the most liberal, and the last coun-try, Hungary, the least liberal WTO regime for trade in financial services.

Serbian index calculated upon its current applied regime is listed last and is the lowest. Serbia maintains significant limitations on cross-border transactions (no life insurance, almost no non-life insurance as well as no bank-deposits abroad). In addi-tion, it has discretionary licensing requirements for establishing a bank or an insurance company. The main reason for this is the reluctance on the part of the government to liberalise these sectors further on the arguments of the unfinished financial regulatory reform, weak oversight structures and incomplete privatization of the sector.

Finally, using the two indices for each sector, we calculated a simple average for insurance services and for banking services. This result is outlined in Figure 1, where countries are ranked by their date of accession to the WTO such that the left-most countries, Czech Republic, Hungary, Romania, Slovak Republic, Poland and Slovenia, are the original members, followed by Bulgaria (which acceded in 1996, but submitted its Schedule in 1997), and ending with Macedonia as the country that among the WTO members acceded last. On the right end of the figure is Serbia which had begun the process of WTO accession.

Source: Authors’ calculations based on the methodology developed in Mattoo (1999).

Figure 1 Mattoo Liberalisation Indices for Banking and Insurance in CESE and CIS

0.00 0.20 0.40 0.60 0.80 1.00 C zech R epubl ic H ungar y Pol and R om ani a S lovak R epubl ic Sl oveni a Bul gar ia K yr gyzst an Lat vi a E st oni a G e or gi a A lbani a C roat ia Li thuani a M ol dova Ar m eni a M ace doni a,

FYR Serbi

a

insurance

As previously discussed, CESE and CIS countries have much more liberal commitments in mode 3 (commercial presence) than in modes 1 and 2. When analyz-ing the results in Table 3 and Figure 1, it is important to bear in mind that mode 3 also has the highest impact in the calculation of the Mattoo liberalisation index. For that reason the penalty impact of MFN exemption in case of Hungary was a very low liberalisation score. They are joined by Serbia which has discretionary licensing pro-cedures for establishing foreign commercial presence.

The results listed in Table 3 in the Appendix show that at the bottom of the ta-ble, with the lowest liberalisation scores, are only the original WTO members and Bulgaria which joined only one year after (plus Macedonia which has pre-committed to future liberalisation in 2008, when its score will be in the upper half of the table). The newly acceded WTO members including all CIS countries are at the top of Table 3. This finding, that the newly acceded members have a higher liberalisation score, is more obvious in Figure 1, where countries were ranked by the date of WTO mem-bership.

The fact that the lowest scored are the original WTO members and also the most developed countries in the pool, clearly points to the possibility that actually applied regulatory regime in those countries may be more liberal than their GATS commitment (autonomous liberalisation). As Table 3 and Figure 1 show, OECD and EU member-countries: Czech Republic, Hungary, Poland and Slovak Republic are among the lowest-ranked. Yet those countries have liberalised their policies in order to achieve OECD and EU requirements. This conclusion is in accord with the find-ings of Felix Eschenbach and Bernard Hoekman (2006), who analyzed the overall GATS commitments of CESE and CIS countries and the EU commitments and com-pared their GATS commitments to the actually applied policies in the service sector as a whole. They find that all countries that had the prospect of accession to the EU apply much higher overall level of services liberalisation than the level they commit-ted to in GATS. In our analysis of the financial services sector this result applies only to the countries that were the original members. Countries that only recently acceded to the WTO (which precedes EU accession) and soon after became EU members have already committed to a high liberalisation level in financial services in GATS.

The highest financial services liberalisation indices in Table 3 are those of two EU member countries (since 2004): Estonia and Lithuania. These are followed by three CIS countries: Georgia, Kyrgyzstan and Armenia. The country’s size and/or the size of the financial markets also play an important part in the decision to liberalise. Asli Demirguc-Kunt (2006) finds that small financial systems tend to under-perform since they “fall short of minimum efficient scale and have much to gain from liberal-ising and sourcing some of their financial services from abroad.” All the countries with the highest financial services’ liberalisation index in Table 3 fall in this cate-gory. This may partially explain why their governments were willing to accept such high level of commitment in financial services.

“undertaken major liberalisation efforts in their WTO accession processes and had little or no margins for further flexibility” (International Centre for Trade and Sus-tainable Development 2003). This also underlines the fact that the WTO structure and accession negotiation procedure demands increasingly higher levels of commit-ments from the prospective members. Furthermore, Eschenbach and Hoekman (2006) find that in five countries, namely Armenia, Georgia, Kyrgyzstan, Moldova and FYR Macedonia, the actual applied regime in all service sectors is less liberal than their GATS commitments.

