THIS REPORT WAS PREPARED BY “STUDENT’S NAME”, A MASTERS IN FINANCE STUDENT OF THE NOVA SCHOOL OF BUSINESS AND

ECONOMICS, EXCLUSIVELY FOR ACADEMIC PURPOSES.THIS REPORT WAS SUPERVISED BY ROSÁRIO ANDRÉ WHO REVIEWED THE

M

ASTERS IN

F

INANCE

E

QUITY

R

ESEARCH

Growing after the emissions scandal

Entering into a “greener” market…

Volkswagen Group is under a lot of pressure after the emissions scandal. First there is a liquidity concern, second the consequences in its market share.

2016 sales figures shown luxury cars demand has more than compensated the decrease in mass market VW Group cars triggered by the scandal.

Commercial Vehicles business unit expects no considerable direct short-term effect of the scandal, protected by long term contracts with customers, which are mainly corporations.

VW Group’s Trucks expect to maintain and intensify their

leader position in Europe, after the acquisition of MAN and Scania. Power Engineering business unit expects smooth sales decrease following the market trend. Passenger cars business unit has started to expand their

portfolio to include more electric cars, in order to maintain sustainably their overall passenger cars market share. Volkswagen Group has started the “e-initiative” to invest

and grow their still small market share in this electric cars’ segment. It is expected CAPEX to revenues ratio of 7% for the following years to fund new production lines, which should be producing at least 30 full electrical car models by 2025.

Company description

Volkswagen Group is the second biggest automaker in the world, comprising more than 12 brands. Its automotive division includes production of passenger cars, light-commercial vehicles, trucks and power engineering. Besides the automotive division, Volkswagen Group also has a financial services division to potentiate and support financially the selling activity of its vehicles.

V

OLKSWAGEN

G

ROUP

C

OMPANY

R

EPORT

AUTOMOTIVE

5 JANUARY 2017

S

TUDENT

:

F

ILIPE

A

NDRADE

S

ANTOS

[email protected]

Recommendation: BUY

Price Target FY17: 204.37 €

Dividends Forecast FY17 9.77 € per share

Price (as of 6-Jan-17) 139.10 €

Bloomberg: VOW3:GR

52-week range (€) 92.70 - 143.10

Market Cap (€m) 70,842

Outstanding Pref. Shares (m) 206.205

Source:Bloomberg

(Values in € millions) 2015H 2016E 2017F

Revenues 213,292 223,810 230,229

EBITDA 14,383 32,338 33,742

Net Profit (1,363) 9,901 9,004

EPS -6.61 48.02 43.67

P/E (19.99) 4.89

VOLKSWAGEN GROUP COMPANY REPORT

Table of Contents

EXECUTIVE SUMMARY ... 3

COMPANY OVERVIEW ... 3

BUSINESS STRUCTURE ... 3

SHAREHOLDER STRUCTURE ... 5

ECONOMY AND INDUSTRY OUTLOOK ... 6

MARKET ANALYSIS ...11

COMPANY’S RISKS AND

OPPORTUNITIES ...12

VALUATION ...13

WEIGHTED AVERAGE COST OF CAPITAL ... 13

PASSENGER CARS ... 15

COMMERCIAL VEHICLES /POWER ENGINEERING ... 18

FINANCIAL SERVICES ... 20

EQUITY-ACCOUNTED INVESTMENTS ... 21

MULTIPLES ...25

SCENARIO ANALYSIS ...26

FINANCIAL STATEMENTS ...28

APPENDIX ...30

VOLKSWAGEN GROUP COMPANY REPORT

Executive summary

VW Group’s value comes mainly from the automotive division and we should look to the financial division as a complementary and non-operational division. VW Group have a considerable position in the Chinese automotive market. However, the company’s presence in China is done mainly by three joint ventures that produce and sell the cars there. There are just a few sales in China from VW Group that are indeed produced by a fully owned subsidiary (mainly just luxury cars produced outside China). So almost 43% of the total VW Group’s sales we can count to be visible just in these joint ventures, which are not consolidated into the company’s financials. For that reason, they were valued separately and added in the end to the VW Group forecasted equity value.

Company Overview

Volkswagen Group is a public German multi-national car manufacturer company, which is present in the stock market with the tickers VOW (ordinary shares)1 and VOW3 (preferred shares)2. The group started first as a single car

brand – Volkswagen – in 1937. Over the years, Volkswagen started to acquire other car, truck and motorcycle brands creating the Volkswagen Group. Nowadays, according to its 2016 third quarter figures, it is currently the second biggest automaker in the world, delivering almost the same number of vehicles as Toyota (the biggest automaker).

Although Volkswagen Group has operations all over the world, in approximately 150 countries3, its most important markets are Europe (43% of total

sales) and Asia-Pacific (also 43% of total sales).

Business Structure

Volkswagen Group is organized into 2 divisions: Automotive and Financial Services. The first is responsible for the production, development and sale of vehicles and engines. This same division includes 2 different business units: Passenger Cars and Commercial Vehicles / Power Engineering.

In the passenger cars business unit VW Group has 9 brands: Volkswagen passenger cars, Audi, Lamborghini, Bugatti, Ducati, Skoda, SEAT, Bentley and Porsche. All these brands ensure a diversified product portfolio to VW Group in the passenger cars market, being present in the 3 most important segments: utilitarian,

1 Ordinary shares have voting rights and normal dividends.

VOLKSWAGEN GROUP COMPANY REPORT

luxury and sportive cars. The purchase of Ducati brand in 2012 shows that VW Group is continuing to diversify at most its portfolio, going even into the motorcycles market. In terms of revenue this is the biggest business unit of the group, representing almost ¾ of total revenues in 2016. In terms of Operating Result (EBIT) this business unit is also the second most profitable, counting with an expected margin of 5.4% in 2016.

In the Commercial Vehicles / Power Engineering business unit there are 3 brands: Volkswagen commercial vehicles, MAN and Scania, which are mainly dedicated to the production of light commercial vehicles, buses and trucks. VW Group has been looking to enforce its position on the market segment of heavy trucks, purchasing in the last 8 years MAN and Scania and becoming this way the largest heavy truck manufacturer in Europe. The Power Engineering is a small part of this business unit, which produces large-bore diesel engines, turbomachinery, compressors and other power systems and gear, mainly for marine and stationary applications. Being the Power Engineering a declining sector and the commercial vehicles a smaller market than passenger cars, this business unit is expected to represent just 14% of the total group revenue in 2016. Its operating result (EBIT) has the smallest margin of the group, expecting to be 3.3% in 2016. This is due to the higher depreciation & amortization costs than in the passenger cars business unit.

Finally, the second division (financial services) offers dealer & customer financing, leasing, direct bank, insurance, fleet management and mobility offerings. The aim of this division is to potentiate and support financially the selling activity of the automotive division. Its revenue is mainly income from interests and commissions and depends heavily on the sales of the automotive division. Being a non-operating division, it has the smallest weight on the total revenue of VW Group. However, in terms of result the financial services division has the good margin, expecting to generate 7.3% of EBT in 2016.

VOLKSWAGEN GROUP COMPANY REPORT

which was extremely valuable to face the emissions scandal. Moreover, the agreed sale price enabled the VW Group to get an income of € 0.2 billion with this operation. In the 5 associates, three of them are publicly traded (Sinotruk Hong Kong Ltd, Bertrandt, and Navistar International Corp.) and two are private (GT Gettaxi Limited - GETT, and There Holding). Sinotruk Hong Kong Ltd is a truck manufacturer in Hongkong, China and the objective of VW Group with this partnership is to potentiate VW Trucks exports to China in both volume and premium segment. Bertrandt is a German company that offers engineering services for the automotive/aviation industry. Navistar International Corp. is an American commercial vehicles manufacturer and VW Group is looking to buy 16.6% of its equity no later than the beginning of 2017. GT Gettaxi Limited - GETT is an on-demand mobility services company based in Israeli. Lastly, There Holding is a company based in the Netherlands and owns 100% the HERE Group, which develops and sells high resolution maps. All of these last four investments in associates were done to promote partnerships for strategic technology and supply cooperation.

