THIS REPORT WAS PREPARED BY MICHAEL LÜFFE, A MASTERS IN FINANCE STUDENT OF THE NOVA SCHOOL OF BUSINESS AND

ECONOMICS, EXCLUSIVELY FOR ACADEMIC PURPOSES.THIS REPORT WAS SUPERVISED BY ROSÁRIO ANDRÉ WHO REVIEWED THE

M

ASTERS IN

F

INANCE

E

QUITY

R

ESEARCH

A flight, investors should board

Capacity discipline continues to be key profit driver

For the past two years Delta Air Lines has been generating benchmark returns that other US legacy carriers were struggling to keep up with.

Going forward the airline will have to increasingly invest in the replacement as well as expansion of its aircraft fleet which is one of the oldest in the industry. Higher capital expenditures will inevitably come at the expense of shareholder cash returns.

Even against the backdrop of rising crude oil and jet fuel prices, operating margins are forecasted to remain in a range of 14% to 18% until 2025. This is subject to the condition that the US airline industry remains disciplined about capacity growth and that unit revenues in Delta’s international markets continue to recover.

Valuation: We recommend buying Delta Air Lines given our price target for year end 2017 of $61.74 per share, offering investors an upside potential of 24.15% to the current share price of $49.73.

Company description

Delta Air Lines, Inc., founded in 1924 and headquartered in Atlanta, Georgia, offers air transportation services to passengers and cargo throughout the United States and on international routes. Furthermore, the company runs an oil refinery which provides its north eastern US airline operations with jet fuel. As of today, the company and its global alliance partners offer air travel services to 323 destinations in 57 countries across all six continents.

D

ELTA

A

IR

L

INES

,

I

NC

.

C

OMPANY

R

EPORT

I

NDUSTRIALS

6

J

ANUARY2017

S

TUDENT

:

M

ICHAEL

L

ÜFFE

(#972)

[email protected]

Recommendation: BUY

Price Target FY17: 61.74 $

Price (as of 6-Jan-17) 49.73 $

Reuters: DAL.N, Bloomberg: DAL:US

52-week range ($) 33.36-51.78 Market Cap ($m) 37,335.00 Outstanding Shares (m) 736.39

Source: Yahoo Finance

Source: Fidelity, 06.01.2017

DELTA AIR LINES,INC. COMPANY REPORT

Table of Contents

COMPANY OVERVIEW ... 3

COMPANY DESCRIPTION ... 3

SHAREHOLDER STRUCTURE ... 4

ANALYSIS OF REGIONS/MARKETS ... 6

NORTH AMERICA... 6

LATIN AMERICA ... 12

ATLANTIC ... 13

THE AIRLINE INDUSTRY ...14

FIVE FORCES ... 14

Competition ... 14

Industry entry and exit ... 15

Substitute and complement products or services ... 16

Supplier power ... 17

Buyer power ... 18

COMPETITIVE ANALYSIS ...19

SWOT ANALYSIS ... 19

Strengths ... 19

Weaknesses ... 20

Opportunities ... 21

Threats ... 21

RISKS TO THE INVESTMENT THESIS ...22

EXTERNAL RISKS... 22

INTERNAL RISKS ... 23

FINANCIAL OUTLOOK ...24

DIVIDEND POLICY ... 24

VALUATION ...24

WACC APPROACH ... 24

MULTIPLES ... 25

DELTA AIR LINES,INC. COMPANY REPORT

Company overview

Company description

Founded in 1924 as an aerial crop dusting operation, Delta Air Lines, Inc. (NYSE: DAL) is nowadays one of the largest US carriers and a globally operating airline, that employs 84,000 people worldwide, manages a mainline fleet of more than 800 aircraft and offers air travel services to nearly 60 countries all over the world.1 Since

2012 the Atlanta-based company has split its operating activities into two distinct segments, airline and refinery, whose relative importance as measured by operating revenues has been very different, a fact that is highlighted by the waterfall chart in Figure 1 giving a precise breakdown of consolidated revenue in 2015. Delta’s airline segment provides air transportation both for passengers and cargo throughout the United States as well as to and from international destinations. With a CAGR2 of 6.52% since 2009 and an 85% share of operating

revenue in 2015, passenger air travel has been an important value driver for Delta Air Lines, while cargo’s CAGR of 0.52% reflects the massive decay that this particular business division has been in for more than four years. Figure 2 further visualizes the evolution of operating revenue. Delta’s extensive route network is based on a system of domestic hubs, most important of which are Atlanta, Boston, Detroit, Los Angeles, Minneapolis-St. Paul, New York JFK, New York LaGuardia, Salt Lake City and Seattle, as well as international gateway airports, such as Amsterdam, London-Heathrow, Paris-Charles de Gaulle and Tokyo-Narita. Delta’s operations in these markets include flights, gathering and distributing traffic from the geographic regions surrounding the hub or gateway to domestic or international cities or other hubs and gateways. Figure 3 provides an overview of the percentages of Delta’s total domestic flights and passengers that were processed through each one of its nine US hubs in 2015. The fact that an astonishing 60% of inland flights and passengers were apportioned to these hubs indicates a strong dependency that has persisted for more than five straight years and suggests a fundamental operational risk.

In addition to air transportation, the airline segment provides other ancillary airline services, such as maintenance and repair services (MRO) for third parties. Delta’s air travel services are sold through various distribution channels, including

1http://news.delta.com/corporate-stats-and-facts

2 The mean annual growth rate over a time period longer than one year is referred to as compound annual growth rate. It

is calculated by dividing the value at the end of a period by the value at the beginning, raising it to the power of one divided by the length of the period and subtracting one from the result.

Figure 1: Operating revenues by segment 2015 (in million USD)

Source: Company Data

Figure 2: Operating revenues 2009-2015 (in million USD)

Source: US Bureau of Transportation

Figure 3: Delta’s US hubs’ share of 2015 domestic passengers and flights apportioned to hubs

DELTA AIR LINES,INC. COMPANY REPORT

telephone reservations, online travel agencies and digital channels, such as mobile and delta.com.

Delta’s refinery segment produces gasoline, diesel and jet fuel. Its wholly owned Monroe Energy subsidiary runs the Trainer refinery located near Philadelphia, Pennsylvania. The refinery facilities include pipelines and terminal assets allowing the supply of jet fuel from its own production as well as from third party suppliers Phillips 66 or BP to the airline segment.3

As of October/November 2016 the flight network of Delta Air Lines encompasses a total of 2,052 routes. These can be split into 64% domestic routes, connecting cities in the contiguous and non-contiguous United States or their insular territories, and 36% international routes. Figure 4 shows that the majority of international routes cover the trans-Atlantic region, followed by the Latin American and the Asian/Pacific region. Figure 5 indicates Delta’s strong positioning in its core market United States, where its trailing twelve months’ market share amounted to 16.8% as of end of September 2016. Only American Airlines and Southwest Airlines were able to claim a bigger share of the domestic market. In 2015 Delta boarded almost 180 million passengers. The airline is a founding member of the SkyTeam global airline alliance and participates in the industry leading transatlantic joint venture with Air France-KLM and Alitalia. Counting its worldwide alliance partners, Delta offers customers more than 15,000 flights per day. By total revenue and capacity, Delta Air Lines is the second largest US carrier after American Airlines.

Like the other US network carriers American Airlines and United Airlines, Delta incurred significant operating losses in the early 2000s. These were not only the result of a strongly receding travel demand in the aftermath of the 9/11 attacks, both at home and abroad, but were to a great extent also caused by the effects of an over-competitive airline industry. In 2005, the new Delta Air Lines emerged from Chapter 11 bankruptcy proceedings and in the same year merged with Northwest Airlines.

