Contagion in Financial Networks: A

network theory and agent-based

approaches to modeling the spread of

risk in financial systems.

Contagion in Financial Networks: A

network theory and agent-based

approaches to modeling the spread of

risk in financial systems.

Dissertação apresentada à Escola de Mate-mática Aplicada da Fundação Getulio Var-gas, para a obtenção do Título de Mestre em Ciências, na área de modelagem mate-mática da informação.

Orientador: Flávio Codeço Coelho

Ficha catalográfica elaborada pela Biblioteca Mario Henrique Simonsen/FGV

Pinheiro, Leonardo dos Santos

Contagion in financial networks: a network theory and agent-based approaches to modeling the spread of risk in financial systems / Leonardo dos Santos Pinheiro. – 2016.

80 f.

Dissertação (mestrado) – Fundação Getulio Vargas, Escola de Matemática Aplicada.

Orientador: Flávio Codeço Coelho. Inclui bibliografia.

1. Finanças – Modelos matemáticos. 2. Crise financeira. 3. Risco financeiro. 4. Fundos de investimento. I. Coelho, Flávio Codeço. II. Fundação Getulio Vargas. Escola de Matemática Aplicada. III. Título.

5

Agradecimentos

Agradeço,

Ao meu orientador, por todo ensinamento, paciência e dedicação.

Aos professores da EMAp, por todo o ensinamento durante o curso de mestrado.

Aos meus colegas de trabalho, por todo apoio, críticas e sugestões.

Aos meus pais Valdeque e Leila, e ao meu filho Nícolas, que são a base da minha

vida. Muito obrigado por todo amor e carinho que sempre pude receber de vocês em

toda a minha vida.

À minha noiva, Alessandra, por compreender a importância desse curso para a

minha vida, por toda paciência e dedicação, por ser minha motivação, e por fazer, dos

7

Resumo

Esta dissertação estuda a propagação de crises sobre o sistema financeiro. Mais

especi-ficamente, busca-se desenvolver modelos que permitam simular como um determinado

choque econômico atinge determinados agentes do sistema financeiro e a partir dele se

propagam, transformando-se em um problema sistêmico. A dissertação é dividida em

dois capítulos, além da introdução. O primeiro capítulo desenvolve um modelo de

propa-gação de crises em fundos de investimento baseado em ciência das redes. Combinando

dois modelos de propagação em redes financeiras, um simulando a propagação de perdas

em redes bipartites de ativos e agentes financeiros e o outro simulando a propagação de

perdas em uma rede de investimentos diretos em quotas de outros agentes, desenvolve-se

um algoritmo para simular a propagação de perdas através de ambos os mecanismos

e utiliza-se este algoritmo para simular uma crise no mercado brasileiro de fundos de

investimento. No capítulo 2, desenvolve-se um modelo de simulação baseado em agentes,

com agentes financeiros, para simular propagação de um choque que afeta o mercado

de operações compromissadas. Criamos também um mercado artificial composto por

bancos, hedge funds e fundos de curto prazo e simulamos a propagação de um choque

de liquidez sobre um ativo de risco secutitizando utilizado para colateralizar operações

Abstract

This dissertation studies the spread of crisis over the financial system. More specifically,

we aim to develop models that allow us to simulate how an economic shock strikes a

few financial agents and from them propagate over the system, becoming a systemic

problem. The dissertation is composed by the introduction and by two chapters. In

the first chapter, we model the spread of crisis over investment funds using network

science. Combining two models of propagation in financial networks, one simulating the

propagation of losses in bipartite networks of assets and financial agents and the other

simulating the propagation of losses in a network of cross-holdings of shares among

financial agents, we develop an algorithm to simulate the spread of losses utilizing both

mechanisms and we use this algorithm to simulate a crisis in the Brazilian market of

investment funds. In Chapter 2 we develop an agent-based simulation model, using

financial agents to simulate the propagation of a shock affecting the repo market. We

also create an artificial market consisting of banks, hedge funds and money market

funds, and simulate the spread of a liquidity shock striking a risky securitized asset

Lista de Figuras

2.1 A weighted directed graph . . . 19

2.2 Portfolio composition by fund class. Fixed income funds represent most

of the total asset in the industry. Fund quotas is by far the most owned

asset, representing a potential source of contagion. Brazilian government

bonds follow as second most owned asset. . . 31

2.3 Number of funds by fund class. Multimarket funds represent the largest

class in number of funds, followed by fixed-income and equity funds.

Funds with more risk appetite are more numerous but smaller in total

assets. . . 32

2.4 Stability of the Investment Fund network. The table shows Jaccard

coeffients of edges and nodes for the network in pairs of months over the

period from Jan/2012 to Dec/2014. . . 33

2.5 Number of nodes and connections on the network over time. The number

over funds grows slowly but steadily over time. The number of edges

2.6 The directionality of the edges indicates the investor fund as the tail

and the invested fund as the head. (a) In degree histogram for the

cross-holdings network. The histogram exhibit typical power law (b)

Out degree histogram for the cross-holdings network. The steepness of

the curve is much lower in the out-degree distribution. . . 34

2.7 Degree histograms for both types of nodes in the bipartite fund-asset

net-work. While both distributions exhibit characteristic power law shapes,

the hubs are much more prominent among assets than funds. . . 36

2.8 Annual probability of default from Brazilian %Year CDS spreads.. . . . 37

2.9 (a) Number of failures after the initial shock as we vary both the critical

value rate and the shock rate. (b) Number of final failures at a fixed

initial shock rate of 15% and critical value rate of 85% as we vary asset

price pressure rate and discontinous loss rate. . . 39

3.1 Liability composition of banks in the simulation. After initial market

creation liabilities are composed by NAV, bank deposits and repurchase

agreements. . . 64

3.2 Portfolio composition of banks in the simulation.Banks leverage to invest

in the risky asset. . . 65

3.3 Deleverage of the banking system as the the system suffers a run on the

repo. . . 66

3.4 Number of solvent, defaulted and bankrupt at each time step in our

simulation. The system reaches a new equilibrium with close to 42% of

the banks having gone bankrupt. . . 67

Lista de Tabelas

2.1 Maximum centrality observed in both networks. The Fund-Asset network

has nodes with much stronger presence as hubs. . . 35

3.1 Summary of Financial Agents. . . 64

1 Introduction 14

2 Financial Contagion in Investment Funds 15

2.1 Introduction. . . 15

2.2 Graph Theory and Network Science . . . 18

2.2.1 Graph Theory . . . 18

2.2.2 Centrality Measures . . . 20

2.2.3 Homophily and Assortativity . . . 22

2.2.4 Dynamic Networks . . . 23

2.3 The Cross-Holdings Contagion Model . . . 23

2.3.1 Primitive Assets and Cross-Holdings . . . 23

2.3.2 Firm Susceptibility to Financial Shocks . . . 25

2.3.3 The Contagion Model . . . 27

2.4 The Data . . . 29

2.5 Results and Discussion . . . 30

2.5.1 Network Topology . . . 30

2.5.2 Simulations . . . 35

2.6 Final Remarks . . . 38

13 Sumário

3 An Agent-based Model of Contagion in Financial Networks 44

3.1 Introduction. . . 44

3.2 Financial Contagion . . . 47

3.3 Agent-Based Computational Finance . . . 49

3.4 The Artificial Repo Market Model . . . 51

3.4.1 Assets . . . 51

3.4.2 Financial Agents . . . 54

3.4.3 Risk Management . . . 58

3.4.4 Market Mechanism . . . 60

3.4.5 Failures, Fire sales and Contagion . . . 61

3.5 Simulation. . . 63

3.5.1 Experimental Design . . . 63

3.5.2 Results . . . 64

3.6 Final Remarks . . . 69

Bibliography 70 A Computational Models 75 A.1 Computational Model for "Financial Contagion in Investment Funds". . 75

