A Work Project, presented as a part of the requirements for the Award of a Master Degree in Management from the NOVA – School of Business and Economics

OPERATIONS MANAGEMENT – PROCESS (RE) DESIGN IN COMMERCIAL BANKING

A PRATICAL EXAMPLE

APPENDIX

Cristiana Arnaut Godinho Antunes

2414

A project carried out on the Master in Management Program, under the supervision of Professor José Crespo de Carvalho

INDEX

Table I –Customers’ Segmentation ... 3

Flowchart I - Branch M General Process ... 4

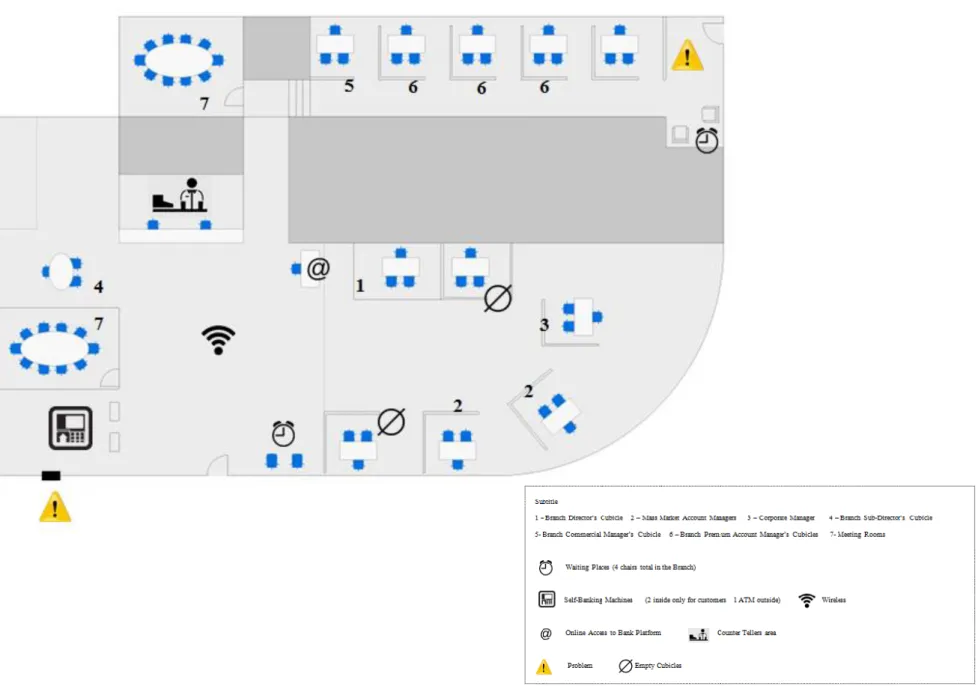

Figure I. - Branch M layout – AS IT IS ... 13

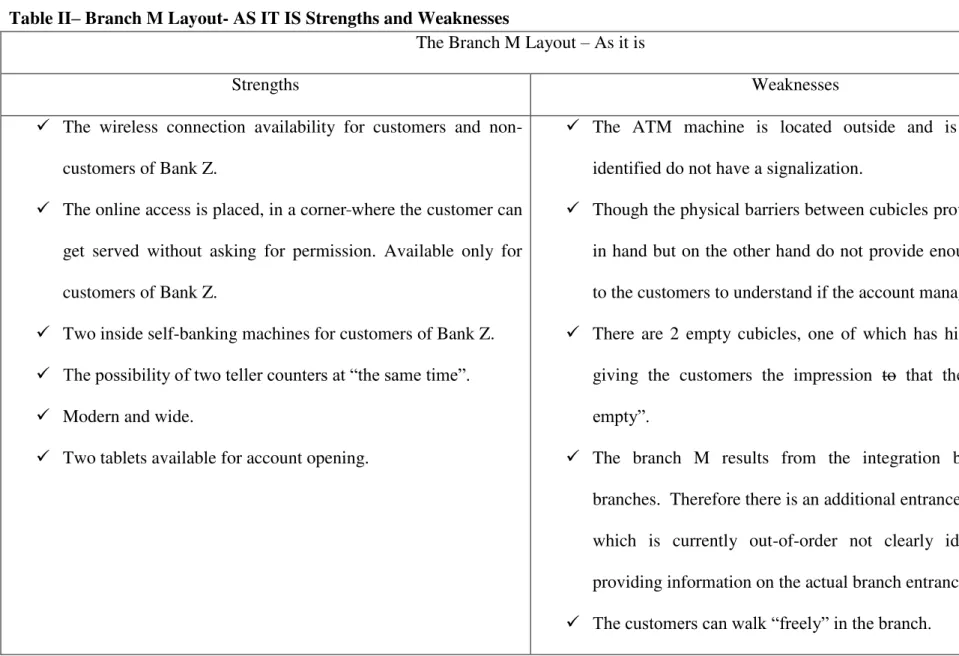

Table II– Branch M Layout- AS IT IS Strengths and Weaknesses ... 14

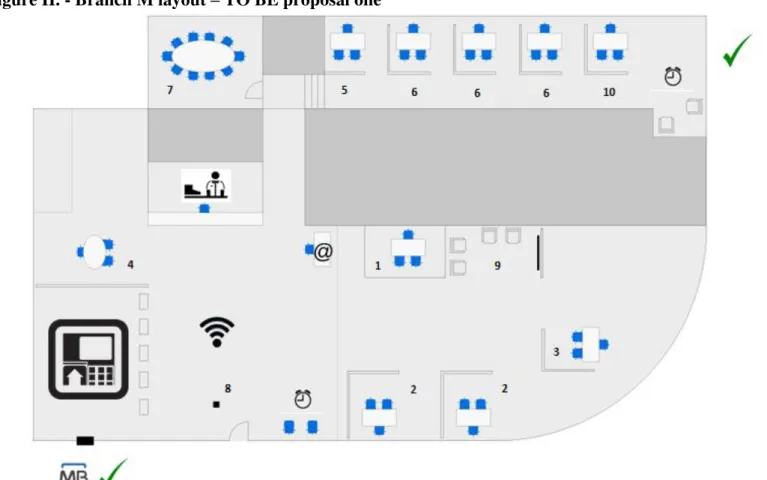

Figure II. - Branch M layout – TO BE proposal one ... 15

Figure III. - Branch M Layout – TO BE Proposal Two ... 16

Circular Charts I. – Percentage of customer per function May, June, July and August ... 17

Chart I. – Total Customer per half hour (May, June, July and August) ... 19

Charts II – Total Customer per half hour per month ... 20

Chart III – Total of Customers to teller counter per month ... 21