Shareholder structure

Figure 6 states that the shareholder structure of Delta Air Lines is largely dominated by institutional owners, which held approximately 83% of the company’s outstanding shares by the end of the third quarter 2016.4 Such a high ownership

stake of institutional investors may impact the company’s stock price in many

3http://www.reuters.com/finance/stocks/companyProfile?symbol=DAL.N

4https://eresearch.fidelity.com/eresearch/evaluate/fundamentals/ownership.jhtml?stockspage=ownership&symbols=DAL Source: US Bureau of Transportation

Figure 5: Trailing twelve months’ (TTM) domestic market share of US airlines Figure 4: Division of Delta’s route network into four geographic regions

Source: Company Data

Source: Fidelity, 13.11.2016

DELTA AIR LINES,INC. COMPANY REPORT

different ways, good and bad. In general, a high percentage of institutional ownership signifies a strong shareholder base as investors are usually in for the long haul and, unless they are momentum investors, endure periods of downturn.5

There has been only a slight change of institutional ownership percentage in 2016. Financial institutions sold more shares than they purchased, leading to a drop in ownership of 1.94%. Given the distinct research capacities that investment banks or fund managers have at their disposal, they are considered to be well informed and to make reasonable investment decisions. In terms of marketing, Delta achieves a multiplier effect by getting large institutions to go long its stock. JP Morgan, for example, advertises its holdings in Delta’s stock in order to create interest in them and boost the stock price. With regards to their corporate governance function, institutional investors can positively influence the company by monitoring management decisions and applying pressure if need be.6

Nonetheless, an institutional investor majority can equally be a burden to the company and hamper its performance. In view of institutions’ thorough research on security and industry fundamentals, any position they take is evaluated by the market as a justified response to a change in the stock’s projected value. However, institutional buy or sell transactions are often merely motivated by arbitrage or short-term market inefficiencies and not necessarily supported by underlying fundamentals.7 This market behavior can easily trigger a sell-off and destroy value,

especially in light of the enormous amount of shares that have to be absorbed by the market in case several institutional investors act at the same time. The compensation of fund managers is usually based to a large degree on the profits they generate and their performance is evaluated against a group of benchmark indices. This system promotes short-term investing, such as the sale of temporarily underperforming stocks, which drives up their volatility.8 In the case of Delta this

could have contributed to a higher systematic risk parameter, given through a levered beta of 1.26, which is slightly above our calculated US airline industry average of 1.25.

Recent research on the airline industry suggested that common institutional ownership among major U.S. airlines has a tremendous impact on airfares, which led the Department of Justice to investigate. Due to the fact that companies such as Delta, American, United or Southwest are all controlled by a small number of institutional investors, the price competition is likely to be less intensive. Even

5https://www.thestreet.com/story/1039002/1/what-short-interest-and-institutional-ownership-tell-you.html 6

http://www.slate.com/articles/news_and_politics/view_from_chicago/2015/04/mutual_funds_make_air_travel_more_expen sive_institutional_investors_reduce.html

DELTA AIR LINES,INC. COMPANY REPORT

though investors do not actively dictate prices or interfere with an airline’s operating business, airfares were shown to be three to five percent higher because of cross-shareholding.9 If for instance Delta and United are the sole competitors on selected

routes, both the fund investing in Delta as well as United and the managers working at the two carriers benefit from higher prices and higher profits.10 As of September

30, 2016, five of the top ten institutional investors in Delta, American and United were the same.

Analysis of regions/markets

Delta Air Lines offers air travel services to four different geographical regions, which are North America, Latin America, Atlantic and Pacific. Each of these regions has unique economic potential for airlines to grow and a different competitive situation, which are two crucial factors that impact Delta’s valuation going forward as they are reflected in the amount of revenue generated. Figure 7 shows the development of Delta’s passenger revenue by geographical regions from 2009 to 2015. Figure 8 specifies the percentage breakdown of these regions in 2015.

North America

In spite of Delta’s global presence, the North American region is still its most important market. Key figures even indicate that it will continue to be for the foreseeable future. Since 2009 the share of passenger revenue generated in this market has increased from approximately 45% to over 50%. Also it is the North American region that Delta traditionally achieves its best load factors in. In terms of Delta’s flight network, roughly two-thirds are domestic routes as of October/November 2016. And on top of this the domestic market accounted for 61% of Delta’s air travel capacity.

As of year-end 2015 North America was the second largest region based on capacity with a 25.3% share of the world total, second only to Asia/Oceania with and slightly ahead of Europe, as Figure 9 proves. However, North America’s growth in capacity, measured in available seat miles (ASM)11, or other metrics,

9

http://www.nytimes.com/2016/04/13/business/dealbook/rise-of-institutional-investors-raisesquestions-of-collusion.html?_r=0

10

http://www.slate.com/articles/news_and_politics/view_from_chicago/2015/04/mutual_funds_make_air_travel_more_expen sive_institutional_investors_reduce.html

11 ASM quantify the amount of capacity offered by an airline. It is the number of seats available for transporting

revenue-paying passengers multiplied by the total number of miles flown over the course of a reporting period.

Figure 7: Passenger revenue 2009-2015 by regions (in million USD)

Source: Company Data

Figure 8: Percentage breakdown of passenger revenue 2015 by regions

Source: Company Data

Source: Oliver Wyman

DELTA AIR LINES,INC. COMPANY REPORT

such as departures, average seats per departure or average stage-length, lag considerably behind those of other world regions. ASM between October 2014 and October 2015 were only up 4.6% compared to a year earlier. Growth in ASM was primarily driven by a 3.5% increase in the seat average per departure and a 2.5% increase of the average stage-length, while the number of scheduled departures between October 2014 and October 2015 actually declined by 1.1%, as is shown in Figure 10. Between October 2011 and October 2015, the decline in departures even amounted to 5%, while seats per departure were up 4.7% and ASM 14%. This development is in line with a general capacity trend for the North American region in which smaller gauge regional jets, usually equipped with less than 70 seats, are continuously being replaced by larger and more fuel efficient aircraft flying longer distances. This development is supported by the fact that as of October 2015 North American airlines had placed orders for almost 2,000 aircraft to be delivered until 2020 with half of the deliveries being for large narrow-body aircraft with more than 160 seats. A look at the ratio between long haul and short haul flights underlines this development. Of a 58 country sample, the United States had the fourth largest share of long haul passengers in 2015, with almost 70% of all domestic passengers travelling on flights that lasted at least three hours. Figure 11 compares the five previously mentioned world regions by their average share of long haul as well as short haul passengers in 2015. For the whole sample, the arithmetic average share of long haul passengers amounted to 29%.

Another significant air travel trend regarding the North American region is that capacity from North America to other regions outgrew capacity within the region by far, suggesting that US airlines have been expanding massively to Latin America and the Caribbean. All in all, capacity growth metrics for North America suggest that the region is the most mature of the five major world regions. There seems to be overcapacity in the market because passenger load factors have been declining since 2013. US airlines are reacting to this by trimming their capacity expansion. Capacity growth within North America was below GDP growth for the year 2015. Due to only moderately rising jet fuel prices, particularly value carriers are forecasted to add capacity inside the region but even more so outside due to their incorporating international flights in the otherwise domestically dominated route networks.

Capacity and traffic numbers considered separately from each other do not indicate a lot about the strategic direction Delta has chosen or its profitability in certain markets. The metric passenger load factor, however, focuses on the ratio between both numbers, thus allowing to properly evaluate ups and downs in the utilization of Delta’s capacity. Appendix 1 shows that in terms of load factor, both

Source: Oliver Wyman

Figure 10: North America capacity changes October 2014/2015

Figure 11: Average share of long haul vs short haul passengers in 2015 by regions

DELTA AIR LINES,INC. COMPANY REPORT

domestic mainline and regional have improved from 2014 to 2015, lifting the domestic region as a whole from 85.18% to 85.98%, a trend that has been reversed in 2016. This is because US airlines have aggressively grown their supply due to lower fuel costs and other facilitating circumstances.

