Econ. Apl. vol.11 número3

Texto

Imagem

Documentos relacionados

In the ocean, the variability of environmental conditions found along depth gradients exposes populations to contrasting levels of perturbation, which can be reflected in the

É aqui, neste patamar da metafísica, que surge rigorosamente o problema da criação divina do Universo, ou seja da atribuição da sua existência, origem e evolução, a um

Tens˜oes normais trativas contribuem de forma mal´efica para a degrada¸c˜ao por fadiga por agirem no processo de abertura de microtrincas; quase a totalidade dos modelos de

Entre os pares de Latossolos Férricos avaliados, a caracterização morfológica foi fundamental na individualização do horizonte concrecionário em

1) Importance of the processes for the municipal department under analysis – the process should be one of the most important in the department (based on the information

The main objective of the present work is to compare the values of texture and rheological parameters for vegetable gels at different formulation and thermal processing condi-

This paper aimed at analyzing the spatial distribution of reference ET in the state of Bahia by means of GIS and geostatistical techniques from historical series

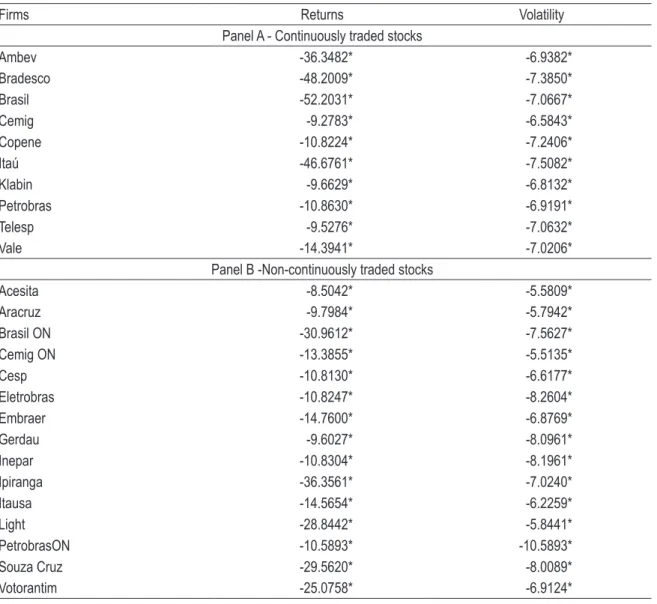

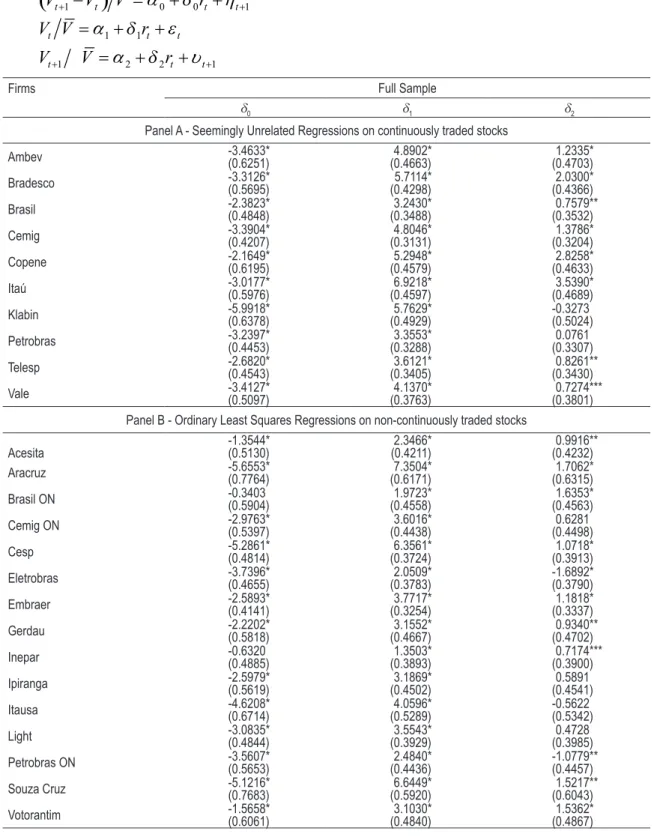

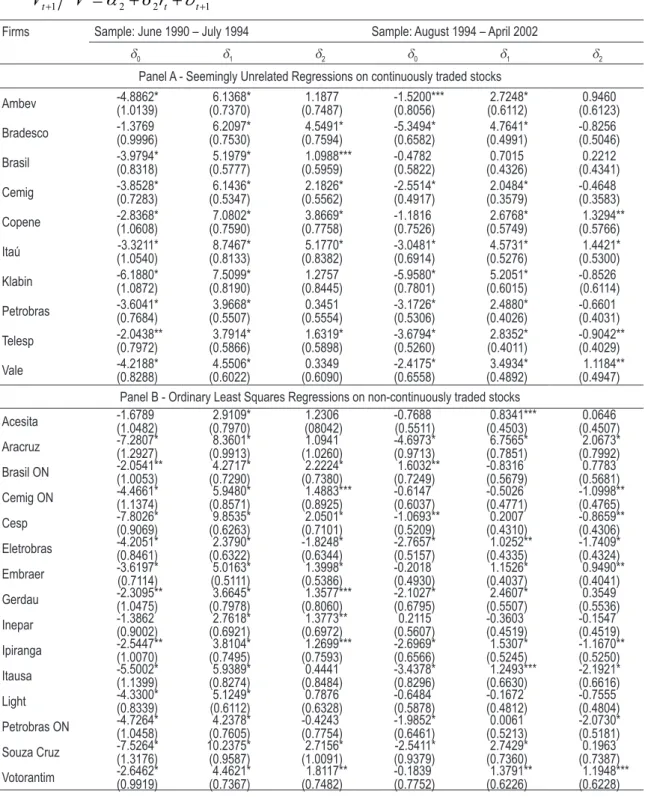

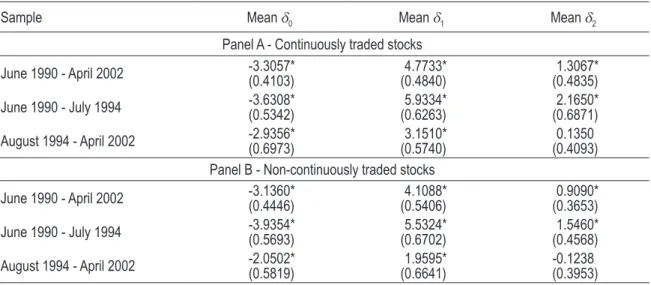

Results indicate that, on average, the impact of the concession announcements on stock returns is negative and suggest that the participation in these projects do not add value to