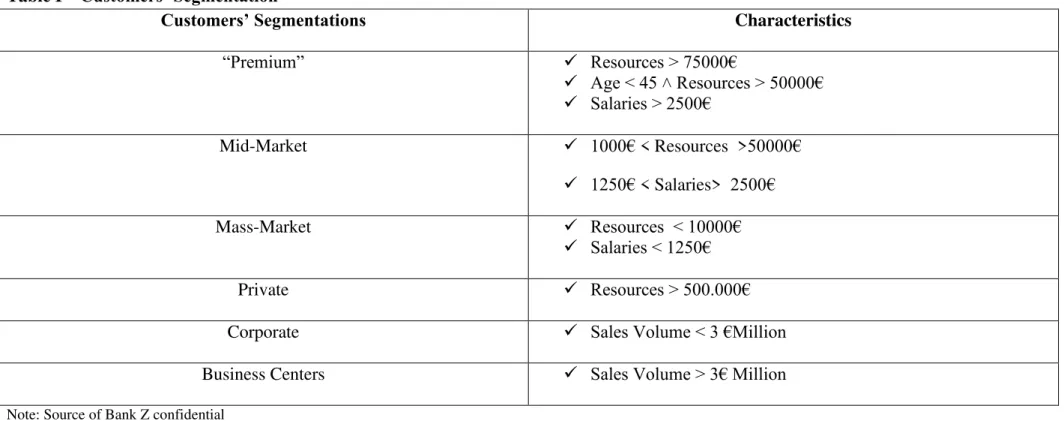

Table I –Customers’ Segmentation

Customers’ Segmentations Characteristics

“Premium” Resources > 75000€

Age < 45 ˄ Resources > 50000€

Salaries > 2500€

Mid-Market 1000€ < Resources >50000€

1250€ < Salaries> 2500€

Mass-Market Resources < 10000€

Salaries < 1250€

Private Resources > 500.000€

Corporate Sales Volume < 3 €Million

Business Centers Sales Volume > 3€ Million

Flowchart I - Branch M General Process

START Customer walks in

Is it for the AM?

Customer goes directly to self-banking machines Customer goes

directly to a desktop station

Customer goes directly to counter teller line

Customer is served Is it for the counter

teller?

Is it for self-banking machines? Is it for online

acess?

Any other services

required? END

Customer has queries

Customer is not able to use the machines

Customer goes to teller counter to ask

Customer fills in the relevant form Send the customer to

the cubicle

Back office sends the form to Central

Services Check via phone/

internal messenger the AM availability

Customer gets in touch with

the “bank” later

Customer is served Are all queries

solved?

