THIS

DOCUMENT

IS

NOT

AN

INVESTMENT

RECOMMENDATION

AND

SHALL

BE

USED

EXCLUSIVELY

FOR

ACADEMIC

PURPOSES

(SEE DISCLOSURES AND DISCLAIMERS AT END OF DOCUMENT)See more information at WWW.NOVASBE.PT Page 1/39

MASTERS IN FINANCE

E

QUITY

R

ESEARCH

Engineering and Construction: has a backlog of €3,3 bn, or roughly two years of revenues, with E&C representing 85% of this value. International activity will be the driver of future growth. Environment and Services: is expected to present interesting margins despite modest growth in revenues. Internationalization reinforced with Geo Vision.

Ascendi: Concessions theoretically with no risk, as they are run under the availability of network system, and therefore not depending on traffic. However, amendments to the contracts are expected in March 2012.

Martifer: increasing pressure on metallic constructions business with declining revenues and negative EBITDA margins. Solar is expected to drive Martifer’s growth for the next years, despite the increasing uncertainty affecting the renewables sector. Additionally, asset sales are expected to enable significant net debt reductions.

Asset’s sale: Mota has 200M€ in assets for sale, which will considerably impact the price target.

Sector’s consolidation: even if the company has denied its intention to participate.

Company description

Mota-Engil SGPS SA is a Portuguese company operating in three major business areas: Engineering and Construction (E&C), Environment and Services (E&S) and Transport Concessions. It carries on its business in 19 countries through branches and subsidiaries around the world. Among the most important markets are Portugal, Poland, Angola, Mozambique, Peru and Mexico.

M

OTA

-E

NGIL

C

OMPANY

R

EPORT

C

ONSTRUCTION

06

J

ANUARY2012

D

UARTE

M

ORAIS

S

ANTOS

[email protected]

Asset’s sale...

...a big question mark!

Recommendation: Buy

Price Target FY12: 1.57 €

Price (as of 6-Jan-12) 1.04 €

Reuters: MOTA.LS, Bloomberg: EGL:PL

52-week range (€) 0.99-2.09

Market Cap (€m) 200.422

Outstanding Shares (m) 193.600

Source: Bloomberg and NOVA SBE Equity Research Team

Source: Bloomberg

(Values in € millions) 2010 2011E 2012F

Revenues 2.005 2.088 2.120

EBITDA 237,3 267,8 269,2

EBITDA margin 11,8% 12,8% 12,7%

Net Profit 37,0 31,5 19,3

EPS 0,19 0,16 0,10

P/E 5,7

Net Debt/EBITDA(1)

4,3 3,8 3,8

Source: Mota-Engil and NOVA SBE Equity Research Team (1) Excluding Ascendi’s debt.

-15 5 25 45 65 85 105 125

03-01-2008 03-01-2009 03-01-2010 03-01-2011 Historical Share Price Performance

MOTA-ENGIL COMPANY REPORT

THIS

DOCUMENT

IS

NOT

AN

INVESTMENT

RECOMMENDATION

AND

SHALL

BE

USED

EXCLUSIVELY

FOR

ACADEMIC

PURPOSES

(SEE DISCLOSURES AND DISCLAIMERS AT END OF DOCUMENT)PAGE 2/39

Table of Contents

COMPANY OVERVIEW ... 4

THE SECTOR ... 5

OVERVIEW... 5

COMPARABLES ... 7

VALUATION ...10

GLOBAL METHODOLOGY ... 10

MULTIPLES VALUATION... 12

ENGINEERING AND CONSTRUCTION ... 13

Iberia ... 13

Africa ... 14

America ... 14

Central Europe ... 15

Total Backlog ... 16

Conclusion ... 16

ENVIRONMENT AND SERVICES ... 17

Waste ... 18

Water ... 18

Logistics ... 19

Multi-services ... 20

Backlog ... 20

Conclusion ... 20

MARTIFER ... 21

Metallic Constructions... 21

Solar ... 22

Conclusion ... 24

Total Backlog ... 25

ASCENDI ... 25

Valuation ... 26

DEBT POSITION ...27

IS MOTA-ENGIL REALLY CREATING VALUE? ...29

M&A SCENARIO ...30

METHODOLOGY... 31

OPWAY ... 32

EDIFER ... 32

SYNERGIES ... 33

APPENDIX ...35

1) FCF CALCULATION – THE END OF THE EUROZONE ... 35

2) PROBABILITIES OF DEFAULT ACCORDING TO RATING ... 37

DISCLOSURES AND DISCLAIMER ...39

MOTA-ENGIL COMPANY REPORT

THIS

DOCUMENT

IS

NOT

AN

INVESTMENT

RECOMMENDATION

AND

SHALL

BE

USED

EXCLUSIVELY

FOR

ACADEMIC

PURPOSES

(SEE DISCLOSURES AND DISCLAIMERS AT END OF DOCUMENT)PAGE 3/39

Investment Considerations

We are rating Mota-Engil BUY with a price target of 1,57€, despite some important risks to our valuation:

1) Rising interest rates.

Mitigation: we have considered a significant increase in interest rates paid,

namely from 5% in 2010 to 8,9% in 2013. We then expect them to decrease to 7,9% by 2016, as the credit markets unfrozen.

2) Failure in assuming the €200 mn.

Mitigation: in our analysis we have considered that the company will only be

able to sell 35% of the €200 mn, with impairment losses amounting to 10%. A sensitivity analysis to the price target was conducted in table 14.

3) Not being able to rollover short term debt.

Mitigation: The company can always sell either or both Ascendi’s and

Martifer’s positions. This would give the company a value of nearly 223M€, representing 43% of 2010’s short term debt.

4) Portugal entering in bankruptcy and exiting the Eurozone.

Mitigation. We tried to mitigate such risk by decreasing Mota-Engil’s FCF. We

did it by introducing additional scenarios (for further details see appendix 1). 5) Amendments to Mota’s concessions contracts.

Mitigation: We have mitigated this risk by not considering the concessions Douro Interior and Pinhal interior in our valuation, and by valuing Copexa and Marechal Rondon Leste only through invested capital. Additionally, when calculating the value under the availability of network system, we have introduced the probability of changes in the contracts previously signed (besides Ascendi’s default probability).

6) Angolan recession. Angola is completely dependent on oil prices. Given the current situation in Europe, some retraction in consumption and, consequently in oil prices, is possible.

Mitigation: We have mitigated this risk with conservative revenues growth forecasts for the country, with a CAGR of 5,4%, from 2010 to 2016.

7) Working capital position.

Mitigation: We have considered a CAGR of 4,3% for the period between 2011

MOTA-ENGIL COMPANY REPORT

THIS

DOCUMENT

IS

NOT

AN

INVESTMENT

RECOMMENDATION

AND

SHALL

BE

USED

EXCLUSIVELY

FOR

ACADEMIC

PURPOSES

(SEE DISCLOSURES AND DISCLAIMERS AT END OF DOCUMENT)PAGE 4/39 64%

5% 2% 2% 2%

25%

Figure 2 - Mota-Engil's Shareholder structure

Mota Family

Privado Holding

NMAS Asset Management

QMC Development Capital

Morgan Stanley

Other

30th largest European construction company in 2010…

Source: Bloomberg and NOVA SBE Equity Research Team

Company Overview

Mota-Engil has been the largest Portuguese civil and public construction contractor for the last decade. According to Bloomberg data, it was the 30th largest European construction group in 2010 when considering total revenues. The group history started in 2000 with the merger between Mota and Engil. However, the know-how accumulated goes well beyond that until 1946 when Mota was originally created. By 1952 Mota was awarded with the construction of Luanda’s International Airport, initiating its internationalization process.

Diversification and internationalization have been a major concern of Mota-Engil due to its declining domestic construction market. The company has taken an astute option and expanded into other business areas, namely waste and water management, logistics, and concessions through a 60% participation in Ascendi. Mota-Engil is also present in the metallic construction and renewable energies markets, through a 37,5% stake in Martifer SGPS. Mota-engil is, nowadays, a true international group, with its structure divided in 3 major areas: Engineering and Construction (E&C), Environment and Services (E&S) and Investments. Figure 1 – Mota-Engil’s Corporate Structure

Source: Mota-Engil; NOVA SBE Equity Research Team

Shareholders’ structure is composed mainly by Mota family (see figure 2), which can be seen as positive for the day to day activity of the company, as it provides considerable stability. On the other side, however, it poses a true threat to small investors, since management may be taking actions in the interest of only a group of shareholders, eventually driven by non-economical reasons. Moreover, it is likely to be an obstacle to capital increases, as the Mota family may be limited in terms of capital and unwilling to dilute their current position. Hostile takeovers are also much less probable, due to difficulties in gaining major shareholder approval.