Eschenbach and Hoekman (2006) also compared CESE and CIS country rank-ings according to the GATS commitment index (for total services) and according to the EBRD Services Reform Index (EBRD Index), which measures the success of overall services policy reform. While ranking according the GATS commitment in-dex for all services is similar to our ranking of financial services in Table 3, the rank-ing accordrank-ing to the EBRD Index is almost reversed. Here Hungary has the highest score, followed by Poland, Estonia, Czech Republic and Slovenia. The EBRD index is lowest for Kyrgyzstan, followed by Georgia, Moldova and Armenia, which are all CIS countries that fare among highest in our financial services sector liberalisation index in Table 3.

4. Conclusion

In this paper we have examined liberalisation commitments of WTO member coun-tries in CESE and CIS in financial services sector. We conclude that of the three fi-nancial services sectors, insurance, banking and others (securities), banking is the most liberal sector according to the WTO commitments, which is also the most de-veloped of the three financial services sectors in CESE and CIS countries. The level of commitment seems to be lowest for insurance sector, where a few countries schedule exclusive provision of mandatory insurance schemes in mode 3, and only one allows cross-border life insurance services.

While all countries have achieved a high level of liberalisation in mode 3 (commercial presence) except for Hungary, Slovenia and Serbia, most of them main-tain some level of capital mobility limitations and modes 1 and 2 are more restricted. Liberal scores on mode 3 especially in banking signal the countries’ recognition of the positive role foreign banks may play in domestic financial system and find that to be an important vehicle for achieving internal competitiveness. However, fewer countries were willing to allow cross-border branching (whereby achieving full liber-alisation in mode 3). This signals that these countries may not be willing to commit to a higher level of external exposure. However, for some countries that are OECD/EU members, the actual level of liberalisation is higher than their GATS commitments. In other CESE countries, this is an indication that the financial ser-vices industries are still relatively under-developed and wish to establish internal competitiveness before being exposed to international competition.

presents an important drawback for GATS which in its successive negotiation rounds still proves to be unable to capture this liberalisation level. In fact, at one point it was hoped that “a nice outcome in services would be one in which members bind autonomous liberalisation which they have carried out since the conclusion of the Uruguay Round of trade negotiations a decade ago” (from interview of Amb. Fer-nando de Mateo y Venturini, Chairperson for services negotiations, in Washington Trade Daily, 2/13/07).

References

Adlung, Rudolf, and Martin Roy. 2005. “Turning Hills into Mountains? Current

Commitments under the GATS and Prospects for Change.” World Trade Organization Economic Research and Statistics Division, Staff Working Paper ERSD-2005-01.

Barth, James R., Juan A. Marchetti, Daniel E. Nolle, and Wanvimol

Sawangngoenyuang. 2006. “Foreign Banking: Do Countries’ WTO Commitments

Match Actual Practices?” World Trade Organization, Economic Research and Statistics Division, Staff Working Paper ERSD-2006-11.

Beck, Thorsten, Asli Demirguc-Kunt, and Maria Soledad Martinez Peria. 2005.

“Reaching Out: Access to and Use of Banking Services Across Countries.” World Bank Policy Research Working Paper 3754.

Claessens, Stijn. 2006a. “Current Challenges in Financial Regulation.” World Bank Policy

Research Working Paper 4013.

Claessens, Stijn. 2006b. “Competitive Implications of Cross-Border Banking.” World Bank

Policy Research Working Paper 3854.

Demirguc-Kunt, Asli. 2006. “Finance and Economic Development: Policy Choices for

Developing Countries.” World Bank Policy Research Working Paper 3955.

Eschenbach, Felix, and Bernard Hoekman. 2006. “Services Policies in Transition

Economies: On the EU and WTO as Commitment Mechanism.” World Bank Policy Research Working Paper 3951.

Harms, Philipp, Aaditya Mattoo, and Ludger Schuknecht. 2003. “Explaining

Liberalisation Commitments in Financial Services Trade.” World Bank Policy Research Working Paper 2999.

International Centre for Trade and Sustainable Development - ICTSD. 2003. Bridges

Weekly New Digest. Geneva: ICTSD.