A.1.1 Dependencies . . . 75

A.1.2 Data . . . 76

A.1.3 Code Description . . . 77

A.2 Computational Model for "An Agent-based Model of Contagion in Fi-nancial Networks" . . . 78

A.2.1 Dependencies . . . 78

A.2.2 Object-Oriented Model . . . 78

Introduction

This dissertation explores the modeling of financial contagion and is composed by two

essays. Each study focus on different types of financial intermediaries and in different

forms interconnectivity and propagation chanels. They also propose different models

to simulate the propagation of economic shocks.

The first article, "Financial Contagion in Investment Funds", develops a cascading

failures algorithm to assess the vulnerability of investment funds to an economic shock

over the financial system. The study considers both the network of cross-holdings of

quotas and the network between assets and investment funds as connectivity measures.

Through these complementary transmition channels shocks can propagate and become

systemic. We also use data from the Brazilian Asset management to provide a

des-cription of the structure of a network of investment funds, to illustrate the proposed

algorithm and to analyse how the network structure affect the results of the algorithm.

The second article, "An Agent-based Model of Contagion in Financial Networks",

develops an artificial financial market model that simulates trading behavior in the

repo markets after a shock hits the financial system. The model is capable of simulating

a "run on the repo"with effects similar to the observed in the repo market during the

Capítulo 2

Financial Contagion in

Investment Funds

Abstract

Many new models for measuring financial contagion have been presented recently.

While these models have not been specified for investment funds directly, there are

many similarities that could be explored to extend the models. In this work we explore

ideas developed about financial contagion to create a network of investment funds using

both cross-holding of quotas and a bipartite network of funds and assets. Using data

from the Brazilian asset management market we analyse not only the contagion pattern

but also the structure of this network and how this model can be used to assess the

stability of the market.

2.1

Introduction

In recent years the use of network representations for the study of economic systems has

and production chains Allen and Babus (2008). A special subject in these topics is

the study of financial systems. Since the global financial crisis that hit the world in

2007-08 the interest in the intricate ways in which financial institutions are intertwined

has soared, with studies showing the several facets of the interconnections of financial

systems, specially in the way these connections affect global stability.

The 2007-08 crisis, which started in the US sub-prime mortgage market, rapidly

spilled over to debt markets in a process of financial contagion that ultimately led to

the demise of major American and European banks and triggered a world recession that

spanned years. Interconnection is also a cause of major concern in the ongoing European

debt crisis, with worries that the interconnection in the European bank system may

cause a serious crisis if one nation defaults on its sovereign debt or enters into recession

putting some of the external private debt at risk.

Due to the aforementioned events, much of the studies on the connectedness of

financial institutions is focused on the mutual exposures between banks, specially the

ones acquired on the interbank market (see Cocco et al. (2009),Mistrulli (2011) and

Iori et al. (2006)). But more recently some attention has been devoted to non-bank

financial intermediaries, such as the studies being conducted by the Financial Stability

Board to address what in being called the "Shadow Banking System" (Board (2011a)

and Board(2011b)). In this work, we aim to explore one of these elements of financial

systems, the asset management industry.

In the Brazilian market, in 2014, asset management firms oversaw the allocation

of approximately U$ 1T in financial assets, consisting of a substantial part of the

Brazilian financial system. Not only is the industry significant in size, but these firms

and the funds they manage transact with other institutions in the financial system,

and within themselves, in a variety of ways. As a consequence, this industry is heavily

interconnected with the bank and insurance markets, augmenting greatly the effects it

17 2.1. Introduction

While it is still highly debatable whether asset management in fact poses systemic

risk, the industry has a number of factors that make it susceptible to financial shocks.

Behaviors such as reaching for yield and herding, redemption risks associated to liquidity

mismatch, high leverage and even behaviors of the asset managers can represent sources

of risk (for a deeper discussion of the risks of asset management see the recent report

of the Office of Financial Research, U.S. Department of the Treasury(2013)). These

are factors that have the potential to amplify financial shocks over the funds and, if

the system is heavily interconnected, cause cascading failures and heavy losses to the

entire financial system.

In this paper we develop a network model to assess the inter-connectivity and

how cascading failures can occur among investment funds. We also take a empirical

approach to study the asset management market through simulations with data from

the Brazilian Market.

In a simple definition, networks can be described as collections of objects in which

some objects can be connected forming a set of links. By this generic definition, many

types of connections can be used to compose the edgeŠs set (Easley and Kleinberg

(2010)).

The literature on financial networks contains many proposed metrics which can

be used to define the connections between firms. For instance, Huang et al. (2013)

propose the use of a bipartite network between firms and assets where a link represents

a ownership relation between firm and asset, Diebold and Yılmaz (2014) propose

connectedness measures built from pieces of variance decompositions and Billio et al.

(2012) proposes a set of econometric measures based on principal-components analysis

and Granger-causality networks. In this regards we follow closely the approach adopted

by Elliott et al.(2014), in which cross-holdings of organizations shares form the edges,

taken together with the approach fromHuang et al.(2013), to better explain the effects

By forming networks considering cross-holdings and common asset holdings we can

analyze the structure of an investment fund network and look for potential impacts of

financial shocks using contagion and diffusion models. While our model uses the ideas

from the aforementioned works, this approach is not exhaustive, there are many other

contagion and diffusion models in the finance literature which could have been explored

(see Gai and Kapadia(2010) and Allen and Gale(2000)).

The structure of this paper is organized as follows. In Section 2 we provide a

background and basic terminology on graphs and networks that will be used throughout

the analysis. In Section 3 we present the contagion model using the frameworks

developed by Elliott et al. (2014) and Huang et al. (2013). Section 4 describes the

data used and give a brief overview of asset management in Brazil. Section 5 presents

the findings about the network structure and the results of simulations over the data.

Finally, in Section 6 we discuss future research directions and present a summary and

final remarks on the work.

2.2

Graph Theory and Network Science

In this section we provide some basic terminology about the concepts used along this

paper. Its comprises concepts from graph theory for the representation of networks

and from Social / Economic Network Analysis for understanding network structure and

stability.