Is an AM available? Does the customer has

an appointment?

Is the customer willing to wait?

END Check via phone/

internal messenger who is available

Central Services Feedback Back office receives

the form

Back office proceeds 1

Can the issue be resolved within the

branch?

Back office communicates the

solution to AM AM informs the

customer Yes Yes No No No

Customer waits for the 1st

Customer has a query

The customer answers the email

back Customer sends

Customer is served Is the customer

sending an email?

END 2

3

Customer is using the online tools

Is the customer using the branch email?

Is the customer calling?

The employee receives and answers

the email

Is the answer satisfactory? Customer sends an email to a specific branch employee Yes

Yes

The branch Director forwards the email

to an employee Yes

Does the customer need to go to the

branch? No

Yes No

Support line provides guidance

An employee answers the call Customer calls the

branch Customer is served

Does the AM solve the problem?

END 3

Customer still has queries Is the customer calling

to the bank support line?

The AM answers the call The customer calls

the AM mobile number

Does the support line solve the problem?

Is the customer calling to the branch telephone

number?

WALKING IN THE BRANCH - COUNTER TELLER SITUATIONS Weaknesses

- Waiting time to get served.

- Asking for the ATM machine inside the branch (even non-customers of the Bank Z).

- Interrupting a customer that is being served in other service.

- An employee has to manage situations: more than one customer at a time.

COUNTER TELLER

- Hypothesis 1 – When customer walks in the branch there is no queue, customer get served.

- Hypothesis 2 – When customer walks in the branch there are already some customers in the queue Additionally, due to the fact that are

two cubicles available for this function, when one is empty makes the perception on customers that there would always be second counter

teller that could start working any time there is a queue The previously described could result, not only in waiting time but eventually customer’s loudness, creating an uncomfortable environment. On the other hand, there is only one money verification machine and one

SELF-BANKING MACHINES/ ONLINE SERVICE

Hypothesis 1 – Customers walk in the branch and are served.

Hypothesis 2 – Customers are not able manage a situation on the online platform or in the self-banking and go to the counter teller asking for

guidance. The online/self-banking customer interrupts the teller counter procedures even if there is another customer being served at the branch

Counter teller asks for customer to wait until the online/self-banking customer is served.

WALKING INTO THE BRANCH –MEETINGS AVAILABLITY Weaknesses

- Waiting time to get served.

- The problem is not solved immediately or at the branch.

- Walking in without an appointment.

- Waiting time between branch and central services communication

- Interruption of ongoing appointments.

- Counter Teller has to manage the walk in customer the account managers: by telephone or internal messenger.

Hypothesis 1 – The customer has an appointment, the account manager is available so the customer gets served or is served by procedures performed by the branch back office.

Hypothesis 2 – The customer does not have an appointment but the account manager is available.

Hypothesis 3 – The customer does not have an account manager associated which means checking who is available.

Hypothesis 4 – The customer walks in without talking to and goes directly to an account manager’s cubicle because customer has already

developed a relationship with the account manager and knows how the branch is organized.

NOTE: There are some procedures that are performed by the back office employee. However there are other procedures that needs to be sent to

specific departments in the central services There is an answer time defined for the central services, that is in D+3 maximum,. However, due to

constrains, sometimes is not possible to comply with the answering time and therefore answer in that time, the role of the manager is to manage

the customer expectations who are not always able to understand and raise a complaint.

EMAILING THE “BANK” SITUATIONS

Weaknesses Points Waiting time for the on customer to get an the answer/problem solved.

Hypothesis 1 - The answer is simple and immediate and as a result customer gets served.

Hypothesis 2 - The answer involves the account manager or an employee asks for additional information to a specific department of central

services.

If the hypothesis 1 occurs the process ends and customer is served. On the contrary, if hypothesis 2 occurs it could lead to an eventual problem,

as the customer starts begins to call to the account managers or the Branch telephone. The Bank has the obligation to always answer the

customers. However, sometimes the needed time to get the situation clarified is greater than the time the customer is willing to wait and he walks

in the branch expressing some anxiety and back feedback on the service provided. These situation results on an eventual weakness point as the

customer requires clear information. Or want more clarifications on the issues.

CALLING THE “BANK”

Weaknesses:

- Waiting time to get served.

- Waiting time to get the call answered.

- The problem is not solved by the support line.

- Account Manager’s Availability.

Hypothesis 1 – The support line/account manager/a specific answering call can solve the customer query and resolve the problem

Hypothesis 2 -When the support line cannot solve the customer’s query, it must forward the customer to the branch for further clarifications. It is important to outline that not all queries are possible to be closed over the phone by the support line.