Mota-Engil

Engineering & Construction

Infrastructure Building Real

Estate Others

Environment & Services

Waste Water Logistics Multi-services

Investments

MOTA-ENGIL COMPANY REPORT

THIS

DOCUMENT

IS

NOT

AN

INVESTMENT

RECOMMENDATION

AND

SHALL

BE

USED

EXCLUSIVELY

FOR

ACADEMIC

PURPOSES

(SEE DISCLOSURES AND DISCLAIMERS AT END OF DOCUMENT)PAGE 5/39

The Sector

Overview

Triggered by the Sovereign debt crisis in Greece, Europe and particularly Portugal are now facing demanding restructuring plans, with severe consequences for the construction sector. Recent estimations are pointing towards a recession between 2,5% and 3% in Portugal, according to the Portuguese government and the European Union, respectively.

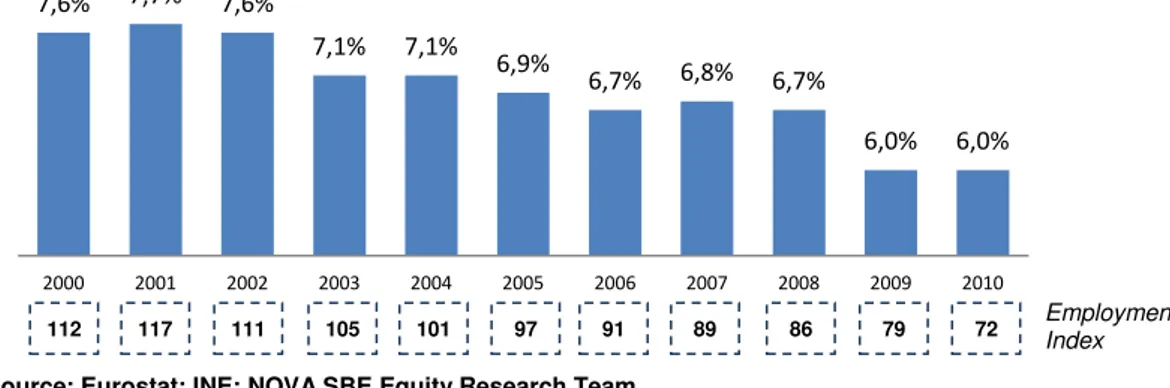

In figure 3 we make a comparison of the gross value added by construction activity among several countries in Europe. Portugal seems to be in line with other European economies. However, in figure 4 we can also conclude that Portuguese evolution in the last decade as been consistently negative, both in terms of value added and employment, gradually decreasing its weight in the Portuguese economy.

Figure 4 – Portuguese Gross Value Added evolution; Employment index (base 100; July 2005)

Source: Eurostat; INE; NOVA SBE Equity Research Team

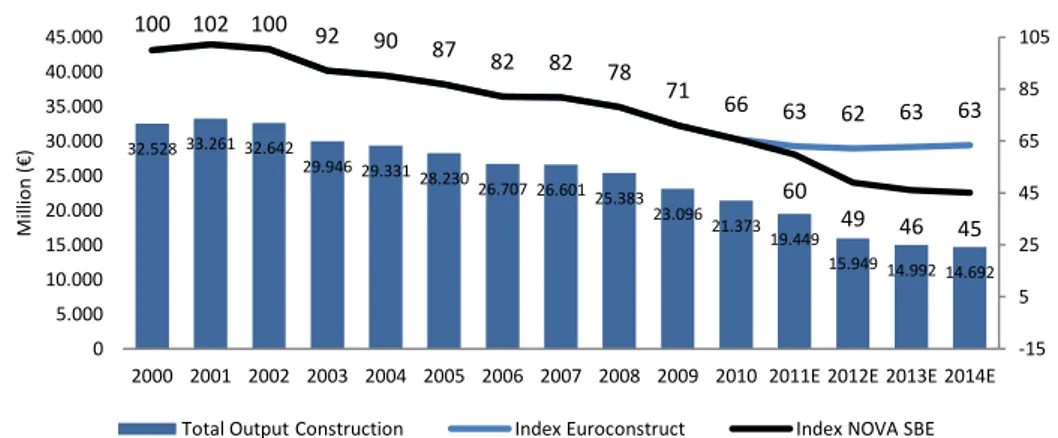

According to Eurocontruct1, the residential new housing market is expected to

continue its decline until 2013. Renovation works will experience a smaller decline, with recovery starting one year sooner – 2012. However we expect a significantly higher decrease given the current reality in the 3rd Q 2011 and a recent forecast of a lower GDP and Public investment, factors that were not included in Euroconstruct’s projections. In figure 5 we compare both expectations.

1Euroconstruct, 2010. 70th Euroconstruct Country Book, European Construction: Market trends until 2013. Budapeste, 2-3 December 2010.

7,6% 7,7% 7,6%

7,1% 7,1%

6,9%

6,7% 6,8% 6,7%

6,0% 6,0%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

4,0% 4,2% 4,8%

5,3% 5,5% 5,9% 6,0% 6,1% 6,4% 6,6% 7,0% 7,1%

9,0% 10,2%

Hungary Germany Norway Belgium Sweden Italy Portugal United Kingdom France Finland Czech Republic Poland Slovakia Spain

Figure 3 - Gross Value Added Contruction (2010)

Decreasing weight of construction on GDP…

Sovereign debt crisis pressuring construction companies…

112 117 111 105 101 97 91 89 86 79 72 Employment

Index

MOTA-ENGIL COMPANY REPORT

THIS

DOCUMENT

IS

NOT

AN

INVESTMENT

RECOMMENDATION

AND

SHALL

BE

USED

EXCLUSIVELY

FOR

ACADEMIC

PURPOSES

(SEE DISCLOSURES AND DISCLAIMERS AT END OF DOCUMENT)PAGE 6/39 Figure 5 – Total Construction Output (base 2000)2

Source: Euroconstruct and NOVA SBE Equity Research Team

According to INE, the total number of concluded residential new buildings declined 8,8% in 2010, while non-residential new buildings declined by 7% (figure 6). When considering renovation works, the decline is much smaller – only 2,4%. To what 2011 is concerned, until October the total decrease was 7,4%, already in line with our forecast of an accumulated 9% decrease for total 2011.

To what new permits for new housing is concerned, 2011 is witnessing a 16,7% decline, leading to an accumulated decline since 2008 of 45%. The decline is considerably larger for residential construction, as can be seen in figure 7.

Several reasons contribute to this decreasing tendency in the sector. The number of inhabitants per dwelling decreased over the last years from 2,1 in 1999 to 1,9 in 2010, among the lowest values in Europe (figure 9).

Figure 9 – Number of inhabitants per dwelling (2010)

Source: European Mortgage Federation and NOVA SBE Equity Research Team.

To what residential debt is concerned (figure 10) we can see that Portuguese families are among the most indebted in Europe.

2Euroconstruct’s projections did not include the recent events

such as a decline in GDP projections or in public investment forecasts. For the year 2011 we have already included the values until October in our analysis. 2012 was computed considering a 9,5% reduction in Public and Private investment, according to the public budget proposal of 2012. Notwithstanding, growth is expected in 2015.