2.2.1 Graph Theory

A graph is a mathematical construct of a set of objects, called nodes or vertices,

con-nected by a set of links, called edges. More formally a graph�= (�,�)is an ordered pair consisting of a set of nodes� and a set of edges� where� ⊆� ×�. The order of

19 2.2. Graph Theory and Network Science

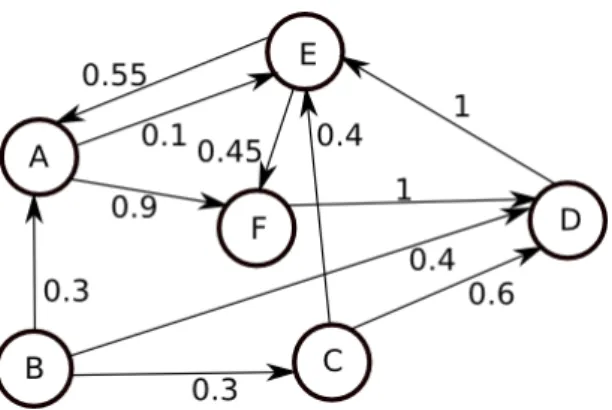

Figure 2.1: A weighted directed graph

A graph may be directed or undirected. A directed graph (or digraph) is a ordered

pair �= (�,�)consisting of a set of nodes� and a set of edges� where �⊆� ×�

and where, for every edge (�,�)∈�, there is a link that leaves uand enters v. We say

that u is the tail andv is the head.

An import metric of networks is their degree distribution. The degree of a node�i

is the number of connections it has. For a digraph we define in-degree as the number

of connections incoming to a node and the out-degree as the number of connections

leaving the node.

Graph labeling is the assignment of labels to edges and/or nodes of a graph. These

labels often represent attributes of the graph. In a labeled graph we define the set of

edges� ⊆� ×�×� where� is the set of labels. Aweighted graph is a labeled graph

where edge labels are members of an ordered set, usually of integers or real numbers,

which represent the "strength" of the connections. We define�ij as the weigh between

nodes�and �.

There are many ways to represent graphs. In this work, they are usually represented

2.2.2 Centrality Measures

Graphs are a natural way to represent networks, but social economic networks usually

exhibit some properties better analyzed through specific metrics. As was found by

Albert and Barabási (2002), many real networks exhibit a property that their degree

distributions are scale-free. In social and economic networks, this property can create a

structure where a few members of the network can gather most of the connections, thus,

controlling the flow of information in the network. This brings up the importance of

analyzing the influence of members in a network. One way to analyze this importance

is through centrality measures.

Centrality measures aim to describe how a given node relate to the network in some

aspect of its structure, such as node position in the network. Four types of centrality

measures are usually described in the network literature (Jackson et al.(2008)), each

one aiming to describe an different aspect of node importance in the network. These

are:

1. Degree Centrality: How many connections a node has;

2. Closeness Centrality: How easily a node can reach other nodes;

3. Betweenness Centrality: How central the node is in creating paths between other

nodes;

4. Eigenvector Centrality: How important (well connected) the nodeŠs neighbors

are.

Degree Centrality is considered the most classical measure of centrality and it

measures how import a node is by the number of connections it has (Freeman et al.

21 2.2. Graph Theory and Network Science

that it misses the location of the node in the network while for some applications, like

spread of processes, the position of the node in the network is a fundamental aspect.

Closeness Centralitymeasures a node importance by how close it is to any other

node in the network (Freeman et al.(1980)) . One way to measure closeness is:

�c(�) =

�−1 ︁n−1

v=1�(�,�)

, (2.1)

where�(�,�)is is the shortest-path distance between� and�, and�is the number

of nodes in the graph. In a diffusion process, the nodes with highest closeness centrality

are likely to be affect by the process more rapidly than others.

Betweenness Centrality captures how well situated a node is in terms of the

paths (Freeman et al.(1980)) in the network. The betweenness centrality of a node�is

the sum of the fraction of all-pairs shortest paths that pass through it. Mathematically

we measure betweenness as::

�b(�) = ︁

s,t∈V

à(�,�|�)

à(�,�) , (2.2)

where à(�,�|�)is the number of shortest (�,�)-paths and à(�,�)is the number of those paths passing through�. In a diffusion process, a node that has high betweenness

can control the flow of information in the network.

Eigenvector Centrality is based on the premise that a nodeŠs importance is

measured by how important its connections are (Bonacich (1972)). The eigenvector

centrality for node � is xi where � is the index of node � and xi is the principal

Ax=Úx (2.3)

where A is the adjacency matrix of the network. In diffusion process, an node

who is high on eigenvector centrality is connected to many nodes which themselves are

connected to many nodes, thus multiplying their probability of contagion.

2.2.3 Homophily and Assortativity

Social and Economic networks sometimes exhibit a property that entities are more prone

to establish connections with similar entities. This property was named homophily by

Kandel (1978). Homophily may play an important role in economic networks, since it

can mean a network can be largely segregated (Jackson et al.(2008)).

One way to measure homophily among labeled nodes is by assortativity.

Assortativ-ity measures the similarAssortativ-ity of connections in a network with relation to some attribute

or label. We define the assortativity coefficient as:

�=

︁

i�ii−︁i�i�i 1−︁

i �i�i

, (2.4)

where �ij is the fraction of edges in the network that connect a type � node to

a type � and�ij = �i�j. The matrix M is the joint probability distribution (mixing matrix) of the specified attributeNewman(2003). Assortativity may play an important

whole in financial networks as segregated financial firms may form regions of closure

23 2.3. The Cross-Holdings Contagion Model

2.2.4 Dynamic Networks

Some networks vary over time. The field that studies how networks change over time

is known as network dynamics or dynamic network analysis (DNA). The main aspects

of DNA is the analysis of the statistical properties of time varying networks and the

simulation of network changes over time. DNA is a broad field and we refer to the work

of Carley (2003) for those interested in it. For the purpose of financial networks and

contagion we focus on the stability of financial networks over time.

One way to measure network stability over time is to check the Jaccard similarity

of nodes and/or edges between pairs of successive time spans (Masys(2014)). This is

a indication of how much nodes and/or edges are formed or removed from the network

between small time steps. The Jaccard similarity coefficient is a measure of similarity

between sets. The coefficient of a set S and a set T is|�∩�|/|�∪�|, that is, the ratio

of the size of the intersection of S and T to the size of their union (Rajaraman et al.

(2012)).

2.3

The Cross-Holdings Contagion Model

In determining interconnectivity between investment funds we follow closely the model

developed by Elliott et al. (2014) for financial firms in which cross-holdings of shares

among organizations may lead to cascading failures. In the context of investment funds,

we measure cross-holdings of fundŠs quotas. We differ from the model when common

assets holdings are considered in the process and in this regard we use the framework

developed by Huang et al.(2013).

2.3.1 Primitive Assets and Cross-Holdings

In the original model developed byElliott et al.(2014) the value of organizations are

the shares of the other organizations which they hold. There are�organizations making

up a set � = 1, 2, ...,�. There is also a group of assets in the economy that may be

owned by firms and these assets compose another set� = 1,2,...,�. For investment

funds as organizations, the primitive assets are formed by assets not issued by other

investment funds and legally permitted to be bought by funds, these may be shares

of companies, corporate bonds, government bonds, derivatives, among others. Funds

can also hold shares of other funds, which creates the cross-holdings among

organiza-tions. As the funds are the only organizations in our system we shall use the terms

interchangeably from this point.