All of these equity investments are not consolidated into the group’s financials, amounting to the following values in the VW Group’s balance sheet in the end of 2015:

Assets

(under the name “Equity-accounted Investments”)

Dec 31, 2015 (€ million) Joint-Ventures:

FAW-Volkswagen Automotive Company 2,918

SAIC-Volkswagen Automotive Company 2,754

SAIC-Volkswagen Sales Company 152

Global Mobility Holding 1,950

Associates:

Sinotruk Hong Kong Ltd 318

Bertrandt 332

Navistar International Corp. NA

GT Gettaxi Limited - GETT NA

There Holding 668

Shareholder structure

VOLKSWAGEN GROUP COMPANY REPORT

Comparing this structure with 2014 structure, we see that there was a transfer of equity from all the group of investors to private shareholders. In fact, the only “slice” of this chart increasing from 2014 to 2015 is the private shareholders, meaning all the other groups of investors transferred equity to this first group.

Economy and Industry Outlook

Starting by looking to the automotive industry globally we can identify several important recent events. First, with special importance in the European economy there is the Brexit (i.e. the possibility of the United Kingdom leaving the European Union). In June 23rd, 2016, there was a referendum in the UK to find out the will of

the country to leave the EU and the result was a win for the “Yes” supporters. Being London the world finance centre, this result had a massive impact on the global markets. More specifically, the British pound fell dramatically, empowering the exports and slowing down the imports of the country. The main automotive manufacturing facilities in the UK belong to the companies: Toyota, Nissan, Tata Motors, BMW Group. Volkswagen Group has a small manufacturing facility in the UK for Bentley (brand for the luxury passenger cars segment), with a residual production compared to the other plants4. Thus, to buy non-luxury cars from

Volkswagen Group, British citizens have to import the cars, which is now more expensive than buying cars that are produced in the country (due to the British pound devaluation). In other words, the Brexit brought competitive disadvantages for VW Group in the biggest car segments (e.g. economy, executive, premium). Furthermore, the fact Toyota is the second biggest automaker in the world with a major and stabilized presence in the British market5, reinforces the difficulty for

Volkswagen Group to gain market share in the UK. Regarding the upcoming years, although there is still some uncertainty (i.e. it is still needed Parliamentary approval), the process for the UK’s exit from the EU is expected to be triggered in March 2017 and could be finalized by the end of 20186.

Second, continuing in the European outlook, we have the negative interest rates of the European Central Bank that have considerable effects on the economy. Negative interest rate means you have to pay to deposit your money in the bank. That was exactly what the European Central Bank have done in March 2016, when set the depositary rates at -0.4%7. The main reason was to fight back

the threat of deflation and push prices up to inflation again, stimulating economic growth. In fact, by penalizing who wants to hold excess cash, the ECB indirectly

4 Annual production of 10,014 cars, according to"Automotive Industry in the United Kingdom." Wikipedia. Wikimedia Foundation, n.d. Web. 30 Dec. 2016 5 "Motor Industry Facts 2010" (PDF). SMMT. Archived from the original (PDF) on 27 November 2010. Retrieved 28 February 2011.

VOLKSWAGEN GROUP COMPANY REPORT

pushed that cash into the economy. This monetary policy made the loan rates and corporate bond yields to fall down, having a positive effect in VW Group by making cheaper debt financing (i.e. decreasing interest expenses).

The IMF expects 0.3% of inflation for the Euro Area in 20168,

which is a really low value but still higher than 2015 inflation rate of 0.03% (figure 1). Among economists is commonly agreed that the deflation’s impact in the economy is negative9: if prices are going

down, people will postpone their consumption and purchases (so they pay less for the goods), slowing down the economy. In other words, with such a low inflation rate in 2016, Europe is threatened by an economic crisis, which would immensely impact VW Group. In fact, in 2016 the European market was responsible for around 43% of total vehicles sold by VW Group10. With this indirect increase in money

supply promoted by the ECB, the IMF expects a recover in inflation to 1.3% in 2017, boosting the European economy and, thus, boosting significantly the VW

Group sales.

Outside Europe, we have the Chinese economy slow-down, which affects transversely all manufacturing industries. China is the second biggest economy in the world in 2015 and it is expected to maintain that position in 201611. In the recent past this country has experienced

extremely high GDP growth rates for many years (figure 2), which was possible by increasing exponentially debt levels. In fact, the Chinese Debt-to-GDP ratio raised from 160% in 2005 to 246.8% in 2015, being taken annually almost one third of the GDP just to service the debt12.

When compared to the United States, United Kingdom and Japan, this ratio is not that alarming, as you can see on the figure 3. However, if we look to the speed of this ratio increase, that is really alarming (i.e. +86.8% in 10 years). As result of such high and not sustainable growth rates, the Chinese economy growth is now slowing down, decreasing the usual high demand levels in China, reducing dramatically the global demand. Also because of this economy slow-down, the Chinese currency (Renminbi or Yuan) has devaluated brutally, promoting Chinese exports and slowing down the Chinese demand even more. This event is considerably dramatic for the global automotive industry, because China has the biggest automotive

8 International Monetary Fund, World Economic Outlook Database, October 2016

9 However, that classic interpretation of deflation’s impact was challenged by a study in 2004 by Andrew Atkeson and Patrick Kehoe: "Deflation and

Depression: Is There an Empirical Link?". According to: Root. "Deflation." Investopedia. N.p., 28 Sept. 2015. Web. 30 Dec. 2016.

10 Volkswagen Group Interim Report Q3 2016

11 In terms of nominal GDP, according to World Bank and to International Monetary Fund for 2015 and 2016, respectively. The biggest economy is U.S. 12 Scott, Malcolm, and Cedric Sam. "China's Growing Debt Problem Isn't Quite What It Seems." Bloomberg.com. Bloomberg, 23 Aug. 2016. Web. 30 Dec.

2016.

247% 251% 266%

392%

C H I N A U S U K J A P A N

F i g u r e 3 : D e b t - t o - G D P R a t i o 2 0 1 5

Source: Bloomberg Source: World Bank

2% 4% 6% 8% 10%

2011 2012 2013 2014 2015

Figure 2: Real GDP Annual Growth Rates

VOLKSWAGEN GROUP COMPANY REPORT

industry in the world since 2008. From 2009 on, China has exceeded Europe or US together with Japan in annual vehicles production13. Furthermore, being the

Chinese market responsible for 40% of the total vehicles sold by VW Group in 201614, this event has a considerable negative effect on this specific company’s

global revenue. The VW Group is also present in China through 3 Joint-Ventures, which increases even more the company’s exposure to this economy growth slow-down. The negative effect on those joint-ventures is already visible in the short-term: their annual sales growth rate decreased from 13% in 2014 to 3.9% in 201515.

Another important market that is currently in trouble is Brazil. Similarly to China, Brazil has experienced high growth rates in the past years. In Brazil’s case, the country economy’s risks have arisen from rampant inflation and corruption. In fact, in 2009 the Brazilian currency (Real) was considered the most overvalued currency around the world16. However, it was China’s

slow-down that was the key factor to trigger Brazil’s recession. In 2013, Brazil’s exports to China represented almost 50% of its entire exports17. In

fact, this trading relationship was so intense, that the yuan’s devaluation and the Chinese economy slow-down was enough to disturb the entire Brazilian economy in a domino effect. This event affects negatively VW Group because Brazil represents about 2.5% of its total vehicles sold in 201618.