Appendix 1 furthermore highlights that since 2014 the share of domestic mainline capacity in relation to Delta’s total system capacity has risen by almost three percentage points to 50.6%. Domestic regional capacity was further reduced, both in absolute and relative terms, as it dropped to just over 10% of total system capacity from above 11% back in 2014. This is the result of Delta’s efforts to be less dependent on regional carriers, conducting flights under Delta Connection. Table 1 shows that as of October/November 2016 the airline is still very much reliant on regional carriers, as SkyWest, Endeavor Air or ExpressJet Airlines each service about a fifth of Delta’s route network. It is also a natural outcome of capacity relocation measures that airlines conduct on a monthly basis in order to have their airplanes serve the most profitable or heavily-frequented routes. Delta’s significant exposure to the US air travel market becomes first and foremost apparent given that domestic mainline and regional capacity combine for a total of approximately 60% of Delta’s entire capacity.

As one of three major US legacy carriers that went into bankruptcy after 9/11 and emerged out of it, Delta has maintained a substantial market share on domestic flights for years. The merger with Northwest Airlines back in 2010 created what was then the largest commercial airline in the world and solidified Delta’s competitive position inside the United States as it pushed domestic market share measured in revenue passenger miles (RPM)12 up by over six percentage points to 16.6%. Since then Delta’s market share has remained relatively steady. Measured by the share of all domestic flights in the United States Delta’s market share in 2015 was 10.85%, a year-on-year increase of about 1% and more than a doubling of the share registered in 2009. Due to their deteriorating financials and competitive positioning inside the United States, further domestic carriers were forced to consolidate, which led to the merger of United Airlines and Continental Airlines in 2012 and the merger of American Airlines and US Airways in 2015, raising the market shares of the two newly created companies to just over 16%. Another major competitor for Delta is Southwest Airlines, one of the top low-cost carriers in the country, which increased its market share by almost 5% within six years to become the market leader as measured by RPM. Other important players in the market are JetBlue Airways, SkyWest Airlines and Alaska Airlines, the latter

12 RPM are the number of revenue-paying passengers per reporting period multiplied by the number of miles they have

been transported during the period. A synonym for RPM is traffic.

Operator No. of routes Pct. of total

Delta Air Lines 1,336 65.11% Westjet 37 1.80% Westjet Encore 4 0.19% KLM 31 1.51% Transavia 0 0.00% Alitalia 14 0.68% Air France 34 1.66% Virgin Atlantic Airways 32 1.56% Air Europa Lineas Aereas 4 0.19% Aeromexico 40 1.95% Aerolineas Argentinas 4 0.19% Korean Air Lines 12 0.58% Virgin Australia International 4 0.19% China Southern Airlines 8 0.39% China Eastern Airlines 11 0.54% China Airlines 4 0.19% Delta Connection

SkyWest 463 22.56% Endeavor Air 451 21.98% Expressjet 441 21.49% Shuttle America 93 4.53% Compass Airline 146 7.12% Gojet Airlines 179 8.72% Aeromexico Connect

Aerolitoral 21 1.02%

Selected Operators

Only Delta Air Lines 889 43.32% Only Third Party Carriers 716 34.89% Total Third Party Carriers 1,163 56.68% Only Delta Connection 522 25.44% Only Air France-KLM-Alitalia 46 2.24% Only Equity Investments 65 3.17%

Table 1: In and outsourcing of Delta’s October/November route network

DELTA AIR LINES,INC. COMPANY REPORT

of which endeavors to become the fifth largest US airline by the time its merger with Virgin America has been completed. Not only since 2009 has consolidation been a major trend for the airline industry. This may be demonstrated by the fact that on routes within the United States the major 13 domestic carriers combined for a total market share of 88.41% in 2015 after a mere 64.81% in 2009. Another metric proving the significant market concentration in the United States is the Herfindahl-Hirschman-Index (HHI). Considering the 13 biggest carriers’ market shares on domestic flights, the HHI rose from 641.22 in 2009 to 1,165.05 in 2015. Above an HHI of 1,000 a marketplace can no longer be characterized as entirely competitive but moderately concentrated. Less competition has had a lasting positive impact on US airlines’ capacity utilization and bottom lines.

Further analysis shows that Delta Air Lines operated 75.73% of its 2015 total of 875,000 domestic flights out of 29 major US airports. This share has gradually decreased since 2009 when it amounted to 79.35%, which suggests that Delta has been diverting to smaller, less-congested airports in an effort to save on fees for airport slots and reduce overall costs. Almost 55% of the 875,000 flights were executed through Delta’s seven major hubs Atlanta, Minneapolis-St. Paul, Detroit, Salt Lake City, Los Angeles as well as both major New York airports JFK and LaGuardia. Hartsfield-Jackson alone services around 28% of all domestic flights, which bears enormous risk in light of the recent power outage at the airport in August 2016 causing multiple delays and cancellations throughout Delta’s entire network. Compared to United Airlines and American Airlines, Delta had less exposure to the 29 major US airports in 2015 and therefore less operational risk as United operated 85.9% and American 82.82% of its entire domestic flights through those airports. However, Southwest Airlines only made 53.38% of its domestic departures from one of the airports in question which is not surprising given the low-cost business model and the point-to-point transit model Southwest Airlines is practicing.

As highlighted by the map in Figure 13 below, which shows Delta’s 2015 market shares on domestic flights at the 29 biggest airports, the airline hassubstantiated a strong market position in the southeastern and mid-western United States. Its top domestic routes, as measured by number of enplaned passengers between October 2015 and September 2016, are listed in Figure 12. The merger with Northwest Airlines back in 2010 has helped Delta to almost double the market share on domestic flights in its southeastern hub Atlanta. Its local market share rose from 34% in 2009 to 62% in 2015. In the same time span Delta achieved even steeper market share gains of 30% or more on domestic flights in Salt Lake City as well as on domestic and international flights in Detroit and Minneapolis-St. Paul.

Source: US Bureau of Transportation

DELTA AIR LINES,INC. COMPANY REPORT

More moderate increases between 5% and 10% were recorded on domestic flights in Los Angeles, New York JFK, New York LaGuardia, Seattle/Tacoma and Tampa and on international flights in Boston, Los Angeles and Portland.

Figure 13: Delta’s market share on domestic flights at 29 major US airports. (Source: US Bureau of Transportation)

Considering domestic as well as international flights, Delta had a total market share above 15% at five out of the 29 major US airports. These were Atlanta (57.95%), Minneapolis-St. Paul (33.11%), Detroit (30.57%), Salt Lake City (30.5%) and New York-JFK (18.77%). Furthermore, Delta was among the top five airlines in terms of market share at 23 out of the 29 major airports. Only at airports in San Diego (6.93%), San Francisco (5.14%), Newark (3.16%), Denver (2.8%), Chicago O’Hare (1.77%) and Houston (1.31%), Delta had insignificantly small operations.