The base value of a fund is determined by the value of itŠs assets. The value of an

asset � is denoted by �k and we call p the vector containing the values of the assets

in �. We also call D the matrix which entry �ik is the share of the value of asset

� held by organization �. Complementary to D we have the matrix C in which, for

each,�,� ∈�,�ij ≥0 is the fraction of organization �owned by organization �. The

matrix C can be seen as a network of direct links between the organizations. There

is also the share �ˆii := 1−︁

i∈N�ij of organization i which is not owned by other organizations in the system. This forms the matrixCˆ.

To determine the fair value of organizations, Elliott et al.(2014) used a framework

developed byFedenia et al.(1994) andBrioschi et al.(1989). The value�iof organization

� is determined by the value of itŠs assets plus the value of itŠs applications on other

organizations:

�i = ︁

k

�ik�k+ ︁

j

�ij�j (2.5)

25 2.3. The Cross-Holdings Contagion Model

V= (I−C)−1Dp (2.6)

Brioschi et al. (1989) and Fedenia et al. (1994) argue that the true value of an

organization is better captured by what is held byoutsideinvestors. This value is equal to�˙i =�ˆii�i, leading to:

˙

V=Cˆ(I−C)−1Dp=ADp (2.7)

We also callA =Cˆ(I−C)−1 the dependency matrix. It captures the true value

of the cross-holdings of quotas in the market and allow us to measure the true value of

the funds and how changes in one organizationŠs value shall affect any other.

2.3.2 Firm Susceptibility to Financial Shocks

Organizations can lose value in discontinuous ways under certain situations. We call

these losses failure costs. Failure costs are assumed if an organization falls bellow some

value threshold, in which case we can interpret that it has transitioned from a financially

stable situation to an unstable one (Elliott et al.(2014)). So, if organization �valueŠs

fall below some threshold �¯i, it incurs in failure costs Ñi(p).

In a more general setting there are many possible explanations for failure costs.

The main assumption in investment funds is that under certain situations there main

occur a run on the fund, forcing it to sell assets at inopportune times at a discount

rate, leading to the discontinuous losses. There may be many situations causing this

run on the fund, such as reputation risk generated by the asset manager, performance

risk caused by risky strategies and leverage, or economic risks such as financial bubbles

When funds are directly connected by cross holdings the spread of a discontinuous

loss is straightforward. Nevertheless, failure costs incurred by one organization may

"affect" other organizations even if they are not directly connected in the network. The

main way in which it can happen is common asset holdings. Since many assets are held

simultaneously by many firms, the way one firm incurs in failure costs can force it to fire

sale itŠs assets and force the price of the asset down in a way that other organizations

holding the same assets may also face difficulties.

To correctly address the effect of common asset holdings we use the framework

developed byHuang et al.(2013). In addition to the network of cross-holdings described

in Equation2.6we use a ancillary network formed by organizations as one type of node

and assets as the other.

In this network a link between a fund and an asset exists if the fund has the asset on

its portfolio. It is a bipartite weighted graph where the weights on the links represent

the gross value of the portfolio position in the asset.

Let B be the bipartite network between the organizations in Nand the assets in

M. We have that

B=

︀

︀ ︀

0n,n W

WT 0m ,m

︀

⎥ ︀,

where W is a�� sub-matrix where�ij is the value of the position of fund�in asset

�. We can rewrite the termDpin2.7in terms ofW. Let⃗1= [1, 1, 1,..., 1]T

n. We write:

Dp=W⃗1.

And Eq. 2.6leading to:

27 2.3. The Cross-Holdings Contagion Model

In the presence of financial instability for an organization�, not only failure costs Ñi

are incurred but also every asset� owned by� suffer a pressure to go down, becoming:

�j = ︁

i�ij−æ�ik ︁

i�ij .

2.3.3 The Contagion Model

Financial contagion can occur when one organization fails and itŠs losses spread to other

organizations causing them to fail as well. This can have the potential to generate a

cascade of failures, potentially breaking the financial system as a whole.

The financial contagion process can be described as a diffusion process where losses

spread in the network of interconnections. Through both the cross-holdings connections

and common asset holdings funds can be affected by this diffusion process.

If funds are directly connected, discontinuities will propagate in the cross-holdings

network, affecting the final value of other funds invested in the broken firms in the path

of connections. These affected funds, in turn, may start to face difficulties and cause

new failures and discontinuous losses. At the same time, these funds may be forced to

sell their assets, causing drops in asset prices which may also cause new failures and

discontinuous losses. These losses shall propagate until a new equilibrium is reached.

But prior to contagion we must have a shock over the system. This shock can be of

any kind, but for the contagion to be triggered at least one fund must lose value until

it fall bellow the critical value to move the system from equilibrium.

Bellow we describe an algorithm containing the step-by-step process to simulate

the cascading failure process.

1. Let�tbe the set of failed organizations at step�. We initialize�0 =∅, indicating

a starting state of equilibrium.

2. At the initial moment we shock a market asset �i or a set of assets M =

the nature of the shock). Each asset is reduced to a fraction of its original value

Ö�i, whereÖ <1 is determined by the strength of the shock.

3. After the initial shock, the loss spreads in the network of cross-holdings and we

recalculate the value of each fund in the system using Equation2.8, checking which

of them have fallen bellow a critical value�crit. Each fund �in which �i < �crit(i)

is added to �.

4. We start the iterative process. At step t, Let ˜bt−1 be a vector with element ˜

bi = Ñi if�∈�t−1 and 0 otherwise, whereÑi is the loss in value due to failure. Also, for each asset �j connected with each fund � in �t−1, its overall market

value is reduced as the marketŠs reaction to the fund failure. The price of asset�j

owned by �becomes �i = ︁

i�ij−æ�ij ︁

i�ij

, where æ is a parameter that measures

the strength of the fire sales over the market price of the asset .

5. The new set �t is formed by the funds which have negative values in:

A︁W⃗1−˜bt−1︁

−vcrit.

6. We terminate if �t=�t−1. Otherwise, we go back to step 4.

This algorithm provides a framework to understand how damages spread to both

other funds and to assets until the cascading failure stops. It also describes a hierarchy

of vulnerability under a specific crisis which is determined by the initial shock.

Many parameters can affect the results of the algorithm. The strength of the initial

shock, the assets affected by the shock, the critical value of the funds, the strength of

the discontinuous losses and of the fire sales are all inputs of the algorithm and must

be determined ex-ante.

Next we will present data taken from the Brazilian asset management industry and

29 2.4. The Data

2.4

The Data

Investment funds , sometimes referred to as collective investment vehicles, are financial

intermediaries that collect financial resources from a pool of investors, both individuals

and companies, and apply these resources into a pool of assets (Bodie et al.(2009)).

In Brazil, investment funds are regulated by the Securities and Exchange Comission

of Brazil (CVM) through CVM Instruction 555 (ICVM 555)1 2. Investment funds are

devoid from legal personality, despite that, they are capable of acquiring and transferring

assets and rights, always represented by their administrators and managers (Fortuna

(2008)).

Traditionally, funds are classified as fixed income and variable income to discriminate

the level of risk of their strategies. Fixed income funds invest in assets with a fixed

return rate, such as government bonds and private credit, and variable income funds

investing in assets with returns that vary with the market, such as shares of companies.

This classification can be refined to better represent investment strategies, two common

classifications are provided by the Brazilian Financial and Capital Markets Association

(Anbima) and by CVM. In this work we will adopt the classification used by CVM.