In North America, the United States is the most important market for VW Group, representing 6% of its total vehicles sold in 201617. Thus, it is worth it to

take a look to this market and to its risks and opportunities. The United States has recovered from the 2008 global financial crisis better and quicker than Europe. Inflation is also higher than in Europe and in good shape: IMF expects 2.3% of inflation for 2017. Real GDP has also been increasing at a higher rate, as you can see on figure 5. As a result of rising inflation and a better situation for employment, FED has been considering a raise in the interest rate. However, if FED increases the interest rate too aggressively, is going to create a stock market crash as it happened in October 198719. In fact, an increase in interest rates

controls the inflation, avoiding speculative bubbles; but if it is not in line with global economic reality, it easily generates a crash. In December

13"RIA Novosti - World - China becomes world's largest car market". En.rian.ru. Retrieved 2009-04-28. & "China emerges as world's auto epicenter -

Politics- msnbc.com". MSNBC. 2009-05-20. Archived from the original on 19 May 2009. Retrieved 2009-05-25. & "More cars are now sold in China than in America". The Economist. 2009-10-23.

14 Volkswagen Group Interim Report Q3 2016 15Volkswagen Group Annual Report 2015 16 Bloomberg

17 Sharma, Rakesh. "Brazil's Recession and Its Effect on the World Economy." Investopedia. N.p., 08 Sept. 2015. Web. 31 Dec. 2016. 18 Volkswagen Group Interim Report Q3 2016

19 Minerd, Scott. "Fed Rate Rise History Reveals Familiar Dilemma." Financial Times. N.p., 14 Sept. 2015. Web. 2 Jan. 2017.

2.5%

1.6% 2.3% 2.2% 2.4% 2.3%

-1% 0% 1% 2% 3% 4% 5%

2010 2011 2012 2013 2014 2015 Figure 5: Real GDP Annual Growth

Rates

World United States

Europe

VOLKSWAGEN GROUP COMPANY REPORT

14th, 2016, it was announced that the FED has increased the interest rate by 25

basis point to 0.75%20. Furthermore, it was forecasted three further increases in

the interest rate for 2017, instead of just two. This forecast increase might have been influenced by the proposal of Donald Trump to “beef up the infrastructure spending and cut taxes”21. Based on this decision, we forecast stable inflation rates

and also stable asset’s prices (e.g. stock market) for the United States. At corporate level, this will increase cost of capital. This is, we expect an increase in cost of debt and in cost of equity for the American market. Globally, there is one more event relevant for the automotive division, which is the declining crude oil prices. In the recent past years, the crude oil has been decreasing as it never did, achieving historical minimums (figure 6). Like any commodity, crude oil prices are set by the law of demand and supply. With a decreasing demand in Europe and China22

(due to their economy slow-down), a constant supply by OPEC23 (to

keep their market share) and an increase in US oil production24 (due to

the more efficient way of extracting oil, called fracking), there was excess production of crude oil, which caused its accentuated price fall. Since the crude oil is the main commodity in the global economy, this event affects negatively all industries around the world, including the automotive industry. In one hand, lower crude oil prices make citizens spending less money in transportation costs. In other hand, it disturbs the national budget and creates deficits in oil-dependent economies, such as OPEC members. In fact, some of those countries, with higher budgetary demands, needed an oil price per barrel much higher than the current one to have balanced budgets (figure 7). In the short term, IMF forecasts a considerable recover of crude oil prices in 2017, offsetting the -15% of 2016. In the long term, IMF forecasts a stable price increase of around 3% per year. However, crude oil prices above 100 USD per barrel, as it happened from 2011 to 2013, are not expected in the near future.

Being the highly use and dependence of crude oil in the global economy the main cause for the global warming, more and more alternative sources of energy are being developed in the current world. In the automotive industry, the global conscience about the risks of global warming has accelerated the demand for new alternative fuels and more efficient engines: such as electric engines, hybrid cars,

20 Media, Triami. "FED Federal Funds Rate, American Central Bank's Interest Rate." Federal Funds Rate FED - American Central Bank's Current and

Historic Interest Rates. N.p., n.d. Web. 02 Jan. 2017.

21 Davidson, Paul. "What Led Fed to Bump up Rate-hike Forecast?" USA Today. Gannett Satellite Information Network, 02 Jan. 2017. Web. 02 Jan. 2017. 22 Investopedia. "What Causes Oil Prices to Fluctuate?" Investopedia. N.p., 27 Jan. 2015. Web. 03 Jan. 2017.

23 OPEC stands for Organization of Petroleum Exporting Countries, comprising 13 countries, which are responsible for 40% of the world’s oil supply. 24 Bowler, Tim. "Falling Oil Prices: Who Are the Winners and Losers?" BBC News. BBC, 19 Jan. 2015. Web. 03 Jan. 2017.

184 131 131 118 105 101 77

L I B Y A I R A N A L G E R I A V E N E Z U E L A R U S S I A I R A Q Q A T A R

F i g u r e 7 : O i l P r i c e p e r b a r r e l n e e d e d t o B a l a n c e B u d g e t s ( U S D )

Source: Deutsche Bank and IMF (2015).

97.04 105.01 42.96 $20 $40 $60 $80 $100 $120

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Figure 6: Average* Crude Oil Price per barrel (USD)

VOLKSWAGEN GROUP COMPANY REPORT

ethanol, and natural gas. This change in mindset is also starting to contribute for a decrease in demand for crude oil, which makes down pressure on its prices. Nevertheless, this transition from traditional petroleum sourced engines to greener sources of energy is being smooth: in fact, there is a high historical dependence and reliability on crude oil as source of energy, which represents a road block for a faster transition. For example, in the automotive industry there are still much less battery power charging stations (for electrical cars) than gas stations, being more convenient for the drivers to continue using traditional petroleum-moved cars. Besides this infrastructure barrier, there are still considerable technology barriers to be overcome to turn these alternative electric cars sustainable for a normal daily driver: namely, the charging speed of the batteries and their electric range. The electric car brand that is the market leader for these two technologic features is Tesla Motors. This automaker is in the lead of this type of technology, being able to deliver electric cars that are 100% charged in 75 minutes (in specific Tesla supercharging stations, which are 769 globally25) and with a battery range up to

506 kilometres (prices for this model start at 134,500 USD). A “more average model” of Tesla starts its price at 66,000 USD and has a battery range up to 320 kilometres26. These figures are really good for the electric cars market but still really

far behind a € 17.2k diesel car that fuels up in 2-3 minutes and has a fuel autonomy up to 1,500 kilometres (car considered is shown in figure 8)27.

All these barriers give some extra time to the automakers adapt to this new market trend and preferences, changing the most important component of their product: the engine and the source of energy of the car. In terms of cost for the driver, on one hand, the driver is directly and immediately compensated by the cheaper cost of electricity compared to petroleum-based fuels. On other hand, the price for an electric car is on average about 90% higher28 than a traditional car moved by a

petroleum-based fuel. However, bear in mind that the first effect is much lower (or almost null) in countries with low petroleum-based fuels prices, such as the US. Without any other type of incentive, it is extremely difficult the entry of this new type of vehicles in these markets. For that reason and to decrease air pollution several developed countries are already implementing government subsidies to buy electric cars: the United States implemented in 2013 a $ 7,500 Federal Tax Rebate29 and France has currently a € 6,300 ecologic bonus plus a € 3,700

conversion premium30. Furthermore, to promote even more this change to greener

25 "Supercharger." Supercharger | Tesla. N.p., n.d. Web. 03 Jan. 2017.

26 Stoll, John D. "Tesla Unveils Electric-Car Battery With a 315-Mile Range." The Wall Street Journal. Dow Jones & Company, 23 Aug. 2016. Web. 03 Jan.

2017.

27 "Découvrir Les Prix Et Finitions De La Peugeot 208 3 Portes." PEUGEOT, n.d. Web. 03 Jan. 2017.

28 Calculations made using some of the cheapest economy cars available in Europe: Mitsubishi i-MiEV electriQ (19,950 € in France excluding government

subsidies) and Dacia Sandero gasoline (10,300 € in France).