Since 2014 the price environment in the United States has been presenting domestic airlines with a big challenge. Average round-trip airfares in the United States have dropped tremendously from 2015 to 2016, as pointed out in Figure 14. While an average itinerary fare, which corresponds to the ticket price charged by the airline plus any additional taxes and fees surcharged by outside entities, cost $392 in 2014, travelers had to pay only $377 in 2015 and $361 in 2016. Intense price wars throughout the US airline industry have contributed to an overall decline in revenues per available seat mile (RASM)13, yields and carriers’ load factors. In

2015 Delta Air Lines faced a slight drop in mainline unit revenues of 0.64% after recording strong growth numbers in this segment between 2009 and 2014. However, considering that from 2014 to 2015 unit revenues were down 3.01% for all of its mainline operations and 3.35% for its entire system, the decline in

13 RASM is the revenue generated on each available seat mile. It is also known as unit revenue. Figure 14: Annual US domestic average

itinerary fare in constant 2016 USD

Source: US Bureau of Transportation

Alaska Airlines American Airlines Delta Air Lines Haw aiian Airlines United Air Lines

Allegiant Air Envoy Air

ExpressJet Airlines Frontier Airlines JetBlue Airw ays SkyWest Airlines Southw est Airlines Spirit Airlines Virgin America

N

et

w

or

k

C

ar

rie

rs

V

al

ue

C

ar

rie

rs

Source: Analyst’s Composition

DELTA AIR LINES,INC. COMPANY REPORT

domestic unit revenue does not seem that significant. Unit revenues were down mainly due to weaker yields. Our analysis includes average domestic itinerary fares that were paid at around 384 airports throughout the United States between the third quarter of 2013 and the second quarter of 2016. These data show that the aforementioned major 29 US airports were particularly affected by the changing yield environment as ticket prices dropped by 4.43% during the period of observation while the remaining 355 airports actually experienced an increase of 2.86%. In view of Delta’s strong reliance on the 29 airports it is understandable that the company’s domestic unit revenues have been under enormous pressure. Chicago O’Hare, Miami, Dallas, Fort Lauderdale and Houston recorded price drops of 7% or more, whereas airports such as Baltimore, Boston, New York-JFK, San Francisco or San Diego incurred only minor drops of up to 2% and were able to compensate to some degree.

In the United States, Delta faces competition from two groups of carriers. The first group consists of network carriers such as Hawaiian Airlines, Alaska Airlines, American Airlines or United Airlines. The latter two, also referred to as legacy carriers, show the highest resemblance with Delta Air Lines’ revenue and cost structure or size of operations. On top of that they operate their individual route networks via the same hub-and-spoke approach as Delta, allowing them to efficiently serve an extensive network of airports across the country. The second group comprises value or low-cost carriers (LCCs) such as JetBlue Airways, Southwest Airlines or SkyWest Airlines or even ultra-low-cost carriers (ULCCs) such as Spirit Airlines or Allegiant Air. Unlike their hub-and-spoke competitors, the second group of carriers has chosen a point-to-point transit model through which they serve a selective network of airports, usually limited to the most profitable routes. By flying to secondary, less congested airports, by reducing parking time on the ground, by employing just a few different aircraft types to lower training and maintenance expenses and through other measures, LCCs and ULCCs are able to substantially reduce operating expenses and undercut ticket prices of network carriers. Figure 15 lists the group of network and value carriers that were subject to our competitive analysis.

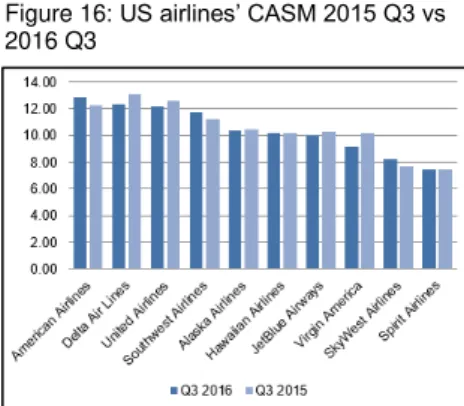

Our analysis of unit revenue, cost and profitability metrics reveals a significant difference between Delta Air Lines and other US network and value carriers. In the third quarter of 2016 our sample of network carriers averaged costs per available seat mile (CASM)14 of 11.56 cents (2015 Q3: 11.72 cents). The average CASM for

our sample of value carriers was 9.59 cents (2015 Q3: 9.8 cents). In spite of

14 CASM is the amount of operating expenses that an airline incurred per available seat mile during a certain reporting

period.

Figure 16: US airlines’ CASM 2015 Q3 vs 2016 Q3

Source: Company Data

Source: Company Data

Figure 17: US airlines’ unit fuel costs 2015 Q3 vs 2016 Q3

Source: Company Data

DELTA AIR LINES,INC. COMPANY REPORT

network carriers’ cost reduction efforts, the unit cost gap between network and value carriers had actually increased from 1.92 cents to 1.97 cents per available seat mile. In both observation quarters Delta Air Lines had the highest unit costs of our nine sample US carriers. However, it also generated the highest operating margin in absolute and relative terms, as measured by the difference between RASM and CASM. What is remarkable for investors is that Delta’s third quarter margin of 30.65% exceeded the operating margins of legacy carrier rivals American Airlines (13.51%) and United Airlines (16.35%) by far. Figure 16 to Figure 22 provide more detail on the competitive analysis.

Outlook:

We anticipate Delta Air Lines to keep domestic capacity expansion for 2017 and 2018 in range of 2% to 4%, with the majority of this expansion coming from mainline flights. Capacity of its regional Delta Connection partners is forecasted to decrease further in 2017.

Latin America

As of October 2015 Latin America and the Caribbean were the smallest of the five major world regions, with a mere 7% of the world’s capacity in ASM. Between October 2014 and October 2015, ASMs were up 5.2% year-on-year. This was primarily due to a 2.4% growth in departures and a 4.6% growth in average seats per departure. The fact that over the same time interval capacity within the region outgrew capacity to other world regions (5.8% vs 4.4%) suggests that Latin American/Caribbean markets are far from being saturated. However, according to demographic and economic indices the Latin American region lags behind other parts of the world. GDP per capita growth since 2012 was only 2.2% and thus the slowest of the five major world regions. Also compared to the almost 2,000 aircraft that North American airlines have ordered until 2020, Latin American/Caribbean airlines have only placed orders for 563 aircraft.

Given the local proximity of individual markets and long-term potential for air travel from the United States to this region and vice versa, Latin America is one of the cornerstones of Delta’s international expansion strategy, even though the current economic uncertainties and political change in many Latin American countries dampen expectations and create some headwind for air travel revenues.

As of October/November 2016, Delta’s entire network of 2,052 routes included 203 routes connecting Latin American/Caribbean and other domestic or international destinations, which corresponds to roughly 10% of the entire route network. Mainline flights to and from Latin America have contributed a little over 7% to Delta’s total passenger revenue in the first nine months of 2016. This is roughly Source: Company Data

Figure 19: US airlines’ other unit costs 2015 Q3 vs 2016 Q3

Figure 20: US airlines’ CASM ex 2015 Q3 vs 2016 Q3

Source: Company Data

Figure 21: US airlines’ PRASM 2015 Q3 vs 2016 Q3

Source: Company Data

Figure 22: US airlines’ operating margin 2015 Q3 vs 2016 Q3

DELTA AIR LINES,INC. COMPANY REPORT

2% more than what had been contributed by the Latin American mainline segment back in 2009, but slightly less than in 2015.

Since 2013 Delta Air Lines has slightly raised its capacity on mainline routes to and from Latin American destinations from 7.75% to 9.09% of total system capacity as recorded after the first three quarters of 2016. Regional capacity to and from the Latin American region more than doubled since 2013, although by the end of the third quarter of 2016 it merely represented 0.28% of total system capacity. Mainline and regional capacity combined the Latin American region has gained almost 2 percentage points in Delta’s total network capacity since 2013. Capacity utilization in the mainline and regional segment has improved during the first three quarters of 2016.