According to CVMŠs classification, funds are organized in 7 classes which reflect their

investment strategies and profile of risk according to the assets they can buy.

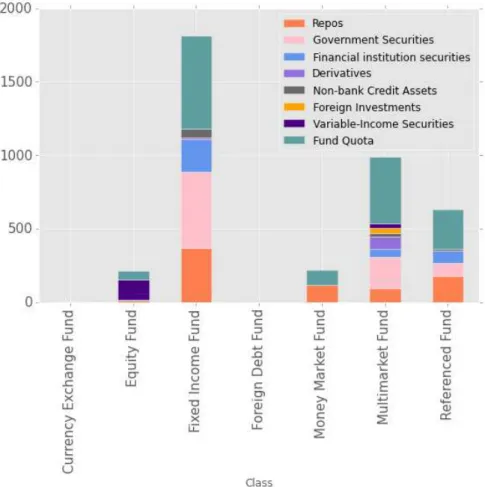

Fixed-income funds are the most representative class in terms of total assets and Multimarket

funds comprise the class with biggest number of funds. Multimarket funds are the class

with most diverse strategies and portfolios, as can be seen in figure2.2.

Another broadly used classification is for open-ended, which are funds open to

redemption at any time after a determined grace period, and closed-ended funds, for

1

ICVM 555 is the current legal diploma for the regulation of investment funds, but many of the classifications used in this paper are based on the definitions of CVM Instruction 409, which was the legal diploma in the period of the analysis.

2

funds with strict restrictions or even completely unavailable for redemption. 3.

Open-ended funds are the majority both in number of funds and in number of assets under

management. Close-ended funds are excluded in simulations, since they are much less

susceptible to events that could trigger failure costs, as modeled in this work, such as

a run on the fund.

For this study we used data of investment funds from the CVM database. To analyze

the network structure we used data from January 2012 up to December 2014 and for

the simulations we used data from December 2014.

2.5

Results and Discussion

2.5.1 Network Topology

To better understand how the market is organized we take a brief look at some key

fea-tures of the network topology. We then proceed to present the results of the simulation

experiments and discuss the role of the topology in the systemŠs dynamics.

Stability

The structure of the network and itŠs stability over time reflect investment decisions

from asset managers. As in Masys (2014) Jaccard similarity coefficients are used to

measure the structural stability of the network over pairs of successive periods. Figure

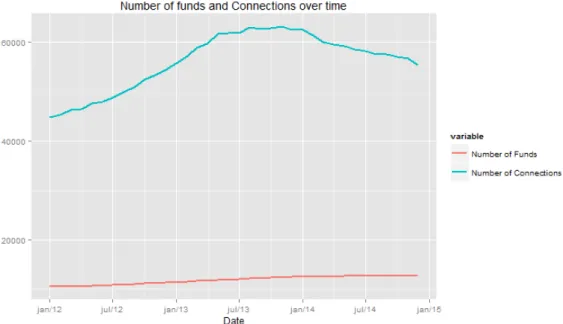

2.5shows the network growth over time and Figure2.4reports a summary of the Jaccard

coefficients. The network exhibit considerable stability between successive months, the

number of nodes exhibit growth at a steady rate while the number of connections seems

to fluctuate more, exhibiting a hump. This fluctuation may indicate some relationship

between the edge count and economic variables which could be further investigated.

3

31 2.5. Results and Discussion

33 2.5. Results and Discussion

Figure 2.4: Stability of the Investment Fund network. The table shows Jaccard coeffients of edges and nodes for the network in pairs of months over the period from Jan/2012 to Dec/2014.

On average, more then 90% of connections are stable between periods, which support

running dynamic models (Snijders et al.(2010)) such as the cascading failures model.

Network Metrics

The cross-holdings network has very low connectivity with an average degree of�avg=

4.34. The degree histogram shows a typical scale free distribution but in-degree and

out-degree curves have very different shapes as can be seen in Figure2.6. The highest

in-degree is 889 and highest out-degree is 70. The in-degree is the most interesting

metric since it is the one that shows how many other funds are directly affected by the

spreading of losses in the cross-holdings network.

The fund-asset network, on the order hand, has an average degree of �avg=20.23.

If we disregard cash, which is connected to almost all funds, the highest asset in-degree

of 4838. The degree distribution in Figure 2.7 shows that a few assets are present in

Figure 2.5: Number of nodes and connections on the network over time. The number over funds grows slowly but steadily over time. The number of edges fluctuates.

(a) In degree histogram (b) Out degree histogram

35 2.5. Results and Discussion

Comparing the two networks we can observe that the fund-asset network is much

more dense, with values of 0.001070 for the fund-asset network and 0.00034 for the

cross-holdings network. In Table 3.1 we can see that in the fund-asset network there

are some very central nodes while in the cross-holding network this metric is much

weaker. While assortativity is not a relevant metric in the fund-asset network, in the

cross-holding network we can observe some level of segregation. Most notably, funds

from same Administrators show assortativity of 0.502 and funds from the same class

exhibit assortativity of 0.217. While the segregation of funds of the same class is not

high enough to indicate regions of confinement for the spread of risk, the segregation

among administrators may be an issue of attention.

Table 2.1: Maximum centrality observed in both networks. The Fund-Asset network has nodes with much stronger presence as hubs.

Cross-Holdings Network Fund-Asset Network

Max. Degree Centrality 0.069 0.256

Max. Closeness Centrality 0.006 0.437

Max. Betweenness Centrality 5.98e-05 0.035 Max. Eigenvector Centrality 0.788 0.670

The nature of the spreading process in this model is very different in the cross-holding

network and in the bipartite network of funds and assets. The results above indicate

that we could observe a faster spreading of contagion caused by asset connections than

by cross-holding connections, this is due to the fact that the network is more dense and

central assets play a stronger whole as hubs.

2.5.2 Simulations

In this section we illustrate how the use of some network metrics combined with the

contagion model can be used to monitor the stability of the financial system and to

identify institutions and assets that could rapidly trigger a contagion process. We build

(a) Degree histogram for fund nodes. (b) Degree histogram for asset nodes.

Figure 2.7: Degree histograms for both types of nodes in the bipartite fund-asset network. While both distributions exhibit characteristic power law shapes, the hubs are much more prominent among assets than funds.

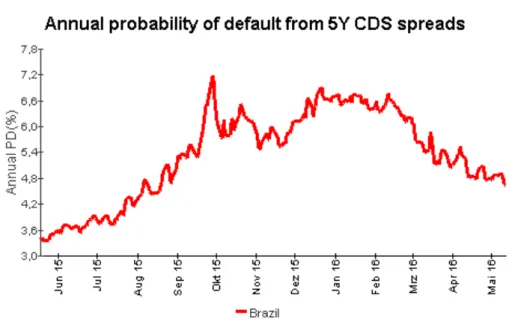

we can see in Figure 2.8, stressing the system to a sovereign debt default.

Sovereign debt default can occur in many forms. A sovereign debt is a contractual

obligation and the most clear-cut example of default is the failure to meet these

obliga-tions to pay interest or principal on the due date. Another example is the failure by

the government to honor debt it has guaranteed where there are clear provisions for

the guarantor to make timely payment.