29 Shahan, Zachary. "11 Electric Cars Cost Less Than Average New Car In US." EV Obsession. N.p., 08 Dec. 2013. Web. 03 Jan. 2017. 30 "Mitsubishi I-MiEV ElectriQ." Mitsubishi I-Miev - Véhicule électrique- I-MiEV ElectriQ. Mitsubishi, n.d. Web. 03 Jan. 2017.

VOLKSWAGEN GROUP COMPANY REPORT

cars, some governments already committed to ban the use of diesel cars in city centres by 2025, such as: Paris, Madrid, Mexico City and Athens31.

Market Analysis

The automotive industry started around 1890 with the first car being produced in 1886 by Carl Benz32. From then on, there were created several different car brands,

shaping the automotive market into an extremely competitive and diverse market. In 2015, Toyota was the biggest automaker in the world, followed by VW Group in second place, with a considerable advance to the automaker in third place, as you can see in the figure 9:

In 2012 Toyota got the first place as the biggest automaker in the world. Since then, VW Group has been getting closer and GM is kind of holding off (figure 10). During 2016, VW Group went back and forward, changing from 2nd to 1st place and vice-versa with its main rival: Toyota. If we look for the VW Group first semester 2016 sales performance, we can see that this group has become the biggest automaker in the world with 5.04 million cars delivered, passing Toyota with 5.02 million cars delivered33. However, if we look from

January to August in 2016, due to sudden increase in Toyota’s sales in August, Toyota took back the position of the biggest automaker with 6.69 million cars delivered, with just more 23 thousand cars than VW Group34.

For the next years, we do expect the VW Group to maintain its global market share.in the passenger car business area of about 13%, with a decrease in 2016 specially due to a sales decrease in North America (US, Canada and Mexico). This sales decrease we forecast as a result of the diesel issue, which will be discussed on the next part of the report.

To maintain its global market share, VW Group will have to enter harder on the electric cars’ segment. If we look to other automakers, we can say VW Group is kind of behind in this segment, losing market share in passenger cars as this

31 McGrath, Matt. "Four Major Cities Move to Ban Diesel Vehicles by 2025." BBC News. BBC, 02 Dec. 2016. Web. 03 Jan. 2017. 32 "Benz Patent Motor Car, the First Automobile (1885 – 1886)." Daimler. N.p., n.d. Web. 04 Jan. 2017.

33 Reuters

34 Schmitt, Bertel. "World's Largest Automakers 2016: Toyota Pulls Ahead Of Volkswagen -- By A Hair." Forbes, 28 Sept. 2016. Web. 04 Jan. 2017.

10.084 9.872

7.988 7.486 6.396

5.170 4.865 4.544

3.034 3.033

T O Y O T A V W G R O U P

H Y U N D A I -K I A

G M F O R D N I S S A N F I A T H O N D A S U Z U K I R E N A U L T

F i g u r e 9 : B i g g e s t A u t o m a k e r s i n t h e W o r l d ( m i l l i o n c a r s p r o d u c e d 2 0 1 5 )

Source: International Organization of Motor Vehicle Manufacturers

6 7 8 9 10 11

2013 2014 2015 Jan-Aug

2016 Figure 10: Top 3 Automakers

Trend (million cars sold)

Toyota VW Group GM

VOLKSWAGEN GROUP COMPANY REPORT

segment grows worldwide. In fact, with an ambitious forecast, the Wall Street Journal has published in November 2016: “By 2018, [electric vehicles] must account for 8% of the maker’s production, and the percentage will rise from there.” VW Group already took conscience of the importance of this electric cars segment and started to expand their electric cars portfolio by pursuing what they call a “e-mobility” initiative. With this adaption to the new market reality, we believe VW Group has sustainable competitive advantages capable of maintaining the automaker’s global market share in the long term.

In China, the Volkswagen passenger cars brand has the biggest market share in the passenger cars segment, selling almost the double of vehicles sold by the second biggest automaker in this segment, which is the brand Wulling35. The VW

Group cars sold in China are mainly sold through a joint-venture with FAW Group, called FAW-Volkswagen Automotive Company (which financials are not consolidated into the VW Group’s financials). However, the same FAW Group has other two 50-50 joint ventures with GM and Toyota, which have brands also in the top ten selling brands for passenger car segment in China. Furthermore, since these two companies also belong to the top four of the biggest automakers in the world, we can say this market is already kind of saturated with presence of major global players. Thus, there is not so much space for market penetration strategy (i.e. gaining market by penetrating in an existing market with existing products36). We believe the sustainable strategy for VW Group in China would be product development, launching the green cars’ segment to this market. However, since these other two big automakers (GM and Toyota) are also producing vehicles for the green cars’ segment we do not expect massive variances in VW Group’s market share in China. Actually, the Chinese government is already “barring car makers that don’t have new-energy capabilities”37.

Company’s Risks and Opportunitie

s

The biggest recent risk VW Group is facing is its global emissions scandal triggered in September 2015 involving fraud in reporting the CO2 emissions in two diesel engines produced by the Group. As result, two types of consequences were expected. First, direct financial consequences regarding car recalls, repurchases, reprogramming and lawsuits charges, which not only negatively affect the net income of the Group but also its liquidity. This first short-term consequence generated costs of € 16.2 billion in 2015 for the group. Second, more in the

35ChinaAutoWeb. China Passenger Car Association (CPCA), n.d. Web. 04 Jan. 2017. 36 Following the principles of the Ansoff Matrix or Product/Market Expansion Grid.

VOLKSWAGEN GROUP COMPANY REPORT

term, it is also expected to be an indirect negative consequence on the sales performance, as the customers can easily lose its confidence in this car manufacturer. However after looking to the fact VW Group became the world largest automaker in the world in the first semester of 2016, we can conclude the first direct consequence is much more certain than the second. Thus, we can expect that this scandal is much more likely to produce only a short-term negative effect than a long-term one. This means, this scandal will have a residual impact in our company valuation as of 2017.

Valuation

To value the Volkswagen Group we have decided to divide the group into 2 parts: an operating one (including the automotive division, with the 2 business units of passenger cars and Commercial Vehicles / Power Engineering) and a non-operating one (including the Financial Services Division, the equity investments in Associates and Joint-Ventures, and some others non-operating assets & liabilities). Pursuing a “sum-of -parts” approach, we valued individually each part of the company and summed in the end their equity values to get the total VW Group equity value.

Weighted Average Cost of Capital

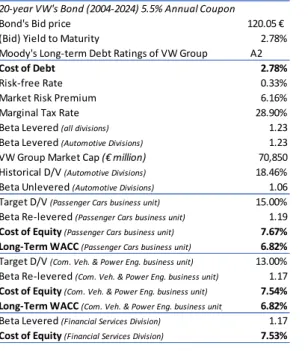

For the cost of debt, we have used a publicly traded long-term bond of the VW Group (figure 11). Since the Moody’s long-term debt rating of VW Group is “A2”38, which is within the superior credit quality level,

we have assumed reasonable to consider zero probability of default of VW Group. Thus, we have used the market Yield to Maturity of a long-term actively traded bond of VW Group as proxy for the real cost of its debt. The specific bond chosen was “VW 5.500% 07Jun2024 Corp (EUR)”, being a 20-year bond in Euro with a 5.5% fixed annual coupon. With a bid price of 120.05€, this bond has a Yield to Maturity of 2.8%39, which we have used as cost

of debt for VW Group.

To estimate the cost of equity, we have considered a risk-free rate of 0.33% (Rf), using the 10-year AAA-rated Euro area central government bonds40. For market risk premium, we have used

6.16%41, which has been considered reasonable by several

38 "Moody's Downgrades VW Financial Services' Long-term Debt Ratings to A2 from A1 and Upgrades VW Bank's Debt Ratings to Aa3 from A1."

Moodys.com. N.p., 03 Aug. 2016. Web. 02 Jan. 2017.