32.528 33.261 32.642

29.946 29.331 28.230

26.707 26.601 25.383 23.096

21.373 19.449

15.949 14.992 14.692

100 102 100 92 90 87

82 82 78 71

66 63 62 63 63

60

49 46 45

-15 5 25 45 65 85 105 0 5.000 10.000 15.000 20.000 25.000 30.000 35.000 40.000 45.000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011E 2012E 2013E 2014E

M ill io n ( € )

Total Output Construction Index Euroconstruct Index NOVA SBE

1,7 1,8 1,8 1,9 1,9 2,0 2,0 2,0 2,1 2,1 2,2 2,2

2,3 2,3 2,3 2,5 2,6 2,7 2,8

Lost decade for the Portuguese construction market… 29 26 22 20 5 5 5 4

2007 2008 2009 2010

Figure 6 - Concluded new construction (thousands) Residential Non-residential CAGR=-10,4% 24 16 15 12 6 5 4 4

2008 2009 2010 2011

Figure 7 - New construction permits (thousands)

Residential Non-residential

CAGR=-18,2%

6 5 5 5

5

5

4 4

2008 2009 2010 2011

Figure 8 - Renovation permits (thousands)

Residential Non-residential

CAGR=-6,8%

Source: INE and NOVA SBE Equity Research Team

Source: INE and NOVA SBE Equity Research Team

MOTA-ENGIL COMPANY REPORT

THIS

DOCUMENT

IS

NOT

AN

INVESTMENT

RECOMMENDATION

AND

SHALL

BE

USED

EXCLUSIVELY

FOR

ACADEMIC

PURPOSES

(SEE DISCLOSURES AND DISCLAIMERS AT END OF DOCUMENT)PAGE 7/39

The number of bankruptcies has been increasing over the last months. This year several major players in the Portuguese market filed in for bankruptcy3. According to AECOPS4 the number of bankruptcies until September 2011 was 1446, a number much higher than the total number for 2010 – 970 companies. As a consequence, banks overdue credit conceded to Portuguese construction companies has reached astonishing values. According to Banco de Portugal, the ratio of overdue debt in the construction sector increased from 2% in December 2006 to 10,5% of total credit conceded in September 2011 – Figure 11. This corresponds to an increase from €457mn in December 2006 to €2.552mn in September 20115.

In terms of public works, it is relevant to notice that major investments were dropped. Tagus Bridge, the new international airport of Lisbon, the high speed train and several other infrastructure plans have been postponed. Also, when observing the motorway extension in Portugal we can conclude that Portugal is among the countries with more km of motorways (figure 12).

Conclusion: Euroconstruct’s forecasts did not include important variables that were recently disclosed. Given current family’s indebtedness levels, as well as lending restrictions being imposed and the delay in public works, we expect a higher and more prolonged decline in total production (see figure 5).

Comparables

The industry in Portugal is characterized by three major players – Mota-Engil, Teixeira Duarte and Soares da Costa - and a reasonable number of other considerably big construtors – Somague, Lena, Opway, Edifer, Monte Adriano, MSF, FDO and DST. The three major players together represented only 9,4% of the market in 20106.

Teixeira Duarte is the most diversified of the three major players. Besides construction, they develop activity in several other areas: concessions, logistics, Energy, Automobiles and own several financial participations, namely in Millennium BCP and BBVA. Soares da Costa, on the contrary, is the least diversified company. Nevertheless, it does business in non-construction areas such as concessions (road, water and waste) and environment and energy through SelfEnergy.

3 This was, for instance, what happened with NOVOPCA, a construction company with more than 60 year of activity, or Mesquita with more than 50

years of emblematic works.

4 Engenharia Portugal, 2011. Falências de mais de 1400 construtoras em 2011. [online] Available at: <

http://www.engenhariaportugal.com/falencia-de-mais-de-1400-construtoras-em-2011> [accessed September 2011].

5 Banco de Portugal, Ocotber 2011, Boletim Estatístico. 6 Based on financial reports and Euroconstruct data

2,0% 2,0% 3,3% 5,6% 7,2% 10,5% 0,0% 2,0% 4,0% 6,0% 8,0% 10,0% 12,0%

2006 2007 2008 2009 2010 2011 Figure 11 - Bad debt levels

Source: Banco de Portugal and NOVA SBE Equity Research Team

13.515 12.645 11.042 6.629 3.673 2693 2.637 1.922 1.855 1.763 1.696 1.383 1.128 765 696 423 418 253 Spain Germany France Italy UK Portugal Netherlands Turkey Sweden Belgium Austria Switzerland Denmark Poland Slovenia Ireland Bulgaria Norway

Figure 12 - Motorway km's (2008)

Source: Eurostat and NOVA SBE Equity Research Team 249% 178% 147% 145% 129% 122% 90% 89% 84% 79% 66% 47% 44% Netherla… Norway Sweden UK Portugal Spain Austria Germany Belgium France Italy Slovenia Lithuania

Figure 10 - Families' total debt / disposable income

MOTA-ENGIL COMPANY REPORT

THIS

DOCUMENT

IS

NOT

AN

INVESTMENT

RECOMMENDATION

AND

SHALL

BE

USED

EXCLUSIVELY

FOR

ACADEMIC

PURPOSES

(SEE DISCLOSURES AND DISCLAIMERS AT END OF DOCUMENT)PAGE 8/39

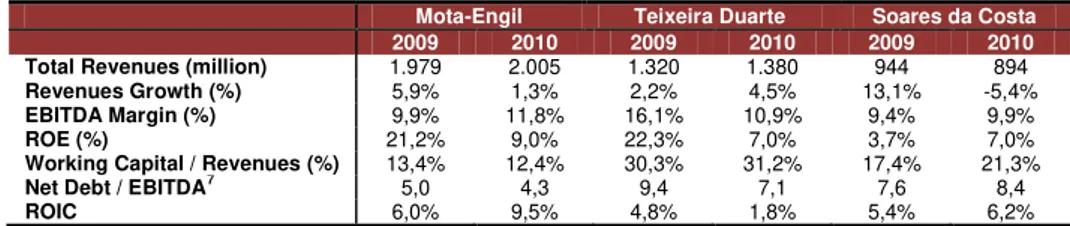

Table 1 allows for a comparison between the three companies in terms of several of the major and most relevant ratios for 2009 and 2010:

Table 1 – Comparison between major portuguese construction companies

Mota-Engil Teixeira Duarte Soares da Costa

2009 2010 2009 2010 2009 2010

Total Revenues (million) 1.979 2.005 1.320 1.380 944 894

Revenues Growth (%) 5,9% 1,3% 2,2% 4,5% 13,1% -5,4%

EBITDA Margin (%) 9,9% 11,8% 16,1% 10,9% 9,4% 9,9%

ROE (%) 21,2% 9,0% 22,3% 7,0% 3,7% 7,0%

Working Capital / Revenues (%) 13,4% 12,4% 30,3% 31,2% 17,4% 21,3%

Net Debt / EBITDA7 5,0 4,3 9,4 7,1 7,6 8,4

ROIC 6,0% 9,5% 4,8% 1,8% 5,4% 6,2%

Source: Companies’ Financial reports

Mota-Engil is clearly the biggest and most deleveraged of the three. Teixeira Duarte, despite interesting margins, has a significantly high NWC, due to increasing inventory levels (almost €400mn). The majority of its EBITDA is generated by construction and Real Estate activities. Both Mota-Engil and Teixeira Duarte present very good ROEs in 2009, with Soares da Costa presenting the lowest of the three, as well as negative revenues growth in 2010. This two facts are justified by the considerable decrease in national activity faced by the company (-15,5%). In terms of value creation, Mota-Engil seems the most consistent of the three and the only actually creating value in 20108.

In terms of diversification and internationalization, when compared to major European players, portuguese companies seem to be on average, resorting to both criteria.

Figure 13 – Internationalization vs. Diversification

Source: European Powers of Construction and Companies’ Financial Reports

7Without onsidering Ascendi’s debt.

8 Based on Mota-Engil’s average WACC of 7,5%.

Mota-Engil Teixeira Duarte Soares da Costa

Vinci

Bouygues Hochtief

ACS

Eiffage Skanska

Strabag

Balfour Beatty

Ferrovial

FCC

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

0% 10% 20% 30% 40% 50% 60% 70%

Int

e

rna

ti

o

na

l

R

e

v

e

nu

e

s

Non-Construction Revenues Mota-Engil, better than

Portuguese competition…

MOTA-ENGIL COMPANY REPORT

THIS

DOCUMENT

IS

NOT

AN

INVESTMENT

RECOMMENDATION

AND

SHALL

BE

USED

EXCLUSIVELY

FOR

ACADEMIC

PURPOSES

(SEE DISCLOSURES AND DISCLAIMERS AT END OF DOCUMENT)PAGE 9/39

Looking at the major construction companies in Europe and to Odebrecht is an interesting exercise to assess the Portuguese companies and their financial ratios. Table 2 shows our findings.