Once the customer enters the branch, his behavior may be conditioned by the telephone experience, where he feels the need of having access to

Table II– Branch M Layout- AS IT IS Strengths and Weaknesses

The Branch M Layout – As it is

Strengths Weaknesses

The wireless connection availability for customers and

non-customers of Bank Z.

The online access is placed, in a corner where the customer can

get served without asking for permission. Available only for

customers of Bank Z.

Two inside self-banking machines for customers of Bank Z.

The possibility of two teller counters at “the same time”.

Modern and wide.

Two tablets available for account opening.

The ATM machine is located outside and is not clearly

identified do not have a signalization.

Though the physical barriers between cubicles provide privacy

in hand but on the other hand do not provide enough visibility

to the customers to understand if the account managers are in

There are 2 empty cubicles, one of which has high visibility,

giving the customers the impression to that the “branch is

empty”.

The branch M results from the integration between two

branches. Therefore there is an additional entrance branch door

which is currently out-of-order not clearly identified and

providing information on the actual branch entrance.

Circular Charts I. – Percentage of customer per function May, June, July and August

33%

67%

% of customers per function May

% clients account manager % clients teller counters

73% 27%

% of customers per function June

12%

88%

% of customers per function July

% clients account manager % clients teller counters

18%

82%

% of customer per function August

Chart I. – Total Customer per half hour (May, June, July and August)

0 50 100 150 200 250 300

TOTAL CUSTOMERS (M+J+J+A)

Charts II – Total Customer per half hour per month

0 10 20 30 40 50 60 70 80 90 100

Num

ber

o

f

cus

to

m

er

s

Half Hours

Total customers Half Hour per month

MAY

JUNE

JULY

Chart III – Total of Customers to teller counter per month

0 10 20 30 40 50 60 70 80 90 100

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31

Num

ber

o

f

cus

to

m

er

s

Total of customers to teller counters per month

May

June

July

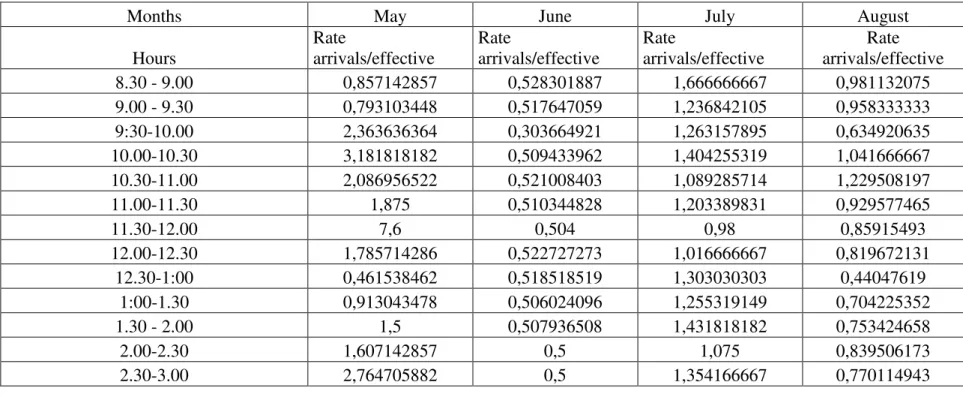

Table III. – Percentage of customer arrivals versus effective customer per month

Months May June July August

Hours

Rate

arrivals/effective

Rate

arrivals/effective

Rate

arrivals/effective

Rate arrivals/effective

8.30 - 9.00 0,857142857 0,528301887 1,666666667 0,981132075

9.00 - 9.30 0,793103448 0,517647059 1,236842105 0,958333333

9:30-10.00 2,363636364 0,303664921 1,263157895 0,634920635

10.00-10.30 3,181818182 0,509433962 1,404255319 1,041666667

10.30-11.00 2,086956522 0,521008403 1,089285714 1,229508197

11.00-11.30 1,875 0,510344828 1,203389831 0,929577465

11.30-12.00 7,6 0,504 0,98 0,85915493

12.00-12.30 1,785714286 0,522727273 1,016666667 0,819672131

12.30-1:00 0,461538462 0,518518519 1,303030303 0,44047619

1:00-1.30 0,913043478 0,506024096 1,255319149 0,704225352

1.30 - 2.00 1,5 0,507936508 1,431818182 0,753424658

2.00-2.30 1,607142857 0,5 1,075 0,839506173

2.30-3.00 2,764705882 0,5 1,354166667 0,770114943

Months May June July August

Average customers effetive 25,57142857 27,55 30 41,52380952