39 As of January 2nd, 2017. Source: “Bond Fact Sheet” in www.bondsupermart.com.

40 Bank, European Central. "Euro Area Yield Curve." European Central Bank. N.p., n.d. Web. 02 Jan. 2017.

41 Damodaran, Aswath. "Damodaran Online" New York University Stern School of Business, Jan. 2017. Web. 04 Jan. 2017. 20-year VW's Bond (2004-2024) 5.5% Annual Coupon

Bond's Bid price 120.05 € (Bid) Yield to Maturity 2.78% Moody's Long-term Debt Ratings of VW Group A2

Cost of Debt 2.78%

Risk-free Rate 0.33%

Market Risk Premium 6.16% Marginal Tax Rate 28.90% Beta Levered (all divisions) 1.23 Beta Levered (Automotive Divisions) 1.23 VW Group Market Cap (€ million) 70,850 Historical D/V (Automotive Divisions) 18.46% Beta Unlevered (Automotive Divisions) 1.06 Target D/V (Passenger Cars business unit) 15.00% Beta Re-levered (Passenger Cars business unit) 1.19

Cost of Equity (Passenger Cars business unit) 7.67% Long-Term WACC (Passenger Cars business unit) 6.82%

Target D/V (Com. Veh. & Power Eng. business unit) 13.00% Beta Re-levered (Com. Veh. & Power Eng. business unit) 1.17

Cost of Equity(Com. Veh. & Power Eng. business unit) 7.54% Long-Term WACC (Com. Veh. & Power Eng. business unit) 6.82%

Beta Levered (Financial Services Division) 1.17

Cost of Equity (Financial Services Division) 7.53%

VOLKSWAGEN GROUP COMPANY REPORT

studies. The levered beta for VW Group of 1.23 was obtained by performing a regression between MSCI World Index (in Euro) and the VW Group stock itself with weekly prices for the last 3 years42. Since the automotive division represents

the major part of this company’s value, we assumed that the beta levered of the automotive division is the same as the levered beta of the entire company. The unlevered beta for the automotive division of 1.06 was obtained using its historical D/V ratio of 18.5%43 (market values). Then, we have computed a specific

re-levered beta for each business unit inside the automotive division, according to their specific target D/V ratio44. The leveraging and un-leveraging operations were

done using the equation: BU = BL / [1 + (1- Tc) x (D/E)]45. After all this, we got a

re-levered beta of 1.25 for the passenger cars business unit and a re-re-levered beta of 1.22 for the commercial vehicles and power engineering business unit. For the levered beta of the financial services division we have used 1.17, which was obtained by performing a regression between MSCI Europe Banks Index (containing comparable companies to this financial services division) and MSCI World Index for the last 5 years using monthly prices46. Then, applying the Capital

Asset Pricing Model (CAPM) formula (RE = Rf + BL x Market Risk Premium)47, we

got three costs of equity: 8.01% for the passenger cars business unit, 7.87% for the commercial vehicles and power engineering business unit and 7.53% for the financial services division.

Finally, we have used these values to compute the WACCs for the two business units of the automotive division: 6.80% for passenger cars and 6.81% for commercial vehicles and power engineering. For these calculations we have used the formula: WACC = D/V x RDx (1 – TC) + E/V x RE48.

Moving on to the next valuation step, in the operating part of the group, (the automotive division), we have opted to do two Discounted-Cash Flow models (one for each business unit), forecasting the free cash flow to the firm generated in the next 5 years (from 2017 until 2022), computing a terminal value on the 5th year and

then discounting those values at the WACC. Summing these discounted cash flows and terminal value, we got the operating enterprise value of the two operating business units (Passenger Cars and Commercial Vehicles / Power Engineering), which after deducting the correspondent net debt gave us their equity value.

42 Reuters. As of December 30th, 2016, with a confidence interval [1.20-1.26] considering a confidence level of 95%.

43 Using the book value for the debt value (which is considered a good proxy for market value in terms of debt) and using the market cap of € 70,850 million

for the equity value (as of December 28th, 2016)

44 Defined based on the 2015’s ratios we got from dividing debt by the market enterprise value of that year (which we have estimated in our DCF’s models).

45being “T

c” the marginal tax rate (28.9%), “D/E” the Debt to Equity ratio, and “BU” and “BL” the unlevered and levered beta, respectively.

46 As of April 2016, with a confidence interval [0.91-1.43] considering a confidence level of 95%. 47 Where R

E is the cost of equity, Rf the risk-free rate and BL the beta levered. 48

VOLKSWAGEN GROUP COMPANY REPORT

Passenger Cars

The passenger cars business unit was the most exposed business unit with the diesel emissions scandal in 2015. However, in 2016 a remarkable and quick sales recovery was verified. In fact, the mass market VW Group’s brands suffered a considered decrease in sales, which was more than compensated by an increase in demand for cars of the premium brands Porsche and Audi. The VW Group’s brand Skoda has contributed also to counteract against the sales decrease. So, we can conclude that the diesel scandal had a negative financially effect on VW Group mainly in the short-term, outperforming competitors in 2016 and not influencing negatively the overall car sales in the short term. However, as we get closer to the end of 2018, we have a negative and very likely event to happen: the exit of the UK from the European Union. Once this happens, the VW Group sales in the UK will depend on new trade agreements between UK and Europe, which are not outlined so far. Furthermore, the UK represents 17% of global VW Group’s sales and VW Group only has a small plant in the UK for Bentley. So after the UK’s exit, if there are applied protectionists measures, VW Group’s sales will be highly affected. Based on this, we have forecasted a slower sales volume growth for 2017 (1%) and an annual 0.5% sales volume decrease in Europe for 2018 and 2019. After the European market has adjusted to this new reality, we expect a recovery in sales volume, achieving sales of 4.5 million passengers in 2020. For next years, 2021 and 2022, boosted by the ECB efforts in stimulating the European economy, we forecast annual growth rates of 1% and 2%, respectively.

With the win of Donald Trump for the Presidential election in the US in 2016, we expect a move into a much more protectionist economy already in 2017, penalizing the imports and stimulating the goods produced in the US. As VW Group only has 5% of its production facilities in North America49, we consider this event

will have a significantly negative effect on this company’s sales in US (which represents more than 60% of VW Group’s sales in North America50). Thus, we

expect a fall in sales in North America from 2017 to 2019, followed by a smooth and stable annual 0.5% growth from 2020 on.

For sales in Asia-Pacific we have assumed the same growth rate as the VW Group’s Chinese joint ventures: a stable 4% annual growth rate from 2018 on (increasing smoothly in 2021 and 2022), based on the country’s planners forecast51,

which will be explained further in this report, in the equity-accounted investments’ part.

49 Volkswagen Group – 2015 Annual Report. 50 Volkswagen Group – 2016 Interim Q3 Report.

VOLKSWAGEN GROUP COMPANY REPORT

For the South America’s sales, since Brazil accounts for more than 63% of this region’s total sales52 and Brazil’s economy deeply depends on China, it was

forecasted a sales performance partially influenced by the Chinese economy. Thus, we expect it will grow over the years at a constant rate, achieving 600 thousand passenger cars sold in 2022, as you can see below in figure 12.

Globally, with our revenue forecast for this business unit, we expect an slightly increase in VW Group’s market share in 2017 in the passenger cars segment, followed by a decrease in 2018 and stabilizing at 13.1%-13.2% from 2019 on. This market share increase and sustainable stabilization forecast is also based on revealing company statements about significant investments projects to launch 30 new all-electrical models until 2025, which will turn VW Group more competitive in the “green” cars segment. This new repositioning of the company to focus on attractive and fast-growing market segments as a response to the scandal ensures to VW Group the ability to adapt to the current changing environment of the automotive industry, becoming more competitive.

Using the IMF forecast for the Euro inflation rate53, we have adjusted annually

the average VW Group passenger car price. Multiplying that adjusted car price by the forecasted number of cars sold we got the revenue forecast for this business unit, which was the starting point to forecast its income statement and its DCF model (figure 13).