But sovereign defaults are often not so explicit. Government responses to financial

distress can take many forms. In some cases, it can be inferred that, even in the absence

of an interruption of debt payments, a default has occurred because actions by the

government result in economic losses by creditors,which can vary widely (Beers et al.

(2014)).

In our network of funds and assets Federal Government Bonds occupy a very central

position. It has a total market cap of 35.12% of the total assets and it also has a degree

centrality of 4838, the biggest among all assets except for Cash. ItŠs average path length

2.19, showing that losses can affect almost any other asset price in the first time step

of the algorithm.

37 2.5. Results and Discussion

Figure 2.8: Annual probability of default from Brazilian %Year CDS spreads.

test the susceptibility of the network in diverse settings. The most important parameters

are the rate of discontinuous loss suffered by funds whenever they fail, the asset prices

factor æ, which affects assets of failed funds, the critical value under which the funds

will fail and the size of the initial shock.Three results are evaluated: the number of

firms failed by the financial shock, the number of total failures caused by the cascading

process and the number of iterations before the system reaches a new equilibrium.

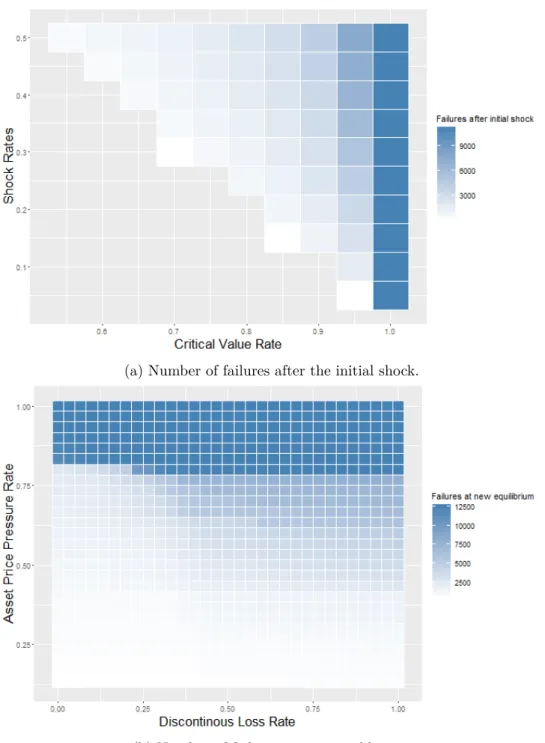

Figure2.9a shows the number of initial failures caused by the initial shock as we

vary the size of the shock and the critical value of organizations. The number of failures

is small when the values are close but escalates quickly as the shock becomes much

stronger than what investors would tolerate. Figure 2.9b shows the number of final

failures as we vary the discontinuous loss rate and the asset pressure rate at a fixed

initial shock rate of 30% and critical value rate of 70%. The asset pressure rate have

a much bigger effect on the number of failures , at a rate of 30% it leads to a total

meltdown of the system independently of the discontinuous loss rate. The discontinuous

These results support our initial hypothesis that the asset network could have a

much bigger influence in the final outcome of the contagion due to the network structure

and the nature of hubs. We emphasize that we do not see these results as robust, but

merely as illustrative of the dynamic of the process.

2.6

Final Remarks

Financial contagion is a complex phenomena with possibly devastating consequences

to financial systems. Here, extending on previous work from Elliott et al. (2014) and

Huang et al.(2013), we have developed a model that accounts for both cross-holdings

among organizations and pressure over asset prices using two complementary networks.

The approach we have developed can be a valuable tool for financial supervisors

and asset managers. For instance, the algorithm can be used with scenario testing to

understand the impact of possible financial crisis to guide supervision and investment

decisions. And, while we do not know if the topological assumptions of the model hold

for other financial firms, we do believe the framework is still valuable for the study

of contagion processes over other financial intermediaries such as banks and insurance

companies.

Although we believe these results are of great value for building a theoretical

un-derstanding of financial contagion, the results obtained in this model would hardly be

reproducible in a real economy since it doesnŠt consider interaction with other financial

intermediaries, existing regulatory measures and the direct intervention of financial

regulators and/or government bailout.

Several improvements to the modeling process are possible to make it more realistic

and closer to the observable reality. To advance this line of research: (1) More work is

required to understand critical values under which discontinuities occur and the value

39 2.6. Final Remarks

(a) Number of failures after the initial shock.

(b) Number of failures at new equilibrium.

needs to be better determined, (3) a better model of financial shocks should be explored,

(4) the interaction with other financial intermediaries should be included and, (5) The

Bibliography

Albert, R. and Barabási, A.-L. (2002). Statistical mechanics of complex networks.

Reviews of modern physics, 74(1):47.

Allen, F. and Babus, A. (2008). Networks in finance.

Allen, F. and Gale, D. (2000). Financial contagion. Journal of political economy, 108(1):1Ű33.

Assaf Neto, A. (2001). Mercado financeiro.

Beers, D., Nadeau, J.-S., et al. (2014). Introducing a new database of sovereign defaults.

Technical report, Bank of Canada.

Billio, M., Getmansky, M., Lo, A. W., and Pelizzon, L. (2012). Econometric measures

of connectedness and systemic risk in the finance and insurance sectors. Journal of Financial Economics, 104(3):535Ű559.

Board, F. S. (2011a). Shadow banking: Scoping the issues. A Background Note of the Financial Stability Board (Basel.

Bonacich, P. (1972). Factoring and weighting approaches to status scores and clique

identification. Journal of Mathematical Sociology, 2(1):113Ű120.

Brioschi, F., Buzzacchi, L., and Colombo, M. G. (1989). Risk capital financing and

the separation of ownership and control in business groups. Journal of Banking & Finance, 13(4):747Ű772.

Carley, K. M. (2003). Dynamic network analysis. Citeseer.

Cocco, J. F., Gomes, F. J., and Martins, N. C. (2009). Lending relationships in the

interbank market. Journal of Financial Intermediation, 18(1):24Ű48.

Diebold, F. X. and Yılmaz, K. (2014). On the network topology of variance

decom-positions: Measuring the connectedness of financial firms. Journal of Econometrics,

182(1):119Ű134.

Easley, D. and Kleinberg, J. (2010). Networks, crowds, and markets: Reasoning about a highly connected world. Cambridge University Press.

Elliott, M., Golub, B., and Jackson, M. O. (2014). Financial networks and contagion.

Available at SSRN 2175056.

Fedenia, M., Hodder, J. E., and Triantis, A. J. (1994). Cross-holdings: estimation

issues, biases, and distortions. Review of Financial Studies, 7(1):61Ű96.

Fortuna, E. (2008). Mercado financeiro: produtos e serviços. Qualitymark Editora

Ltda.

Freeman, L. C., Roeder, D., and Mulholland, R. R. (1980). Centrality in social

networks: Ii. experimental results. Social networks, 2(2):119Ű141.

Gai, P. and Kapadia, S. (2010). Contagion in financial networks. InProceedings of the Royal Society of London A: Mathematical, Physical and Engineering Sciences,

43 Bibliography

Huang, X., Vodenska, I., Havlin, S., and Stanley, H. E. (2013). Cascading failures in

bi-partite graphs: model for systemic risk propagation. Scientific reports, 3.