Table 2 – Comparison between Mota and international construction groups

2010

Mota-Engil

ACS Ferrovial Vinci Eiffage Hochtief Odebrecht Average

Total Revenues (million) 2.005 15.380 12.169 33.376 13.553 20.159 24.7809

Revenues Growth (%) 1,3% 0% -0,1% 8,6% 0,7% 11% 32,9% 8,9%

EBITDA Margin (%) 11,8% 9,8% 20,7% 10,1% 13,8% 6,9% 11,6% 12,2%

ROE (%) 9,0% 32,5% 27,4% 9% 9,3% 12,8% 31% 20,3%

Net Debt / EBITDA 4,3 5,3 8,1 4,1 6,9 0,6

Rating (S&P) - - BBB- BBB+ - - -

Source: Companies’ Financial reports

Mota-Engil is still very small compared to major European players. This fact constitutes a major obstacle to all Portuguese companies in the international markets, since they may not be able to compete for bigger projects. In terms of revenues growth, all the companies considered exhibited small changes in 2010, with the exception of Hochtief and Odebrecht. Hochtief revenues increase was driven by their presence in emerging markets, while Odebrecht’s were the result of being one of the major players in Brazil, a fast growing economy. To what the EBITDA margin is concerned, it is pretty much in line with the average. Ferrovial’s EBITDA margin is a result of the increase of airports business, fully consolidated in 2010, presenting above average margins. In terms of net debt to EBITDA, Mota-Engil is in line with average values, even when considering Ascendi’s debt. Ferrovial’s debt level is a consequence mainly of the €10.3 bn deal to acquire BAA.

9 Based on revenues of 32.325 million USD converted at an exchange rate of 1,3045.

MOTA-ENGIL COMPANY REPORT

THIS

DOCUMENT

IS

NOT

AN

INVESTMENT

RECOMMENDATION

AND

SHALL

BE

USED

EXCLUSIVELY

FOR

ACADEMIC

PURPOSES

(SEE DISCLOSURES AND DISCLAIMERS AT END OF DOCUMENT)PAGE 10/39

Valuation

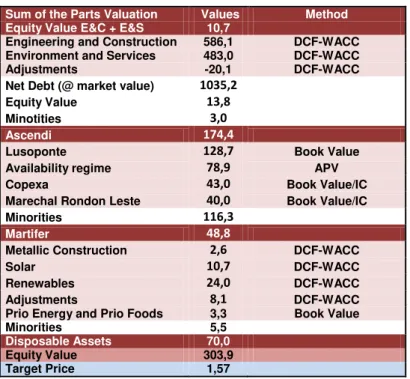

We valued Mota-Engil using a sum-of-the-parts approach. Table 3 summarizes each valuation and the respective method used.

Table 3 – Sum of the Parts Valuation

Sum of the Parts Valuation Values Method Equity Value E&C + E&S 10,7 Engineering and Construction 586,1 DCF-WACC Environment and Services 483,0 DCF-WACC

Adjustments -20,1 DCF-WACC

Net Debt (@ market value) 1035,2

Equity Value 13,8

Minotities 3,0

Ascendi 174,4

Lusoponte 128,7 Book Value

Availability regime 78,9 APV

Copexa 43,0 Book Value/IC

Marechal Rondon Leste 40,0 Book Value/IC

Minorities 116,3

Martifer 48,8

Metallic Construction 2,6 DCF-WACC

Solar 10,7 DCF-WACC

Renewables 24,0 DCF-WACC

Adjustments 8,1 DCF-WACC

Prio Energy and Prio Foods 3,3 Book Value

Minorities 5,5

Disposable Assets 70,0

Equity Value 303,9

Target Price 1,57

Source: Mota-Engil and NOVA SBE Equity Research Team

Global Methodology

The value found in each DCF valuation was obtained considering a terminal value in accordance with the expected sustainable growth rate for emerging markets and mature markets. To calculate the potential growth rate we have considered both the reinvestment rate and the return on invested capital10

. Then, assuming

that Mota-Engil will not be able to sustain its competitive advantage as opportunities are exhausted in existing geographies, we assumed a nominal growth of 2,5% for the E&C unit. For E&S we assumed 3% as it still offers interesting opportunities of expansion into emerging markets11. For the risk freewe have assumed a 12 month average of the 10 year German Bunds.

10 Sustainable Growth Rate = , where:

ROIC = Reivestment Rate =

MOTA-ENGIL COMPANY REPORT

THIS

DOCUMENT

IS

NOT

AN

INVESTMENT

RECOMMENDATION

AND

SHALL

BE

USED

EXCLUSIVELY

FOR

ACADEMIC

PURPOSES

(SEE DISCLOSURES AND DISCLAIMERS AT END OF DOCUMENT)PAGE 11/39

To what the calculation of betas is concerned, we have resorted to bottom-up betas (unadjusted regression betas from comparable companies)12. We then delevered them13, and computed an average unlevered beta for the industry, leveraging it again using the company’s target capital structure. This was usually obtained by applying the debt structure forecasted for 2014 and was calculated using market prices both for equity and debt (when possible)14.

In order to obtain an adjusted equity premium that would correspond to the systematic risk of each country we have considered a country Beta15 instead of a country risk premium (as we include diversifiable risks in the FCF calculation16). To calculate it we resorted to the relative volatility of the country index to the S&P and considered a correlation of 1, since in economic recessions correlations tend to increase17. Then we resorted to the standard CAPM equation, adjusted to the country Beta18.

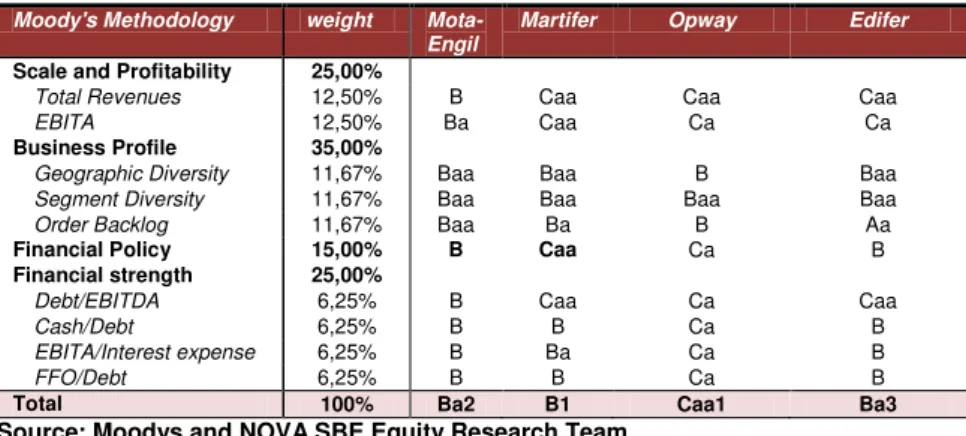

Since Mota-Engil is not rated, we applied a synthetic rating to find a suitable cost of debt for each company/segment using Moody’s methodology for global construction companies19. Table 4 summarizes our computations.

Table 4 – Rating scores and correspondent overall rating (Moody’s)

Moody's Methodology weight Mota-Engil

Martifer Opway Edifer

Scale and Profitability 25,00%

Total Revenues 12,50% B Caa Caa Caa

EBITA 12,50% Ba Caa Ca Ca

Business Profile 35,00%

Geographic Diversity 11,67% Baa Baa B Baa Segment Diversity 11,67% Baa Baa Baa Baa

Order Backlog 11,67% Baa Ba B Aa

Financial Policy 15,00% B Caa Ca B

Financial strength 25,00%

Debt/EBITDA 6,25% B Caa Ca Caa

Cash/Debt 6,25% B B Ca B

EBITA/Interest expense 6,25% B Ba Ca B

FFO/Debt 6,25% B B Ca B

Total 100% Ba2 B1 Caa1 Ba3

Source: Moodys and NOVA SBE Equity Research Team

Afterwards, we have looked for companies with the same rating20 and computed an average yield to maturity. By comparing other Portuguese rated companies to

12 For E&C we have considered NCC, BAM, YIT Group, Hochtief, Strabag and Skanska. E&S: Suez Environnement, Veolia Environnement, Acque

Potabili, Pennon and Severn Trent. Ascendi: Brisa, Abertis, Atlantia and Societe des Autoroutes. Martifer Metallic Constructions: Ruukki, Pomimex-Mostostal and Lindab International. Martifer Solar: several companies from the Bloomberg solar index.