52 Volkswagen Group – 2016 Interim Q3 Report.

53 International Monetary Fund, World Economic Outlook Database, October 2016

Passenger Cars (PC) - Revenue Estimation Brands: Volkswagen Passenger Cars, Audi, SEAT, ŠKODA, Bentley, Bugatti, Lamborghini, Porsche, Ducati Millions of Cars 2013 2014 2015 2016 E 2017 F 2018 F 2019 F 2020 F 2021 F 2022 F

Passenger Car Sales Worldwide 67.24 70.66 72.37 74.31 75.59 77.69 79.85 82.07 83.68 85.84

Growth Rate Worldwide - 5.1% 2.4% 2.7% 1.7% 2.8% 2.8% 2.8% 2.0% 2.6%

VW Group Pas. Car Sales (incl. Joint Ventures) 9.07 9.58 9.37 9.99 10.18 10.32 10.48 10.73 10.98 11.31

VW Group Market Share (incl. Joint Ventures) 13.5% 13.6% 13.0% 13.4% 13.5% 13.3% 13.1% 13.1% 13.1% 13.2%

VW Group Car Sales by Region: 5.8% 2.0% 5.1% 1.0% -0.5% -0.5% 1.1% 1.0% 2.0%

Europe 3.92 4.15 4.24 4.45 4.50 4.48 4.45 4.50 4.55 4.64

North America 0.84 0.82 0.88 0.93 0.90 0.88 0.87 0.88 0.88 0.88

South America 0.92 0.74 0.51 0.53 0.54 0.55 0.56 0.58 0.59 0.60

Asia-Pacific 0.25 0.61 0.29 0.31 0.32 0.33 0.35 0.36 0.38 0.39

VW Group Pas. Car Sales (excl. Joint Ventures) 5.94 6.33 5.92 6.22 6.26 6.24 6.24 6.31 6.39 6.51

Euro Inflation Rate 1.5% 0.5% 0.0% 0.3% 1.3% 1.6% 1.7% 1.8% 1.8% 1.8%

Average VW Group PC Price (€) 24,084 23,245 26,016 26,084 26,432 26,853 27,303 27,785 28,295 28,793

VW Group PC Sales Revenue (€ million) 142,961 147,080 153,964 162,266 165,485 167,670 170,300 175,426 180,781 187,555

VOLKSWAGEN GROUP COMPANY REPORT

NOPLAT means Net Operating Profit Less Adjusted Taxes and is the starting point for the unlevered free cash flow calculation. The NOPLAT was computed using the formula: EBIT x (1 – Tc) – Adjust. & Deferred taxes.

The unlevered free cash flow represents the cash flow to the firm (i.e. to shareholders and debtholders) and was computed using the formula: UFCF = NOPLAT + Non-cash Expenses (i.e. Dep. & Amort. and Impairments) + Cash flow from Investing Activities (i.e. capital expenditures, change in vehicles leased out, capitalized development costs, change in operating net working capital and change in other operating assets/liabilities).

In VW Group expects to increase its CAPEX to revenues ratio to 7%54. VW

Group is looking more and more to invest in new production lines and R&D for “greener” passenger cars models. This adjustment of the company products portfolio to the current more efficient and more restricted emissions reality implies a huge investment from the automaker. The fact that a lot of the production of passenger cars is automatized decreases personnel costs but it requires considerable upfront investments in machinery and equipment. We believe VW Group will considerably increase this investment in 2016 to recover its late entry in this “green” passenger cars segment, as discussed in the market analysis. With extra investment done in 2016, we expect that VW Group becomes competitive in this growing segment. Thus, we expect the CAPEX and capitalized development costs to stabilize, assuming from 2017 to 2020 a constant CAPEX & Capitalized Development Costs to Sales ratio. From 2020 on, after being done the required

54 VW Group – 2015 Annual Report

Passenger Cars - DCF Valuation

€ million Years ended Dec 31, 2013 2014 2015 2016 E 2017 F 2018 F 2019 F 2020 F 2021 F 2022 F

EBIT 8,538 9,358 (4,851) 8,796 8,464 11,080 10,768 11,187 11,688 12,588 Tax (@29.8%) (2,544) (2,789) 1,446 (2,621) (2,522) (3,302) (3,209) (3,334) (3,483) (3,751) Adjustments & Deferred Tax 554 917 (142) 492 367 435 431 445 449 453

NOPLAT 6,548 7,486 (3,548) 6,666 6,309 8,213 7,990 8,298 8,653 9,290 Depreciation & Amortization 8,212 9,549 10,389 11,101 12,042 12,900 13,690 14,457 15,207 15,965

Impairment Losses 251 274 959 0 0 0 0 0 0 0

Cash Flow from Operating Activities 15,011 17,309 7,801 17,768 18,351 21,113 21,680 22,755 23,861 25,255

CAPEX (excluding capitalized dev. costs)

in Property, Plant & Equipment (8,661) (9,143) (10,201) (12,486) (12,844) (13,153) (13,475) (13,970) (14,489) (15,115) Δ Vehicles Leased Out (1,156) (1,192) (1,352) (1,425) (1,453) (1,472) (1,495) (1,540) (1,587) (1,647) Capitalized Development Costs (3,572) (4,110) (4,626) (4,185) (4,268) (4,325) (4,392) (4,525) (4,663) (4,838) Δ Operating Net Working Capital NA (598) 148 2,754 496 1,656 (57) (196) (273) (322) Δ Other Operating Assets/Liabilities NA 2,373 337 275 129 107 132 160 162 176

Cash Flow from Investing Activities (13,390) (12,670) (15,694) (15,067) (17,940) (17,187) (19,287) (20,071) (20,850) (21,745)

Unlevered Free Cash Flow 1,622 4,639 (7,893) 2,701 410 3,926 2,393 2,684 3,010 3,510

WACC 6.8%

Perpetual Growth rate 3.77%

Operating Enterprise Value 76,329 89,424 92,818 98,733 101,535 106,063 110,607 115,134 119,471 Net Debt 10,640 13,426 13,923 14,810 15,230 15,909 16,591 17,270 17,921

target D/V ratio (Market Values) 13.9% 15.0% 15.0% 15.0% 15.0% 15.0% 15.0% 15.0% 15.0%

Equity (Market Value) 65,690 75,998 78,895 83,923 86,305 90,153 94,016 97,864 101,551

VOLKSWAGEN GROUP COMPANY REPORT

investment for the “e-initiative”, we expect CAPEX to sales ratio to decrease smoothly to 6.9%.

For the terminal value (observable on the “operating enterprise value” row with the “2022 F” column), we have used the following perpetuity formula: TVT =

Unlevered Free Cash Flow T x (1 + g) / (WACC – g), where “g” is the perpetual

growth rate. For this growth rate, we have assumed the forecasted GDP growth rate55, weighted by VW Group’s regional sales (of this specific business unit),

which is 2.01%. In fact, there is empirical evidence that mature industries with a considerable weight on total GDP, such as the automotive industry, have a strong correlation with GDP growth56. Assuming the RONIC57 equal to the WACC and this

2.01% as a sustainable growth rate, we get an implied re-investment rate of 55%58,

which is reasonable when compared to the re-investment rate of 62% in 202259. In

fact, in the long term, a sustainable RONIC has to be the same as WACC. Otherwise, new players will enter in the market until the RONIC lowers to the WACC level. Or to the other way, nobody will invest in this company, because the opportunity cost of capital (WACC) is higher than the investment return. Then, discounting that terminal value until 2017 and summing the additional five annual discounted cash flows we will get on that period, we got an operating enterprise value in 2017 of € 98,733 million.