Key, Sydney J. 2003. The Doha Round and Financial Services Negotiations. Washington

D.C.: The AEI Press, American Enterprise Institute.

Kireyev, Alexei. 2002. “Liberalisation of Financial Services Trade and Financial Stability: An

Analytical Approach.” IMF Working Paper WP/02/138.

Liu, Li-Gang. 2005. “The Impact of Financial Services Trade Liberalisation on China.”

Research Institute of Economy, Trade and Industry, RIETI Discussion Paper Series 05-E-024.

Mattoo, Aaditya. 1999. “Financial Services and the World Trade Organization, Liberalisation

Commitments of the Developing and Transition Economies.” Development Research Group, World Bank Policy Research Working Paper 2184.

Mattoo, Aaditya, Randeep Rathindran, and Arvind Subramanian. 2001. “Measuring

Services Trade Liberalisation and its Impact on Economic Growth: An Illustration.” World Bank Research Working Paper 2655.

McGuire, Greg. 1998. Australia’s Restrictions to Trade in Financial Services. Canberra:

AusInfo.

Organization for Economic Cooperation and Development - OECD. 2003. “Comparative

Eastern Europe Regional Programme, Forum on Trade in Services in South Eastern Europe and Vienna Institute for International Economic Studies. Paris: OECD.

Rajan, Ramkishen S., and Graham Bird. 2002. “Will Asian Economies Gain from

Liberalising Trade in Services?” Journal of World Trade, 36(6): 1061–1079.

Rajan, Ramkishen S., and Rahul Sen. 2002. “Liberalisation of International Trade in

Financial Services in South East Asia: Indonesia, Malaysia, Philippines and Thailand.” Centre for International Economic Studies, University of Adelaide Discussion Paper 0217.

Warren, Tony, and Christopher Findlay. 2000. “How Significant are the Barriers?

Measuring Impediments to Trade in Services.” In Services 2000: New Directions in

Services Trade Liberalisation, ed. Pierre Sauvé and Robert M. Stern, 57-85. Washington, D.C.: Brookings Institution Press.

Washington Trade Daily. 2007. “Interview with Fernando de Mateo y Venturini,” February

13, 2007.

World Trade Organization - WTO. 2000. “Note on Assessment of Trade in Services in

Appendix

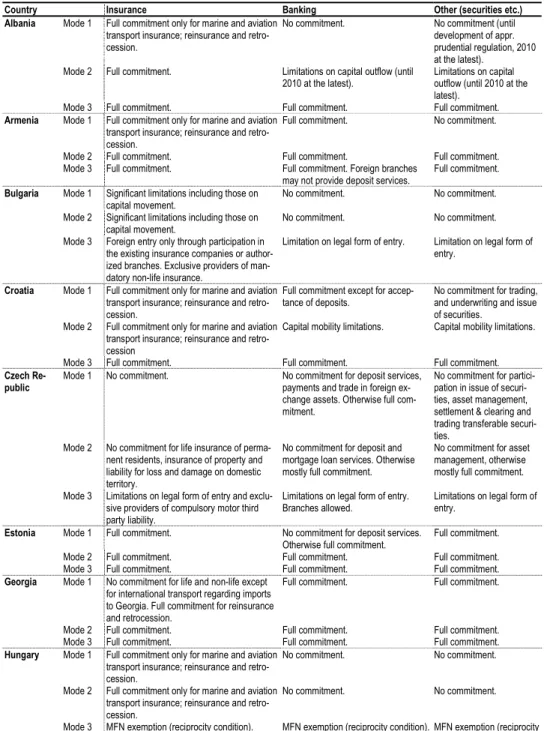

Table 2 Liberalisation Commitments in Financial Services for CESE and CIS Countries

Country Insurance Banking Other (securities etc.)

Albania Mode 1 Full commitment only for marine and aviation

transport insurance; reinsurance and retro-cession.

No commitment. No commitment (until development of appr. prudential regulation, 2010 at the latest).

Mode 2 Full commitment. Limitations on capital outflow (until 2010 at the latest).

Limitations on capital outflow (until 2010 at the latest).

Mode 3 Full commitment. Full commitment. Full commitment.

Armenia Mode 1 Full commitment only for marine and aviation

transport insurance; reinsurance and retro-cession.

Full commitment. No commitment.

Mode 2 Full commitment. Full commitment. Full commitment.

Mode 3 Full commitment. Full commitment. Foreign branches may not provide deposit services.

Full commitment.