Joint ventures and equity stakes have lined up some promising growth potential for Delta Air Lines in the Latin American region. Its equity stakes in Aeroméxico and Gol Linhas Aéreas provide Delta with long-term income and a foothold both in Mexico and Brazil, which the Atlanta-based carrier regards as particularly important. Pending antitrust immunity, which was expected to be granted by the US Department of Transportation by the end of 2016, the airline will invest another $815 million in Aeroméxico and increase its stake to 49%. This will make Delta the dominant foreign carrier in Mexico and bring a sizable revenue boost. Open skies agreements between the United States and Mexico have been ratified in late August 2016 and Delta’s US Mexico scale is expected to triple through the joint venture. Moreover, Delta is looking into increasing its current stake of 9% in Gol Linhas Aéreas or buying the financially struggling airline altogether, provided the Brazilian government raises its foreign ownership limits on airlines. Despite Brazil’s recent political and economic woes, the country is still regarded as one of Latin America’s most vibrant regions, with the Summer Olympics in 2016 having initiated another surge in travel demand. After 16 consecutive quarters with negative year-on-year growth, Brazil’s unit revenues increased 30% during the third quarter of 2016. The strengthening Real has raised point-of-sale demand in Brazil.

Outlook:

Capacity in Latin America is expected to remain flat in 2017 and 2018 as Delta aims at optimizing its unit revenues before adding further capacity to the region.

Atlantic

DELTA AIR LINES,INC. COMPANY REPORT

Air travel service across the Atlantic is regulated through Open Skies agreements between the United States, Canada and the European Union, which allows airlines to enter and exit almost every transatlantic market. On the part of the United States, the only airlines offering transatlantic flights are the three legacy carriers Delta Air Lines, American Airlines and United Airlines, each of which has its own revenue sharing joint venture or strategic alliance with a European airline which helps to efficiently operate this long-haul region. Delta collaborates with its Skyteam partners Air France/KLM, American Airlines cooperates with its Oneworld partner British Airways/Iberia and United Airlines has partnered up with its Star Alliance co-member Lufthansa. Along with Air Canada, which is also part of Star Alliance, the three US legacy carriers and their European partners offer more than 82% of daily flights across the Atlantic.

For several quarters the transatlantic region has been subject to overcapacity as well as decreasing yields and unit revenues. In the third quarter of 2016 alone Delta’s unit revenues declined by 9.7% year-on-year.

Between January 2016 and September 2016 the Atlantic region accounted for slightly over 20% of Delta’s total system capacity, making the region a strategic gateway to Europe and Africa.

This was the result of a variety of macroeconomic, sociological and competitive forces. There has been a lot of economic uncertainty within the European Union, ultimately depressing economic growth as well as discretionary income available for travelling. Amongst others this was the result of aggressive capacity expansion by Middle East carriers, the continuous emergence of new, primarily European low-cost competitors, economic uncertainties and an overall sluggish demand in the wake of the Brexit as well as travelers’ growing fear of terrorist attacks.

The airline industry

Five forces

In accordance with Porter’s strategic analysis framework, Delta Air Lines’ domestic as well as international operations are subject to five forces, each of which has a unique significance for the strategic alignment of Delta Air Lines. The five forces are competition, industry entry and exit, availability of substitutes or complements, supplier power and buyer power.

DELTA AIR LINES,INC. COMPANY REPORT

Both on domestic and international routes, Delta Air Lines finds itself exposed to significant competitive pressure, as multiple other carriers compete with a largely undifferentiated service for the same customer base and on mostly identical routes. In the US the Airline Deregulation Act of 1978 removed government control over air fares, routes as well as market entry and exposed US airlines to larger competitive constraints, which narrowed profit margins considerably.

In international markets, such as Europe, South East Asia or the Middle East, Delta experiences similar competitive forces, although these are often times the result of excessive government intervention. In the Gulf region, for example, the amount of government subsidies received by carriers such as Emirates, Etihad and Qatar Airways, makes it especially difficult for foreign carriers to compete on prices. This is regarded as a violation of multilateral open skies agreements, which are supposed to liberalize the regulation of international aviation, minimize this sort of government intervention and guarantee a free-market environment.

Furthermore, the competitive landscape for Delta Air Lines is influenced by other aspects of the airline industry, such as socioeconomic or technological dynamics. One example is the surge of online travel agencies over the past 20 years, which capitalized on the fact that customers became less loyal to certain airlines and that the price elasticity of their demand for air travel increased greatly. The internet raised transparency for travelers and enabled them to meticulously compare prices, which needless to say intensified price competition between carriers.

Industry entry and exit

The airline industry has high entry barriers since carriers require an extensive amount of capital to cover fixed costs from investments in aircraft, ground equipment and other property, as well as variable costs from purchasing jet fuel, employing staff or paying airport fees. Economies of scale, from spreading fixed costs over a greater capacity, optimizing load factors or entering into code-sharing agreements, provide a significant cost advantage for established carriers such as Delta Air Lines and further strengthen barriers to enter the airline market. Another considerable industry entry barrier is the availability of airport slots15, which are

kind of a precious commodity at certain highly congested airports and which may be locked into long-term contracts and would have to be acquired directly from other carriers. Hence emergent airlines are often forced to depart from and arrive at remote airports during off-peak times.

DELTA AIR LINES,INC. COMPANY REPORT

Exit from the airline industry is also a complicated endeavor since it requires carriers to liquidate their tangible and intangible assets in addition to fulfilling existing passenger reservations. The complexity of a complete industry exit drove several major US airlines over the course of the past 15 years to enter Chapter 11 bankruptcy protection, reorganize and eventually reemerge.

Substitute and complement products or services

Instead of taking a plane, business and leisure travelers in the US can use one of several alternative means of travel, such as train, car or bus. Given the sheer size of the country, however, viable substitutes for long distance air travel are rather scarce. Although the US has an interstate rail system, it lacks high-speed trains, which makes long distance journeys via train less economical than by plane as they take far longer. In spite of a low-fare bus transportation, Delta and other US airlines still offer a better value for money on long-haul journeys. This is not the case for short distances of up to 250 miles, for which trains, cars and buses are usually the preferable means of transport not only cost-wise but also with regards to travel time. Because of the strict security procedures at airports, people are typically better off travelling by land for short distances. Those airlines, whose majority of flights are short haul, are naturally at a higher risk of substitution should they decide to increase their prices. For Delta this is only a medium threat given the expansion of its domestic route network.

High net-worth or business customers might even substitute commercial air travel by chartering jets, which seems more attractive in light of fractional-ownership programs as well as a more comfortable pre-boarding and flying experience. The continuous development of telecommunications constitutes another relevant substitute to air travel, particularly for business travelers. Fiber optic networks and high-speed internet allow corporations to increasingly conduct business meetings via video conference and reduce corporate travel expenses. This is especially bad for legacy carriers, for which first-class seating is a pivotal part of their pricing strategy, as first-class travelers essentially overpay for the service received and thereby boost overall passenger yields.

DELTA AIR LINES,INC. COMPANY REPORT

by land. Bilateral complements are products and services offered outside air travel. These can be hotel stays, car rentals or other things business and leisure travelers demand. There is a reciprocal relationship between air travel and bilateral complements. A reduction in ticket prices is likely to stimulate air travel and increase the demand for bilateral complements, while a drop in prices of these travel-related goods and services can have the same effect on the demand for air travel.

Supplier power

Delta Air Lines requires the supply of jet fuel, labor and aircraft in order to run its business. In view of the importance of these input factors for the sake of smooth airline operations and their share of total operating expenses, supplier power is a significant force inside the Porter framework.