13β unlevered =

14 Debt Market Value =

, where n stands for debt’s average maturity

15β

country =

16 See exhibit 1

17

Elaine Jones, 2009. Recession and International Market Correlations. University of Central Missouri, Warrensburg, Missouri, US

18Rlevered equity = Risk Free + β levered*βcountry* Market Premium

MOTA-ENGIL COMPANY REPORT

THIS

DOCUMENT

IS

NOT

AN

INVESTMENT

RECOMMENDATION

AND

SHALL

BE

USED

EXCLUSIVELY

FOR

ACADEMIC

PURPOSES

(SEE DISCLOSURES AND DISCLAIMERS AT END OF DOCUMENT)PAGE 12/39

the average yield of their specific rating we concluded that investors are demanding a premium to hold Portuguese debt21. Bearing in mind that the cost of debt will be the expected return22, we have considered a probability of default for each company (see appendix 2)23. Under the default case debt holders would receive only a recovery rate, calculated resorting to the following criteria: (1) Goodwill and intangible assets were not considered; (2) tangible assets sold for 50% of book value; (3) Current assets valued at 75% of book value; (4) cash and derivative financial instruments considered at 100% of book value24.

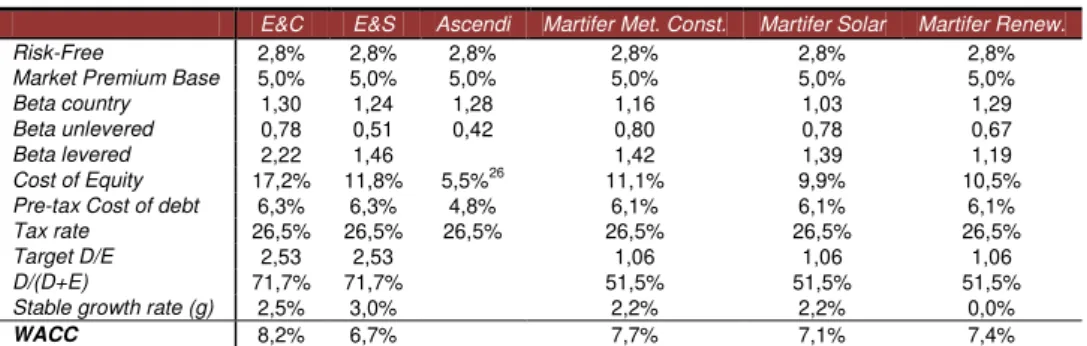

Then, we were in conditions to calculate the weighted average cost of capital for the company/segment25. A summary of the calculations realized for each company/segment can be seen in table 5.

Table 5 – Cost of Capital calculation

E&C E&S Ascendi Martifer Met. Const. Martifer Solar Martifer Renew.

Risk-Free 2,8% 2,8% 2,8% 2,8% 2,8% 2,8% Market Premium Base 5,0% 5,0% 5,0% 5,0% 5,0% 5,0% Beta country 1,30 1,24 1,28 1,16 1,03 1,29 Beta unlevered 0,78 0,51 0,42 0,80 0,78 0,67

Beta levered 2,22 1,46 1,42 1,39 1,19

Cost of Equity 17,2% 11,8% 5,5%26 11,1% 9,9% 10,5% Pre-tax Cost of debt 6,3% 6,3% 4,8% 6,1% 6,1% 6,1% Tax rate 26,5% 26,5% 26,5% 26,5% 26,5% 26,5%

Target D/E 2,53 2,53 1,06 1,06 1,06

D/(D+E) 71,7% 71,7% 51,5% 51,5% 51,5% Stable growth rate (g) 2,5% 3,0% 2,2% 2,2% 0,0%

WACC 8,2% 6,7% 7,7% 7,1% 7,4%

Source: Companies’ reports and NOVA SBE Equity Research Team

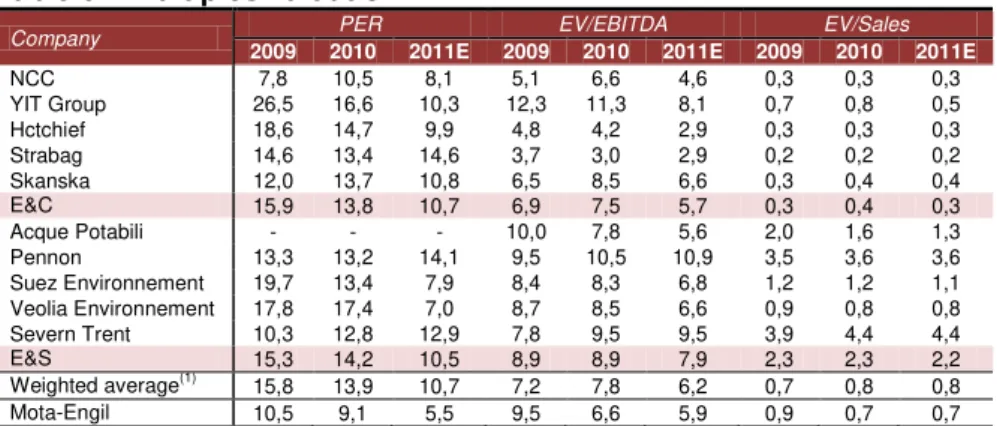

Multiples Valuation

In order to evaluate the accuracy of our analysis, we conducted a relative valuation for Mota-Engil (table 6) concluding that the company is being undervalued by the market.

20

Companies complying with the following criteria: (1) issuing amount superior to 300M€ to guarantee liquidity; (2) maturity in 2021, to match cash flows; (3) and finally, yields converted to Euros20.

21 PT long term emission and average Bloomberg BB composite indexes

22 Debt Expected Return = , where stands for probability of default. 23Moody’s Global Credit Policy, 2008. Corporate Default and Recovery Rates, 1920-2008. Moody’s.

24 Although there is no consensus in the field, we have adapted Benjamin Grahams conclusions. 25 WACC =

26 Cost of unlevered equity

MOTA-ENGIL COMPANY REPORT

THIS

DOCUMENT

IS

NOT

AN

INVESTMENT

RECOMMENDATION

AND

SHALL

BE

USED

EXCLUSIVELY

FOR

ACADEMIC

PURPOSES

(SEE DISCLOSURES AND DISCLAIMERS AT END OF DOCUMENT)PAGE 13/39 Source: Mota-Engil and NOVA SBE Equity

Research Team

Source: Mota-Engil and NOVA SBE Equity Research Team

Source: Mota-Engil and NOVA SBE Equity Research Team

Table 6 – Multiples valuation

Company PER EV/EBITDA EV/Sales

2009 2010 2011E 2009 2010 2011E 2009 2010 2011E

NCC 7,8 10,5 8,1 5,1 6,6 4,6 0,3 0,3 0,3

YIT Group 26,5 16,6 10,3 12,3 11,3 8,1 0,7 0,8 0,5

Hctchief 18,6 14,7 9,9 4,8 4,2 2,9 0,3 0,3 0,3

Strabag 14,6 13,4 14,6 3,7 3,0 2,9 0,2 0,2 0,2

Skanska 12,0 13,7 10,8 6,5 8,5 6,6 0,3 0,4 0,4

E&C 15,9 13,8 10,7 6,9 7,5 5,7 0,3 0,4 0,3

Acque Potabili - - - 10,0 7,8 5,6 2,0 1,6 1,3

Pennon 13,3 13,2 14,1 9,5 10,5 10,9 3,5 3,6 3,6

Suez Environnement 19,7 13,4 7,9 8,4 8,3 6,8 1,2 1,2 1,1

Veolia Environnement 17,8 17,4 7,0 8,7 8,5 6,6 0,9 0,8 0,8

Severn Trent 10,3 12,8 12,9 7,8 9,5 9,5 3,9 4,4 4,4

E&S 15,3 14,2 10,5 8,9 8,9 7,9 2,3 2,3 2,2

Weighted average(1)

15,8 13,9 10,7 7,2 7,8 6,2 0,7 0,8 0,8

Mota-Engil 10,5 9,1 5,5 9,5 6,6 5,9 0,9 0,7 0,7

Source: Bloomberg and NOVA SBE Equity Research Team

Engineering and Construction

Mota-Engil Engineering has more than 60 years of experience and constitutes Mota-Engil’s core business. Mota-Engil Engineering performs the full range of engineering and construction activities. It can be divided in four main areas: Infrastructures, Buildings, Real Estate and Other, where the remaining activities covering the spectrum of engineering and construction are included.