Bulgaria Mode 1 Significant limitations including those on

capital movement.

No commitment. No commitment.

Mode 2 Significant limitations including those on capital movement.

No commitment. No commitment.

Mode 3 Foreign entry only through participation in the existing insurance companies or author-ized branches. Exclusive providers of man-datory non-life insurance.

Limitation on legal form of entry. Limitation on legal form of entry.

Croatia Mode 1 Full commitment only for marine and aviation

transport insurance; reinsurance and retro-cession.

Full commitment except for accep-tance of deposits.

No commitment for trading, and underwriting and issue of securities.

Mode 2 Full commitment only for marine and aviation transport insurance; reinsurance and retro-cession

Capital mobility limitations. Capital mobility limitations.

Mode 3 Full commitment. Full commitment. Full commitment.

Czech Re-public

Mode 1 No commitment. No commitment for deposit services, payments and trade in foreign ex-change assets. Otherwise full com-mitment.

No commitment for partici-pation in issue of securi-ties, asset management, settlement & clearing and trading transferable securi-ties.

Mode 2 No commitment for life insurance of perma-nent residents, insurance of property and liability for loss and damage on domestic territory.

No commitment for deposit and mortgage loan services. Otherwise mostly full commitment.

No commitment for asset management, otherwise mostly full commitment.

Mode 3 Limitations on legal form of entry and exclu-sive providers of compulsory motor third party liability.

Limitations on legal form of entry. Branches allowed.

Limitations on legal form of entry.

Estonia Mode 1 Full commitment. No commitment for deposit services.

Otherwise full commitment.

Full commitment.

Mode 2 Full commitment. Full commitment. Full commitment.

Mode 3 Full commitment. Full commitment. Full commitment.

Georgia Mode 1 No commitment for life and non-life except

for international transport regarding imports to Georgia. Full commitment for reinsurance and retrocession.

Full commitment. Full commitment.

Mode 2 Full commitment. Full commitment. Full commitment.

Mode 3 Full commitment. Full commitment. Full commitment.

Hungary Mode 1 Full commitment only for marine and aviation

transport insurance; reinsurance and retro-cession.

No commitment. No commitment.

Mode 2 Full commitment only for marine and aviation transport insurance; reinsurance and retro-cession.

No commitment. No commitment.

Country Insurance Banking Other (securities etc.)

Kyrgyzstan Mode 1 No commitment, except for insurance of

cargo transportation, brokerage and reinsur-ance.

Full commitment. Full commitment.

Mode 2 Full commitment. Full commitment. Full commitment.

Mode 3 Full commitment. Full commitment. Full commitment.

Latvia Mode 1 No commitment except for reinsurance. No commitment. No commitment.

Mode 2 Full commitment. Full commitment. Full commitment.

Mode 3 Full commitment. Full commitment. Full commitment.

Lithuania Mode 1 Full commitment only for marine and aviation

transport insurance; reinsurance and retro-cession.

Full commitment. Full commitment.

Mode 2 Full commitment. Full commitment. Full commitment.

Mode 3 Full commitment. Full commitment. Full commitment.

Macedonia, FYR

Mode 1 Full commitment only for marine and aviation transport insurance; insurance of commer-cially licensed transportation vehicles; and reinsurance and retrocession.

No commitment. No commitment.

Mode 2 Full commitment only for marine and aviation transport insurance; insurance of commer-cially licensed transportation vehicles; and reinsurance and retrocession

Full commitment except for deposit services which will be liberalised upon phase II of Stabilisation and Associa-tion Agreement (SAA).

No commitment, full com-mitment will be awarded gradually to trading, with the application of SAA with the EU.

Mode 3 Limitation on legal form of entry, branches allowed from 2008.

Limitation on legal form of entry. Branches allowed from 2008.

Limitations on legal form of entry.

Moldova Mode 1 Full commitment only for marine and aviation

transport insurance; reinsurance and retro-cession.

No commitment No commitment.

Mode 2 Full commitment. Full commitment except that outgoing capital transactions require approval.

Full commitment except that outgoing capital transactions require ap-proval.

Mode 3 Full commitment. Limitations on legal form of entry & branches.

Limitations on legal form of entry.

Poland Mode 1 Full commitment only for reinsurance and

retrocession and goods in international transport.

No commitment. No commitment.

Mode 2 Full commitment only for reinsurance and retrocession and goods in international transport.

No commitment. No commitment.