The price of kerosene is closely linked to the changes in global supply and demand of crude oil. As a result, airlines are sensitive to the volatile price movements of this commodity. An upwards or downwards change of one cent in the price of a gallon of jet fuel, has an annualized impact of $40 million for Delta Air Lines. About half of the global oil production is contributed by the Organization of the Petroleum Exporting Countries (OPEC), giving it comprehensive power over worldwide oil markets. In spite of the recent oversupply and the slide of crude oil prices, aircraft fuel still represents one of the largest cost items for Delta, second only to labor expenses. Compared to American Airlines or United Air Lines, however, Delta has more bargaining power in the purchase of kerosene. The Atlanta-based carrier had not only entered into numerous contracts to hedge against upwards shifts in oil prices, but also adopted more drastic measures in 2012, when the company purchased an old ConocoPhillips oil refinery located outside of Trainer, Pennsylvania. Although analysts and other industry experts feared that efficiently running a refinery would be impossible for an airline, since its core competencies clearly lie elsewhere, Delta has managed to redeem its initial capital investment of $150 million and be more independent from external supply of jet fuel.

DELTA AIR LINES,INC. COMPANY REPORT

unions to increasingly demand a fair compensation, with the Air Line Pilots Association’s recent request for a 40% pay increase until 2018 leading the way. Despite the significance of maintaining a sound employee morale as well as the need to prevent major work stoppages, an excessive increase in labor costs would constitute a big hit to Delta’s future earnings and subsequently its stock price. With regards to labor relations, legacy carriers such as Delta Air Lines are at clear disadvantage relative to LCCs or ULCCs which enjoyed non-unionization for years and still pay their employees comparatively less.

Delta and its rival carriers are confronted with an even bigger supplier power when it comes to purchasing aircraft. Boeing and Airbus virtually have a duopoly on large aircraft. As of December 31, 2015, both manufacturers combined for roughly 78% of Delta’s fleet, counting 809 aircraft. Boeing alone constituted a 58% share of the total. In addition to the lack of alternative, high-end aircraft manufacturers, the sole nature of the product gives Boeing and Airbus a favorable bargaining position. Aircraft are no mass-produced articles, but are rather manufactured and delivered on order, which including post-production testing can take up to three months. After all, these are products that have to meet the latest safety standards in air travel. The remainder of the air transport supply chain includes airports, which sell take-off and landing slots, ticketing facilities, boarding gates and operations areas to airlines. As the annual number of passengers travelling throughout the US and worldwide increases, airports will continue to become more congested and put a higher mark-up on their products and services.

Buyer power

DELTA AIR LINES,INC. COMPANY REPORT

online, so as to enhance transparency and aggravate the consumer’s search for the best deal even further.

Competitive analysis

SWOT analysis

Beyond Porter’s five forces framework, Delta’s competitive positioning may be specified by contrasting strengths, weaknesses, opportunities and threats.

Strengths

Delta Air Lines continues to post strong operational metrics, leading the industry in 2015 in terms of completion factor (99.6%), on-time rate (85.9%) and number of days with a 100% mainline completion factor (161) and making it the best legacy carrier by far. In only five years, Delta’s executives have managed to lead the airline to industry-leading operational metrics, after it had been rated one of the worst airlines in this department in 2010.

1 Strong operational metrics, eg. mainline completion factor and on-time rate, have improved customer satisfaction

1 International operations expose Delta to local ups and downs of the economy and particularly to foreign exchange volatility

2 Deleveraging has reduced risk of financial distress, decreased interest expenses and led to an investment grade rating by Moody's

2 Investors tend to be bearish about airlines especially from the US

3 Solid international revenues make Delta more stable in the event of a downturn of the US economy

4 Excellent maintenance facilities in Atlanta allow Delta to use older planes than competitors

5 Merger with Northwest Airlines has been realized with very little route overlap and has not destabilized Delta as opposed to the mergers of American and United

6 Historic net operating losses have wiped out Delta's tax obligations

1 Political upheaval and terrorist attacks may cause serious damage to Delta's operations and depress passenger demand and stock performance

1 Strategic alliances and equity stakes in international airlines promise further growth potential outside a rather mature domestic market

2 Medical hazards, such as the outbreak of highly infectious viruses may deter travelers from going to certain regions

3 Persistent increase of oil price to over $70 per barrel will have a deeply adverse impact on profits and cash flows

4 Stricter rules and regulations regarding the training of regional airline pilots may lead to increase in operating costs

STRENGTHS WEAKNESSES

DELTA AIR LINES,INC. COMPANY REPORT

In early February 2016 Moody’s upgraded Delta’s senior unsecured debt securities to Baa3, rewarding the company with an investment grade rating for its ongoing efforts to reduce net debt. Since 2009, management has slashed adjusted net debt by $10.3 billion. At the end of 2015 adjusted net debt amounted to a total of $6.7 billion and the company plans to reduce this number even further to $4 billion by 2020. The true value of reduced leverage and lower interest expenses will start to reveal itself once industry fundamentals, such as crude oil prices or interest rates, start to worsen as it puts Delta in more control of an industry downturn.

Another strength is the solid international revenue base of Delta Air Lines, which makes it less prone to economic downturns of the US market and receding consumer discretionary spending. In 2015 Delta generated approximately 32% of its total passenger revenue of $34.78 billion in foreign markets, with the Latin American region contributing 7%, the transatlantic region contributing 16% and the Pacific region contributing another 9%.

Delta has a strongly ROIC focused approach in managing its aircraft fleet. While American Airlines and United Air Lines have greatly modernized their fleets, Delta Air Lines has learnt from its pre-bankruptcy mistakes and spent considerably less on new aircraft. Delta’s cost advantage is amplified by the fact that, in spite of its fleet being on average older than American’s or United’s, it actually has a lower unit maintenance cost than the two rival legacy carriers. Also its mainline completion and on-time arrival results are better, which suggests Delta knows how to utilize its older aircraft efficiently and that its maintenance and repair facilities are performing well. Although new aircraft, such as the Boeing 787 Dreamliner, are known to be more fuel efficient than old models, Delta’s choice of older planes has saved a lot of capital expenditures. It also speaks for Delta’s economic sense that they purchase older planes which are less expensive.

Compared to its legacy carrier rivals American Airlines and United Air Lines, Delta has fully realized its cost and revenue synergies from merging with Northwest Airlines. The 2008 merger has combined Northwest’s presence in Asia with Delta’s strong performance in Latin America and Europe. While Delta’s merger integration risk is retired, United is still wrapping up the merger with Continental and lags Delta in terms of operating margin. American is still highly leveraged after merging with US Airways in 2013.

Weaknesses

DELTA AIR LINES,INC. COMPANY REPORT

dollar against several other currencies, that Delta had economic exposure in, created major headwinds as it lowered non-US dollar earnings after translating them back into US dollar. In the fourth quarter of 2015 alone, the headwind accounted for $160 million in loss of revenue.

In light of the company’s bankruptcy in 2005 as well as the general airline industry’s longstanding plight, investors are still highly pessimistic on Delta’s stock. That being said, a lot of issues, such as capacity growth, fuel prices or union demands make airline stocks in general a lot riskier than other stocks. Like its network carrier rivals, Delta Air Lines is strongly undervalued compared to average industrials or transportation stocks and remains haunted by the past industry mistakes.

Opportunities

Joint ventures and equity stakes have lined up some promising international growth potential for Delta Air Lines. Equity stakes in airlines, such as Aeroméxico, China Easter, GOL or Virgin Atlantic, provide Delta with long-term income and a foothold in regions, which the Atlanta-based carrier regards as strategically important. Furthermore, these investments diversify Delta’s financial exposure to different regions and currencies. Further joint ventures with China Eastern (3%), Virgin Atlantic (49%) or Air France/KLM have firmly established Delta Air Lines on Atlantic and Pacific routes, without incurring the expenses of organic expansion.