Iori, G., Jafarey, S., and Padilla, F. G. (2006). Systemic risk on the interbank market.

Journal of Economic Behavior & Organization, 61(4):525Ű542.

Jackson, M. O. et al. (2008). Social and economic networks, volume 3. Princeton

University Press Princeton.

Kandel, D. B. (1978). Homophily, selection, and socialization in adolescent friendships.

American journal of Sociology, pages 427Ű436.

Masys, A. J. (2014). Networks and network analysis for defence and security. Springer

Science & Business Media.

Mistrulli, P. E. (2011). Assessing financial contagion in the interbank market:

Max-imum entropy versus observed interbank lending patterns. Journal of Banking & Finance, 35(5):1114Ű1127.

Newman, M. E. (2003). Mixing patterns in networks. Physical Review E, 67(2):026126. Office of Financial Research, U.S. Department of the Treasury (2013). Asset

manage-ment and financial stability. Technical report.

Rajaraman, A., Ullman, J. D., Ullman, J. D., and Ullman, J. D. (2012). Mining of massive datasets, volume 77. Cambridge University Press Cambridge.

Snijders, T. A., Van de Bunt, G. G., and Steglich, C. E. (2010). Introduction to

An Agent-based Model of

Contagion in Financial Networks

Abstract

This work develops an agent-based model for the study of how the leverage through

the use of repurchase agreements can function as a mechanism for the propagation

and amplification of financial shocks in a financial system. Based on the analysis of

financial intermediaries in the repo and interbank lending markets during the 2007-08

financial crisis we develop a model that can be used to simulate the dynamics of financial

contagion.

3.1

Introduction

In recent years, the use of complex models for the analysis of financial contagion in

economic systems has become widely used. The recent 2007-08 financial crisis, regularly

attributed to the complex relationships among financial institutions, has revived the

45 3.1. Introduction

interlinkages which serve as channels for the transmission and amplification of economic

shocks.

The crisis, which started with a liquidity drain in the US sub-prime mortgage

market, due to the collapse of a bubble in the housing market, quickly overflowed to

debt markets and stock markets in a process of financial contagion that eventually

prompted the downfall of major American and European banks and triggered a world

recession. The means by which the crisis spread from a specific bubble to the whole

financial system is what we call financial contagion and it is a process made possible

by the existing interconnectivity between financial institutions.

Financial institutions are interconnected in a variety of ways, both directly and

indirectly. Direct interconnectedness happen mostly through mutual credit exposures

while indirect interconnectedness occurs mainly through common asset holdings, margin

call losses and haircut increases triggered by fire sales and liquidity drain and information

spillover (Liu et al.(2015)).

Direct interconnectedness occurs because mutual credit exposures between financial

institutions can lead to domino effects. With the complex chains of intermediation which

exist in the global financial system, the failure of a highly interconnected institution can

cause major disruptions to the financial system as a whole as this institution wouldnŠt

be able to fulfill itŠs obligations and cause mark-to-market losses in the balance sheets

of all other institutions with direct exposure to it, which could cause a number of other

institutions to face distress as well.

Indirect interconnectedness occurs as institutions facing distress can start fire selling

itŠs assets. Fire sales further stress the market prices of the assets owned by the company,

causing mark-to-market losses in all institutions with common asset holdings and causing

increases in margin calls and haircuts in repurchase agreements backed by these assets.

Information spillover can also cause other institutions with similar balance sheets to

As more institutions suffer losses and become distressed, market conditions may

further deteriorate via the aforementioned contagion channels, leading to a negative

feedback loop and, possibly, to a cascade of failures.

While many approches to understand the dynamics of financial contagion using

equation-based modeling have been developed, mostly through economic and network

models (see Gai and Kapadia (2010), Huang et al. (2013) and Elliott et al. (2014)),

these approaches have the limitation of reproducing an homogenized and simplified

approximation of the observed reality, sometimes producing unrealistic models which

are not sufficiently justified (Helbing and Balietti(2010)).

In this work we focus on the prospects of the computer simulation of economic

systems to model the dynamics of financial contagion. Agent-based modeling is a

computational technique where the components of a system are encapsulated as agents,

which can represent individuals, groups, companies and/or countries, while the analysis

of the system is carried out through the interactions of these agents (Helbing(2012)).

By modeling the financial system through the use of agents, we are capable not

only of creating simulations that reflect the interactions between different entities more

accurately, but also of testing the implications of different hypothesis. We furthermore

emphasize the importance of building models using a range of empirical observations

to design more realistic models which are capable of representing market dynamics

observed in historical episodes and allows us to explore in more detail the dynamics of

financial markets.

In this work we focus on modeling one of the most prominent effects of the

2007-08 financial crisis: the liquidity drain observed in the repurchase agreement (repo)

markets. During the crisis both interbank lending and repurchase agreements shrank

dramatically, causing a massive deleverage in the financial system and threatening

several banks with insolvency in a movement that only stopped through a government

47 3.2. Financial Contagion

market funds and hedge funds in the repo and interbank markets in order to recreate

this financial contagion movement.

The remainder of this paper is structured as follows. In Section3.2 we introduce

the problem of financial contagion and focus on the repo markets. Section3.3discusses

agent-based models of financial markets and how they can be used to understand

market dynamics such as the one we wish to model. Section 3.4 presents our

agent-based financial contagion model. In Section3.5we perform some numerical simulations

and discuss the results. Finally, in Section 3.6 we discuss extensions of the proposed

method and our conclusions.

3.2

Financial Contagion

Strong financial contagion has been one of the key features of most recent financial

crises, as localized problems in certain segments of the markets spread to other segments

leading to the risk of cascading defaults and failures which are often avoided through

government bailouts of institutions deemed "too big to fail".

As described byGorton and Metrick(2009), the panic of 2007-08 occurred through

a run on the repo market. The repo market is very important market that provides

collaterized financing for banks.They work very much like bank deposits, but for firms

operating in the capital markets. In a repurchase agreement the bank sells a security

with the promise of repurchasing the security at a specified price in the end of the

contract. The intermediary buying the security from the bank is remunerated by the

spread in operation.

According toGorton and Metrick (2009), in the last twenty-five years a number of

financial innovations have allowed traditional assets of banks to be traded in capital

markets through securitization and loan sales and have allowed banks to leverage

Since the 2007-08 crisis, the interconnected nature of financial markets has not

only been studied as an explanation for the spread of risk and losses throughout the

system, but also motivated much of the policy recommendations in the aftermath. Yet,

a framework to understand how the dynamics of the network structure of the financial

market, specially the repo market, leads to systemic risk remains incomplete.

In a broader sense, there is currently a high level of uncertainty about which elements

in the structure of the financial system causes contagion and how it occurs. Early work,

prior to the crisis, focused on general aspects of interbank lending such as the work of

Allen and Gale(2000), which modeled contagion as an equilibrium phenomenon caused

by liquidity preference shocks through economic regions, and of Rochet and Tirole

(1996), which considers the systemic risk created by interbank lending and investigates

whether decentralized bank interactions can be preserved while maintaining the stability

of the system.