Commercial Vehicles / Power Engineering

For the short term we expect this business unit to be much less affected by the emission scandal. In fact, the majority of customers of this VW Group’s business segment are companies, which usually have long term relationships and contracts with the stands. Thus, a shift from VW’s brands to others, due to the emissions scandal, would not be so immediate and easy as in the passenger cars. However, VW Group is not as strong on this market segment as in the passenger cars segment. This group has had for the past years a market share for light commercial vehicles always around 2.2%, which we have considered to be maintained in the long-term, after a slight decrease in 2016 of 0.1%, due to the emission scandal. Regarding trucks and buses, VW Group is stronger, having a market share of 6.4% in 2015. Actually, VW group has become the biggest truck producer in Europe after having acquired the brands MAN and Scania. Europe represents 74% of VW Group

55 World Bank

56EU SME Centre 2015. “The Automotive Market in China”.

57 RONIC stands for return on new invested capital and is computed by the formula: NOPLAT / IC, where IC = Invested Capital = Operating Assets –

Operating Liabilities

VOLKSWAGEN GROUP COMPANY REPORT

truck’s sales. Since truck sales are really dependent on manufacturing industries, whom are facing lower growth with the Brexit and low inflation, we have forecasted a smoother sales grow of just 0.5% for 2016, followed by a slow recovery until it achieves 2% sales growth in 2021.

For the power engineering business, based on VW Group’s expectations, we assumed that its small sized sales volume will decrease annually 2.5% until 2019 and then remain constant, reflecting the declining status of this market segment. Based on these assumptions, adding the Euro inflation to the average unit price and multiplying we got the following revenues forecast for this business unit (figure 14).

With this revenue forecast, we have forecasted the income statement of this business unit and built the following DCF model (figure 15).

In this business unit, we expect over the years the same CAPEX & Capitalized Development Costs to Sales ratio as the passenger cars business unit. Also, the change in vehicles leased out depends entirely on the vehicles sold.

For the terminal value (observable on the “operating enterprise value” row with the “2022 F” column), we have used the same formulas as in the passenger cars business unit. For the growth rate, by the same reasons, we have assumed again the GDP growth rate, weighted by VW Group’s regional sales (of this specific business unit), which is 1.97%. Assuming RONIC is equal to the WACC, we get the same implied re-investment rate as the passenger cars: 55%, which is also reasonable when compared to this business unit’s re-investment rate of 49% in 2022.Then, discounting that terminal value until 2017 and summing the additional € million Years ended Dec 31, 2013 2014 2015 2016 E 2017 F 2018 F 2019 F 2020 F 2021 F 2022 F

Trucks & Power Eng. Sales Rev. 23,440 21,863 20,914 21,073 21,535 22,068 22,709 23,395 24,199 25,019

Light Commercial Vehicles Sales Revenue 8,602 8,595 9,057 8,838 9,544 10,418 10,888 11,388 11,825 12,343

Total Business Unit Revenue 32,042 30,458 29,971 29,911 31,079 32,486 33,597 34,782 36,024 37,362

Growth Rate -4.9% -1.6% -0.2% 3.9% 4.5% 3.4% 3.5% 3.6% 3.7%

Commercial Vehicles & Power Engineering - DCF Valuation

€ million Years ended Dec 31, 2013 2014 2015 2016 E 2017 F 2018 F 2019 F 2020 F 2021 F 2022 F

EBIT 1,267 1,421 (1,456) 988 1,028 1,692 1,746 1,879 2,027 2,222 Tax (@29.8%) (378) (424) 434 (294) (306) (504) (520) (560) (604) (662) Adjustments & Deferred Tax (310) (190) (414) 96 64 78 78 81 84 87 NOPLAT 579 807 (1,436) 789 786 1,266 1,303 1,401 1,507 1,647 Depreciation & Amortization 2,487 2,494 2,522 2,675 2,819 2,954 3,081 3,207 3,336 3,469

Impairment Losses 56 57 199 0 0 0 0 0 0 0

Cash Flow from Operating Activities 3,123 3,358 1,284 3,464 3,605 4,220 4,384 4,608 4,842 5,116

CAPEX (excluding capitalized dev. costs)

in Property, Plant & Equipment (1,941) (1,893) (1,986) (2,431) (2,500) (2,560) (2,623) (2,719) (2,820) (2,942) Δ Vehicles Leased Out (259) (247) (263) (263) (273) (285) (295) (305) (316) (328) Capitalized Development Costs (801) (851) (900) (815) (847) (885) (915) (947) (981) (1,018) Δ Operating Net Working Capital NA (226) (2) 399 (188) 72 (159) (74) (60) (15) Δ Other Operating Assets/Liabilities NA 346 (70) (65) 64 90 68 43 44 34

Cash Flow from Investing Activities (3,001) (2,871) (3,221) (3,175) (3,744) (3,568) (3,925) (4,003) (4,134) (4,268)

Unlevered Free Cash Flow 122 487 (1,937) 290 (139) 651 459 605 708 847

WACC 6.8%

Perpetual Growth rate 3.73%

Operating Enterprise Value 17,314 20,431 21,533 23,140 24,065 25,246 26,362 27,450 28,474

Net Debt 2,203 2,614 2,799 3,008 3,129 3,282 3,427 3,569 3,702

target D/V ratio (Market Values) 12.7% 12.8% 13.0% 13.0% 13.0% 13.0% 13.0% 13.0% 13.0%

Equity (Market Value) 15,111 17,817 18,734 20,132 20,937 21,964 22,935 23,882 24,772

Figure 14.

VOLKSWAGEN GROUP COMPANY REPORT

five annual discounted cash flows we got an operating enterprise value in 2017 of € 16,273 million for this business unit.

Financial Services

This division is a complementary division to the automotive division, being responsible to potentiate the automotive division’s sales by financing services. Additionally, this division has been responsible for innovation on the new type of services provided (e.g. Carsharing) and new integrated end-to-end solutions, string growth in emerging markets, where there is a lot of potential for market penetration (e.g. China). The investment in the GT Gettaxi Limited (GETT) is a perfect example of that, which ensures a sustainable growth to this division. To forecast the revenue of this division, since its mission is to potentiate and support financially the sales of the automotive division, we have assumed as a percentage of the number of cars sold by the automotive division. This percentage we have assumed to vary accordingly to the interest rate movements and financing fees changes. For interest rate we have assumed a 0.2% annual increase from 2017 on, assuming these ECB decisions about low interest rates will slowly invert as the European economy grows.For the financial services division, due to its non-operating nature, we have opted for a Cash Flow to Equity model, forecasting the cash flows this division will generate for equity holders in the same time horizon (5 years), computing its terminal value on the 5th year, and discounting those values

at the Cost of Equity (Re). Summing these discounted cash flows to equity, we directly got an equity value of the financial services division for 2017 of negative € 78,737 million. This might seem strange but it makes sense if you consider this division has to keep all the cars leased out in their balance sheet, affecting negatively their cash flow, as you can see in figure 16.