Mode 3 Limitations on legal form of entry. Branches allowed.

Limitations on legal form of entry. Branches allowed.

Limitations on legal form of entry. Branches allowed.

Romania Mode 1 No commitment except for reinsurance of the

part of the risk that cannot be placed on domestic market.

Full commitment except for payments where no commitment.

No commitment.

Mode 2 No commitment except that ceding reinsur-ance on international market allowed for reinsured risk that cannot be placed on domestic market.

Only with the National Bank permis-sion.

No commitment.

Mode 3 Allowed only as a joint venture with a do-mestic person

Full commitment. Limitations on legal form of entry.

Slovak Republic

Mode 1 No commitment for life insurance of perma-nent residents, insurance of property and liability for loss and damage on domestic territory and air and maritime insurance. Otherwise full commitment.

No commitment for deposit services, payments and trade in foreign ex-change assets. Capital mobility limitations.

No commitment for partici-pation in issue of securi-ties, asset management, settlement & clearing services and trading transferable securities.

Mode 2 No commitment for life insurance of perma-nent residents, insurance of property and liability for loss and damage on domestic territory. Otherwise full commitment.

No commitment for deposit services. Capital mobility limitations.

No commitment for asset management. Capital mobility limitations.

Mode 3 Limitations on legal form of entry and exclu-sive providers of mandatory insurance schemes.

Limitations on legal form of entry. Branches allowed.

Country Insurance Banking Other (securities etc.)

Slovenia Mode 1 Full commitment for marine and aviation

transport insurance and goods in interna-tional transit. Otherwise no commitment.

No commitment. Only inbound credit, guarantees and commitments allowed, except for consumer credits (to be allowed upon acceptance of new Law).

No commitment.

Mode 2 Full commitment for marine and aviation transport insurance; goods in international transit and reinsurance and retrocession of the part of the risk that cannot be placed on domestic market (to be abolished upon adoption of new Law). Otherwise no com-mitment.

No commitment. No commitment.

Mode 3 Only as a joint venture with domestic entities and upon approval. Maximum foreign own-ership 99% (to be abolished upon adoption of new Law). No commitment for privatiza-tion.

Potential discretionary licensing for foreign participation. No branches. Will be liberalised upon adoption of new Law. No commitment on privatization.

Limitations on legal form of entry.

Note:

No commitment – market closed (although in effect it may be open, the country did not make any obligation to keep it so); Full commitments – fully open market

Mode 1 – cross border trade, Mode 2 – consumption abroad, Mode 3 – commercial presence

Source: Authors’ analysis of the WTO financial services commitments of the above countries.1

1

Table 3 Liberalisation Indices for Direct Insurance and Banking in CESE and CIS

Country EU and OECD

membership

WTO membership

date

Direct insurance Banking

Life insurance

Non-life

insurance Acceptance of deposits All types of loans

Estonia EU 1999, 13-Nov 1.00 1.00 0.88 1.00 Lithuania EU 2001, 31-May 0.88 0.90 1.00 1.00 Georgia - 2000, 14-Jun 0.88 0.80 1.00 1.00 Kyrgyzstan - 1998, 20-Dec 0.88 0.80 1.00 1.00 Armenia - 2003, 5-Feb 0.88 0.90 0.79 1.00 Croatia - 2000, 30-Nov 0.85 0.88 0.85 0.98 Albania - 2000, 8-Sep 0.88 0.90 0.87 0.78 Latvia EU 1999, 10-Feb 0.88 0.80 0.88 0.80 Moldova - 2001, 26-Jul 0.88 0.90 0.67 0.61 Romania EU 1995, 1-Jan 0.64 0.56 0.99 0.98 Poland OECD, EU 1995, 1-Jul 0.85 0.75 0.64 0.56 Macedonia, FYR - 2003, 4-Apr 0.64 0.69 0.64 0.61

Slovenia EU 1995, 30-Jul 0.64 0.69 0.43 0.63 Bulgaria EU 1996, 1-Dec 0.64 0.48 0.64 0.56 Slovak

Republic OECD, EU 1995, 1-Jan 0.43 0.50 0.64 0.69 Czech

Republic OECD, EU 1995, 1-Jan 0.44 0.40 0.64 0.81

Hungary OECD, EU 1995, 1-Jan 0.21 0.31 0.21 0.19 Serbia - not a member 0.21 0.19 0.21 0.29

Note: Higher levels of index indicate higher liberalisation commitments