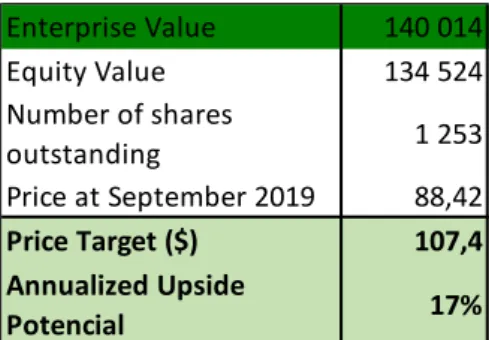

Equity research - Starbucks

Texto

Imagem

Documentos relacionados

Essa característica das línguas do grupo ao qual pertencem o latim e o português torna relevante a investigação da evolução da fonologia para a compreensão da evolução

Estrogen metabolites, namely 2- and 4-hydroxyestrone and 2- and 4-hydroxyestradiol might generate electrophilic metabolites, and for mercapturate pathway-related metabolites

Art. 97 - A validação de disciplinas cursadas em outras instituições obedecerá ao disposto na legislação específica, definida pelo Conselho Nacional de

Neste trabalho o objetivo central foi a ampliação e adequação do procedimento e programa computacional baseado no programa comercial MSC.PATRAN, para a geração automática de modelos

Estrutura para análises fisico-químicas laboratoriais 23 Pesca com 'galão' realizada no açude Paus Branco, Madalena/CE 28 Macrófitas aquáticas flutuantes no nude Paus

As doenças mais frequentes com localização na cabeça dos coelhos são a doença dentária adquirida, os abcessos dentários mandibulares ou maxilares, a otite interna e o empiema da

Para determinar o teor em água, a fonte emite neutrões, quer a partir da superfície do terreno (“transmissão indireta”), quer a partir do interior do mesmo

No caso e x p líc ito da Biblioteca Central da UFPb, ela já vem seguindo diretrizes para a seleção de periódicos desde 1978,, diretrizes essas que valem para os 7