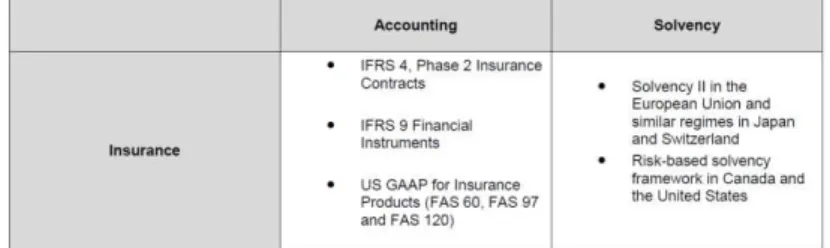

DENSITY AND PENETRATION INSURANCE ON ACCIDENT & HEALTH PREMIUMS IN FUTURE IMPLEMENTATION OF SOLVENCY II – EMPIRICAL STUDY

Texto

Imagem

Documentos relacionados

The probability of attending school four our group of interest in this region increased by 6.5 percentage points after the expansion of the Bolsa Família program in 2007 and

A "questão social" contemporânea, chamada erroneamente de "nova questão social", advém dessas profundas modificações nos padrões de produção, de

The persistence and growth of the private sector in health insurance and/or provision of medical services are not an inertial phenomenon, since they involve economic interests

Foi possível, também, comprovar a relação dos fatores motivacionais para o voluntariado com o bem-estar dos voluntários do CNE, e simultaneamente analisar a existência de relação

No que diz respeito às relações constantes no modelo hipotetizado para os alunos do 3.º Ciclo do Ensino Básico CEB, foi assumido, por parcimónia, que cada um dos construtos

O principal negociador de 1954, Pham Van Dong fora forçado pelos soviéticos e chineses a assinar um acordo, que, mais tarde, Mao admitiu que fora um erro (YANG, 2002). Le

É nesta mudança, abruptamente solicitada e muitas das vezes legislada, que nos vão impondo, neste contexto de sociedades sem emprego; a ordem para a flexibilização como

Extinction with social support is blocked by the protein synthesis inhibitors anisomycin and rapamycin and by the inhibitor of gene expression 5,6-dichloro-1- β-