Angola was Mota’s first international experience. After that, the company expanded into several other Portuguese speaking countries. As a consequence of the international experience, engineering and construction activity is nowadays grouped in: Iberia, Africa and America, and Central Europe. Mota-Engil’s main objective is to focus on fast growing foreign markets as Angola, Poland, Brazil, Peru and Mexico, while decreasing domestic market weight.

Iberia

The Portuguese business segment includes not only Portugal but also residual activity in Spain and Ireland. Nevertheless, Portugal accounts for the majority of the turnover.

Europe is confronted with one of the most severe crisis of its history. Portugal’s GDP is expected to fall by 3% in 201227, Ireland will face a marginal growth of

0,4%, while Spain is forecasted to grow 0,8%, the last two according to IMF. As previously shown, Portugal has undergone a systematic crisis in the sector for the last decade. The austerity measures taken by the new executive and imposed by the Troika will pressure even more the fragile Portuguese construction industry.

Bottom line: We expect revenues to decrease at a CAGR of -1,8% from 2011 until 2016. EBITDA margin is expected to remain stable at 6,5% by 2016.

27 According to European Union statistics.

301 539

709

330 287 239

700 879 664

2008 2009 2010

Figure 14 - Historical sales by geography (million)

Africa & America Central Europe Iberia

61 74

113

5 4 8

64 53 42

2008 2009 2010

Figure 15 - Historical EBITDA by geography (million)

Africa & America Central Europe Iberia

700 879

664 638

552 540

0,0% 2,0% 4,0% 6,0% 8,0% 10,0%

0 200 400 600 800 1.000

2008 2009 2010 2011 (F) 2012 (F) 2013 (F)

M

il

li

on

s

Figure 16 - Iberia

MOTA-ENGIL COMPANY REPORT

THIS

DOCUMENT

IS

NOT

AN

INVESTMENT

RECOMMENDATION

AND

SHALL

BE

USED

EXCLUSIVELY

FOR

ACADEMIC

PURPOSES

(SEE DISCLOSURES AND DISCLAIMERS AT END OF DOCUMENT)PAGE 14/39 Africa

With more than 60 years of activity in Angola, in 2010 the group decided to constitute Mota-Engil Angola, as a result of a partnership with Sonangol. Historically Angola has been one of the fastest growing economies in the world – average real GDP growth rate of 12% during the period 2003-201028 - and is

expected to continue its growth after a sluggish period precipitated by commodities decrease in price in the aftermath of the 2008 crisis. IMF projections point towards a 3,7% real GDP growth in 2011 and a 10,8% increase in 2012, followed by a more stable growth of 6% afterwards.

Growth rates in real GDP are also very interesting in Mozambique. Again, according to IMF projections, Mozambique will grow 7,2% in 2011 and 7,5% in 2012, maintaining growth at these levels after that year. During the year of 2011 Mota-Engil started road works in Mozambique worth €108 mn. As the majority of the construction works in Mozambique, this construction project will be paid in 80% by the World Bank. The Olympic village involving the construction of 106 buildings within a 15 hectares area was inaugurated in August, 10 months after its beginning, sealing Mota-Engil’s reputation in the market.

Malawi business profile is considerably different, with mining being Mota-Engil’s main activity in this market, posing an opportunity to diversify. Even though, IMF predicts 4,6% in 2011 and 4,2% in 2012, well above European growth rates.

Bottom line: In the first 9 months revenues declined 22%, mainly due to delays in Angola. EBITDA margin increased from 18,5% to 20,3%, result of the effort to increase efficiency, namely through centralized purchasing. Bearing this in mind, we expect EBITDA margins to increase to 20,6% by the end of 2011. Revenues are expected to increase at a CAGR of 7,4% in Euros from 2011 until 2016, reaching an EBITDA margin of 17,8% in that year. Angola is expected to grow at a CAGR of 5,4% over the same period.

America

The most significant countries for Mota-Engil in America are Mexico and Peru. Mota-Engil intends to enter the Columbian market and, as António Mota stated last year, Mota-Engil expects to announce an entry in the Brazilian market very soon.

Brazil will receive the Football World Cup in 2014 (estimated total investment of $55bn) and the Olympic Games in 2016 (forecasted investment of $15bn)29.

28 International Monetary Fund, September 2011. World Economic Outlook, IMF.

29 Deloitte, 2010. Brasil, bola da vez. Negócios e investimentos a caminho dos megaeventos desportivos. 0 20 40 60 80 100 120 140 160 N o v-06 Feb 2 00 7 M ay 2 00 7 A u g 2 00 7 N o v-07 Feb 2 00 8 M ay 2 00 8 A u g 2 00 8 N o v-08 Feb 2 00 9 M ay 2 00 9 A u g 2 00 9 N o v-09 US D

Figure 17 - WTI Crude Oil Price

Source: Bloomberg and NOVA SBE Equity Research Team

Source: Mota-Engil and NOVA SBE Equity Research Team

Source: Mota-Engil and NOVA SBE Equity Research Team

301

403 452

312 328 339

0 100 200 300 400 500

2008 2009 2010 2011 (F) 2012 (F) 2013 (F) M il li on s

Figure 19 - Turnover Angola

Source: Mota-Engil and NOVA SBE Equity Research Team 301 497 626 481 523 552 0,0% 5,0% 10,0% 15,0% 20,0% 25,0% 0 100 200 300 400 500 600 700

2008 2009 2010 2011 (F) 2012 (F) 2013 (F)

M il li o n s

Figure 18 - Africa

Revenues EBITDA margin CAGR =12,9% 42 83 134 176 201 0,0% 2,0% 4,0% 6,0% 8,0% 10,0% 12,0% 0 50 100 150 200 250

2009 2010 2011 (F) 2012 (F) 2013 (F)

M

il

li

ons

Figure 20 - America

MOTA-ENGIL COMPANY REPORT

THIS

DOCUMENT

IS

NOT

AN

INVESTMENT

RECOMMENDATION

AND

SHALL

BE

USED

EXCLUSIVELY

FOR

ACADEMIC

PURPOSES

(SEE DISCLOSURES AND DISCLAIMERS AT END OF DOCUMENT)PAGE 15/39

Furthermore, according to BNDES (Banco Nacional do Desenvolvimento), Brazil will invest near €120 bn in infrastructures until 2013. Allied to this, the IMF expects a real GDP growth of 3,8% and 3,6% for 2011 and 2012, respectively, hence, substantial construction activity is expected for the next few years. Portuguese construction companies entering the market are, though, facing substantial difficulties: obtaining the recognition of Portuguese engineering certificates is taking, typically, more than 12 months30; bureaucracy is a constant in every step

you take; and, it is already a rather competitive environment. Nevertheless, several diplomatic efforts are being taken, framing the conditions for Mota-Engil entrance.

Mota-Engil announced the adjudication of 4 contracts worth €125mn for the construction and recovery of roads giving access to a mine in Cusco’s region of Peru. The company has also announced in March the adjudication of another contract worth €59,5mn. Also during the year the company’s headquarters in the country were inaugurated, signaling Mota-Engil’s commitment to this geography. Peru is expected to present interesting GDP growth rates in 2011 and 2012 of 6,2% and 5,6%, according to IMF forecasts.

Mota-Engil has also improved its position in Mexico with the extension of the Perote-Xalapa contract, both in terms of time and size. Mota-Engil’s activity in Mexico is done through IDINSA, a jointly owned company with Opway. It is through this company that the Group expects to drive its growth in the Mexican market, continuing taking advantage of the Mexican government’s 2007-2012 National Infrastructure Programme, estimated at €300 bn31.

Bottom line: In the first 9 months of 2011 the company registered an increase of 292% in its turnover (€). We expect America to continue its top-notch performance and to sustain 2010 margins, with revenues growing at a CAGR of 15% in Euros until 2016, reaching an EBITDA margin of 10% vs 7% in 2010.

Central Europe

The Engineering and Construction area, although doing business in other countries of the region, concentrates its activity in Poland.