Threats

Political upheaval as well as terrorist attacks have the potential to do serious damage to Delta’s operations as the carrier may temporarily need to cancel flights to certain affected regions, as experienced in the case of Brussels, or travelers may switch to other means of transport as they lose confidence in the safety of air travel. The spreading of ISIS and other extremist groups will continue to pose a big threat.

The outbreak of highly infectious viruses, such as Ebola or Zika, can negatively impact Delta’s operations as travelers may deter from going to certain regions. However, these medical risks may rather shift leisure travel to other regions or markets than end it completely.

DELTA AIR LINES,INC. COMPANY REPORT

China increased its crude oil imports, OPEC is negotiating an output freeze and also the US crude oil production in major shale regions has dropped.

Stricter rules and regulations regarding minimum training hours as well as deeper labor issues on working hours, compensation and retirement led to massive pilot dropouts at regional airlines, which adversely affects not only their own operating costs, but also represents a big threat to larger carriers, such as Delta Air Lines. Delta depends on mid-sized carriers to serve rural passengers and feed them into their network.

Risks to the investment thesis

Investing in Delta Air Lines is subject to a variety of company internal risks as well as external risks linked to the airline industry or other macroeconomic variables.

External risks

A major source of risk for the entire airline sector is the cost of crude oil and thus the price for aircraft fuel. While fuel prices have remained relatively flat during the 1990s, they experienced a steep rise from the beginning of the new millennium onwards until they peaked in the first half of 2012. Since then they gradually declined to lower levels. The volatile nature of oil prices and the fact that aircraft fuel expenses represent a material cost component for every carrier, put operating results at substantial risk. Even though most airlines hedge against a future upwards shift in the oil price, sudden price jumps can still severely impair the operating business of airlines as they may not be fully able to pass along higher fuel costs to customers, particularly those that purchased their tickets well in advance.

Not only since the events of September 11, 2001, have geopolitical conflicts and potential terrorist attacks posed a significant threat to the demand for air travel across the globe and reinforced the necessity to implement stricter security measures at airports and airlines alike. As a consequence, the operating business of many airlines has been adversely affected by sharp increases in security costs and selective, yet mostly temporary decreases in revenues. The attacks witnessed in Paris, Istanbul and Brussels in late 2015 and early 2016 respectively, demonstrate the still omnipresent threat of terrorist activities to the aviation industry in general.

DELTA AIR LINES,INC. COMPANY REPORT

the willingness to travel to certain regions of the earth and travel restrictions can adversely impact airlines’ operating results.

Internal risks

Unlike American Airlines, Delta Air Lines has been hedging the upside of oil price movements. Although these hedging activities aim at reducing the risk of adverse oil price movements, the mere rebalancing or mark-to-market adjustments of the hedge portfolio may require Delta to post a significant amount of margin on short notice and heavily dip into its cash holdings.

The main purposes of Delta’s non-controlling investments in as well as its joint ventures and strategic alliances with other airlines, are to broaden the global network, achieve revenue or cost synergies and to make a reasonable return on investment. However, these commercial relationships expose Delta Air Lines to potentially improper business behavior or non-compliance with laws and regulations by their partners and any service disruptions or reputational damages associated with it.

The solvency of Delta Air Lines relies on the continuous guarantee of credit facilities which require the company to hold a certain amount of liquidity or post collateral against the risk of default. A rapid decline in the value of collateral could adversely affect Delta’s credit rating across global equity and debt markets, lead to the reevaluation or even cancellation of credit agreements and accelerate a possible default.

As for any other labor intensive business, labor disputes or even strikes of certain employee groups may seriously disrupt operations and bring about financial losses for Delta Air Lines. The fact that approximately 18% of Delta’s staff was unionized at the end of 2015 underlines the great risk involved in labor relations. Another labor-related risk is the turnover of senior management or crucial members of staff without finding adequate replacements which may impact business in the short, medium and long run.

DELTA AIR LINES,INC. COMPANY REPORT

Financial outlook

Dividend policy

As Delta’s management repeatedly said in the past, the company will stick to its strategy of returning large amounts of cash to shareholders. In May 2015, management announced to return $6 billion in cash to shareholders until end of 2017. Legacy carriers such as Delta, American or United have had a long history of not paying any dividends at all, until Delta reinstated its dividend in 2013, followed suit by American in 2014. Unlike American, however, Delta did not keep its dividend constant but increased it from a quarterly 3 cents in 2013, to 7.5 cents in 2014 and 11.25 cents in 2015. In expectation of lower-for-longer oil prices, solid earnings, decreasing debt levels and strong cash flows, I forecast Delta to further boost its quarterly dividend, although more conservatively than in the last two years, and endeavour to portray itself as a dividend growth stock.

Beyond increasing its dividends, the Atlanta-based carrier will continue to buy back shares on a massive scale. Of the $6 billion in cash, which shareholders were promised until the end of 2017, Delta plans to buy back equity in the amount of $5 billion. Since introducing dividend payments in 2013, Delta has reduced its outstanding shares from 856.6 million to 736.4 million at the end of 2016. Share buybacks have three major advantages over dividends. First of all, by reducing outstanding shares they raise the dividend per share without actually increasing total dividend distribution. Second of all, they continue to be a cheap form of shareholder compensation while the stock trades at such a large discount to average industrials or transport stocks. Third of all, they leave Delta more room for manoeuver than committing to a fixed dividend payment.

Valuation

Delta Air Lines is projected to change its debt-to-equity ratio to 22% until 2025. Since the leverage of Delta, American and United differs greatly from the leverage of LCCs, it does not make sense to include the latter in the target capital ratio. Based on this assumption, the WACC approach will value Delta’s free cash flows until perpetuity.

WACC approach

Figure 23: Daily Yields 30 Year USDELTA AIR LINES,INC. COMPANY REPORT

The underlying valuation model assumes Delta Air Lines is part of a group of industry peers, composed of both legacy carriers and LCCs. Although the LCCs in the peer group16 have a different capital structure, their systematic risk is

comparable to that of legacy carriers. The cost of equity is calculated through application of the CAPM. I assume the risk free rate to correspond to the yield on 30-year US Treasury bonds, which as of December 30, 2016 was 3.06%. Figure 23 highlights 30-year US T-Bond yields since May 2011. The market risk premium is set at 5%.

Multiples

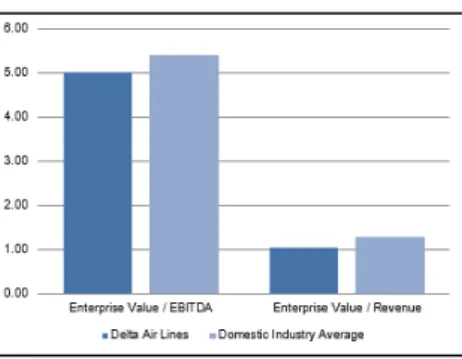

We considered several different ratios for a multiples valuation of Delta Air Lines and found the company to be largely undervalued compared to most of its domestic as well as international competitors. Figure 24 collates Delta’s enterprise value multiples with the arithmetic average of sample US network and value carriers mentioned before. Our analysis suggests that Delta is trading at a 6.83% discount (EV/EBITDA) respectively a 20.39% discount (EV/Revenue) to its industry peers. An even more precise valuation is provided in Figure 25 which compares Delta’s price earnings multiples with the averages of domestic as well as international airlines. According to forward price earnings ratios, Delta Air Lines is undervalued by 24.42% against domestic peers and 40.61% against a sample of international carriers, mostly from Asia.

The systematic undervaluation across different financial metrics substantiates investors’ generally pessimistic perception of Delta. Effectively the market is questioning Delta’s capability to continue to post the level of operating margins that it has for the last two years from 2017 onwards.