More recent work, such as Gai and Kapadia (2010), Acemoglu et al. (2013) and

Elliott et al.(2014) examine how shocks propagate through a network based on debt

holdings or interbank lending and, also, how shocks propagate as a function of network

architecture.

While these works have provided useful insights about financial contagion (although

presenting quite different and complementary results), the use of economic equilibrium

and network models have some limitations in the study of the phenomenon. For

instance, financial agents usually have different goals and strategies, thus, behaving

very differently. Also, we must consider that the nature of debt exposures as connectivity

measures can also vary greatly, with mutual lending exposures, cross-holding of shares,

repurchase agreements and common asset holdinds of other sorts (e.g. stocks) having

a different impact on the propagation of shocks.

Accounting for these heterogeneities in network and economic models can lead to

49 3.3. Agent-Based Computational Finance

accurate representation of the financial system, despite being unable to render an

analytical solution to understand the problem, is to use agent-based simulation, as we

describe bellow.

3.3

Agent-Based Computational Finance

Much of the work in economics and finance hopes to simplify human interactions and

behaviors in a way that we can analyze these systems through aggregated macro-features.

But complex systems involves complex interactions among many individuals and, in

some cases, this complexity makes the use of analytical models to understand the

system unfeasible. For this reason, agent-based models and simulations have become

an invaluable tool for understanding the dynamics of the economic and/or financial

system as a whole.

Agent-based models are a class of computational models used to simulate the actions

and interactions of autonomous agents (Gilbert(2008)). In computational economics,

these models have been used to study properties of markets by building and simulating

markets, especially in the field of computational finance and there are many ways in

which agent-based models can be used to study financial markets1

The building of artificial markets is one of the most important contributions of

agent-based models to the study of financial systems. They allow us to model economic agents

according to a theoretical model and to observe if our economic assumptions about the

agents interactions in a financial setting would generate the expected dynamics.

Since the eighties some models of artificial markets have been tried, specially for

stock markets. Cohen et al.(1983) tried to look the impact of random behaving agents

on various market structures, while Kim and Markowitz (1989) used discrete event

1

simulation to model the interactions of different kinds of trading agents andDe Grauwe

et al. (1995) focused on the dynamics of foreign exchange markets.

One of most notable and most sophisticated markets is the Santa Fe Institute (SFI)

market. The SFI market was created with the idea of modeling a financial market

with an ecology of trading strategies (LeBaron (2002)). The SFI Market structure

was modeled to consider preferences and risk aversion in trading and even allowed

the emergence of trading patterns over time through the use of genetic algorithms.

Although there have been several generations of the SFI artificial market, consisting

of modifications of the market structure and of different programming platforms, the

fundamentals of the theoretical model have persisted2.

Other artificial stock markets have been designed focusing on features not included

in the SFI artificial market model. For instance,LeBaron(2001b) andLeBaron (2001a)

have used a new framework including varying forecasting horizons and memory lengths,

which is crucial in the convergence to a rational expectations equilibrium, while

Ser-guieva and Wu (2007) have investigated herding behaviors as a possible reason for

contagion among different markets, and Martinez-Jaramillo and Tsang (2009) have

elaborated an artificial market in which trading behaviors model technical,

fundamen-tal and noise traders, being able to recreate statistical properties of price series in real

financial markets.

Outside of stock markets, Arciero et al.(2008) developed a model of real time gross

settlement paying system for predicting the impact of disruptive events in the flow of

interbank payments andLlacay and Peffer (2010) developed a model to simulate crisis

and risk management in fixed-income markets.

Agent-based models of financial markets have allows to simulate and recreate

episodes observed in historical data to assess economic theories. In this work we

2

51 3.4. The Artificial Repo Market Model

focus on building an artificial repo market and itŠs behavior under a liquidity shock.

3.4

The Artificial Repo Market Model

To simulate the dynamics of financial contagion in the repo market we build an artificial

financial market where financial agents must manage their risk and may face defaults

and bankruptcy if there are significant imbalances between their balance sheets. The

financial risk is measured and controlled trough losses, liquidity and leverage metrics.

Our artificial market structure is designed to reflect financial intermediaries that

may choose to invest in a set of tradeable assets from outside the financial system

(representing economic projects) and that can also make operations among themselves

to improve resource allocation.

We design three types of financial intermediaries as agents, which can be banks,

money market funds (MMFs) or hedge funds. These intermediaries interact with each

other trading assets according to their roles, as described bellow, and with an

optimiza-tion strategy. Every intermediary tries to maximize their gains while managing their

risk.

3.4.1 Assets

For the assets that can be traded by the agents, there is a risk free government bond,

a stock, representing a risky liquid asset, and a risky fixed-income asset (from this

point only called risky asset), representing a economic project financed and securitized

by banks. The intermediaries can also trade resources through interbank lending and

repurchase agreements. These serve as instruments for them to improve resource

allocation, and manage risk.

List of Assets:

In our market there is a government bond, consisting of a risk free asset, paying a

constant interest rate, �f =0.10. This asset has complete liquidity as there is we assume there are external agents willing to match the order imbalance (treasury,

foreign investors, central banks, etc.).

B) Stock

There is also a risky stock, similar to the one described inLeBaron(2002), paying

stochastic dividend following the autoregressive process:

�t=�¯+�(�t−1−�¯) +Ût (3.1)

with �¯ = 10, � = 0.95 and Û

t ∼ �(0,àµ2). The price of the stock is determined endogenously in the market.

C) Risky Asset

There is a risky asset paying a constant interest rate�r=0.11. This asset represents an economic project financed by banks and securitized in the capital markets. This

asset can lose liquidity fast and may be a major source of risk. Since we do not

implement mark-to-market calculation of bond prices, mainly because there are

no variation in Government Bond interest rates, the higher interest rate reflects

exclusively the perceived liquidity risk and the default risk of the asset.

D) Interbank Loan

Interbank lending play a key role in the financial system. They are vital for banksŠ

liquidity management.The interbank lending market is constituted by unsecured

loans (the interbank loan) and secured loans (through repurchase agreements and

53 3.4. The Artificial Repo Market Model

The interbank loan is an operation where banks extend loans to one another for a

small term. In our model they are used when banks donŠt have access to secured

loans and must meet liquidity or cash requirements to avoid a default. The interbank

loan has an interest rater�IL = �f +Ói where Ói is the risk premium paid by the borrower and:

Ói =

︁ j��ij ︁

�i�sell(�)

(3.2)

where ��ij is the value of interbank loan issued from bank� to bank�, �i is the

total value of asset�owned by the bank�and�sell(�i)is the probability of selling the asset�at each timestep, which is determined by the liquidity index of the asset,

defined in Subsection 3.4.3. Interbank loans are always overnight.

E) Repurchase Agreement

Repos are a key mechanism in our fixed-income market. Repos require margining

practices, where the borrower pays an initial margin, or ŚhaircutŠ, to provide some

protection to the lender in case the other party defaults.

In our market, we implement a simplified version of repo operations3. Repos

can be backed up by Government Bonds or by the Risky Asset. Also, repos, as

interbank loans, are always overnight, but can be renewed at each time step. We

also implement margining pratices with the haircut being calculated as:

�������=1−�sell(�) (3.3)

3