Poland is expected to exhibit GDP growth rates of 3,8% in 2011 and 3% in 2012. Besides being the host of the Euro 2012, Poland has currently a huge shortage of infrastructures. The total amount of funds allocated to the road construction

30Sol, 2011. Brasil bloqueia participação de engenheiros portugueses no Mundial e Jogos Olímpicos. [online] Available at:

<http://sol.sapo.pt/inicio/Internacional/Interior.aspx?content_id=30790> [Accessed November 2011].

31 Mexican Infrastructure, 2007. [online] Available at <http://www.infraestructura.gob.mx/> [Accessed on November 2011].

Brazil as an opportunity for Mota-Engil expansion’s in America…

Source: Mota-Engil and NOVA SBE Equity Research Team

330 287

239

365 365 377

0,0% 1,0% 2,0% 3,0% 4,0% 5,0% 6,0%

0 50 100 150 200 250 300 350 400

2008 2009 2010 2011 (F) 2012 (F) 2013 (F)

M

il

li

on

s

Figure 21 - Central Europe

MOTA-ENGIL COMPANY REPORT

THIS

DOCUMENT

IS

NOT

AN

INVESTMENT

RECOMMENDATION

AND

SHALL

BE

USED

EXCLUSIVELY

FOR

ACADEMIC

PURPOSES

(SEE DISCLOSURES AND DISCLAIMERS AT END OF DOCUMENT)PAGE 16/39 30%

18% 25%

13% 14%

Figure 22 - Total Backlog

E&C Portugal E&C Central Europe E&C Africa

E&C America E&S

program starting in 2013 will amount to €20,7 bn , which poses a good opportunity for Mota-Engil in the market32 given its current know-how and positioning.

Historically, Mota-Engil’s margins in the country have been substantially low. In order to improve it, the Group implemented changes to the Corporate Management Model and a modernization of the Management Systems of Mota-Engil Central Europe. In September Mota-Mota-Engil won the construction of 16,6km of the S8 motorway worth €127 mn, reinforcing its backlog in the country to €600 mn. In March the company was awarded with the construction of 24,5km of the S17 motorway, worth €158 mn.

Bottom line: In the first 9 months of 2011, revenues grew by 64% (€) when

compared to the same period of the previous year. EBITDA margin, after a good growth to 6,4% in the second quarter of 2011, fell again to 2,6% in the third quarter. We expect revenues to grow at a CAGR of 4,9% in Euros until 2016, with EBITDA margins improving from 3,3% in 2010 to 6,5% in 2016.

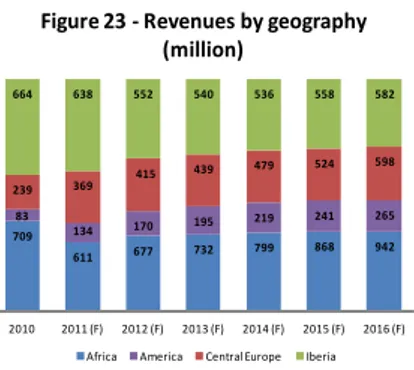

Total Backlog

Figure 22 shows the backlog distribution by geography and business area in the third quarter of 2011. The total backlog remained relatively stable, amounting to €3,3 bn, the same value as at the end of 2010. More than 60% of this value comes from international activity, which represents a noticeable increase from €1.7 bn in 2010 to €2 bn in 2011. The estimated backlog for the E&C area still represents the majority of total value – €2,9 bn. Total backlog represents 1 year and 8 months of sales, very good indicator since according to AECOPS33, the average backlog for Portuguese construction companies corresponds to 8 months of sales.

Conclusion

All in all, we expect the national market to represent only 29,2% of total group's revenues in 2016 vs 41,5% in 2010. EBITDA margins from international markets will also be considerable higher compared to the domestic market, reaching 12,8% in 2016 vs. 6,5% for the Iberian market.

32 Jornal Construir, 2011.

Polónia apresenta na Concreta plano de investimento de 20,7 mil milhões de euros. [online] Available at:

<http://www.construir.pt/2011/10/18/polonia-apresenta-na-concreta-plano-de-investimento-de-207-mil-milhoes-de-euros/> [accessed on December

2011].

33 Jornal da Construção, 2011. Carteira de encomendas das empresas é inferior a oito meses. [online] Available at:

<http://www.jornaldaconstrucao.pt/index.php?id=10&n=2140&fp=1> [Accessed November 2011].

Improving margins in Central Europe…

Source: Mota-Engil and NOVA SBE Equity Research Team

Source: Mota-Engil and NOVA SBE Equity Research Team

709

611 677 732 799 868 942

83

134 170 195 219 241 265

239 369 415

439 479 524 598

664 638 552 540 536 558 582

2010 2011 (F) 2012 (F) 2013 (F) 2014 (F) 2015 (F) 2016 (F)

Figure 23 - Revenues by geography (million)

MOTA-ENGIL COMPANY REPORT

THIS

DOCUMENT

IS

NOT

AN

INVESTMENT

RECOMMENDATION

AND

SHALL

BE

USED

EXCLUSIVELY

FOR

ACADEMIC

PURPOSES

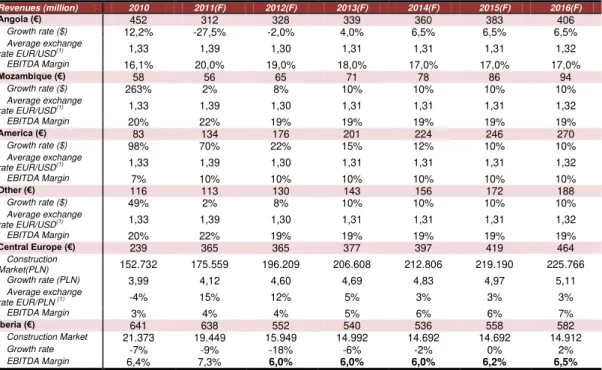

(SEE DISCLOSURES AND DISCLAIMERS AT END OF DOCUMENT)PAGE 17/39 Table 7 – E&C revenue’s growth rates and EBITDA margin estimates:

Revenues (million) 2010 2011(F) 2012(F) 2013(F) 2014(F) 2015(F) 2016(F)

Angola (€) 452 312 328 339 360 383 406

Growth rate ($) 12,2% -27,5% -2,0% 4,0% 6,5% 6,5% 6,5%

Average exchange

rate EUR/USD(1) 1,33 1,39 1,30 1,31 1,31 1,31 1,32

EBITDA Margin 16,1% 20,0% 19,0% 18,0% 17,0% 17,0% 17,0%

Mozambique (€) 58 56 65 71 78 86 94

Growth rate ($) 263% 2% 8% 10% 10% 10% 10%

Average exchange

rate EUR/USD(1) 1,33 1,39 1,30 1,31 1,31 1,31 1,32

EBITDA Margin 20% 22% 19% 19% 19% 19% 19%

America (€) 83 134 176 201 224 246 270

Growth rate ($) 98% 70% 22% 15% 12% 10% 10%

Average exchange

rate EUR/USD(1) 1,33 1,39 1,30 1,31 1,31 1,31 1,32

EBITDA Margin 7% 10% 10% 10% 10% 10% 10%

Other (€) 116 113 130 143 156 172 188

Growth rate ($) 49% 2% 8% 10% 10% 10% 10%

Average exchange

rate EUR/USD(1) 1,33 1,39 1,30 1,31 1,31 1,31 1,32

EBITDA Margin 20% 22% 19% 19% 19% 19% 19%

Central Europe (€) 239 365 365 377 397 419 464

Construction

Market(PLN) 152.732 175.559 196.209 206.608 212.806 219.190 225.766

Growth rate (PLN) 3,99 4,12 4,60 4,69 4,83 4,97 5,11

Average exchange

rate EUR/PLN (1) -4% 15% 12% 5% 3% 3% 3%

EBITDA Margin 3% 4% 4% 5% 6% 6% 7%

Iberia (€) 641 638 552 540 536 558 582

Construction Market 21.373 19.449 15.949 14.992 14.692 14.692 14.912

Growth rate -7% -9% -18% -6% -2% 0% 2%

EBITDA Margin 6,4% 7,3% 6,0% 6,0% 6,0% 6,2% 6,5%

Source: Mota-Engil and NOVA SBE Equity Research Team

(1) Data collected Monday, January 02, 2012.

After a small decrease in 2011 due to payments from the Angolan government that were due in 2009 and 2010, we expect net working capital to increase slightly as a percentage of revenues until 2013, period after which we expect it to stabilize as uncertainty is reduced. Both growth and maintenance capex are assumed to increase in 2014, when credit restrictions are expected to be considerably lower than today.