16 The LCCs analyzed are Southwest Airlines, JetBlue Airways, SkyWest, Alaska Air Group, Hawaiian Holdings and Spirit

Airlines.

Figure 24: Enterprise Value multiples Delta vs competitors

Source: Yahoo Finance

Figure 25: P/E multiples Delta vs competitors

Source: Morningstar

DELTA AIR LINES,INC. COMPANY REPORT

Appendix

Appendix 1

–

Audited (A) and Forecasted (F) traffic, capacity and

passenger load factors by regions

Domestic 2014A 2015A 2016F 2017F 2018F 2019F 2020F 2021F 2022F 2023F 2024F 2025F Traffic (RPM m)

Domestic 120,211 126,298 130,780 133,428 138,972 143,250 147,660 152,206 155,250 158,355 161,523 164,753

Domestic Mainline 98,844 105,455 109,949 112,716 117,224 120,741 124,363 128,094 130,656 133,269 135,935 138,653

Domestic Regional 21,367 20,843 20,832 20,712 21,748 22,509 23,297 24,112 24,594 25,086 25,588 26,100

Total System 202,925 209,625 213,089 214,639 219,234 223,173 227,769 232,512 236,398 240,357 244,389 248,496

Domestic 59.24% 60.25% 61.37% 62.16% 63.39% 64.19% 64.83% 65.46% 65.67% 65.88% 66.09% 66.30%

Domestic Mainline 48.71% 50.31% 51.60% 52.51% 53.47% 54.10% 54.60% 55.09% 55.27% 55.45% 55.62% 55.80%

Domestic Regional 10.53% 9.94% 9.78% 9.65% 9.92% 10.09% 10.23% 10.37% 10.40% 10.44% 10.47% 10.50%

Total System 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00%

Capacity (ASM m)

Domestic 141,128 146,899 153,338 156,394 162,908 167,930 173,108 178,446 182,015 185,656 189,369 193,156

Domestic Mainline 114,180 121,095 127,433 130,619 135,844 139,919 144,117 148,440 151,409 154,437 157,526 160,676

Domestic Regional 26,948 25,804 25,905 25,775 27,064 28,011 28,992 30,006 30,606 31,218 31,843 32,480

Total System 239,676 246,764 251,856 253,756 259,157 263,790 269,176 274,737 279,314 283,976 288,725 293,562

Domestic 58.88% 59.53% 60.88% 61.63% 62.86% 63.66% 64.31% 64.95% 65.17% 65.38% 65.59% 65.80%

Domestic Mainline 47.64% 49.07% 50.60% 51.47% 52.42% 53.04% 53.54% 54.03% 54.21% 54.38% 54.56% 54.73%

Domestic Regional 11.24% 10.46% 10.29% 10.16% 10.44% 10.62% 10.77% 10.92% 10.96% 10.99% 11.03% 11.06%

Total System 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00%

Load Factor

Domestic 85.18% 85.98% 85.29% 85.32% 85.31% 85.30% 85.30% 85.30% 85.30% 85.30% 85.30% 85.30%

Domestic Mainline 86.57% 87.08% 86.28% 86.29% 86.29% 86.29% 86.29% 86.29% 86.29% 86.29% 86.29% 86.29%

Domestic Regional 79.29% 80.77% 80.42% 80.36% 80.36% 80.36% 80.36% 80.36% 80.36% 80.36% 80.36% 80.36%

Total System 84.67% 84.95% 84.61% 84.58% 84.60% 84.60% 84.62% 84.63% 84.64% 84.64% 84.64% 84.65%

Latin America 2014A 2015A 2016F 2017F 2018F 2019F 2020F 2021F 2022F 2023F 2024F 2025F Traffic (RPM m)

Latin America 18,062 19,004 19,778 19,964 20,472 20,742 21,021 21,310 21,459 21,612 21,768 21,927

Latin America Mainline 17,690 18,587 19,232 19,361 19,748 19,945 20,145 20,346 20,448 20,550 20,653 20,756

Latin America Regional 372 417 546 603 724 796 876 963 1,011 1,062 1,115 1,171

Total System 202,925 209,625 213,089 214,639 219,234 223,173 227,769 232,512 236,398 240,357 244,389 248,496

Latin America 8.90% 9.07% 9.28% 9.30% 9.34% 9.29% 9.23% 9.16% 9.08% 8.99% 8.91% 8.82%

Latin America Mainline 8.72% 8.87% 9.03% 9.02% 9.01% 8.94% 8.84% 8.75% 8.65% 8.55% 8.45% 8.35%

Latin America Regional 0.18% 0.20% 0.26% 0.28% 0.33% 0.36% 0.38% 0.41% 0.43% 0.44% 0.46% 0.47%

Total System 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00%

Capacity (ASM m)

Latin America 21,725 22,966 23,297 23,547 24,154 24,477 24,812 25,159 25,340 25,524 25,711 25,903

Latin America Mainline 21,230 22,435 22,608 22,789 23,244 23,477 23,712 23,949 24,068 24,189 24,310 24,431

Latin America Regional 496 531 689 758 910 1,001 1,101 1,211 1,271 1,335 1,402 1,472

Total System 239,676 246,764 251,856 253,756 259,157 263,790 269,176 274,737 279,314 283,976 288,725 293,562

Latin America 9.06% 9.31% 9.25% 9.28% 9.32% 9.28% 9.22% 9.16% 9.07% 8.99% 8.91% 8.82%

Latin America Mainline 8.86% 9.09% 8.98% 8.98% 8.97% 8.90% 8.81% 8.72% 8.62% 8.52% 8.42% 8.32%

Latin America Regional 0.21% 0.22% 0.27% 0.30% 0.35% 0.38% 0.41% 0.44% 0.46% 0.47% 0.49% 0.50%

Total System 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00%

Load Factor

Latin America 83.14% 82.75% 84.89% 84.78% 84.75% 84.74% 84.72% 84.70% 84.69% 84.68% 84.66% 84.65%

Latin America Mainline 83.33% 82.85% 85.07% 84.96% 84.96% 84.96% 84.96% 84.96% 84.96% 84.96% 84.96% 84.96%

Latin America Regional 74.98% 78.55% 79.23% 79.56% 79.56% 79.56% 79.56% 79.56% 79.56% 79.56% 79.56% 79.56%

Total System 84.67% 84.95% 84.61% 84.58% 84.60% 84.60% 84.62% 84.63% 84.64% 84.64% 84.64% 84.65%

Atlantic 2014A 2015A 2016F 2017F 2018F 2019F 2020F 2021F 2022F 2023F 2024F 2025F Traffic (RPM m)

Atlantic 40,205 40,437 39,748 39,735 39,139 38,943 38,749 38,555 38,940 39,330 39,723 40,120

Total System 202,925 209,625 213,089 214,639 219,234 223,173 227,769 232,512 236,398 240,357 244,389 248,496

Atlantic 19.81% 19.29% 18.65% 18.51% 17.85% 17.45% 17.01% 16.58% 16.47% 16.36% 16.25% 16.15%

Total System 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00%

Capacity (ASM m)

Atlantic 47,566 49,096 49,249 49,298 48,559 48,316 48,074 47,834 48,312 48,796 49,284 49,776

Total System 239,676 246,764 251,856 253,756 259,157 263,790 269,176 274,737 279,314 283,976 288,725 293,562

Atlantic 19.85% 19.90% 19.55% 19.43% 18.74% 18.32% 17.86% 17.41% 17.30% 17.18% 17.07% 16.96%

Total System 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00%

Load Factor

Atlantic 84.52% 82.36% 80.71% 80.60% 80.60% 80.60% 80.60% 80.60% 80.60% 80.60% 80.60% 80.60%