Financial Services - FTE Valuation

€ million Years ended Dec 31, 2013 2014 2015 2016 E 2017 F 2018 F 2019 F 2020 F 2021 F 2022 F

EBIT 1,864 1,916 2,236 2,406 1,526 767 185 (47) (133) 18 Tax (@29.8%) (555) (571) (666) (717) (455) (229) (55) 14 39 (5) Adjustments & Deferred Tax 176 (44) 109 86 92 98 104 110 156 183

NOPLAT 1,485 1,301 1,679 1,775 1,164 637 234 77 63 195

Depreciation & Amortization 3,798 4,521 5,543 6,373 7,862 9,177 10,337 11,388 12,344 13,234

Impairment Losses 39 46 163 0 0 0 0 0 0 0

Cash Flow from Operating Activities 5,321 5,869 7,384 8,147 9,026 9,814 10,571 11,466 12,407 13,430

Δ Property, Plant & Equipment (458) (523) (613) (661) (703) (744) (786) (840) (896) (961) Δ Vehicles Leased Out (10,508) (12,659) (16,665) (17,409) (17,591) (17,645) (17,672) (17,912) (18,142) (18,506) Δ Accounts Receivables NA (13,423) (9,040) (9,211) (8,205) (7,879) (8,184) (10,366) (10,936) (12,541) Δ Accounts Payables NA 256 61 138 123 118 123 156 164 188 Δ Ongoing Operating Provisions NA 891 (89) 645 233 522 257 440 483 604 Δ Other Operating Assets/Liabilities NA 465 (1,227) (186) (251) (235) (246) (333) (354) (418)

Cash Flow from Investing Activities (10,966) (24,993) (27,574) (26,684) (26,394) (25,863) (26,508) (28,856) (29,681) (31,634)

Unlevered Operating Free Cash Flow (5,645) (19,124) (20,190) (18,537) (17,368) (16,049) (15,937) (17,390) (17,274) (18,205)

Δ other non-operating assets/liabilities NA 1,223 5,450 (1,442) 109 (136) (124) (129) (173) (193)

Total Unlevered Free Cash Flow (5,645) (17,901) (14,740) (19,979) (17,259) (16,185) (16,061) (17,519) (17,447) (18,398) target D/V ratio (Book Values) 88.6% 87.7% 86.9% 88.0% 88.0% 88.0% 88.0% 88.0% 88.0% 88.0%

Net Debt 109,027 124,395 138,623 160,084 176,256 190,834 204,971 220,249 235,375 251,421 Δ Net Debt NA 15,368 14,228 21,460 16,173 14,578 14,137 15,278 15,126 16,046 Interests 130 (169) (110) (125) (138) (149) (160) (172) (183) (196)

Tax Shields (39) 50 33 37 41 44 48 51 55 58

Free Cash Flow to Equity (5,554) (2,651) (589) 1,393 (1,183) (1,711) (2,037) (2,362) (2,450) (2,489)

Cost of Capital for Equity (Re) 7.5%

Perpetual Growth rate 3.76%

Equity Value (78,737) (77,146) (75,252) (73,056) (70,778) (68,463)

VOLKSWAGEN GROUP COMPANY REPORT

The main drivers for this negative value for the financial services division are the changes in vehicles leased out and in accounts receivables, which are expectable due to the non-operating and complementary nature of this division. For the terminal value wew have used the same formual as in the automotive division and we have assumed for the growth rate an average of the growth rates assumed in the automotive division, weighted with the business units’ specific equity value.

Equity-Accounted Investments

Regarding the equity investments on the 4 joint-ventures and 5 associates, we have opted for different valuing approaches in each one, depending on their investment size and on how much of their financial data is publicly available. Starting by the joint-ventures, these were the approaches chosen:

Joint-venture Method used

FAW-Volkswagen Automotive Company Simplified DCF model SAIC-Volkswagen Automotive Company Simplified DCF model SAIC-Volkswagen Sales Company Simplified DCF model

Global Mobility Holding Estimated Fair value (using as reference the sale price of LeasePlan shares)

Looking deeper into the three first joint-ventures, which are the most significant, we can see by their few financial data publicly available that practically none of them have debt. Also, all of them are located in China (Changchun and Shanghai) and have the same business activity: develop, produce and sell passenger cars. To compute a specific WACC for these Chinese joint-ventures we have a considered a country specific risk premium of 2.55%60, which was added

to the market risk premium of 6.16%61 (used also for VW Group’s WACC

estimation) to reflect a specific adjusted market risk premium for China. For the risk free rate, it was considered the European risk-free rate of 0.33%62 (used also

for VW Group’s WACC estimation). Then, we have used an average unlevered beta for large caps in the automotive industry in China of 0.8463, which we consider

to be comparable to these three companies. To be able to use this beta in the CAPM model we had to lever it, using again the formula: BU = BL / [1 + (1- Tc) x

(D/E)]64. Applying the CAPM model (already shown before) we got the cost of

equity, which was used as input in the WACC formula (already shown before) to get a final cost of capital for these 3 Chinese joint-ventures of 7.6% (figure 17). Note that the fact that the tax rate is different in each of the 3 companies does not

60 Damodaran, Aswath. "Country Default Spreads and Risk Premiums." New York University Stern School of Business, July 2016. Web. 04 Jan. 2017. 61 Damodaran, Aswath. "Damodaran Online" New York University Stern School of Business, Jan. 2017. Web. 04 Jan. 2017.

62 10-year AAA-rated Euro area central government bonds 63 WACC Expert Index

64being “Tc” the marginal tax rate (28.9%), “D/E” the Debt to Equity ratio, and “BU” and “BL” the unlevered and levered beta, respectively.

D/V 0.0%

Cost of Debt 0.0%

Country Risk Premium 2.6%

Risk-free rate 0.3%

Unlevered Beta 0.84

Market Premium 6.2%

Long-Term WACC 7.6%

VOLKSWAGEN GROUP COMPANY REPORT

produce any effect on their WACC computations, because they do not have any debt.

Looking for the sales of these joint ventures, we can see the Chinese economy slow-down effect: their annual sales growth rate decreased from 12% in 2014 to -1.4% in 2015, representing the initial reaction to this new economic scenario. We forecast on the short-term (for 2016) a sales growth recovery, to correct what we consider an over-reaction in 2015 allied with a higher demand for luxury cars (specially Audi). On the long term, we forecast a stable 4% annual growth rate in vehicles sold, as targeted by the country’s planners65, after the

Chinese automotive industry having adjusted to this new and long-term economic scenario. Through a product development strategy (explained already in the market analysis), starting to sell “greener” cars in this market, we expect these joint ventures to be able to sustainably maintain their market share in China. This annual growth rate from 2017 on seems to be reasonable when compared to the 5.4% average GDP real growth rate for China66. Actually, we expect the automotive

industry to continue to expand in the Chinese economy, but slightly decreasing its weight on GDP. In 2014, by each 1,000 Chinese people there was just 105 cars, which is lower than the global average of 140 cars67. So the penetration rate is low,

but there are high barriers to increase that, such as the low purchasing power of the population and incentives from the government to use public transportation instead. This sales growth is also backed by the recovered economic growth of China, which is supporting a growing demand for luxury passenger cars (such as Audi and Bentley). To answer to the market specific needs, VW Group has specific models for China, using as base others already developed models. The Audi A6L is the classic example where VW Group takes the European model A6 as base and modifies it to meet Chinese market demands (in this case it stretches the car and includes additional luxurious features). There is also a growing demand in China for electric cars, which VW Group is fulfilling by its “e-mobility” initiative. These actions are supported by the valuable partnerships (associates & joint ventures) in China, which help to tailor the imported models according to the Chinese market and to produce locally some specific models for this market.

Finally, using the inflation rate forecast of IMF for Euro, we got the total revenue forecast for the three joint ventures present in figure 18.

65 Schmitt, Bertel. "China To Automakers: 'Make EVs, Or Die'" Forbes. Forbes Magazine, 25 Nov. 2016. Web. 04 Jan. 2017. 66 World Bank (estimates from 2017 to 2022).

67EU SME Centre 2015. “The Automotive Market in China”.

FAW + SAIC VW Automotive & Sales Companies (1 + 2 + 3)

€ million Years ended Dec 31, 2013 2014 2015 2016 E 2017 F 2018 F 2019 F 2020 F 2021 F 2022 F

Vehicles Sold (thousands) 3,135 3,506 3,456 3,773 3,924 4,081 4,244 4,414 4,590 4,792

Growth Rate 11.8% -1.4% 9.2% 4.0% 4.0% 4.0% 4.0% 4.2% 4.4%

Average Unit Price (€) 26,245 26,501 27,927 27,999 28,373 28,825 29,309 29,825 30,373 30,908 Euro Inflation Rate 1.5% 0.5% 0.0% 0.3% 1.3% 1.6% 1.7% 1.8% 1.8% 1.8% Revenue 82,279 92,913 96,515 105,641 111,334 117,631 124,389 131,645 139,426 148,122