Table 7 – E&C FCF calculation

FREE CASH FLOW 2012(F) 2013(F) 2014(F) 2015(F) 2016(F) Terminal Value

(+) EBIT 102,1 105,7 119,7 191,6 211,3

(-) Income Tax -27,3 -28,3 -32,1 -51,4 -56,5

(+) D&A 55,4 55,4 57,2 0,0 0,0

(+) Provisions & Others 8,0 11,6 7,0 7,4 6,0

(-) Capex -69,8 -72,2 -83,5 -100,0 -110,5

(-) Change in NWC 23,2 -36,2 -0,6 -12,3 -15,2

Free Cash Flow Most Probable 91,6 36,0 67,7 35,3 35,1

Probability 96,1% 91,6% 86,2% 83,6% 81,5%

FCF Bankruptcy 0,0 0,0 0,0 0,0 0,0

Probability 3,9% 8,4% 13,8% 16,4% 18,5%

Weighted FCF 88,0 32,9 58,3 29,5 28,6 512,5

Source: NOVA SBE Equity Research Team

Environment and Services

Mota-Engil Environment and Services has more than 15 years of experience and is involved in an ample range of activities. The business unit is divided in four

Source: Mota-Engil and NOVA SBE Equity Research Team

101,4

112 119

14 47 76

143

151 159

27,5 53 58

0% 20% 40% 60% 80% 100%

2008 2009 2010

Figure 24- Historical sales by segment (million)

MOTA-ENGIL COMPANY REPORT

THIS

DOCUMENT

IS

NOT

AN

INVESTMENT

RECOMMENDATION

AND

SHALL

BE

USED

EXCLUSIVELY

FOR

ACADEMIC

PURPOSES

(SEE DISCLOSURES AND DISCLAIMERS AT END OF DOCUMENT)PAGE 18/39

distinct segments: Waste, Water, Logistics and Multi-services. All the segments are characterized by relative stability and very interesting margins.

Waste

Mota-Engil is the market leader in the privatized solid urban waste management market, mainly through SUMA and its subsidiaries, representing a core business of this business unit.

The Waste sector in Portugal is mostly characterized by stagnation due to its maturity levels. SUMA reached a market share of 54% at the end of 2010, when considering only the privatized market. Abroad, SUMA expanded its activity to Poland and Angola. Last year it acquired Geo Vision and entered the Brazilian market34. If in 2010 only 20% of the turnover was generate internationally, by 2011 this value is expected to increase to 47%35. Since a substantial part of the business is still held in Portugal, we expect the current financial crisis to provoke a delay in payments from municipalities, impacting net working capital.

Bottom line: In the first 9 months of 2011 revenues increased 53% due to Geo Vision’s consolidation, with a slight decrease in the margin from 25,9% to 23,6%. We expect revenues to grow at a CAGR of 5,0% until 2016 vs. 11,5% in the last 3 years. EBITDA Margins are expected to remain stable at 24% until 2016. There is, however, the risk of adjustments to already celebrated contracts. The risk was mitigated by considering considerably lower margins in 2016 than the historical ones.

Water

Mota-Engil Water management business is developed through Indaqua. In Portugal it includes the concessions of Fafe, Santo Tirso, Trofa, Santa Maria da Feira, Matosinhos and Vila do Conde. Internationally, Indaqua controls Vista Water, an Angolan company.

Indaqua is the major private Portuguese Operator to what municipal water concessions is concerned. Despite of not so interesting prospects due to the recent financial turmoil the company expects to maintain its current client’s base. The company is actively seeking for new locations, namely in South America. Peru and Brazil, due to their macroeconomic environment and Mota-Engil’s previous experience, are seen as the most interesting targets. Ireland is also an alternative, due to huge shortfalls of infrastructures in the water segment.

34 Geo Vision’s consolidation was responsible for the recent growth presented in the first 9 months results.

35 SUMA, 2011. Suma em números. [online] Available at: <http://www.suma.pt/conteudos/artigos/detalhe_artigo.aspx?idc=5&idsc=10&idl=1>

[accessed December 2011].

Geo Vision broadening Waste management international profile…

Source: INE and private operators

Municipa l; 3.800.584 Concessio ns; 1.897.833 E.E.M; 1.859.817 E.M.S.A; 334.109 SMAS; 2.734.907

Figure 27 - Water Management (operator €)

Source: Mota-Engil and NOVA SBE Equity Research Team

Source: Mota-Engil and NOVA SBE Equity Research Team

101 112 119

175 192 204 21,0% 22,0% 23,0% 24,0% 25,0% 26,0% 27,0% 28,0% 0 50 100 150 200 250

2008 2009 2010 2011 (F) 2012 (F) 2013 (F) M il li on s

Figure 25 - Waste

Revenues EBITDA margin CAGR= 15% 14 47 76 86 91 97 0,0% 10,0% 20,0% 30,0% 40,0% 0 20 40 60 80 100 120

2008 2009 2010 2011 (F) 2012 (F) 2013 (F) M il li on s

Figure 26- Water

MOTA-ENGIL COMPANY REPORT

THIS

DOCUMENT

IS

NOT

AN

INVESTMENT

RECOMMENDATION

AND

SHALL

BE

USED

EXCLUSIVELY

FOR

ACADEMIC

PURPOSES

(SEE DISCLOSURES AND DISCLAIMERS AT END OF DOCUMENT)PAGE 19/39

Bottom line: Turnover of the segment amounted to €61 mn in the first 9 months of 2011, a 12% increase when compared with 2010. EBITDA margin amounted to 22,6% versus 21,5% in 2010. If on the one hand, revenues growth is expected to decline to more reasonable values, growing at a CAGR of 4,4% until 2016, on the other hand EBITDA margins are expected to improve after mid 2012 to 26% in 2016 vs. 23,4% in 2010. We believe there is the risk of adjustments to already celebrated contracts. Once again, we have mitigated this risk by considering considerably lower margins in 2016 than historical ones.

Logistics

Mota-Engil, through its subsidiary Tertir, is the national market leader in ports. It explores Leixões, Aveiro, Lisboa, Setúbal and Sines marine terminals, as well as the logistic platform in Poceirão, allowing an integrated logistics and carriage of goods by train. However, Portugal is not their solely market. The company operates a 30 year concession in Peru (Puerto Paita), the second largest in the country, and has a participation in Transitex, a global player acting in markets such as Spain, Mexico, Venezuela, amid others. Tertir Group will continue to focus in its internationalization process, namely through the increase of Sonauta’s activity, an Angolan company specialized in coastal shipping between Angolan ports.

Despite of the severe economic crisis affecting Portugal, the logistics segment increased its turnover during the first 9 months of the year. This was mainly due to stable imports and increasing exports that contributed to an increase of traffic on the marine terminals, namely Sines and Leixões.

It is important to highlight that Mota-Engil expects the revocation extending the Alcantara terminal concession to 2042 to be declared unconstitutional. However, no decision has yet been made. We have considered the extension in our analysis. However, under a scenario under which the concession ends in 2015, we expect it to impact the price target in 0,04€.

A possible driver for the segment will be the expansion of Panama Canal, as it may impact the world current ship routes. With it, an increase in traffic to Portugal from Asia may be a reality. The expansion is not expected to be completed before 2014, though.

Bottom line: In the first 9 months of the year revenues increased 13%, while EBITDA margin increased from 19,7% to 21,9%. We expect revenues to grow at

291 0 328 15 163 305 0 337 30 247 0 50 100 150 200 250 300 350 400

LEIXÕES AVEIRO LISBOA SETÚBAL SINES

T h ou sa n d s

Figure 29 - Total number of containers

2009 2010

Source: IPTM and NOVA SBE Equity Research Team INDAQUA 27% Aquapor 26% AGS 24% Veolia 15% Other 8%

Figure 28 - Percentage of total population served by private water

operators

Source: INE and private operators

Source: Mota-Engil and NOVA SBE Equity Research Team

143 151 159

172 186 197

0,0% 5,0% 10,0% 15,0% 20,0% 25,0% 30,0% 0 50 100 150 200 250

2008 2009 2010 2011 (F) 2012 (F) 2013 (F) M ill ion s

Figure 30 - Logistics

Revenues EBITDA margin